Coinbase: Searching for the Next Cryptocurrency Catalyst

TechFlow Selected TechFlow Selected

Coinbase: Searching for the Next Cryptocurrency Catalyst

Bitcoin halving triggers bullish trend, but macro factors could impact the market.

Text by: David Han

Translation: Lynn, Mars Finance

At first glance, despite on-chain innovation reaching unprecedented levels—constructive for the sector in the long run—we believe macro factors may play a significant role in the near term.

Key Takeaways

-

While Bitcoin halvings have historically triggered bullish trends, these cyclical rallies are often accompanied by other ecosystem catalysts that provide additional momentum.

-

A growing talent pool, mature development tools, and improving blockchain scalability have made broader verticals catalysts this cycle, even though inbound liquidity channels appear to have shifted from risk financing to spot ETF inflows.

-

In the short term, we expect Bitcoin’s dominance to remain high as the broader macro environment becomes more risk-averse, and liquidity injected via ETFs is unlikely to rotate into higher-beta assets.

Beyond the Bitcoin halving, which we previously detailed, the market is now seeking new catalysts to sustain the rally that began in Q1 2024 following the approval of U.S. spot Bitcoin ETFs. Continued growth in stablecoin issuance and rising total value locked (TVL) in DeFi protocols suggest persistent strength in on-chain activity. Meanwhile, ongoing platform innovation at Layer 1 (L1) and Layer 2 (L2) levels, coupled with improved wallet tools enhancing user experience, form the basis of what we consider some of the most relevant narratives over the coming months.

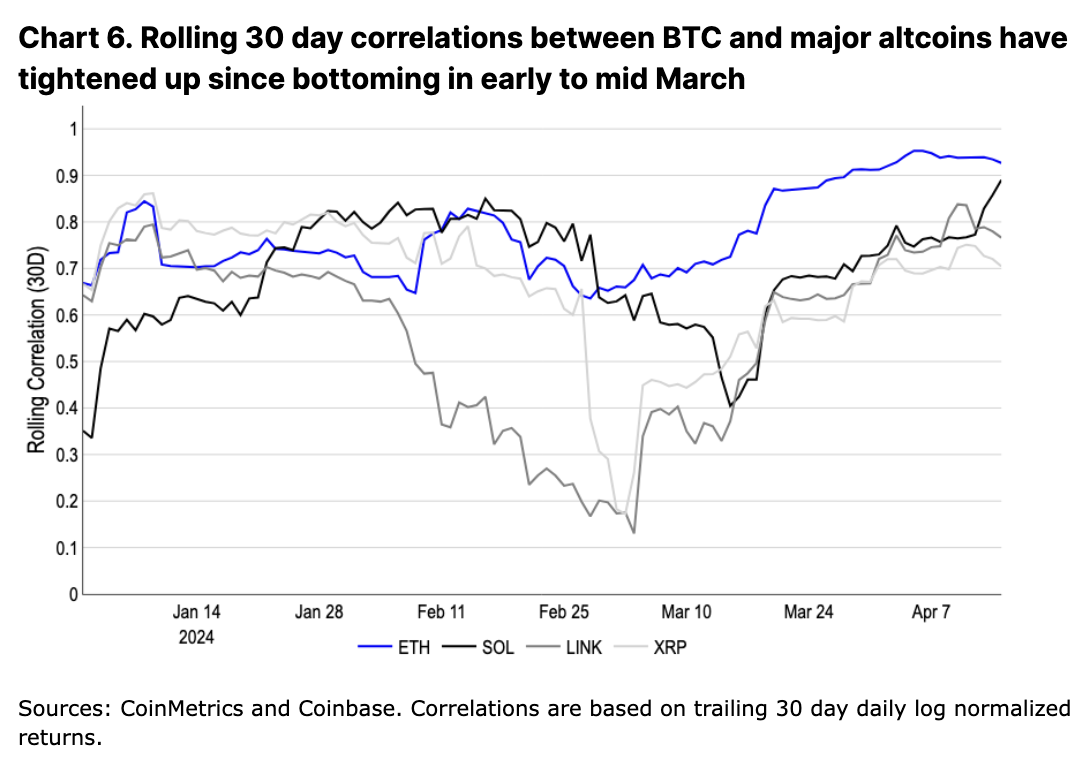

That said, we believe short-term movements will likely be driven more by macro factors, even as crypto fundamentals remain broadly strong. These are largely exogenous to crypto and include rising geopolitical tensions, higher long-term interest rates, reflationary pressures, and increasing national debt. Indeed, the recent rise in altcoin correlation with BTC underscores this point, highlighting BTC's anchoring role within the space as it solidifies its status as a macro asset.

