RootData: 2023 Web3 Industry Development Research Report and Annual Top Rankings

TechFlow Selected TechFlow Selected

RootData: 2023 Web3 Industry Development Research Report and Annual Top Rankings

The report provides a detailed analysis and interpretation of the development of the Web3 industry last year.

Author: RootData Research

The Web3 industry as a whole has shown strong signs of recovery. Bitcoin achieved a maximum annual gain of 160%, outperforming all major global asset classes in terms of investment returns, while spot Bitcoin ETFs have become a new channel for incremental capital inflows.

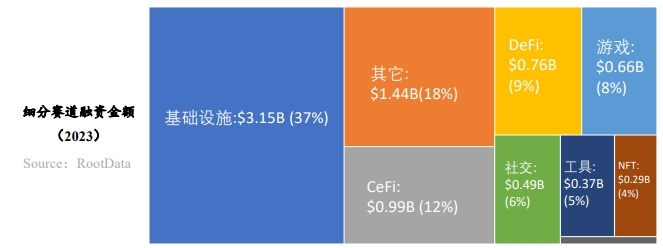

Total funding in the Web3 sector reached $9.043 billion in 2023, with varying performance across different sectors. Enterprise infrastructure and wallet-focused projects attracted significant investor interest. In the DeFi space, DEX competition intensified, while derivatives and RWA gained notable attention. Although CeFi saw a decline in total fundraising, opportunities within the Bitcoin ecosystem drew increasing capital focus.

Identifying native new assets that achieve broad consensus has become a key pattern in Web3 development. Developer numbers increased by 66% year-on-year, with the Ethereum ecosystem maintaining its dominant leadership position. Popular sectors remain concentrated in traditional areas such as DeFi, L1/L2, and gaming, while compliance and social-oriented opportunities are emerging as important market consensus themes.

Over ten institutions led at least eight funding rounds in 2023. HashKey Capital topped the annual ranking in number of investments, making extensive moves across infrastructure and DeFi, particularly in the Asia-Pacific region. DWF Labs emerged as the year's dark horse, primarily investing in already-tokenized projects with relatively low market热度.

I. Overall Trends in the Web3 Industry

1.1 Secondary Market & Macro Analysis: Bitcoin Leads Global Asset Gains; Spot ETFs Open New Growth Dimensions

1. Bitcoin: A Highlight Among Global Assets

In 2023, Bitcoin performed exceptionally well as an asset class. According to NYDIG, as of October 2023, Bitcoin delivered a 63.3% return, making it the top-performing asset among 40 selected categories. This surpassed large-cap U.S. growth stocks (28.2%), along with other major asset classes including U.S. equities (12.2%), commodities (6%), cash (3.8%), and gold (1.1%). Furthermore, Kaiko Research reported that despite macroeconomic pressures and headwinds within the crypto industry, Bitcoin’s price rose over 160% in 2023.

2. Bitcoin Halving: A New Supply-Demand Opportunity

The next Bitcoin halving event is expected in Q2 2024. Historically, each halving has been followed by significant price increases, albeit accompanied by higher volatility. On the demand side, data from Glassnode shows that as of December 22, 2023, the number of non-zero Bitcoin addresses exceeded 50 million, reflecting growing user adoption. These factors collectively influence Bitcoin’s market value and trading activity.

3. Bitcoin Spot ETFs: Leading the Growth Trend

Bitcoin spot ETFs stood out in market performance, recording over $1.8 billion in trading volume on January 16—triple the combined volume of 500 other ETFs traded the same day. Trading volume approached $2 billion in the first three days. Key funds include those managed by Grayscale, BlackRock, and Fidelity. Standard Chartered’s Head of FX Strategy forecasts potential inflows between $50 billion and $100 billion in 2024, highlighting strong market interest and growth potential.

4. Monetary Policy Shift: Catalyzing a New Bull Run in Web3

The previous bull market coincided with loose U.S. monetary policy. However, recent data suggests the Federal Reserve may cut interest rates in 2024. In this context, cryptocurrencies like Bitcoin—with their low correlation to traditional markets and safe-haven attributes—may become attractive diversification tools for investors. Following approval of spot Bitcoin ETFs, Bitcoin is transitioning from retail to institutional investment, reducing circulating supply and enhancing scarcity. Anticipated Fed rate cuts and inflation hedging strategies could drive further Bitcoin allocations, signaling the beginning of a new bull cycle in the Web3 industry.

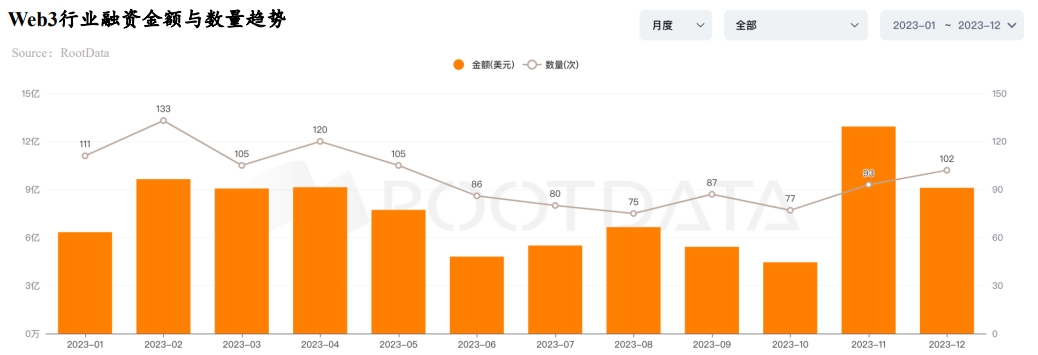

1.2 Total Investment in 2023 Reached $9.043 Billion: Synergy Between Primary and Secondary Markets Fuels Web3 Recovery and Growth

Stimulated by positive developments around Bitcoin spot ETFs, BTC prices broke through the $30,000 resistance level after multiple tests. With strong bullish sentiment prevailing, total Web3 industry funding reached $9.13 billion by December 31, 2023. The highest monthly funding was recorded in November at $1.312 billion, and Q4 alone accounted for more funding than the first three quarters combined. This momentum is largely attributable to the short feedback loop between primary and secondary markets in Web3, indicating that the primary market is gradually returning to a path of recovery and growth.

