How the U.S. Combats Cryptocurrency Tax Evasion: An Analysis of the Oyster Protocol and Bruno Block Cases

TechFlow Selected TechFlow Selected

How the U.S. Combats Cryptocurrency Tax Evasion: An Analysis of the Oyster Protocol and Bruno Block Cases

This article will analyze the legal basis for the U.S. government's tax evasion charges against him.

Author: TaxDAO-Ray, TaxDAO-Leslie

In October 2018, the cryptocurrency platform Oyster Protocol suffered a major crisis when its founder, Bruno Block (real name Amir Bruno Elmaani), exploited a vulnerability in the smart contract to privately mint a large number of new Oyster Pearl (PRL) tokens and dumped them on the market, causing the price of PRL to plummet. Elmaani was later charged with tax evasion and fraud, and on October 31 of this year, he was sentenced to four years in prison.

This article outlines the facts and background of Bruno Block’s fraud and tax evasion case, analyzes the legal basis for the U.S. government's charges of tax evasion, and further examines the regulatory and compliance requirements imposed by the U.S. government and the Internal Revenue Service (IRS) on cryptocurrency issuance, aiming to provide guidance for the industry.

1 Case Facts and Background

1.1 Oyster Protocol and Its Business Model

Oyster Protocol was launched in September 2017 by an anonymous founder using the pseudonym Bruno Block. It is a blockchain-based data storage platform utilizing IOTA and Ethereum technologies, designed to offer websites a decentralized, privacy-preserving, and low-cost solution for data storage and transmission. The goal of Oyster Protocol is to provide decentralized storage and encryption services by leveraging idle browser storage space and CPU power from users, while offering website owners a new source of revenue.

The native token of Oyster Protocol is Pearl (PRL), an ERC20 token built on Ethereum, used to buy and sell data on the Oyster Protocol network. PRL also serves to incentivize nodes within the network, maintaining its security and stability.

PRL was issued to enable the operation and monetization of the data storage platform. Oyster Protocol allows users to store and retrieve files through a decentralized, anonymous, and secure system. On one hand, internet users visiting websites that use Oyster Protocol can contribute a portion of their computing power to help other users store data on a distributed ledger. Meanwhile, users needing cloud storage can pay for storage using PRL tokens and earn additional PRL as rewards for participating in network maintenance. On the other hand, website owners and content publishers can also generate income by integrating Oyster Protocol into their sites. By adding just one line of code, they can leverage user-provided computing resources to host their content and receive a share of the PRL payments made by users. This eliminates reliance on traditional advertising models and avoids issues like ad blockers or malware. Oyster Protocol claimed that issuing PRL would create a win-win ecosystem where both websites and users benefit from data storage, enabling value exchange and incentive mechanisms via PRL tokens.

1.2 Development Timeline of Oyster Protocol

In October 2017, Oyster Protocol conducted its initial coin offering (ICO), raising approximately $3 million.

In January 2018, Oyster Protocol launched its testnet, demonstrating data storage and retrieval capabilities. In April of the same year, it released its mainnet, officially launching its data storage service. The mainnet introduced a new token called Shell (SHL), used to pay for network connectivity and decentralized application (DApp) operations; SHL was distributed to PRL holders via airdrop. The mainnet launch marked Oyster Protocol’s transition from concept to functional product, opening up more possibilities for future development.

In October 2018, Oyster Protocol faced a severe crisis when its founder, Amir Bruno Elmaani (also known as Bruno Block), exploited a vulnerability in the smart contract to privately mint millions of new PRL tokens and sold them on the market, causing the PRL token price to crash. Elmaani was subsequently charged with tax evasion and fraud and sentenced to four years in prison.

In November 2018, Oyster Protocol rebranded as Opacity and launched a new token, OPQ, replacing the PRL token. Opacity inherited Oyster Protocol’s technology and vision but severed all ties with Elmaani. Opacity remains operational today, supported by a modest user base and community.

2 Analysis of Elmaani’s Tax Evasion and Fraud Case

In addition to criminal charges brought by the U.S. government, Elmaani’s act of privately minting and cashing out PRL also triggered a civil lawsuit filed by the U.S. Securities and Exchange Commission (SEC). The SEC alleged that Elmaani violated anti-fraud provisions of the Securities Act and the Exchange Act by selling and issuing PRL through false promises and deception, seeking court orders to confiscate his illicit gains and impose civil penalties. Under existing U.S. legal precedents,[1] fraudulent proceeds are still subject to taxation; thus, the outcome of the SEC’s civil suit does not affect the determination of whether Elmaani had taxable income. Therefore, this article will focus primarily on the criminal prosecution initiated by the U.S. government.