While cryptocurrencies have historically been viewed primarily as risky assets, we believe Bitcoin’s sustained resilience and the approval of spot ETFs have created a bifurcated investor base (especially around Bitcoin)—one viewing it as a purely speculative asset, and another seeing it as “digital gold” and a hedge against geopolitical risks. We believe the growth of the latter camp partly explains the reduced drawdown magnitude observed so far in this cycle, given broader macro risks.

Post-Halving Patterns

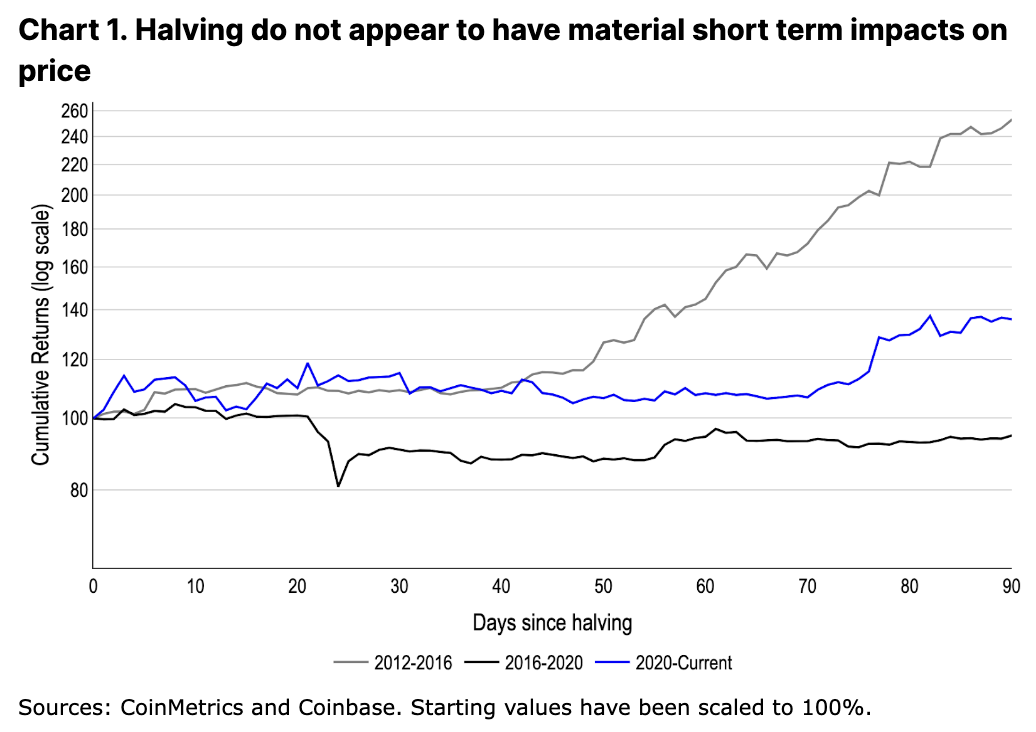

Previous halvings are typically seen as triggers for cyclical bull runs, although the immediate impact of a halving appears largely negligible in the short term. In fact, BTC fell 19% within a month after the 2016 halving and remained relatively flat for over two months post-halving in 2020 (see Figure 1). Similarly, we do not expect the upcoming halving to become an intense trading narrative, though we believe its relevance in flows has thus been overlooked—given BTC at $63,000, the halving equates to a reduction of $10.3B in annual BTC issuance, comparable to the $12.4B net inflow into U.S. spot BTC ETFs to date, offsetting a similar magnitude of BTC outflows.

