Opinion: Should We Prepare for the Rejection of Spot Ethereum ETFs?

TechFlow Selected TechFlow Selected

Opinion: Should We Prepare for the Rejection of Spot Ethereum ETFs?

Aside from the oft-repeated "securitization risk," data also shows that whales and derivatives traders do not have high expectations for approval.

Author: BloFin

Translation: Frank, Foresight News

Compared to spot Bitcoin ETFs, the negative impacts of PoS mechanisms, price manipulation risks, and securitization risks significantly reduce the likelihood of a spot Ethereum ETF being approved. However, whether or not an Ethereum ETF is approved will ultimately not affect ETH's potential for breakthrough price growth.

That said, with the rise of other competitors, Ethereum may struggle to further expand its market share.

Securitization Risk

Many investors believe that after the approval of spot Bitcoin ETFs, the approval of a spot Ethereum ETF is "only a matter of time." Previously, some analysts believed that because BlackRock was one of the applicants for a spot Ethereum ETF, the probability of approval could even reach 80%.

However, as more details have emerged, analysts have gradually lowered their expectations for a spot Ethereum ETF.

Analysts' concerns are not unfounded. Although Ethereum futures ETFs were approved last year, with the launch of spot Bitcoin ETFs, the U.S. Securities and Exchange Commission (SEC) chair appears to have established criteria for reviewing crypto spot ETF applications—namely, “commodity tokens” without securities attributes or risk of being classified as securities.

Undoubtedly, Bitcoin is seen by the SEC as one of the "gold standards":

-

Bitcoin is similar to mined gold—limited in supply, non-renewable, and costly to obtain;

-

The Bitcoin network is stable and mature; factors such as consensus mechanism upgrades are unlikely to cause major changes in the foreseeable future, just as wheat won’t turn into corn;

-

It never underwent an ICO (Initial Coin Offering) or any form of fundraising, and its market gradually formed through user-to-user trading—similar to how the Chicago livestock and grain markets laid the foundation for the Chicago Mercantile Exchange (CME), a classic case;

-

Holders are numerous and widely distributed, resulting in relatively low risk of price manipulation.

For Ethereum, however, these standards do not appear to be fully met.

Although the new mechanisms introduced by Ethereum 2.0 and subsequent upgrades will create a deflationary trend for ETH, reducing its circulating supply, ETH continues to be newly issued under the PoS mechanism, has no theoretical supply cap, and its "inflation" and "deflation" are closely tied to its own network activity.

For example, when Ethereum’s network activity was low (such as in July 2023), ETH experienced renewed "inflation."

Some have analogized Ethereum as a "renewable digital commodity," akin to renewable agricultural products like corn and soybeans, emphasizing that it can be "planted" and "harvested" in digital space, with the PoS mechanism likened to sowing—holding 32 ETH is equivalent to owning "seeds" that allow participation in staking and earning rewards.

However, holding crops does not confer voting rights, whereas ETH holders under the PoS mechanism can vote—the more ETH held, the greater the voting power and influence over Ethereum’s future development. Furthermore, it is difficult to find a more reasonable explanation to make ETH appear more like a "commodity" rather than a "security."

-

The Ethereum network is constantly upgrading. The year after Ethereum futures officially launched on the Chicago Mercantile Exchange (CME), it underwent a major upgrade—transitioning its consensus mechanism from PoW to PoS and experiencing a mainnet fork. Like the "Ship of Theseus," Ethereum continuously evolves through upgrades; ETH in March 2024 is fundamentally different from ETH in March 2021;

-

ETH conducted an ICO in 2014, and this fundraising event may classify ETH as an asset with "securities characteristics." Both the U.S. SEC and financial regulators in other countries have stated that "ICO tokens may be considered securities." For assets with contested classification, the U.S. SEC may scrutinize them more carefully;