It should be noted that although news reports indicate Elmaani pleaded guilty to the judge on April 5, 2023, and the formal sentencing occurred on October 31 of that year,[2] the full judgment text has not been publicly accessible at the time of writing. The most recent relevant legal document available is a “slip copy”—an unofficial draft judgment—signed by the presiding judge on April 4, 2023, as updated on Westlaw.[3] Given that Elmaani entered his guilty plea the day after this draft was published and did not dispute the core facts outlined therein, this analysis will rely on this draft to reconstruct the court’s reasoning.

2.1 Prosecution’s Investigation and Allegations Against Elmaani

According to the indictment filed by the prosecution (representing the U.S. government), there is evidence showing Elmaani engaged in the following acts涉嫌 tax evasion and fraud:

First, between 2017 and 2018, Elmaani sold his PRL holdings for U.S. dollars through a series of intermediary steps. He converted large amounts of PRL held on a first cryptocurrency exchange (“Exchange-1”) into other cryptocurrencies, then transferred these newly acquired coins to a second cryptocurrency platform (“Exchange-2”) and exchanged them for USD.

Second, in October 2018, Elmaani secretly issued millions of additional PRL tokens, sold them, and kept the proceeds (“exit scam”). He modified the PRL smart contract to freely create millions of new Pearl tokens for himself. Using the same method as described above, he converted these PRL tokens into U.S. dollars. During this process, Elmaani used cryptocurrency “mixers” (or “tumblers”)—services that combine transactions from multiple users to obscure individual transaction trails. He also transferred cryptocurrency and U.S. dollars through accounts belonging to friends and family members (including his spouse), further concealing the movement of funds.

Third, Elmaani took additional measures to conceal his income, including trading precious metals.

As a result of Elmaani’s transactions, PRL became nearly worthless. When Exchange-1 discovered the exit scam, it immediately halted all PRL trading and delisted the token two weeks later, resulting in significant investor losses. Two days after executing the exit scam, Elmaani stated that one reason for carrying it out was that “taxes were very annoying.”

2.2 Charges Brought by the Prosecution

The U.S. government charged that during 2017 and 2018, defendant Amir Elmaani earned millions of dollars in income—including proceeds from a newly created cryptocurrency called Pearl—and failed to pay taxes on nearly all of this income. According to the indictment, Elmaani evaded most of his income tax obligations for these two years through various means:

(a) Filing a false income tax return for the 2017 tax year, failing to report substantial income to the IRS;

(b) In 2018, using nominees to receive portions of his unreported income and transferring those funds to himself;

(c) Operating businesses under pseudonyms and hiding his true identity to earn unreported income in 2017 and 2018;

(d) Holding assets through anonymous entities or in others’ names during 2017 and 2018;

(e) Generating additional unreported income through a cryptocurrency exit scam in October 2018, while attempting to conceal his involvement; and

(f) Conducting extensive cryptocurrency, cash, and precious metals transactions in 2017 and 2018 to hide unreported income.

2.3 Elmaani’s Defense

Elmaani did not deny engaging in the actions listed by the prosecution and even admitted knowing he had tax obligations, yet he raised three defenses. First, he argued that his actions were not intended to evade taxes, but rather to avoid scrutiny and tracking by Pearl investors, team members, and the Pearl community. Second, he claimed he never received tax forms from Exchange-2, so he was unaware of how much tax he owed and therefore could not file or pay. Third, he asserted that he suffered from mental illness (insanity) during the period in question, lacked the intent to commit tax evasion, and did not act with tax avoidance in mind. Interestingly, he explained this mental condition as follows: after setting up the scams, he began fearing a collapse of the global financial system and wanted to retrofit a yacht he purchased with his illicit profits to ensure financial security for his family during an impending crisis.

2.4 Summary of Court Ruling

Section 7201 of the U.S. Internal Revenue Code (IRC §7201) defines the federal crime of tax evasion, a felony punishable by up to five years in prison and a $100,000 fine ($500,000 for corporations). The presiding judge in Elmaani’s case noted that, per precedent set in *United States v. Josephberg*,[4] the prosecution must prove three elements to establish tax evasion: (1) a substantial tax liability; (2) willfulness (intent to evade); and (3) affirmative acts taken to evade tax. As previously mentioned, Elmaani admitted to element (1), and although he denied willfulness, he chose not to contest element (2). Thus, the case centered on element (3)—whether Elmaani took affirmative steps to evade taxes, which relates directly to his third defense.

The prosecution rebutted Elmaani’s defense via motion, arguing that mental health evidence should be strictly limited and that Elmaani’s claim of insanity constituted “impermissible evidence that seeks to ‘excuse’ the crime.” The rationale was that even if Elmaani genuinely feared a financial apocalypse, such psychological concerns do not conflict with the duty to pay income tax—meaning he could simultaneously suffer from such delusions and possess the intent to evade taxes. The court accepted the prosecution’s argument and excluded Elmaani’s defense. Ultimately, the court found no evidence or explanation sufficient to absolve Elmaani of tax evasion charges. However, this draft judgment does not specify the final sentence; detailed reasoning and conclusions await the release of the official ruling.