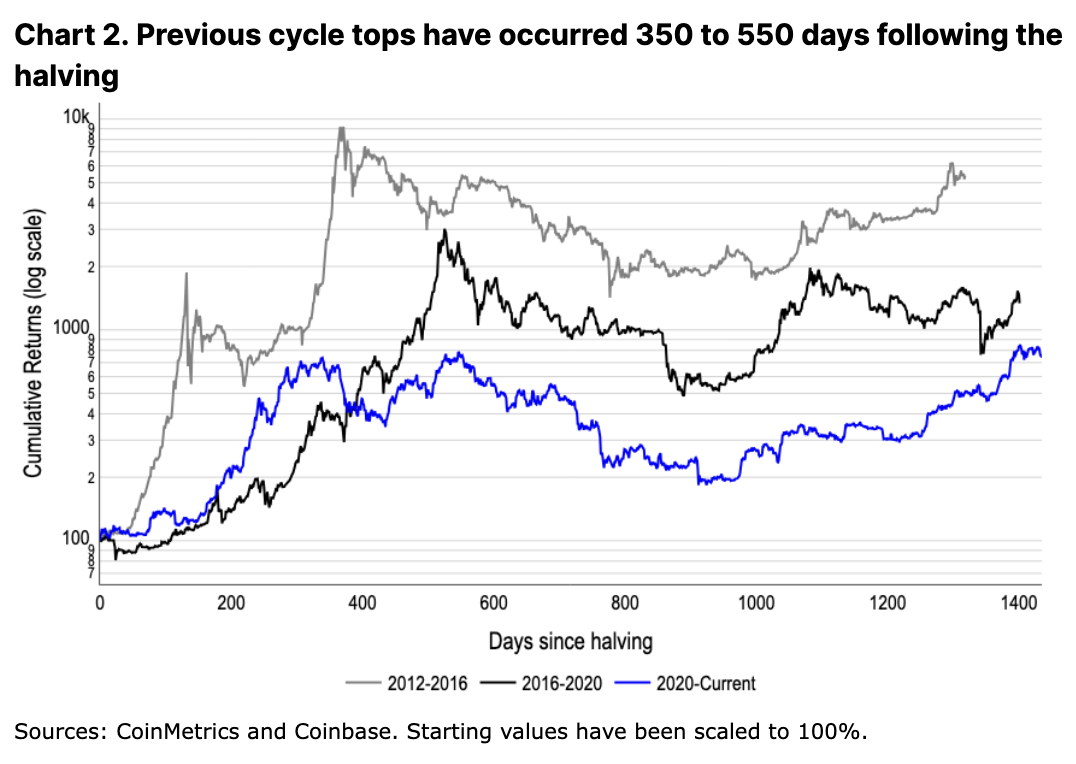

We believe, however, that increased access to a broader capital base through spot ETFs, combined with new supply-side dynamics, is structurally constructive for the asset class over the long term. Yet, if past cycles are any indication, this may take several months to fully materialize. Previous post-halving peaks occurred between 350 and 550 days after the event (see Figure 2), though this cycle already differs. With Bitcoin reaching all-time highs over a month before the halving amid spot ETF inflows, we expect further deviation from prior timing trends.

However, the halving benefits more than just Bitcoin. As the industry matures, constructive narratives across parallel crypto verticals often emerge following the halving. After the 2016 halving, the ICO boom carried market enthusiasm into 2017. Likewise, the 2020 DeFi summer launched the rise of decentralized applications (dApps) like Uniswap and Maker, initiating nearly two years of experimentation in DeFi primitives and other early-stage products.

Sources of Liquidity

With the emergence of new tools and use cases, the number of crypto verticals today has expanded tenfold. Blockspace has never been cheaper, and there has never been more to do on-chain. Social apps like Farcaster show promise for early adoption, while a range of well-designed blockchain games are beginning to launch. Wallet improvements allow developers to deploy smoother onboarding experiences, and DeFi primitives continue expanding into areas like liquid restaking and novel on-chain derivatives. Meanwhile, tokenization initiatives across financial products and jurisdictions are making significant progress, with growing overlap between on-chain finance and real-world off-chain assets. This is largely driven by the remarkable infrastructure buildup during the bear market.