-

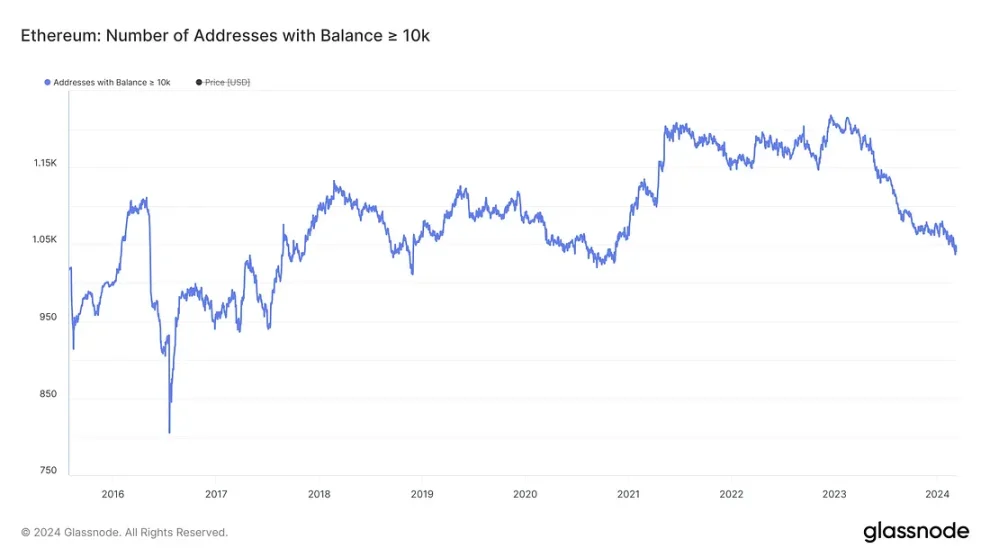

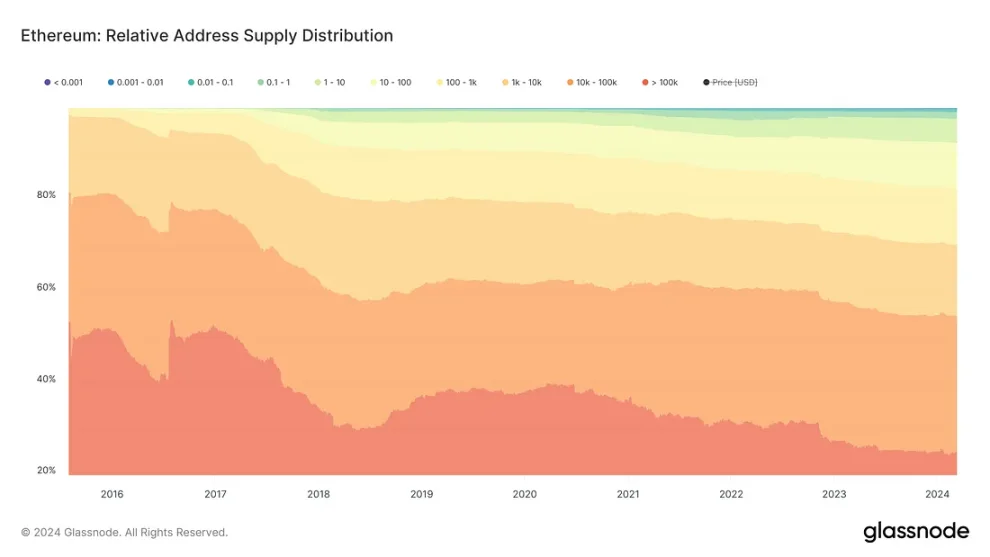

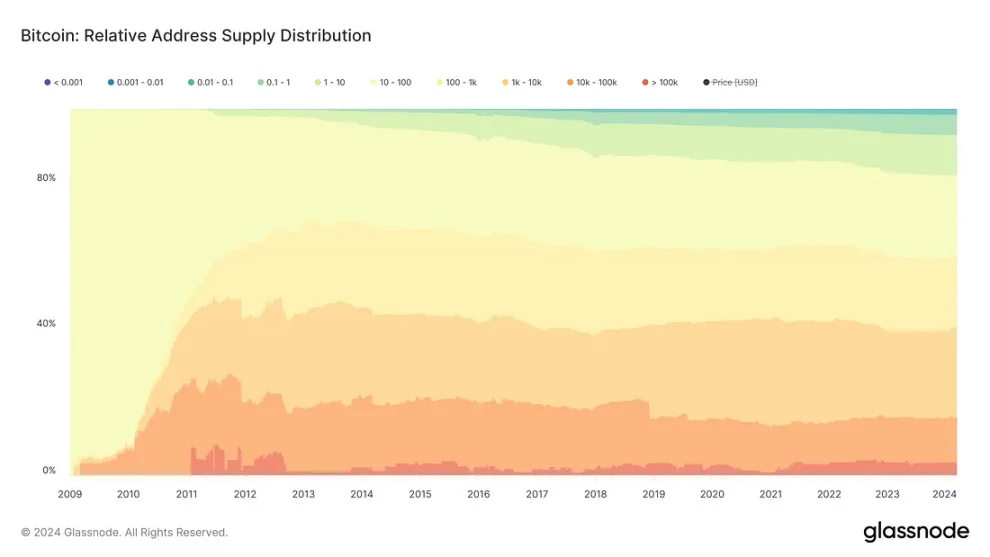

Whale concentration. According to Glassnode data, approximately 55% of ETH supply (around 66 million ETH) is held by 1,041 addresses, each with an average balance exceeding 10,000 ETH. In contrast, retail holders own less than 45% of the total ETH supply. Moreover, under the PoS mechanism, token holdings are nearly directly linked to voting rights, meaning these 1,041 addresses can significantly influence Ethereum’s upgrades and operations;

In contrast, Bitcoin holders have no voting rights and thus cannot significantly impact Bitcoin’s network operations. Since 2009, Bitcoin ownership has become highly decentralized. As of March 2024, whales holding more than 1,000 BTC account for only about 40% of the total circulating supply, and the number of whale addresses has reached 2,100, making Bitcoin far less susceptible to price manipulation than Ethereum.

Of course, the U.S. Securities and Exchange Commission (SEC) remains cautious—at least for now. In public filings, the SEC has expressed concerns about potential risks arising from Ethereum’s PoS mechanism:

“Do ETH and its ecosystem possess certain specific characteristics—including the PoS mechanism and excessive centralization of control or influence among a small number of individuals or entities—that raise concerns about Ethereum’s susceptibility to fraud and manipulation?”

In summary, due to the presence of “securitization risk,” although we hope for the approval of a spot Ethereum ETF, we must also prepare for the possibility of rejection by the SEC.

What Whales Think

Compared to the situation surrounding the approval of spot Bitcoin ETFs, spot whales and derivatives traders seem to have low expectations for the approval of a spot Ethereum ETF and are already preparing accordingly.