Since Q3 2023, several funds have announced successful closings: Web3 fund Lightspeed Faction raised $285 million (14% above target), Standard Chartered partnered with Japanese financial giant SBI to launch a $100 million Web3 fund, and CMCC Global, backed by Richard Li, completed a $100 million fundraising round.

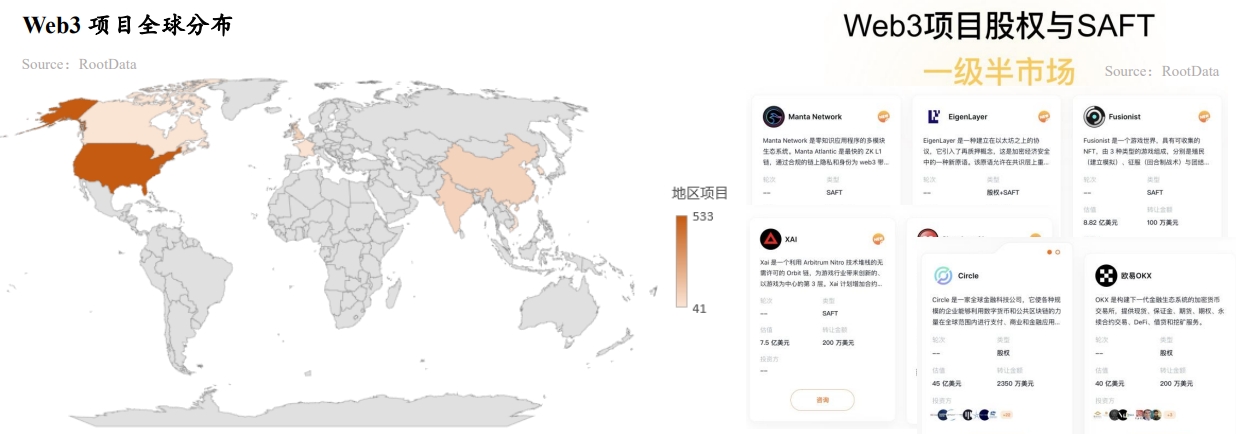

1.3 The Pre-IPO Market Is Becoming a New Path for Investment or Exit: Fireblocks’ OTC Valuation Drops Most, EigenLayer’s Rises Most

-

As Web3 accelerates toward compliance, the tight linkage between primary and secondary markets often triggers FOMO among investors and leads to inflated valuations. As a result, an increasing number of investors are turning to the pre-IPO (private secondary) market as a strategic route for both investment and exit.

-

Among the 45 projects listed on RootData’s pre-IPO market, Fireblocks experienced the largest valuation drop, falling approximately $4 billion from its last funding round. Copper and Dune Analytics also saw OTC valuations decline by hundreds of millions. In contrast, EigenLayer demonstrated strong momentum, with its current $2.5 billion OTC valuation being five times its latest funding round of $500 million. Projects like Aleo and LayerZero maintained relatively stable OTC valuations.

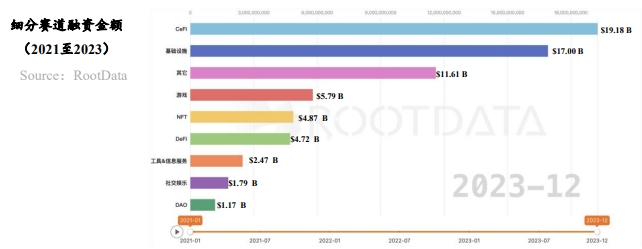

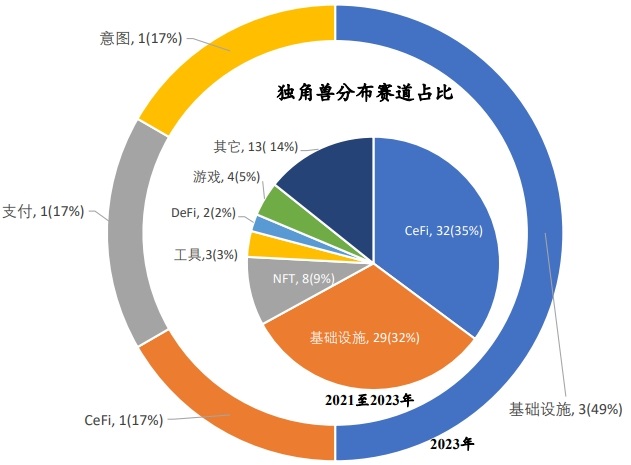

1.4 Infrastructure and CeFi Led Web3 Development in 2023, Adding Six New Unicorns

According to RootData, infrastructure, CeFi, gaming, NFTs, and DeFi have consistently attracted the most capital over the past three years. The average funding amount in 2023 was $9.9 million, nearly half of the $18.8 million average in 2022. Despite two consecutive bearish years, infrastructure remains a high-activity sector.

As of December 31, 2023, the Web3 industry had produced a total of 91 unicorn projects: 32 in CeFi, 29 in infrastructure, and 8 in NFTs. However, due to prolonged market downturns and slower investment pace in the primary market, only six new Web3 unicorns emerged in 2023—Andalusia Labs, Scroll, Flashbots, BitGo, Wormhole, and Ramp—representing just one-fifth the number from 2022.