Overall, the trial involved little contention, posed no complex theoretical dilemmas, and featured no ambiguous facts. The dispute focused on traditional elements of criminal liability and did not directly reflect unique characteristics or judicial trends in cryptocurrency-related tax crimes. Nevertheless, given that the Elmaani case occurred as the ICO boom began to wane and considering the rarity of criminal tax cases involving cryptocurrency, it holds notable pioneering and representative significance in the U.S. and globally. The following section will extract insights about U.S. cryptocurrency tax policy from this case and offer extended analysis.

3 Tax-Related Analysis of the Case

3.1 U.S. Cryptocurrency Tax Regime

Taxing cryptocurrency requires first determining its legal nature. Different U.S. agencies hold differing views. For example, the SEC treats cryptocurrencies as securities, while the Commodity Futures Trading Commission (CFTC) classifies them as commodities based on derivative instruments. The IRS, however, defines cryptocurrency as property. Since the IRS is the tax authority, its classification governs cryptocurrency taxation.

The U.S. cryptocurrency tax system primarily revolves around income tax and capital gains tax. Broadly speaking, capital gains tax falls under the umbrella of income tax but is often separately codified due to policy considerations. As early as 2014, the IRS established cryptocurrency tax rules in Notice 2014-21, mandating that cryptocurrencies be taxed like property. Specifically, purchasing and holding cryptocurrency does not trigger tax liability. For income tax purposes, receiving cryptocurrency through airdrops, DeFi lending, mining, or as salary or compensation constitutes taxable income valued at fair market value. For capital gains tax, converting cryptocurrency to fiat currency, gifting cryptocurrency, using it to purchase goods or services, or swapping one crypto for another triggers capital gains tax, calculated based on cost basis and holding period, with different rates applying depending on duration.[5]

However, Elmaani’s conduct presents a special aspect: prior to selling Pearl tokens, he engaged in minting new ones. While capital gains tax on token sales is straightforward, the IRS has not definitively ruled on whether minting itself is a taxable event. Some argue that minting is analogous to mining—both involve computational work to create digital assets—and thus should be taxed similarly. This article posits that whether minted tokens constitute taxable income depends on market liquidity. Without liquidity, the token’s value cannot be reliably determined, making income assessment impossible. In Elmaani’s case, however, the PRL market already had sufficient liquidity when he illegally minted new tokens, meaning their value was reasonably ascertainable. Hence, these newly minted tokens represented taxable income to Elmaani.

3.2 Federal Crime of Tax Evasion

As discussed, the federal tax evasion offense comprises three core elements. Though seemingly simple, these elements have been enriched through numerous judicial precedents, some aspects of which were omitted from the draft judgment but are crucial to understanding the case.

Element (1) requires a substantial tax deficiency—i.e., the amount actually paid falls far short of the legally owed tax. Three points are worth noting. First, U.S. income tax liability is assessed annually; each year’s obligation is independent. If a taxpayer earns taxable income and evades tax over three consecutive years, they face three separate charges, not one aggregated count. Thus, Elmaani may have committed federal tax evasion in both 2017 and 2018. Second, the prosecution (typically the U.S. government) need not prove the exact amount of evaded tax. The purpose of criminal punishment is not to recover a specific sum but to deter and penalize tax evasion. Whether an imprecise figure qualifies as “substantial” lacks a fixed formula and is typically decided by juries based on context.[6] This explains why neither the judge, prosecutors, nor Elmaani contested the precise tax amount in the draft ruling. Third, as previously noted, the source of income does not affect its taxability—even illegal or fraudulent income is subject to income tax.[7] Therefore, the outcome of the SEC’s securities fraud case against Elmaani does not impact his tax evasion conviction.

Element (2) requires willfulness—the defendant must have intentionally sought to evade tax. Several standards apply in assessing willfulness. First, a “good motive” cannot negate willfulness. The prosecution need not prove malicious or nefarious intent; it suffices to show voluntary and intentional violation of a known legal duty.[8] Second, deliberate ignorance constitutes willfulness. This refers to situations where a taxpayer knows they lack knowledge of tax laws but files returns anyway. However, an exception exists: if tax laws are unclear or ambiguous, misunderstanding them can serve as a valid defense.[9] Third, diminished mental capacity can be a defense—but only if the mental impairment directly relates to the criminal act. Otherwise, as the prosecution argued in this case, mental conditions unrelated to tax compliance (such as apocalyptic fears) cannot excuse tax evasion.