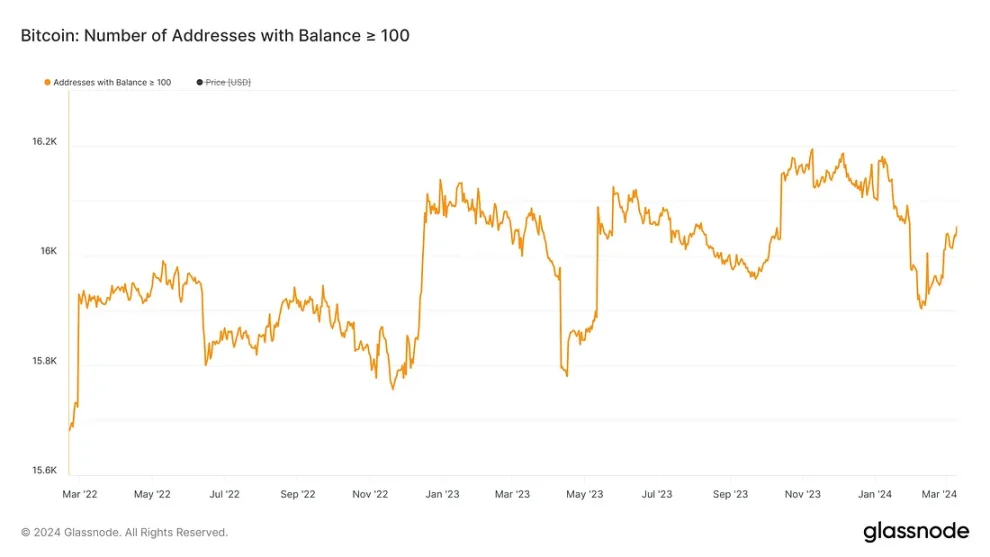

From on-chain data, although miner sell-offs every quarter impact statistics to some extent, since May 2023, the number of addresses holding more than 100 BTC has clearly increased. Compared to Q1 2022 and the first half of 2023, the impact of miner sell-offs on address counts has weakened significantly, indicating that prior to the approval of spot Bitcoin ETFs, many spot whales accumulated large amounts of BTC.

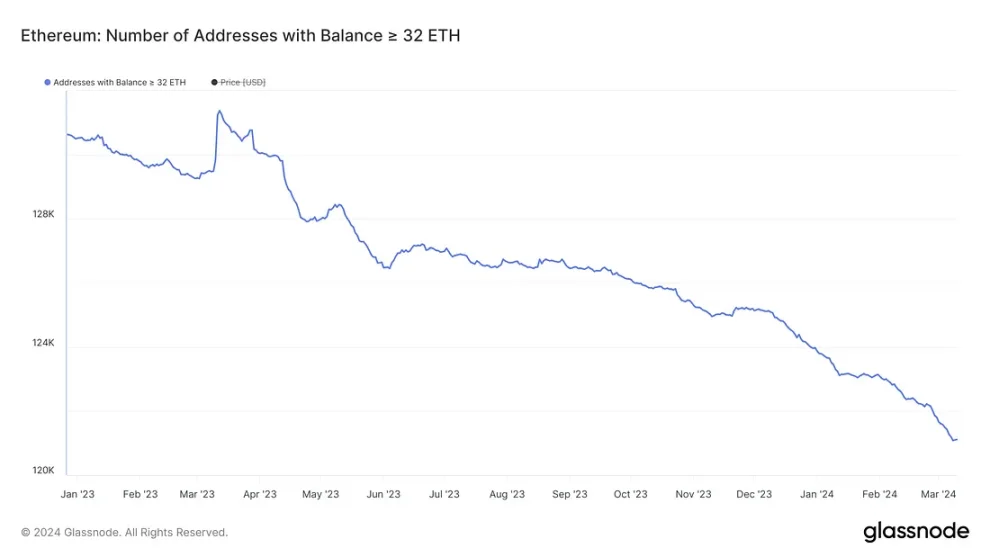

However, ETH on-chain data does not show similar signs. Even using relatively loose criteria, the number of addresses holding more than 32 ETH has been steadily decreasing since January 2023. Speculative hype around a spot Ethereum ETF has not notably affected this downward trend—in fact, the decline has accelerated.