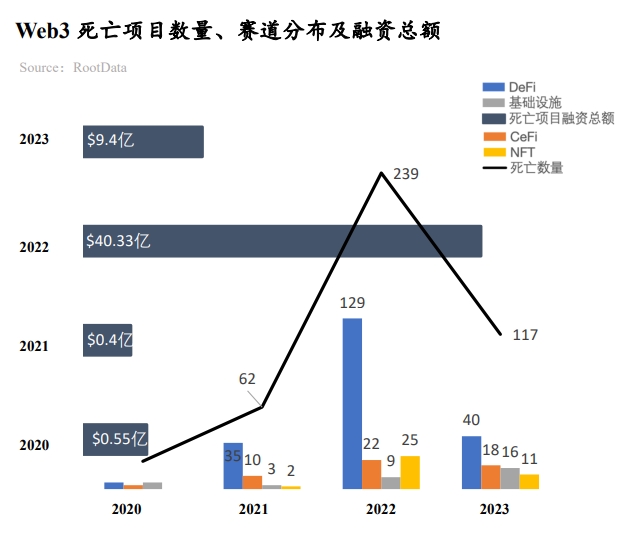

1.5 The Web3 Industry Is Maturing: Number of Failed Projects Down 50% Year-on-Year in 2023

According to RootData, approximately 120 projects announced bankruptcy or ceased operations in 2023, having raised a cumulative $940 million. Compared to 239 failed projects in 2022 with total funding of $4.033 billion, this represents a significant decline, indicating the industry is becoming more mature and stable. Failed projects spanned various sectors, with DeFi seeing the highest number (40), followed by CeFi (18) and infrastructure (16).

The top three failed projects by funding were Prime Trust ($163 million), Voice ($150 million), and Rally ($72 million). Insufficient funding was the primary and most direct reason for shutdowns, with other contributing factors including lack of product-market fit, tightening regulations, and hacker attacks.

II. Characteristics and Sector Trends in Web3 Asset Development

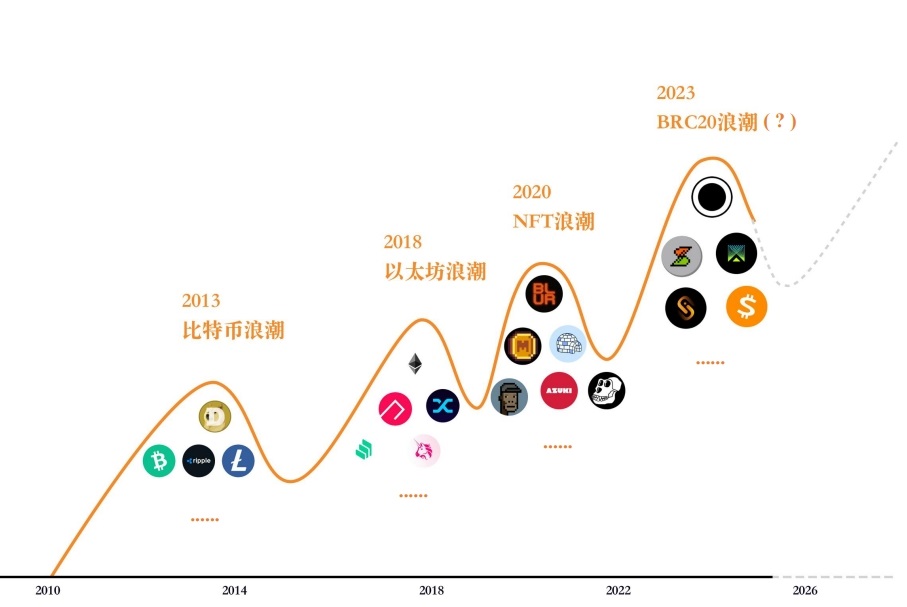

2.1 Four Waves of Innovation in the Web3 Industry: Seeking Native New Assets with Broadest Consensus

The essence of four innovation waves in the Web3 industry lies in discovering native new assets that achieve the broadest consensus. New assets drive capital inflows, making it crucial to understand the pathways and scenarios where these new Web3-native assets emerge—especially native ones, which face fewer barriers and offer greater narrative potential compared to non-native assets.

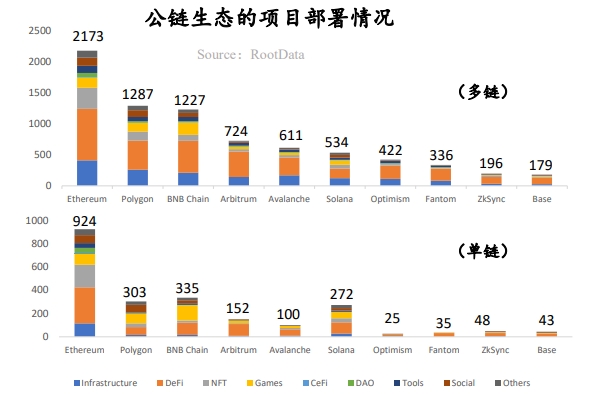

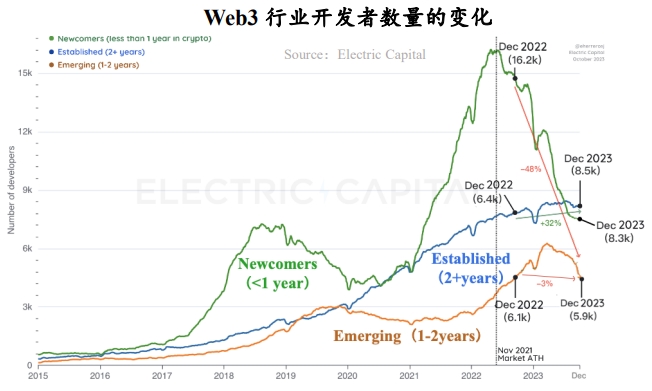

2.2 Web3 Developer Count Up 66% Year-on-Year: Ethereum Ecosystem Holds Overwhelming Advantage

-

Ethereum ecosystem holds overwhelming dominance: Whether measured by single-chain or multi-chain metrics, Ethereum maintains a clear lead, with other ecosystems mainly capturing overflow value from Ethereum;

