Arthur Hayes: Predicts cryptocurrency may see a sharp decline in March this year, followed by a rally

TechFlow Selected TechFlow Selected

Arthur Hayes: Predicts cryptocurrency may see a sharp decline in March this year, followed by a rally

I like to buy well-performing stocks when the market starts viewing as possible what it previously considered impossible.

By ARTHUR HAYES

Translated by TechFlow

Arthur Hayes released his new article on January 5, outlining his outlook for early 2024 market conditions and his trading strategy. TechFlow has translated the full text.

(The views expressed below are those of the author alone and should not be taken as investment advice, nor should they be interpreted as a recommendation or encouragement to engage in any investment activity.)

In the blizzards of Hokkaido, trees give me direction, just as central bankers and politicians provide guidance when I invest in global capital markets. While no trader can predict the future, we can observe markets and assign probabilities to various outcomes. When the market’s implied probability of an event diverges from our own assessment, a trading opportunity arises.

The crypto bull market is still in its early stages, but we must temper our enthusiasm. Just as Bitcoin generates a block every ten minutes, the current flawed fiat financial system is approaching its predetermined, ignoble end. Though I am confident about this ultimate outcome, the path forward remains uncertain. We must remain vigilant and position our bets accordingly.

In short, I have already deployed sufficient capital for this phase of the cycle—selling fiat and buying cryptocurrencies. I am preparing for a sharp downturn across all crypto assets in March, anticipating various events that signal this will occur. I will explain my reasoning and the turning points I’ll watch for—those that will give me the confidence to use Bitcoin put options to aggressively short the crypto market, sell U.S. Treasury bills (T-bills), and then buy more Bitcoin and other cryptocurrencies.

Variables

There are three conflicting variables in March, each framed as a question.