We believe this could lead to a different pattern this cycle—one where more diverse sub-sectors perform strongly simultaneously (rather than concentration around one or two dominant themes). Particularly in a world where standalone applications (abstracting blockchain components from users) grow increasingly sophisticated, the gap between tokens and revenue models widens significantly. This breadth enables new forms of revenue generation previously inaccessible in earlier cycles. For example, BonkBot, a Telegram bot developed in collaboration with the BONK community, regularly generates over $100,000 in fees daily (with single-day fee revenue peaking at $1.4M).

We further believe that distinctions among crypto verticals this cycle may lead to more pronounced capital rotation between sectors. Indeed, early focus on AI projects, followed by excessive attention toward memecoins and restaking, has already shown signs of such rotation.

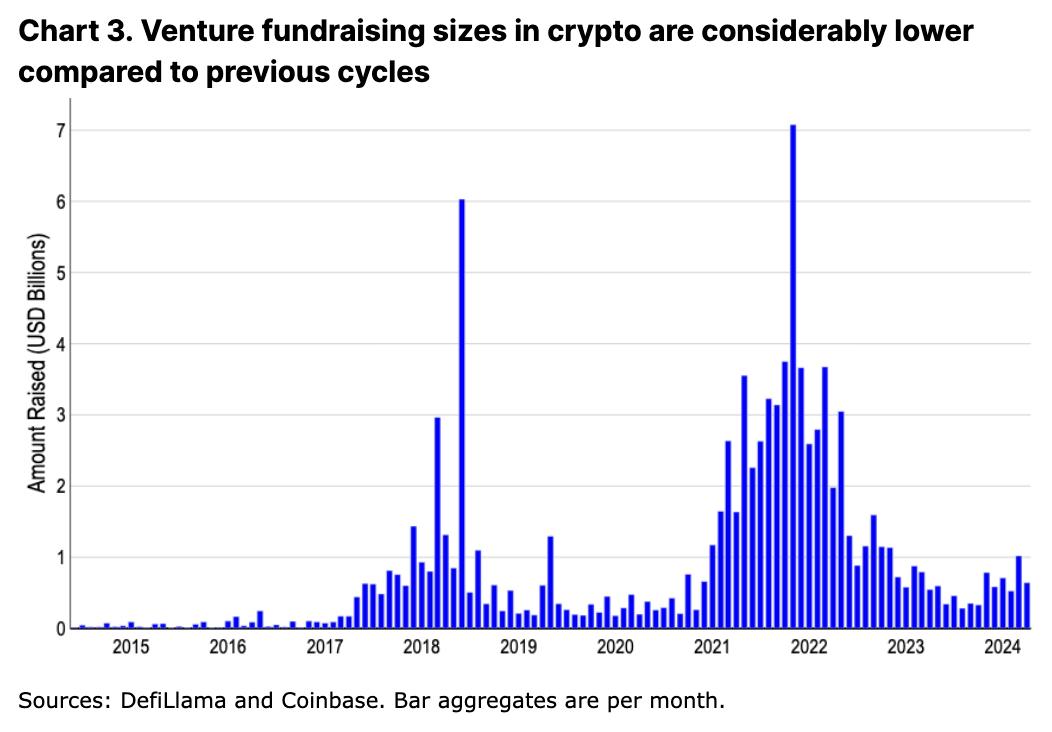

Declining levels of crypto fundraising—relative to prior cycles—support this view. It reduces a primary source of new liquidity for high-beta assets. Average monthly fundraising in 2024 remains below $1B, lower than even 2017–18 levels and only about a quarter of 2021–22 volumes. Reduced funding stems both from the severe aftermath of previous cycles and current macro headwinds. Private markets contracted broadly in 2023, with venture funds raising the lowest amount in six years—a 60% drop since 2022.