-

Solana emerged as the standout public chain in 2023: SOL token surged nearly 1000%; the Solana Foundation reported over 2,500 monthly active developers. Star projects—from established DeFi platforms like Raydium, Orca, and Solend to newer names such as Jito, Jupiter, and Pyth Network—have helped form a unique and vibrant ecosystem advantage.

-

Overall developer count up from previous cycle: Compared to the last bear market, the number of developers has increased by 66%;

-

Shift in developer composition: Experienced builders continue to strengthen their presence in Web3, while speculative developers have largely exited. Data from 2023 shows the biggest change during this bear market was among novice developers (down 58%), whereas experienced developers grew steadily, accounting for 75% of code commits with over one year of experience.

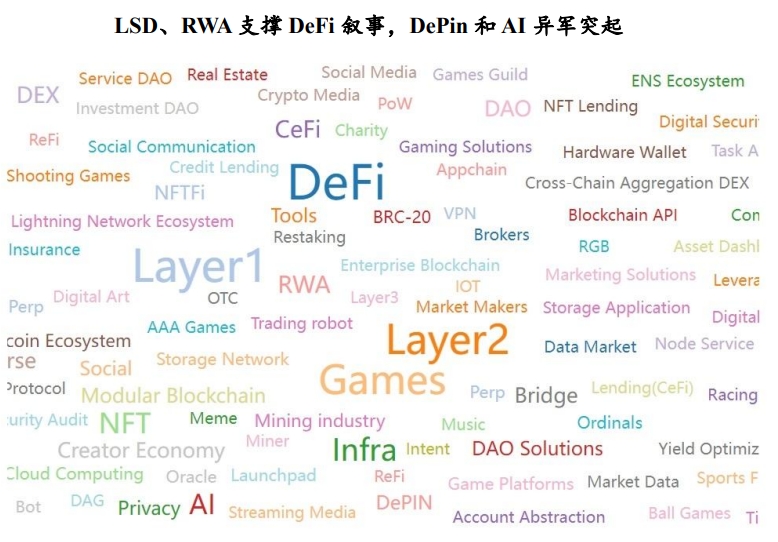

2.3 Rotation of Hot Web3 Sectors: L1/L2, DeFi, and Gaming Remain Top Focus, While Layer3, Intent, and Restaking Gain Attention

-

Based on millions of tag clicks on RootData, DeFi, L1/L2, and Games are the most popular tags. Leaders like staking giant Lido and RWA pioneer MakerDAO have revitalized the DeFi sector.

-

Newer sectors such as Layer3, Intent-centric architectures, and restaking are gaining market attention. EigenLayer brings Ethereum-level trust to middleware layers, creating an entirely new restaking ecosystem.

-

Binance listed 26 new tokens in 2023, covering over 20 hot tags including infrastructure, Layer1, and Meme coins. Tags with declining search热度 include NFTFi, DAG, and DOV.

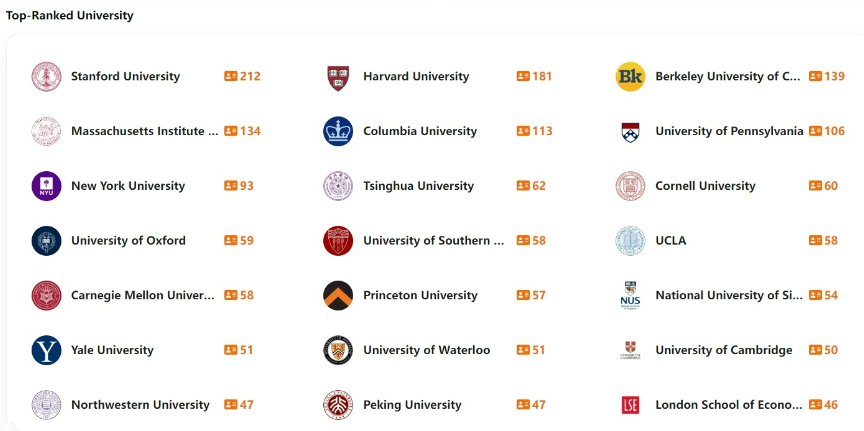

2.4 Stanford Produces Most Web3 Professionals, Google Alumni Projects Raise Highest Funding

-

In terms of education and work background, the U.S., China, and Singapore are the main countries producing Web3 projects. Leading Web3 professionals typically possess dual expertise and resources in finance and technology.

-

Harvard-affiliated and Google-affiliated startup teams have raised the highest total funding amounts. Peking University-affiliated teams rank 15th in total funding, while Binance-affiliated teams rank 10th. Among Chinese founders, Binance and HTX alumni lead in number. Additionally, startup teams from OKX and Bitmain are increasing in number. Non-native Chinese participants mainly come from Alibaba and Tencent.