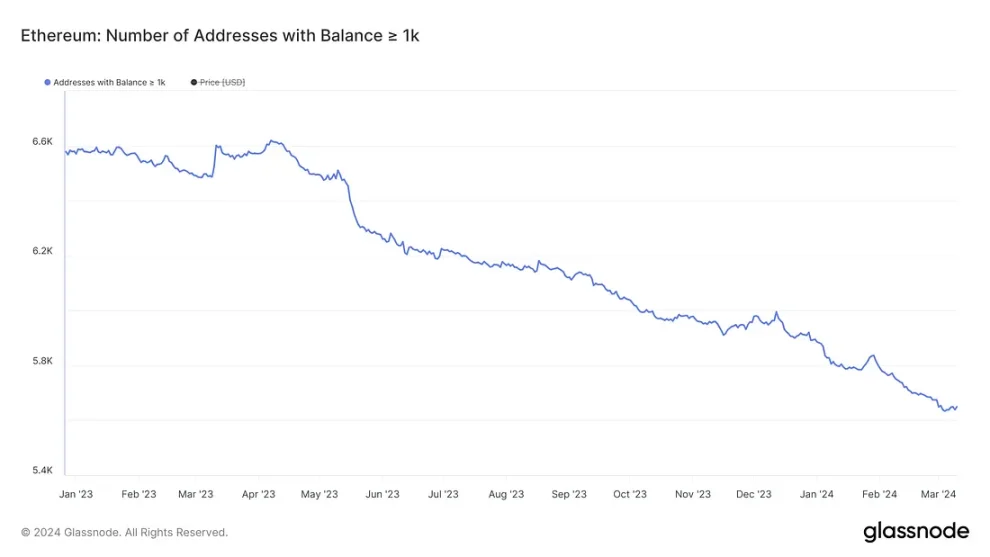

If we consider only addresses holding more than 1,000 ETH, the same conclusion holds—whales appear to be selling their ETH for profit amid speculation and optimism.

In the options market, we also find clues. After the announcement of spot Bitcoin ETF applications, both BTC and ETH showed significant increases in forward options "skew" (Foresight News note: a statistical concept describing asymmetry in data distribution, categorized as negative or positive skew), peaking in November 2023—indicating that option traders at the time were more inclined to bet on rising prices (bullish).

By comparison, the news of spot Ethereum ETF applications did not trigger additional bullish sentiment among options traders; the rise in forward options skew in February this year was more likely driven by a return of liquidity.

Is a Spot ETF Important?

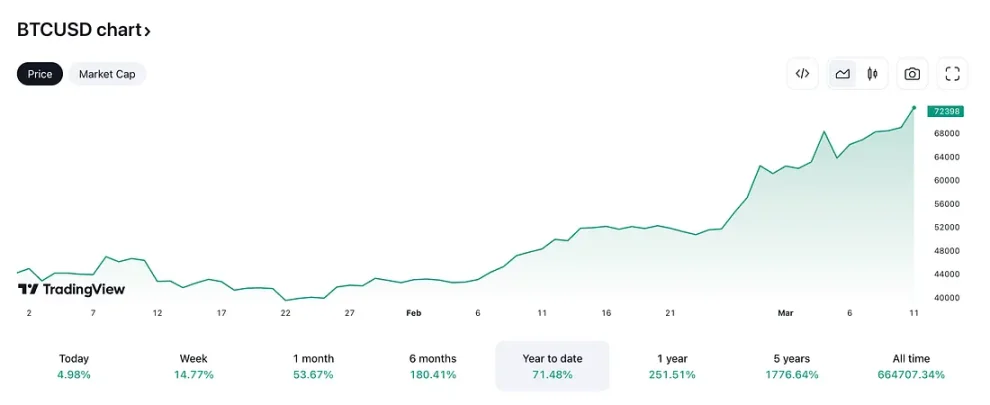

Undoubtedly, spot ETFs are indeed important—they provide a boost to the price of the underlying cryptocurrency upon approval. After the approval of spot ETFs, additional liquidity support from U.S. markets pushed Bitcoin’s price up by over 71% year-to-date, surpassing $72,000 and setting new all-time highs.