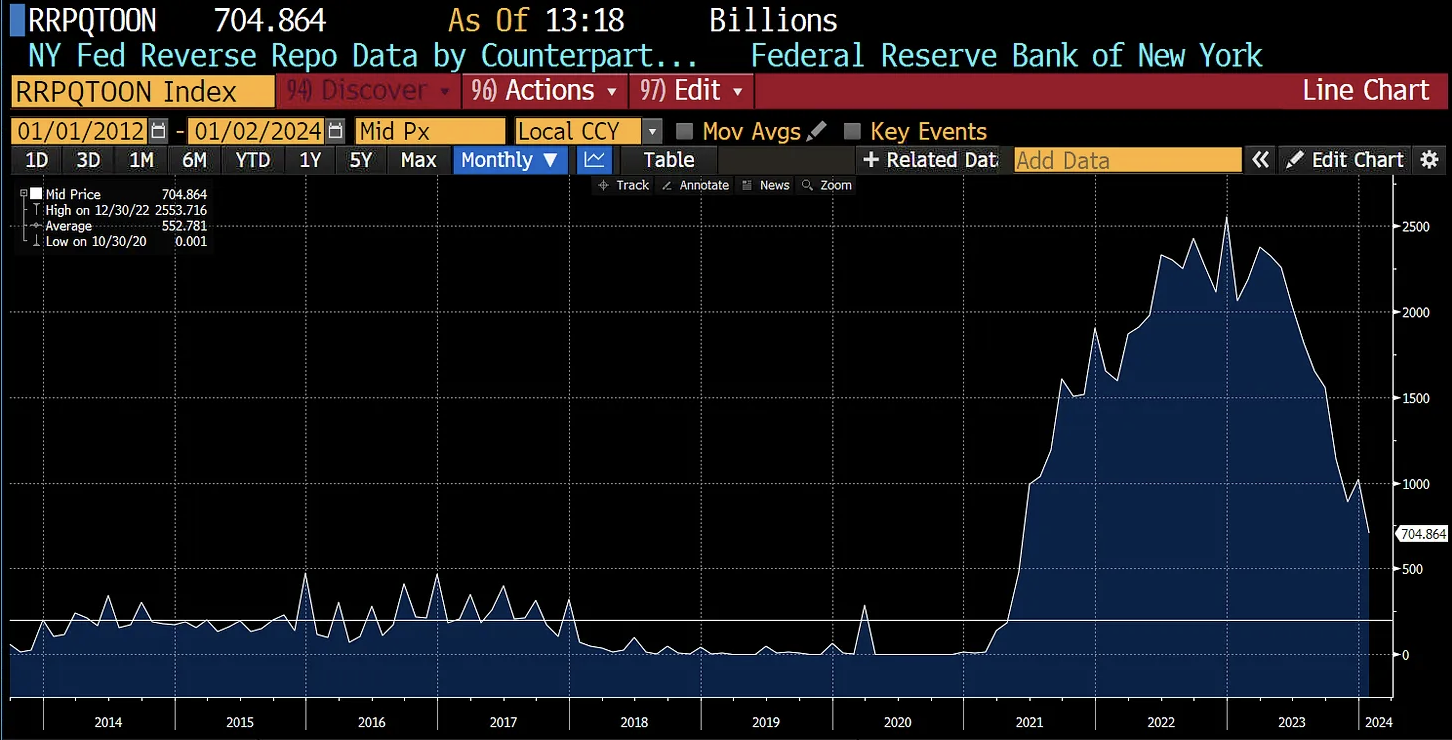

When will Reverse Repo Facility (RRP) balances approach zero?

Reducing RRP balances injects liquidity into financial markets. When this figure nears zero—which I define as $200 billion in liquidity—the market will wonder what comes next and whether another source of dollar liquidity will emerge to sustain the rally.

For a deeper understanding of how declining RRP balances inject liquidity into the system, please read my article "Bad Gurl."

This chart shows the RRP balance since inception. The horizontal white line marks $200 billion.

I believe RRP balances will reach $200 billion by early March. This estimate is based on the rate of decline observed from different starting points in 2023.

Will the Bank Term Funding Program (BTFP) continue?

On March 12, insolvent banks must find cash to swap for U.S. Treasuries and other qualified bonds they repoed to the Federal Reserve. Ultimately, this decision rests with Yellen, the U.S. Treasury Secretary. In the weeks leading up, markets will begin questioning whether the BTFP will be extended.

Under the original BTFP terms, banks could post $80 worth of U.S. Treasuries in the open market and receive $100 in cash. At maturity, they must repay $100 to retrieve their original collateral. If that cash went to fleeing depositors, how will banks raise $100 without issuing more equity or high-yield debt?

To understand why BTFP was created and how it affects the pace and scale of fiat devaluation, please read my article "Kaiseki."

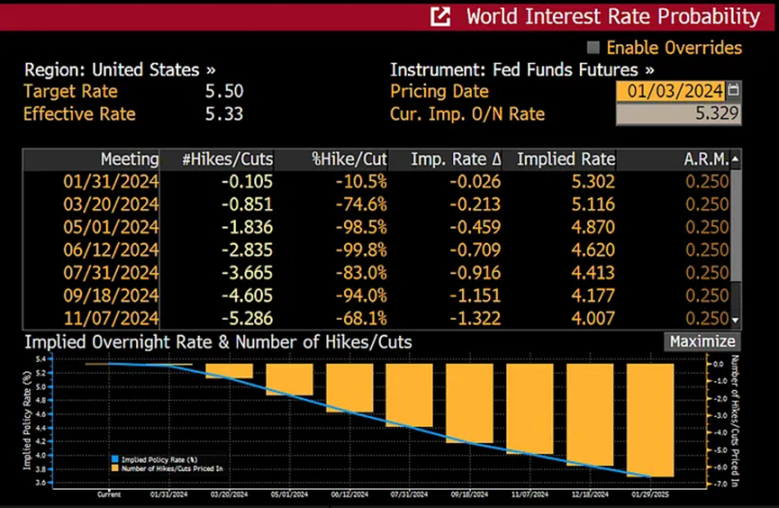

Will the Fed cut interest rates?

The Fed’s March meeting concludes on the 20th. Currently, markets expect the first rate cut since hiking began in March 2021, with at least a 0.25% reduction.

This chart shows Fed funds futures pricing the probability of rate changes at upcoming meetings. As of January 3, markets price in a 75% chance of a 0.25% cut.

These variables are interdependent. Their sequence matters, as it will shape market assumptions about how much dollar liquidity the Fed and Treasury will—or won’t—provide going forward.

If My Predictions Are Correct

Now we must assign probabilities to different scenarios and forecast market reactions.

Speed of RRP Drawdown

If RRP balances approach zero by early March, financial markets will start falling. Remember the surge in Treasury yields coinciding with the stock market plunge? That spike began on November 1, triggered by the quarterly Treasury Debt Management Report released that day (TechFlow note: these reports aim to provide transparency on government borrowing needs and strategies, informing investors and markets about upcoming auctions, types and sizes of securities issued, and any shifts in debt management policy. They are crucial to financial markets as they influence interest rates and investment decisions.)