III. Capital Flow Characteristics and Trend Analysis in Web3

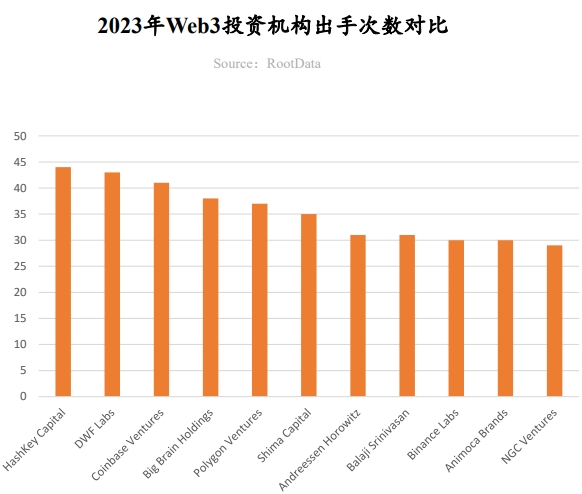

3.1 2023 Web3 Investor Style & Activity Analysis: HashKey Capital Most Active, a16z Crypto Prefers Lead Investments

HashKey Capital became the most active investor of the year

HashKey Capital ranked first in number of investments in 2023, making broad moves in infrastructure and DeFi, with particular focus on Asia-Pacific projects. In January 2023, it announced the close of its third fund at $500 million, supporting its high-frequency investment strategy. Notable investments include MyShell, DappOS, Supra, SynFutures, and PolyHedra.

DWF Labs emerged as the year's dark horse

DWF Labs primarily invested in already-tokenized but low-heat projects, a strategy that sparked controversy. Notable investments include EOS, Conflux, Mask Network, Synthetix, and Fetch.ai.

a16z Crypto favors lead and large-scale investments

a16z Crypto maintains a preference for leading and large-ticket investments, actively participating in infrastructure, gaming, and entertainment sectors. Key investments include Gensyn, Mythical Games, Proof of Play, Story Protocol, and CCP Games.

Over 10 institutions led at least 8 funding rounds in 2023

In terms of lead investment frequency, Andreessen Horowitz, Polychain, Bitkraft Ventures, Dragonfly, 1kx, Hack VC, Shima Capital, Jump Crypto, and ABCDE Capital ranked in the top ten, each leading at least 8 rounds in 2023.

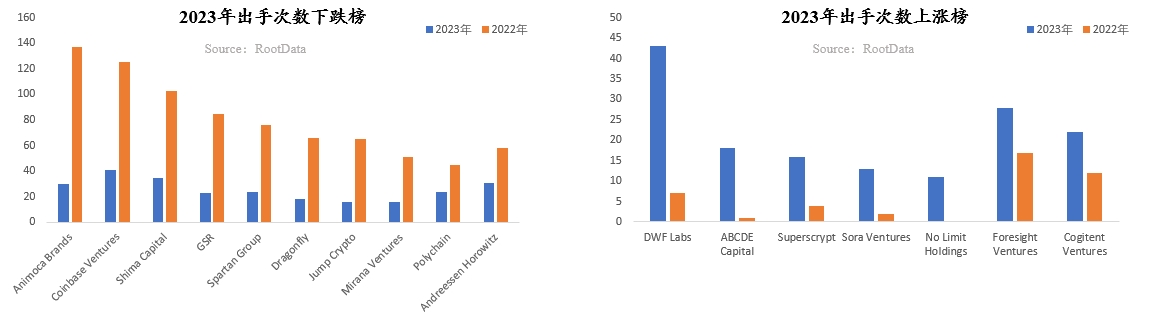

3.2 2023 Web3 Investor Activity Trends: Animoca Brands Saw Largest Drop in Deal Count, 85 Firms Invested Over 10 Times

-

In terms of deal volume, 85 investors made over 10 investments, and 9 made over 30—both figures significantly down from 2022, reflecting widespread challenges such as fundraising difficulties and weakened confidence leading to reduced investment frequency.

-

Investors including Animoca Brands, GSR, Coinbase Ventures, Shima Capital, Spartan Group, a16z, Paradigm, Circle Ventures, and Mirana Ventures all saw investment counts drop significantly, by over 40%.

-

Most Web3 investment firms faced fundraising challenges, with only Blockchain Capital, HashKey Capital, CMCC Global, Bitkraft Ventures, and No Limit Holdings announcing raises exceeding $50 million.

-

Meanwhile, a few firms accelerated their investment pace, injecting momentum into a weak market. ABCDE Capital, Superscrypt, Foresight Ventures, OKX Ventures, Sora Ventures, and No Limit Holdings all increased investment counts by over 50% in 2023.

-

During the year-end Bitcoin ecosystem surge, ABCDE Capital, Sora Ventures, and Waterdrip Capital remained highly active, becoming key investors in Bitcoin-native projects.

3.3 Infrastructure Sector: Cross-Chain Saw Largest Funding Round of the Year; Enterprise Infrastructure and Wallets Attract Strong Capital Interest

Cross-chain sector produced the year’s largest funding round

Wormhole announced a $225 million raise in November 2023, marking the largest single funding round of the year. Cross-chain solutions were among the hottest trends in 2023. As Layer1, Layer2, and even Layer3 networks proliferate, demand for cross-chain asset and data movement is rapidly rising. Wormhole and LayerZero are bridging blockchains through cross-chain communication protocols.

Wallets as traffic gateways receive capital support

As user entry points, wallets remain a key target for capital. Hardware wallet Ledger and social login wallet Magic both secured major funding, reflecting growing user demand for security and convenience. Their evolution is critical to enabling blockchain to onboard the next billion users.

Enterprise infrastructure becomes a strategic focus

Enterprise-grade infrastructure is now a core investment theme. Auradine, a digital asset issuance and custody platform, and QuickNode, a blockchain development platform, both serve enterprise clients, helping companies solve challenges in asset issuance and application development, thereby continuously feeding high-quality assets and projects into the market.