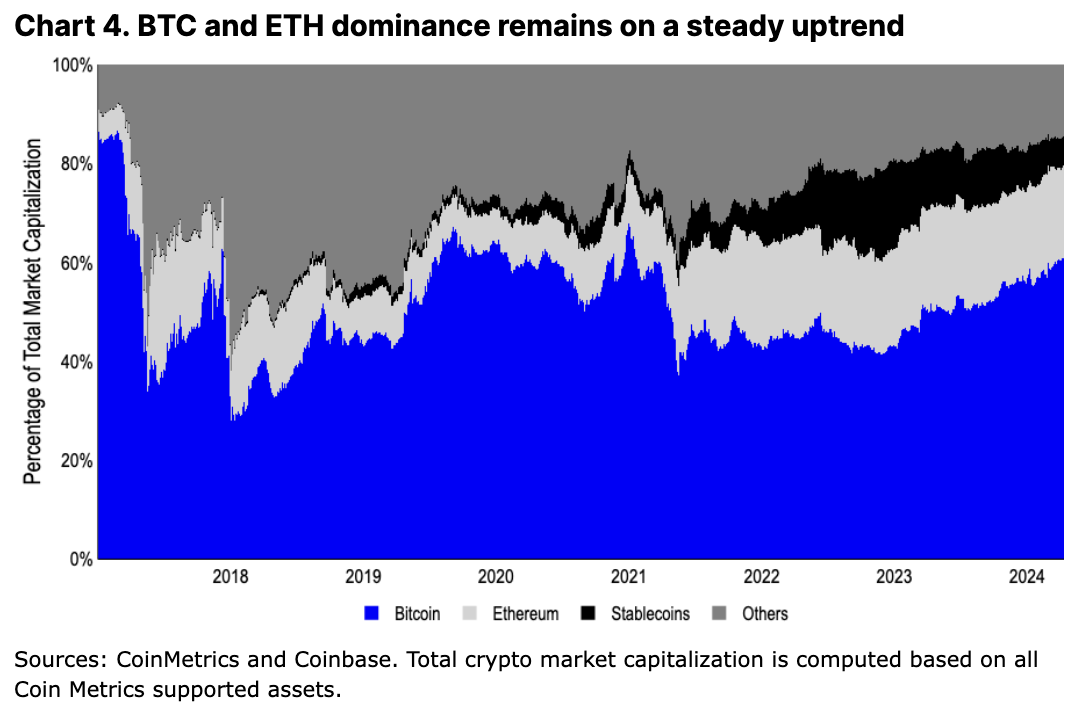

The relative lack of fundraising raises questions about how liquidity enters the space. Spot ETFs are undoubtedly one of the main channels, as we’ve previously discussed. They tap into a broader capital pool, including allocations from registered investment advisors (RIAs) and other managed funds. For instance, BlackRock has plans to include its spot Bitcoin ETF in global allocation funds. However, these inflows are limited to BTC (and possibly ETH in the future) and are unlikely to cascade further down the risk curve. If this market structure doesn’t change significantly, we expect Bitcoin’s dominance to remain elevated for the foreseeable future.