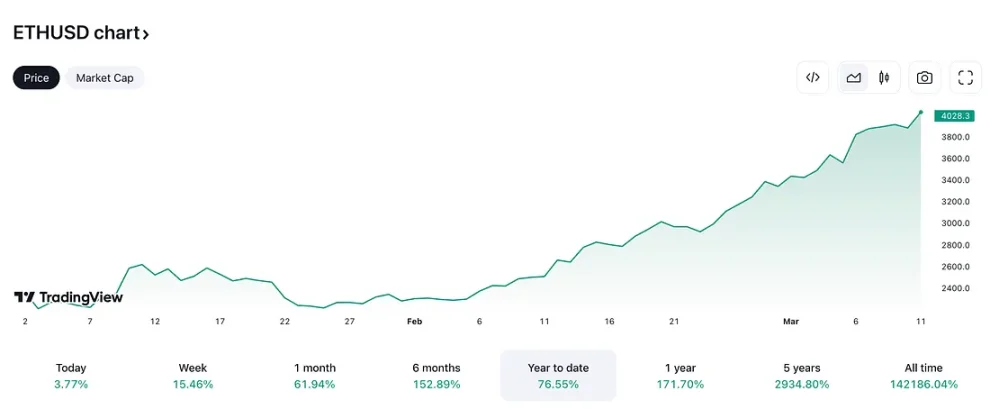

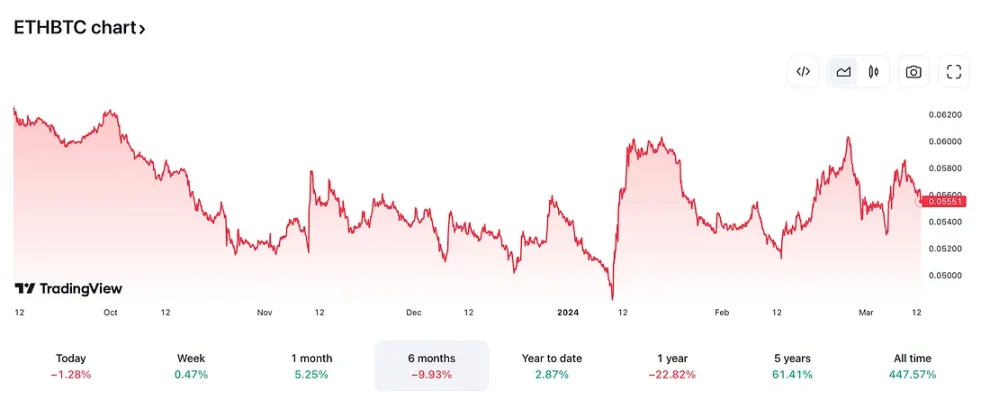

Notably, while ETH has underperformed BTC in relative terms, in absolute price gains, ETH has performed no worse than BTC—and has slightly outperformed BTC year-to-date.

ETH’s recent strong performance depends on multiple factors:

On one hand, when Bitcoin’s price rises sharply, investor inertia in the crypto market often leads them to sell Bitcoin and buy Ethereum instead, transferring the cash liquidity stored in Bitcoin to Ethereum and other cryptocurrencies. At the same time, rapid liquidity inflows provide stronger support for Ethereum’s price, and Ethereum’s relatively high volatility offers greater growth potential.

Therefore, in the medium to long term, as more capital flows into the crypto market, Ethereum’s price increase is expected—and already reflected in derivatives pricing: the persistent positive skew in forward call options best reflects investor bullishness; it’s only a matter of time before Ethereum reaches new highs.

Approval of a spot ETF would merely accelerate this process—but even without approval, it wouldn’t change the fundamental outlook. Ethereum’s price might experience some volatility or even a sharp pullback. Yet in a bull market environment, any downturns will quickly be reversed, and Ethereum’s upward price trajectory will remain intact.

Notably, if a spot ETF is not approved, Ethereum will face increasing competition from within the crypto market—SOL has outperformed BTC over the past six months, and other smart contract platform tokens are gaining momentum.

While Ethereum’s leading position remains unchallenged for now, competing projects will undoubtedly divert liquidity that might otherwise flow to Ethereum. Given that central banks worldwide have generally adopted relatively stable monetary policies, the return of liquidity to crypto markets will be “relatively slow and steady.” Therefore, competing for existing liquidity will become one of Ethereum’s key challenges.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News