That report confirmed the U.S. Treasury would shift more borrowing to the short end of the yield curve. With increased T-bill supply and higher yields, money market funds (MMFs) gained economic incentive to use cash parked in the RRP to buy T-bills. All else equal, the decline in RRP balances added liquidity to the system—this is why global bond and stock markets rallied sharply.

The white line is the 10-year Treasury yield; the yellow line is the spread between 10-year and 2-year yields. As you can see, yields peaked in late October in a bear steepening move—both lines rising together. Then, in early November, a violent short squeeze erupted in bonds, sending yields plummeting.

Without another fresh source of dollar liquidity, I believe bonds, stocks, and even crypto will suffer. I’ll elaborate in the tactical trading section, but I will buy a large position in Bitcoin put options at that time.

We cannot know in advance how fast the RRP will decline. Therefore, I will closely monitor its pace. If it deviates materially from my forecast, I will adjust my trading strategy accordingly. Regardless, I bought heavily into crypto in the second half of 2023, and I believe this period—from now through April—is not an ideal time to be bullish on crypto.

Bank Term Funding Program (BTFP)

2024 is a U.S. election year, and ordinary Americans are tired of bailing out bankers. Thus, I believe Yellen will let BTFP expire to demonstrate strength in the U.S. banking system. However, once several large non-TBTF banks (TBTF meaning “Too Big To Fail”) face insolvency due to near-zero equity and depleted regulatory capital, Yellen will be forced to inject more liquidity via a revived BTFP.

With RRP liquidity drained and printed money insufficient to cover bond losses on non-TBTF bank balance sheets, global financial markets will be severely hit. Financial asset holders will take heavy losses, forcing the Fed and Treasury to restart stimulus. These dynamics are correlated. All assets—including crypto—will fall together as markets fear a return to free-market discipline and the purge of insolvent banks from the system.

March FOMC Meeting

BTFP expires on March 12; the Fed’s rate decision comes on March 20. Six trading days separate these two pivotal moments. If my forecast holds, market conditions during this window will push some banks into collapse, forcing the Fed to cut rates and reinstate BTFP.

Technically, the U.S. Treasury cannot lend directly to banks—that’s the Fed’s role. But if the Fed incurs losses by accepting collateral worth less than the dollars lent, those losses flow to the Treasury and ultimately to U.S. taxpayers, who must borrow more to cover the Fed’s shortfall.

Bitcoin will initially drop sharply with broader financial markets but rebound before the Fed meeting. This is because Bitcoin is the only globally traded, neutral hard currency reserve asset that isn’t someone else’s liability within the banking system. Bitcoin knows that when things go bad, the Fed always responds with liquidity injections. It may come under a new name to confuse TikTok news consumers, but rest assured, Bitcoin knows—no matter the disguise, printed money is always printed money. Thus, Bitcoin will surge both before and after the Fed ultimately capitulates and reactivates the printing press.

If My Predictions Are Wrong

If I’m wrong, the following will happen:

-

The Reverse Repo Program (RRP) will decline slowly, continuing to support financial markets into late Q2

-

Yellen will clearly signal before March 12 that BTFP will be extended

-

The Fed’s March decision becomes irrelevant. Whether they cut, hold, or hike, the net effect—combined with continued dollar liquidity injections from the Fed and Treasury—remains stimulative.

If the RRP drawdown is slower than expected, I will refrain from establishing my put option position in early March. Moreover, the moment Yellen signals BTFP extension, I will exit my non-trading zone and resume selling Treasuries to buy Bitcoin and other cryptos.

Trading Strategy

Let’s return to my base case: RRP drains by early March, BTFP expires on the 12th but is reinstated by the 20th, and the Fed cuts rates. Now I’ll detail my trading plan.

Bitcoin Put Options

As many of you know, I hold a diversified crypto portfolio. My largest positions are Bitcoin and Ethereum, making up about 70% of my holdings. My other crypto assets are far less liquid, especially their derivatives. Therefore, if I want a liquid macro hedge for crypto, I must use Bitcoin derivatives. I use the term “hedge”—but this is actually a trade, designed to resolve within two weeks. Since it’s a trade, I’ll use options, which let me cap my maximum loss at the premium paid for the put. An added benefit is that I don’t need to monitor margin levels like with perpetual swaps or futures contracts.

I expect Bitcoin, regardless of its price in early March, to undergo a 20%–30% correction. If spot Bitcoin ETFs in the U.S. have already launched, the shakeout could be worse. Imagine hundreds of billions in fiat flowing into these ETFs, pushing Bitcoin above $60,000 toward the 2021 high of nearly $70,000. Then, with a sudden withdrawal of dollar liquidity, I could easily see a 30%–40% pullback. This is why I cannot buy Bitcoin until after these key March decision dates pass.