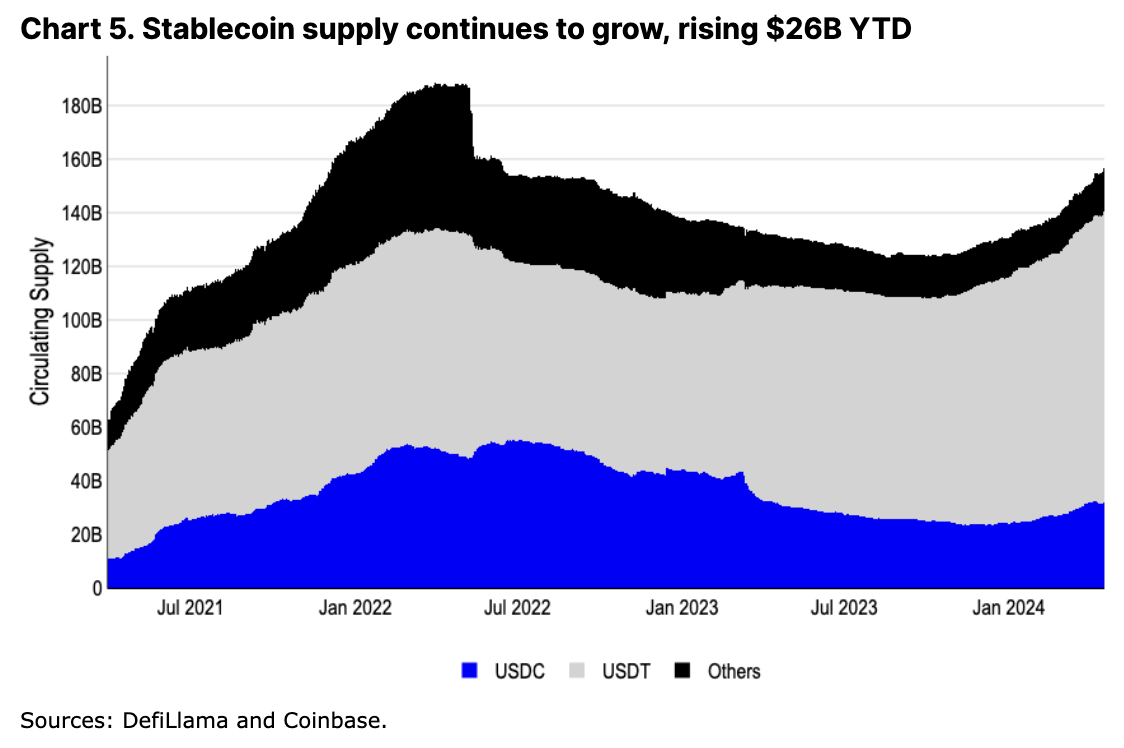

On the other hand, we believe the primary means (excluding leverage) of injecting liquidity into altcoins comes from net growth in stablecoins. Stablecoins account for roughly 65% of $2.6B in daily DEX trading volume and serve as trading pairs on many centralized exchanges (CEXs). Although total stablecoin market cap remains below its 2022 peak, USDC and USDT issuance has reached all-time highs and continues climbing. Adjusting for the now-defunct TerraUSD’s impact on total market cap, stablecoins collectively are actually nearing their prior highs.

Bitcoin Macro Outlook

While we anticipate rising endogenous crypto catalysts ahead, we believe macro conditions will play a more critical role in the near term. Indeed, in previous cycles, macro tailwinds were important—even potentially more impactful than native crypto catalysts. The 2012 halving occurred against the backdrop of the Fed’s QE program and the U.S. debt ceiling crisis. In 2016, Brexit and the contentious U.S. election likely sparked fiscal concerns in the UK and Europe. The early 2020 pandemic led to unprecedented stimulus, driving massive liquidity expansion.

We believe this cycle is no different—today’s macro environment is equally vital for Bitcoin and the broader crypto market. Following escalating Middle East conflicts, recent deleveraging has reset funding rates close to zero. Ongoing war along the Ukraine-Russia front and tensions in the South China Sea paint a globally uncertain picture. We believe rising global geopolitical significance within broader deglobalization and reshoring trends may be a defining macro feature of this cycle—especially in risk-off environments. After a period of unclear market direction, Bitcoin’s correlation with most other cryptos, which had decoupled during Q1 2024’s rally, has since consolidated upward.

