Can Grayscale's "Bitcoin Mini Trust" application stem GBTC outflows?

TechFlow Selected TechFlow Selected

Can Grayscale's "Bitcoin Mini Trust" application stem GBTC outflows?

At this stage, the launch of the Grayscale Bitcoin Mini Trust may somewhat slow down GBTC's outflows, but the effect is likely to be limited.

By Andrew Throuvalas, Decrypt

Translated by Jordan, PANews

On the evening of March 12, according to an S-1 filing disclosed by the U.S. Securities and Exchange Commission (SEC), Grayscale, the cryptocurrency asset management giant, has filed to register a new "mini" Bitcoin trust product: the Grayscale Bitcoin Mini Trust, with the ticker symbol "BTC." According to the filing, if this mini version of GBTC is approved by regulators, it will be listed on the New York Stock Exchange and operate independently from GBTC.

Why Is Grayscale Launching a 'New Version of GBTC'?

In the ETF industry, launching a mini version of a flagship trust fund is not uncommon. However, according to a source close to Grayscale, unlike GBTC, the new fund—Grayscale Bitcoin Mini Trust—is being created via a spin-off, meaning Grayscale will need to automatically transfer a portion of GBTC shares into the new Grayscale Bitcoin Mini Trust.

Currently, the S-1 filing disclosed by the SEC does not specify the proportion of shares Grayscale plans to allocate. However, details regarding the split terms and conditions are expected to be further described in a subsequent Form 14C filing by GBTC. Additionally, Grayscale stated that it has not yet sought shareholder consent, authorization, approval, or proxies for the GBTC split. GBTC shareholders will not be required to pay any consideration, exchange or surrender their existing GBTC shares, or take any other action to receive shares distributed through the mini GBTC on the distribution date.

So why is Grayscale choosing to launch this “mini Bitcoin trust” more than two months after its spot Bitcoin ETF, GBTC, received SEC approval?

First, the Grayscale Bitcoin Mini Trust may allow Grayscale to become more competitive on fees. In fact, capital gains realization is one reason GBTC shareholders have remained tied to the existing product, as Grayscale’s GBTC fees are relatively high compared to competing offerings.