Element (3) requires affirmative acts taken to evade tax, falling into two categories: evasion of assessment and evasion of payment. The former includes omitting or understating income or overstating deductions; the latter involves concealing assets after tax assessment to avoid payment. Mere non-payment, without concealment or falsification, does not constitute federal tax evasion. Elmaani engaged in evasion of assessment—the most common form. Had he simply refused to pay taxes after selling tokens—without filing false returns, operating anonymously, or obfuscating transactions—he might only have faced misdemeanor charges under IRC §2703 for willful failure to file, rather than the felony charge of tax evasion.

3.3 U.S. Reporting Requirements for Cryptocurrency Taxes

There is no separate reporting category or procedure specifically for cryptocurrency taxes. Filings occur within the existing income and capital gains tax frameworks. However, the IRS has steadily tightened and refined its reporting requirements, increasing enforcement and oversight through both direct and indirect means.

Directly, the IRS has intensified tax administration over cryptocurrency users. For instance, since 2020, IRS Form 1040 includes the question: “Did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency in [year]?” Additionally, the IRS has increased its budget, allocating more human and financial resources to enforce cryptocurrency tax compliance. Furthermore, starting in 2024, individuals who receive more than $10,000 in cryptocurrency through transactions or business activities must report it to the IRS.

Indirectly, the IRS leverages centralized exchanges (CEXs) to obtain taxpayer information. Because CEX users must complete KYC verification before trading, even if taxpayers do not self-report crypto activity, exchanges report user transaction data to the IRS via forms such as 1099. Moreover, the IRS employs blockchain analytics tools to trace transaction patterns. If wallet addresses interact with regulated platforms like CEXs, the owner’s identity and transaction history may be uncovered.

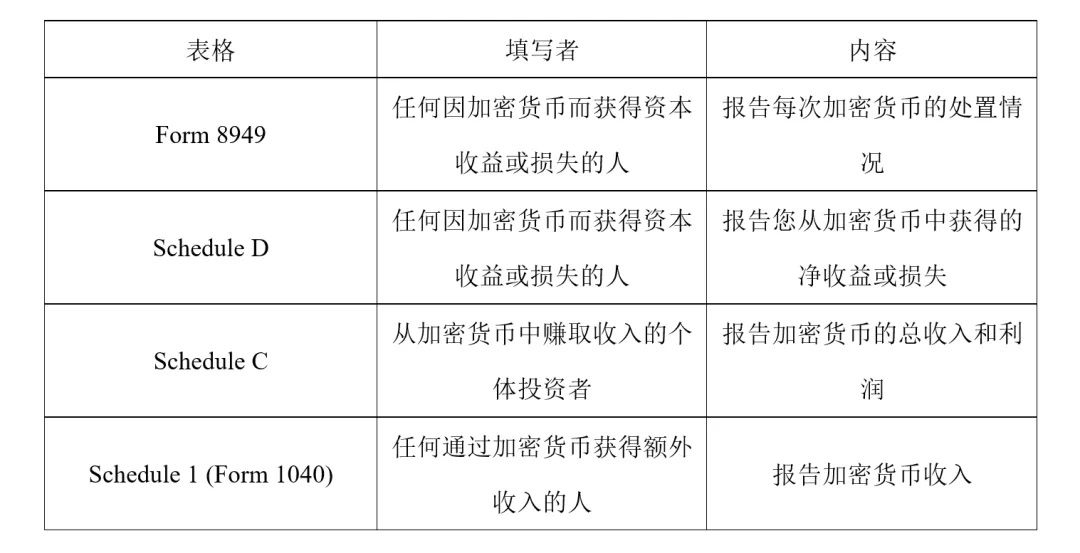

Specifically, taxpayers may need to file the following forms when reporting cryptocurrency taxes:

Additionally, taxpayers may receive 1099-K, 1099-MISC, or 1099-B forms from CEXs, depending on the platform. However, unlike the forms listed above, 1099-K is not used to report individual transaction taxes but helps the IRS gather transaction data. Similarly, 1099-MISC and 1099-B serve informational purposes. Yet none of these forms fully meet the needs of cryptocurrency transactions, prompting the IRS to plan a new 1099-DA form tailored to crypto activity.

4 Conclusion

In stark contrast to the rapid and dynamic growth of cryptocurrency is the relatively lagging and inadequate legal framework, particularly regarding fraud and taxation in crypto transactions. Countries around the world, including the United States, have yet to develop comprehensive regulatory regimes. The Elmaani case involves both civil securities fraud and criminal tax violations—former harming investor rights, the latter undermining state fiscal revenue. This article focuses on the U.S. federal tax evasion charge in the Elmaani case, analyzing the elements of the offense alongside the U.S. cryptocurrency tax system and reporting requirements. Due to the complexity of the cryptocurrency domain and the technical nature of tax compliance, this article highlights key issues; deeper theoretical and practical questions regarding crypto taxation will be addressed in future writings.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News