"Chainlink's 'Fed' hikes rates in emergency move, Maker launches 'DAI defense'? "

TechFlow Selected TechFlow Selected

"Chainlink's 'Fed' hikes rates in emergency move, Maker launches 'DAI defense'? "

DSR and multiple core treasuries have significantly adjusted their interest rates—what impacts will this have on Maker and the broader DeFi market?

Author: ImperiumPaper

Translation: Frank, Foresight News

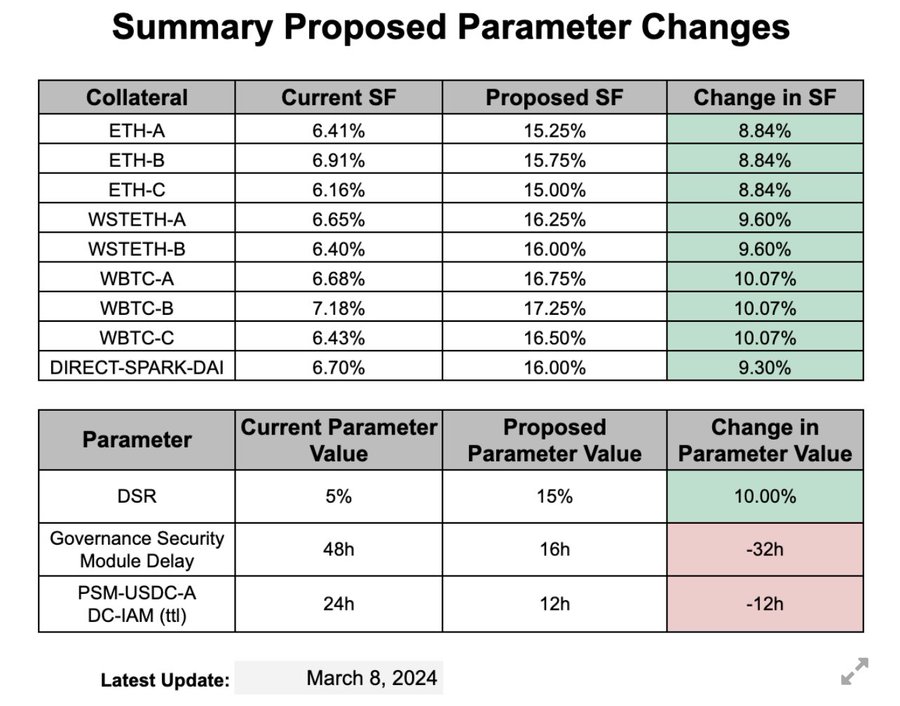

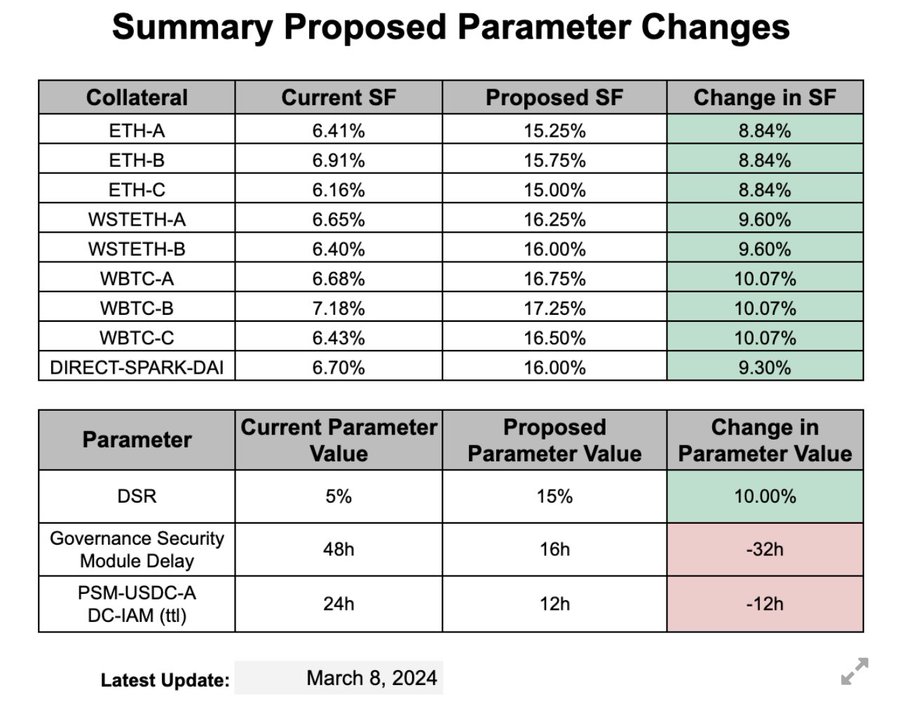

Editor's Note: On March 11, MakerDAO made a series of adjustments to key vault stability fees for DAI savings rate, ETH, WBTC, and other core components. This article aims to briefly analyze the underlying reasons and potential impacts.