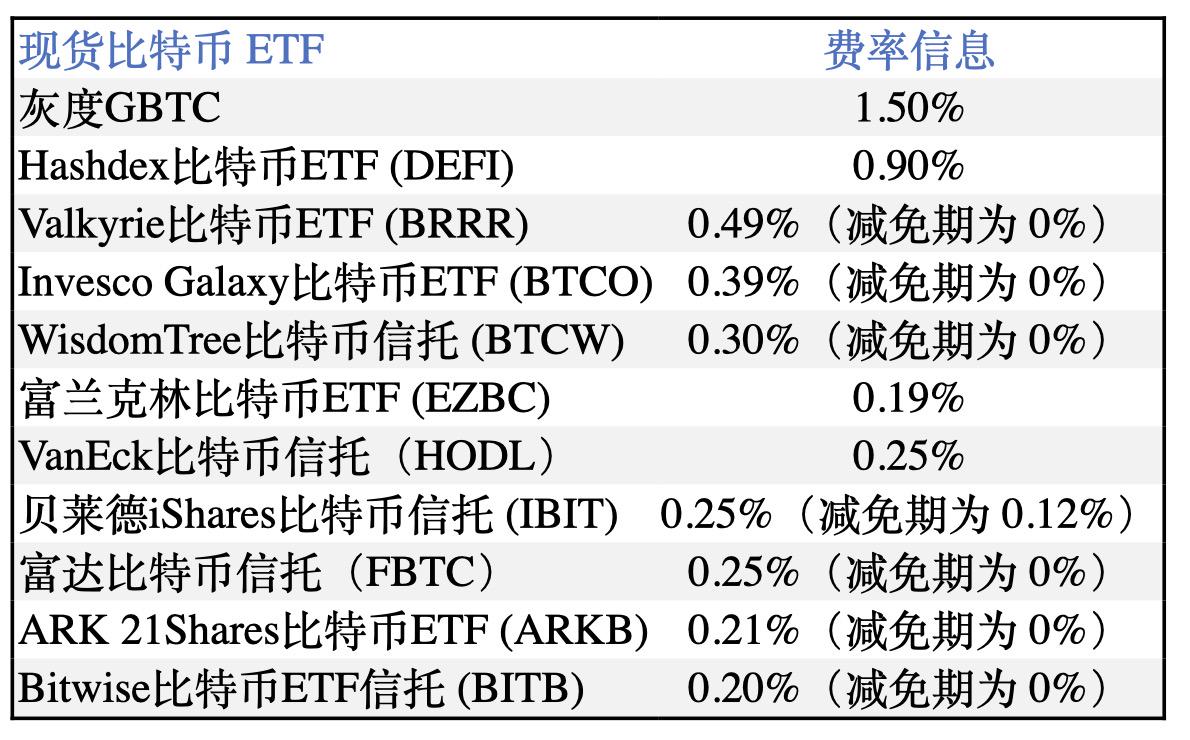

At its current fee structure, GBTC indeed struggles to compete with some of the lower-cost spot Bitcoin ETFs in the market. Although Grayscale converted GBTC from a closed-end Bitcoin fund into an ETF, as shown in the table above, its 1.5% fee rate is the highest among peers (prior to conversion into a spot Bitcoin ETF, GBTC's fee was as high as 2%). By comparison, Franklin’s EZBC charges only 0.19%, and Bitwise’s BITB is even lower at 0.2%. For registered investment advisors (RIAs) and brokers recommending Bitcoin ETF products to clients, fees could become a decisive factor in product selection. Therefore, offering a cheaper alternative to GBTC makes strategic sense.

Although Grayscale has not yet disclosed the fee structure for the “mini trust,” given current market conditions, the number is unlikely to be very high.

Another potential reason behind Grayscale’s application for the “mini trust” relates to tax considerations. Since the approval of Bitcoin ETFs, investors in Grayscale’s Bitcoin Trust have been shifting toward ETFs, and the tax implications of such moves can vary significantly depending on an investor’s position.

For investors holding GBTC within retirement accounts in the U.S., although all these securities serve as proxies for Bitcoin, they are held through traditional brokers. This means that transferring from any of them into a new ETF within a retirement account would be tax-free. However, for investors holding GBTC in taxable accounts, the situation differs. Whether taxes apply depends on whether their position reflects unrealized gains or losses. If an investor holds unrealized gains, selling the investment to move into an ETF would trigger taxable gains, effectively diluting the capital available for reinvestment due to tax obligations.

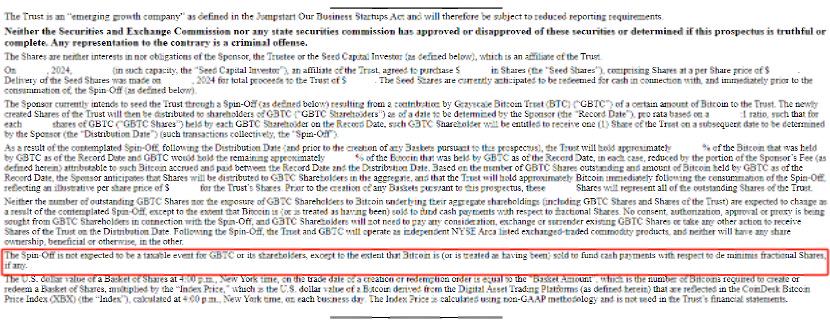

To help investors manage tax liabilities efficiently, Grayscale explicitly stated in its S-1 filing submitted to the SEC: “The spin-off of the mini trust will not constitute a taxable event for GBTC or its shareholders.”