I consider myself a focused trader. I’ll try to top-pick the market in late February and then buy a substantial put position. I’ll purchase puts expiring on June 28. I won’t choose March 29 expiry, as I’m entering in early March. High negative theta would overwhelm any delta, gamma, or vega gains. A longer-dated option is more expensive, but with over a quarter until expiry, time decay won’t erode value as quickly.

I’ll set a maximum loss amount—relatively large compared to my standard trade size—and buy puts accordingly. To get meaningful upside on these puts, I’ll select a strike price 20%–25% out-of-the-money, based on the current June quarterly futures price.

Exiting the Position

Many traders, especially option traders, are good at entry but fail at exit. Because option returns are path-dependent, you can be right on direction but still lose money by holding too long. Every day I hold these puts, I lose money. If my forecast is correct, the market should begin a notable correction around March 12. Between the 12th and 20th, I’ll try to exit at lows and lock in profits. If my policy call is right but Bitcoin holds steady or rallies, I must immediately close my put position.

Bull Market Continues

By late March, we’ll be back on track. Yellen and Powell will reaffirm their commitment to preserving the solvency of the U.S.-led fiat financial order. Once this brief market turbulence passes, crypto can once again surge on expectations surrounding the upcoming Bitcoin block reward halving. I will resume selling Treasuries and buying Bitcoin and other cryptos.

Unexpected Variables

This article focuses entirely on decisions by the two stewards of the U.S.-centric financial system. But other key players in the fiat system cannot be ignored.

China

Taiwan’s elections could result in a pro-China candidate winning, prompting Beijing to turn on the yuan printing press. A flood of yuan credit into global markets could overshadow any issues in the U.S. banking system. Even if RRP dries up and BTFP isn’t renewed, crypto could still rise. In that case, I might skip buying puts and instead increase my crypto exposure.

Japan

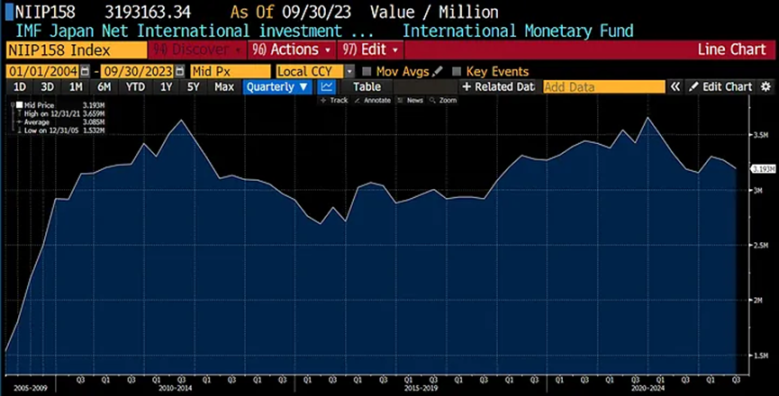

The Bank of Japan is currently allowing Japanese Government Bond (JGB) yields to rise gradually. If JGB yields continue climbing, Japanese corporations, pension funds, insurers, and households will have strong financial incentives to repatriate capital. They’ll sell U.S. Treasuries and buy JGBs, attracted by better domestic yields. If this trend accelerates, I will certainly write a detailed piece on it. Given Japan’s status as the largest holder of U.S. Treasuries and the world’s biggest international creditor (based on net international investment position), private-sector rebalancing could exert significant upward pressure on long-end U.S. Treasury yields.

IMF data estimates Japan’s net international investment position at a positive $3.3 trillion.

This pressure could emerge before early March, forcing the U.S. to resort to further money printing. If so, I might not even get a chance to make this trade—Yellen could renew BTFP and introduce a novel easing mechanism before mid-March. One candidate is a new Treasury program to issue more short-term debt to buy existing long-dated U.S. Treasuries. This would be a mild form of yield curve control, which she might call a "repo program." There was an explanatory paper on this last year—click here if you're interested.

Final Thoughts

As the new year begins, with central banks printing money in various forms and spot Bitcoin ETFs expected to launch in the U.S. and Hong Kong, downside risks are mounting. Being bullish now isn’t hard. I prefer buying strong performers when the market believes something impossible is becoming possible. From a trading perspective, taking a contrarian view at these binary junctures offers better risk-reward. I may ultimately be wrong. But if I’m right on expected value, my returns will vastly exceed those of the consensus crowd.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News