To get straight to the point, MakerDAO’s Peg Stability Module (PSM) experienced significant outflows of DAI last week. While the outflows remain within reasonable levels so far, Maker was forced to respond by liquidating treasury bond reserves (tbills) and withdrawing USDC from its Coinbase Custody cold wallet, injecting over $900 million into the PSM to date.

It should be noted that while MakerDAO has not explicitly mentioned this, it has implied that treasury bond reserves (tbills) have been gradually reduced over the past three months.

Maker's "Exchange Rate Stability" Dilemma

Roughly speaking, the cause of the DAI outflows is that MakerDAO and Spark’s lending rates are lower than their peers.

It must be clarified that although the Atlas protocol uses different formulas to set interest rates in Maker’s money markets, these formulas ultimately tie back to the yield on 3-month U.S. Treasury bills (T-bill) (Foresight News note: The Atlas protocol is the foundational rule set governing MakerDAO).

In short, MakerDAO’s system-wide interest rates ultimately depend on the 3-month U.S. Treasury yield. For more details, search for “Yield Collateral Benchmark.”

This further implies that as overall DeFi market rates rise relative to traditional finance (TradFi), MakerDAO’s DAI rates have failed to reflect the increasing cost of borrowing in a timely manner (Foresight News note: i.e., DAI rates were not raised promptly).

Under floating exchange rates, such misalignment could lead to inflation. However, for a currency maintaining a fixed exchange rate (i.e., DAI), the system must use foreign exchange reserves (USDC) to intervene in the market and maintain the peg to the dollar at 1:1.

The problem is that Maker’s hands are tied—as stated above, because its rates are determined by U.S. Treasury yields, it cannot adjust flexibly. For those unfamiliar with how MakerDAO operates, Maker’s “endgame” involves strictly adhering to the Atlas protocol, holding weekly meetings to interpret its meaning, making even minor rule changes extremely difficult and causing mounting pressure due to its disconnect from DeFi market rates.

Until last week, the situation took a sharp turn—PSM’s USDC reserves came dangerously close to depletion, with only 26 minutes of buffer remaining. At this moment, Richard Heart dumped over 300 million DAI to purchase large amounts of ETH. Although MakerDAO still holds $1 billion in U.S. Treasury reserves, weekend wire transfers couldn’t settle in time, creating uncertainty and placing immense pressure on MakerDAO.

Against this backdrop, the BA Labs team proposed emergency fee adjustments. I think they would also admit this approach is quite extreme (Foresight News note: BA Labs submitted a comprehensive proposal on March 9 to increase various fees related to DAI).

However, politically speaking, continuously raising rates is not a viable long-term path.

How to View Maker's Actions

Alright, having analyzed the causes, let’s now examine the logic behind:

-

Raise borrowing rates to encourage repayment of DAI—ideally through exchanging USDC for DAI;

-

Increase DSR (DAI Savings Rate) to incentivize holding DAI—preferably with users operating within the PSM;

These measures are relatively straightforward.

We can also speculate about potential consequences—note that the following content is speculative:

Raising borrowing rates is a conventional and correct move. However, the execution method—such a massive one-time rate hike—is debatable. At least in my view, this could potentially trigger market volatility, though it might not.

Regarding the DSR rate, I remain cautious, as this adjustment feels rushed. I believe they should have waited for borrowers and lenders to adapt to the new borrowing rates and assessed actual yields before making more careful adjustments to DSR.

Considering features like CHAI/sDAI as collateral and integration with Blast, I don’t think DSR needed to be set this high (i.e., 15%)—the DSR rate adjustment appears overly aggressive.

I’ve been in crypto longer than most participants, and historically, many currencies with fixed exchange rates have suffered severe crises when failing to follow market rates. Therefore, while MakerDAO correctly corrected itself by raising borrowing rates, I fear they may have repeated the same mistake with the DSR rate adjustment.

Overall, this feels reminiscent of Thailand/Indonesia/Philippines in 1997 or Mexico in 1994. MakerDAO’s DSR rate hike feels like an expansionary monetary policy, but unlike the Federal Reserve—because DSR can easily be re-collateralized, thereby lowering borrowing costs.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News