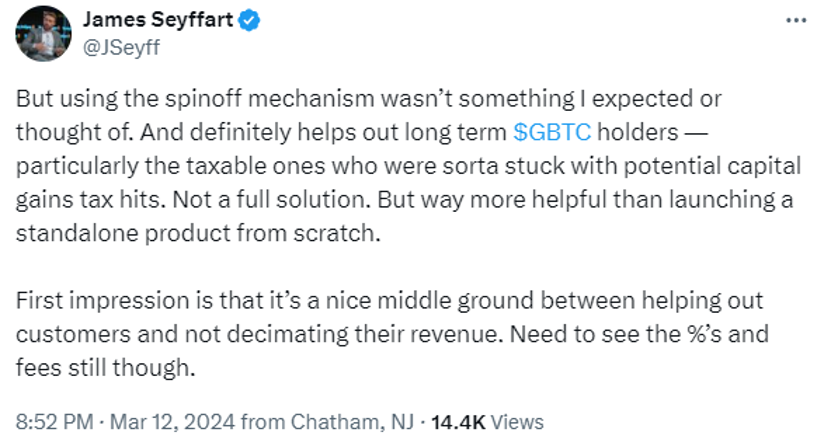

Bloomberg ETF analyst James Seyffart bluntly stated that Grayscale’s mini trust filing is clearly aimed at helping long-term holders avoid taxes. He added that the mini trust will almost certainly benefit long-term GBTC holders—especially those facing potential capital gains taxes—and represents a smart middle ground for clients who previously had no choice but to pay taxes, allowing them to transition without reducing holdings or triggering sales.

Can the 'Mini Trust' Halt GBTC Outflows?

Since converting into a spot Bitcoin ETF on January 11, GBTC investors have redeemed approximately 229,000 BTC (worth over $10 billion). The fund has yet to record a single day of net inflows. In contrast, BlackRock and Fidelity, Grayscale’s biggest competitors, have accumulated 204,000 BTC and 128,000 BTC respectively in their spot Bitcoin ETFs.

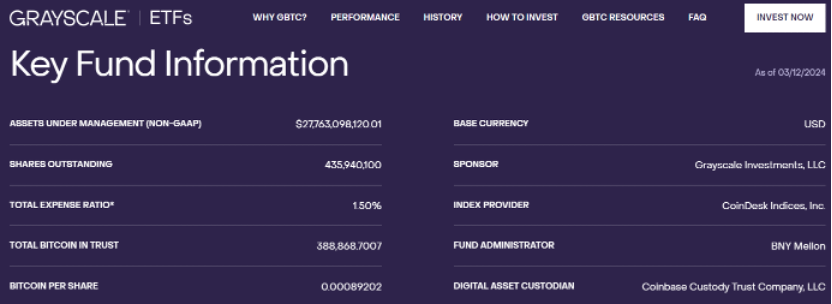

According to official Grayscale data, as of March 12, GBTC’s Bitcoin holdings have fallen below the 400,000 BTC mark, dropping to 388,868.7007 BTC, while the number of outstanding shares has declined below 500 million. However, thanks to a rebound in the crypto market—particularly Bitcoin rising into the $70,000 range—GBTC’s assets under management (non-GAAP) remain in the $27–28 billion range, making it still the largest among peer products.

However, it should be noted that signs of weakening in Grayscale’s market dominance are beginning to emerge. On last Friday’s close, GBTC’s share of total trading volume among spot Bitcoin ETFs fell below 20% for the first time. Meanwhile, combined trading volume for BlackRock and Fidelity’s ETFs rose to 69% (with BlackRock’s IBIT accounting for nearly 47%). Recall that when spot Bitcoin ETFs began trading in January, Grayscale’s GBTC captured about half of all trading activity. This shift suggests that as GBTC sell-offs gradually subside, early investors who have already redeemed their funds are increasingly moving toward competing products.

At this stage, the launch of the Grayscale Bitcoin Mini Trust might slow down GBTC outflows to some extent, but the impact could be limited. On one hand, Grayscale must contend with intense competition and prevent existing customers from switching to rival products. On the other hand, it also needs to attract new investors. Even if the Grayscale Bitcoin Mini Trust receives regulatory approval and lists, it remains uncertain whether the product will offer investors substantially more attractive benefits in terms of taxation and fees. We’ll just have to wait and see!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News