3.4 DeFi Sector: DEX Competition Intensifies; Derivatives and RWA Emerge as Key Focus Areas

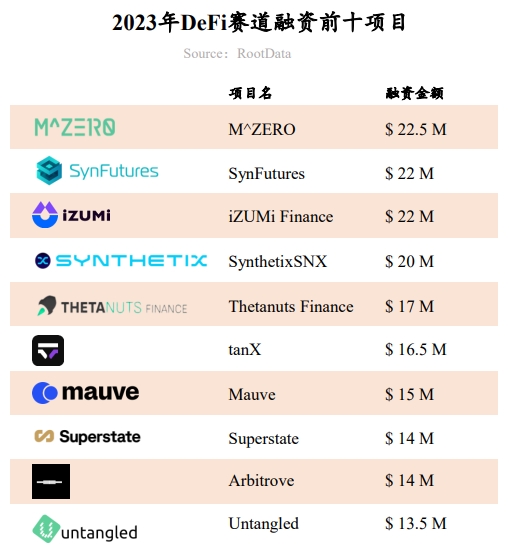

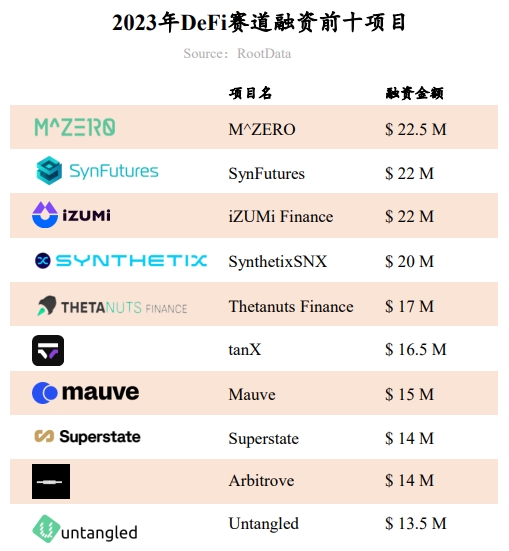

Derivatives protocols attract investor attention

Derivatives protocols are a focal point in DeFi, with SynFutures, Thetanuts Finance, and Synthetix receiving backing for their innovations in perpetual contracts, synthetic assets, and structured products. Their strengths lie in transparent, permissionless operation and improved user experience.

DEX competition intensifies in compliance, order book, and cross-chain features

The decentralized exchange space continues to innovate. Mauve (compliance-focused), tanX (order book model), and iZUMi Finance (multi-chain specialization) are carving out niches to compete with leaders like Uniswap, drawing strong investor expectations.

High expectations for RWA

RWA is becoming the most anticipated direction in DeFi. Assets like real estate, government bonds, and commercial paper offer stable yields, enabling RWA to deliver sustainable and diverse real yields to the crypto market. Superstate, founded by the creator of Compound, is a new major player in the RWA space, aiming to purchase short-term U.S. Treasuries and tokenize them on-chain for direct trading and circulation.

3.5 CeFi Sector: Largest Funding Decline Among Major Sectors; Bitcoin Ecosystem Opportunities Draw Capital

Largest decline among major sectors

In 2023, total CeFi funding amounted to $1.18 billion, a 75% drop—the steepest decline among major sectors—largely due to a series of high-profile CeFi collapses starting in 2022.

Bitcoin-related financial services attract investor bets

Bitcoin-focused financial services received the most capital attention. Swan, Unchained, and River Financial provide savings, lending, brokerage, and other solutions tailored to the Bitcoin ecosystem. As the highest-value crypto asset, Bitcoin holds vast untapped potential for services catering to its holders.

Exchange sector undergoes transformation

Following the FTX collapse, the vacant market space continues to attract investor interest. Exchanges like Blockchain.com and One Trading secured large funding rounds by leveraging vertical specializations, regional advantages, or regulatory licenses.

3.6 GameFi Sector: Total Funding Drops Over 57%; 3A Games Still Favored by Investors

GameFi sector sees over 57% drop in total funding

Affected by secondary market conditions, overall GameFi funding dropped over 57%. Major funding rounds were led by a16z Crypto, Griffin Gaming Partners, and Bitkraft Ventures.

Playability-first becomes dominant trend

3A games are particularly favored by investors. Traditional genres like football, shooting, and adventure games show promising potential in Web3. Playability-first has become the defining trend in GameFi. Meanwhile, fully on-chain games are gaining strong investor and market expectations.