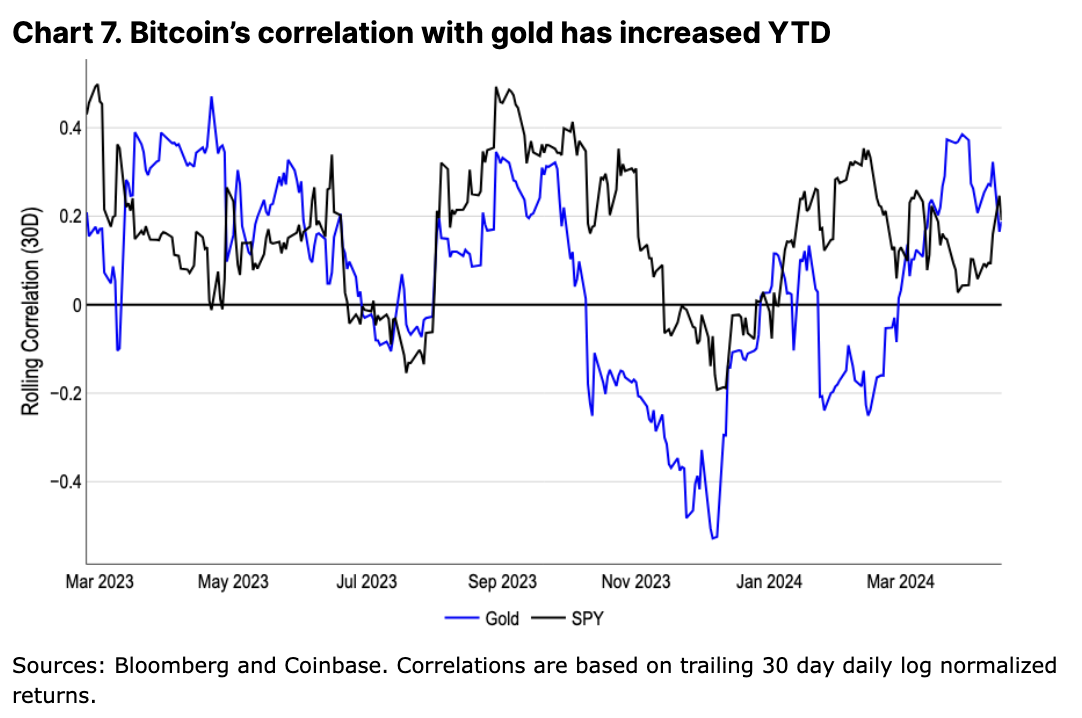

Bitcoin’s correlation with gold rose steadily in March and April amid rising inflation concerns, further indicating Bitcoin’s strengthening role as a sensitive macro asset in the absence of crypto-specific catalysts like spot ETF approvals. This behavior is encouraging given Bitcoin’s positioning as a store of value, though we believe this thesis was already reinforced during the recent bear market.

Bitcoin saw strong bids during uncertainties around the U.S. debt ceiling in January 2023 and the regional banking crisis in March of that year. Compressed price appreciation—like the past six months—may distort this signal somewhat by introducing speculation and excitement. Nonetheless, we maintain that Bitcoin’s value as a geopolitical hedge has so far contributed to stronger buy-the-dip behavior, limiting maximum drawdowns to 18% (compared to over 30% in previous cycles).

Additionally, rising U.S. Treasury levels are another concern for Bitcoin advocates. The Congressional Budget Office forecasts $870B in interest payments on national debt for 2024, up from $658B in 2023. We find this concerning and believe it contributes to an inverted yield curve—long-term higher rates may be fiscally unsustainable as U.S. Treasuries require refinancing.

That said, even as the pace of U.S. debt accumulation accelerates, there remains potential for the U.S. to grow out of debt (or balance budgets via spending cuts or tax increases, though neither seems likely before mid-term elections). Stronger-than-expected GDP growth and robust employment data could boost overall tax revenues. While we believe current growth rates cannot fully offset rising debt burdens, they also cannot be entirely discounted. Geopolitical tensions, inflation, and national debt together form the macro backdrop of this cycle.

Conclusion

All else equal, Bitcoin halvings are inherently constructive events. Yet, we believe macro conditions and tangential breakthroughs across crypto verticals have historically played crucial roles in catalyzing cyclical bull markets. While this process usually takes months and varies by cycle, evolving market structures—including major ETF inflows and declining venture funding—may give this cycle some unique characteristics.

We further believe that the previous cycle cemented Bitcoin’s sensitivity to global liquidity following COVID-driven stimulus. However, global liquidity no longer expands at the same scale and has taken a back seat to greater structural instability both domestically and internationally. Given this, we believe the upcoming cycle will center on testing Bitcoin’s store-of-value narrative, supported by a broader dispersion of crypto catalysts across diverse verticals.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News