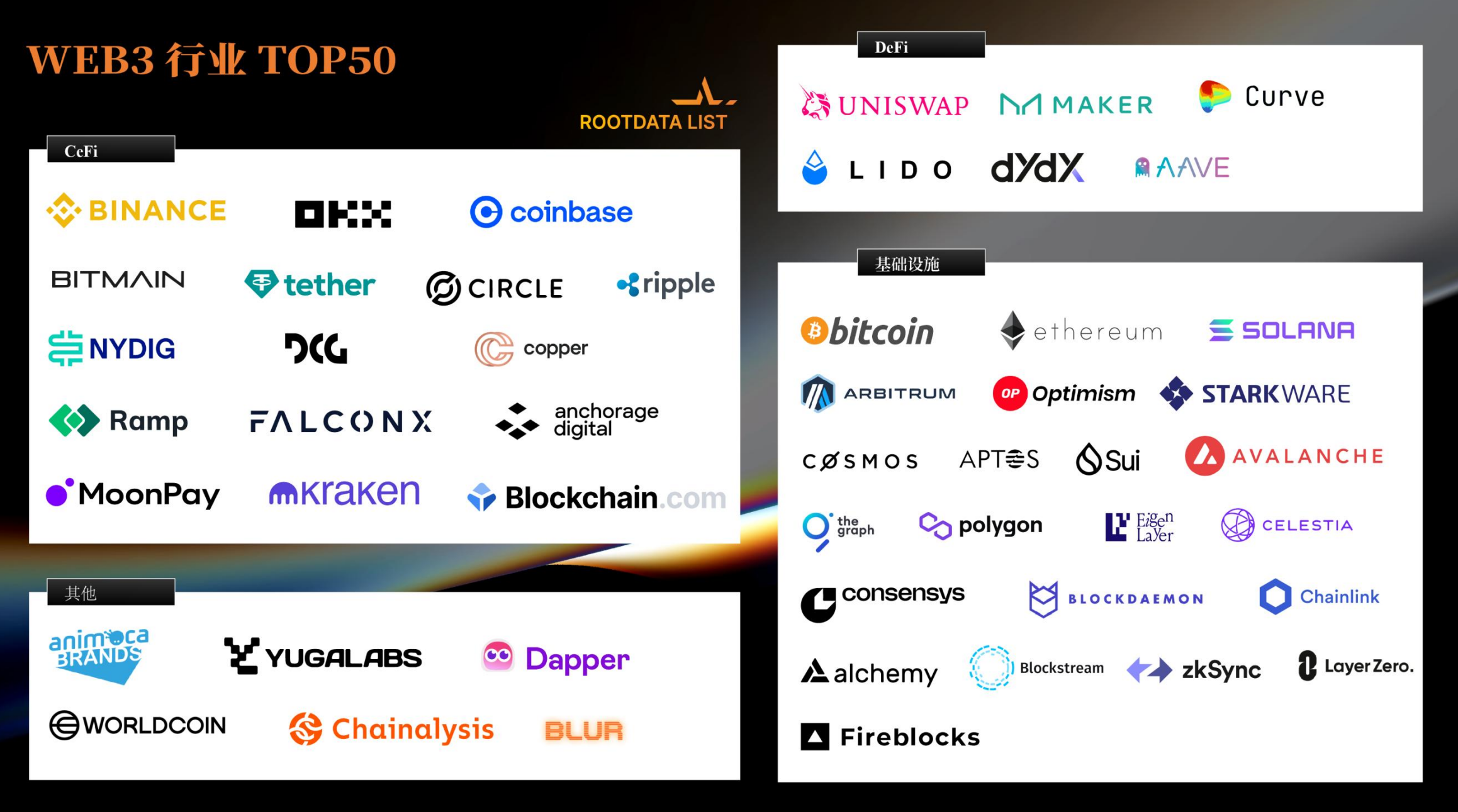

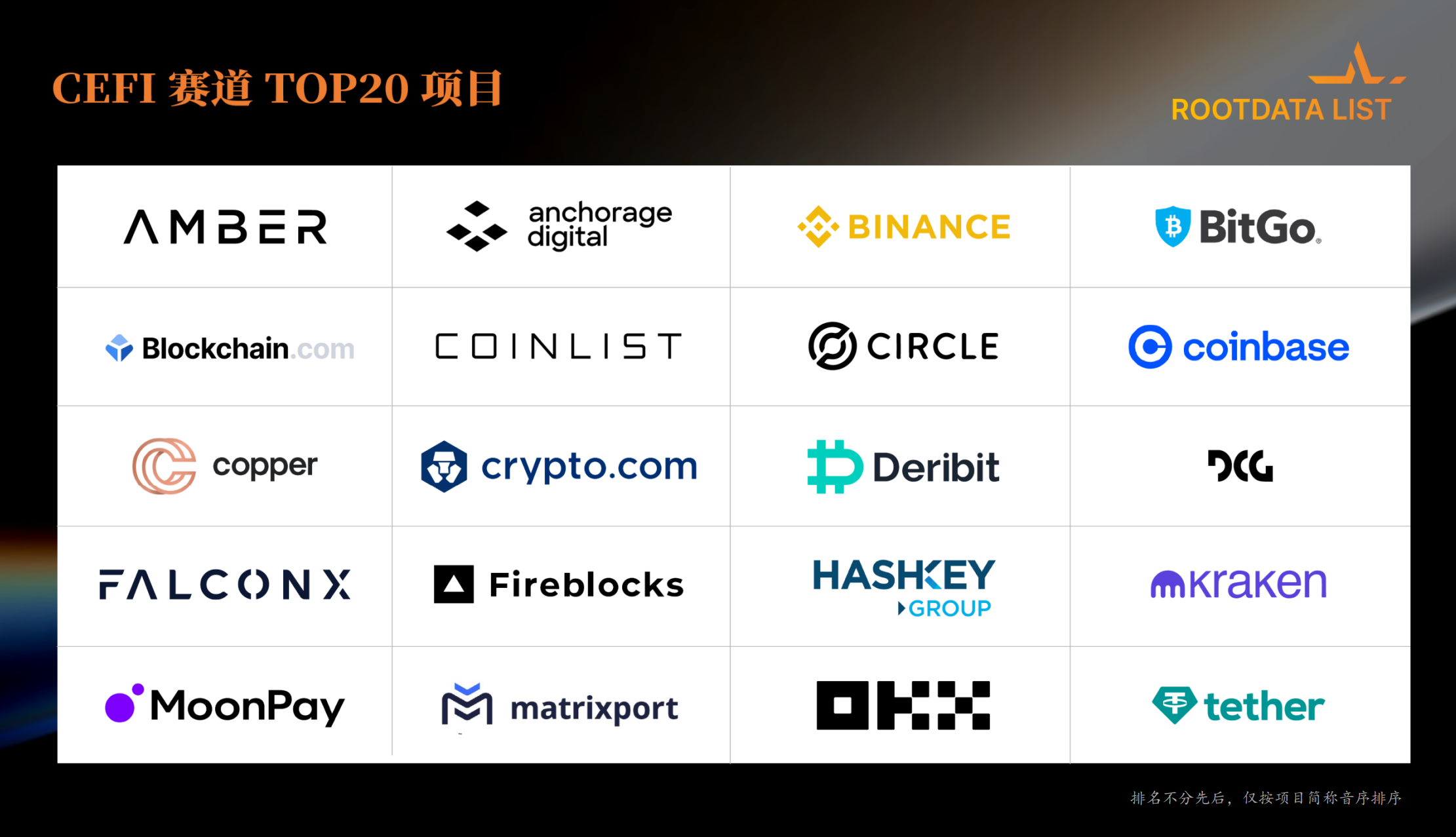

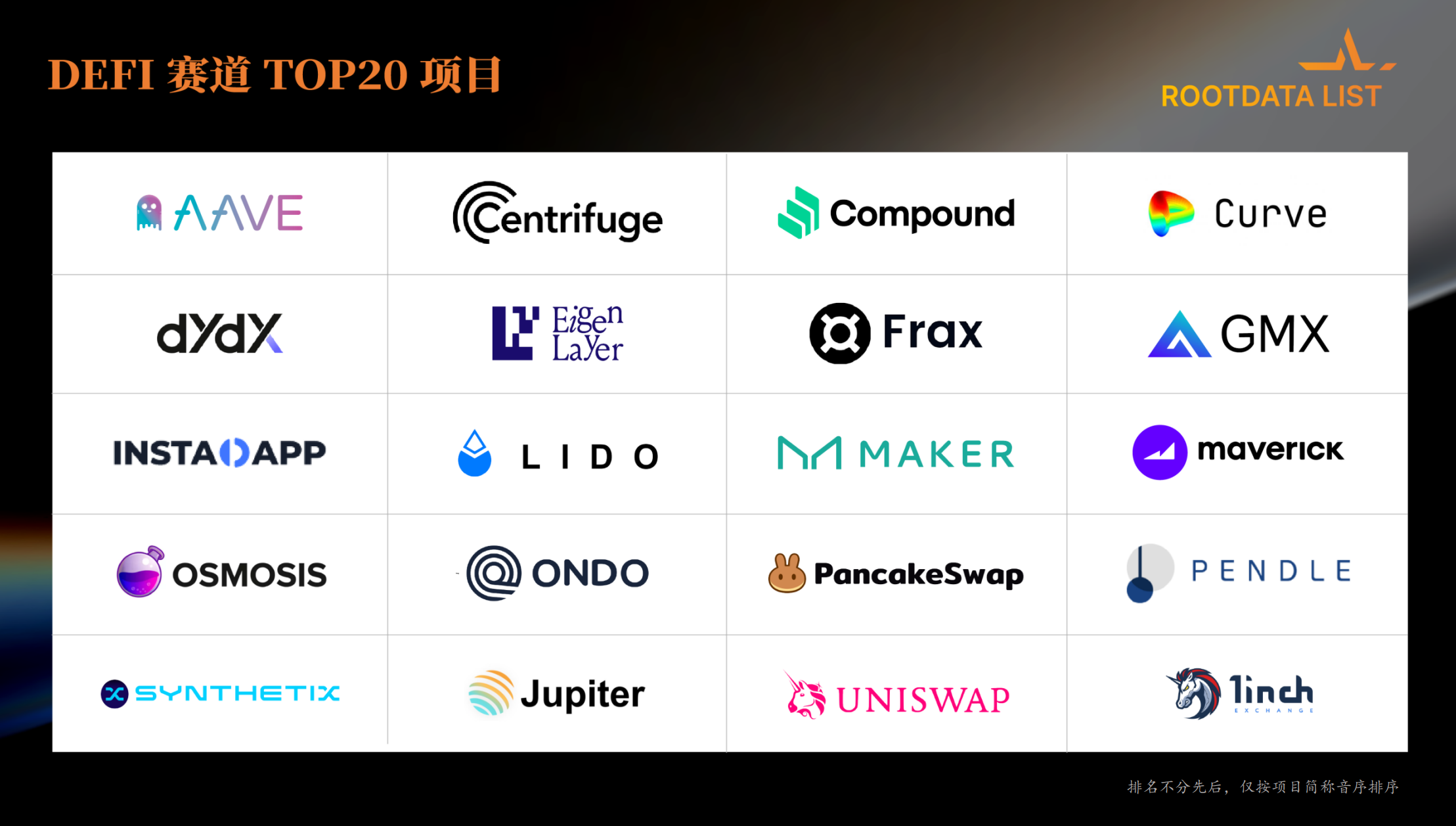

IV. 2023 ROOTDATA LIST

Web3 is becoming an undeniable transformative force globally. To clearly highlight these impactful contributors, RootData leverages its leading and rich data resources, supported by tens of millions of user visits and queries. Adhering to principles of professionalism, objectivity, rigor, and fairness, we aim to create a data-driven, industry-recognized ranking—the ROOTDATA LIST—to showcase more representative players in the Web3 space and promote high-quality industry development.

The 2023 ROOTDATA LIST includes: Top 50 Web3 Projects, Top 100 Web3 Investment Institutions, Top 20 CeFi Projects, Top 20 DeFi Projects, Top 20 Layer1 Projects, Top 20 Layer2 Projects, Top 20 GameFi Projects, and Top 20 SocialFi Projects.

Evaluation Criteria:

Institution Evaluation: Core metrics include number of investments, lead investment count, portfolio quality, media热度, and RootData热度.

Project Evaluation: Core metrics include market cap/valuation, media热度, total value locked (TVL), funding amount, RootData热度, quality of investors, and narrative and sector positioning.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News