10,000-Word Web3 Research Report: 2023 Panoramic Review and 2024 Trend Outlook

TechFlow Selected TechFlow Selected

10,000-Word Web3 Research Report: 2023 Panoramic Review and 2024 Trend Outlook

Also this year, people questioned narratives, understood narratives, and became narratives.

Author: Odaily Planet Daily Editorial Team

2023 has been a year of rapid transformation and intensifying divergence.

Old conflicts have yet to subside as new battles emerge. Technology blockades and economic suppression continue to escalate.

AI, represented by ChatGPT, has entered large-scale commercialization, accelerating the debate between accelerationism and technological pessimism at what may be the dawn of humanity's most significant innovation revolution. The much-hyped online duel between two social media giants—Musk and Zuckerberg—ended without materializing. Meanwhile, globally influential cultural, entertainment, pop culture, and consumer phenomena were notably absent. These trends appear to be inevitable outcomes of deepening pluralistic values.

Under shifting demographics and macroeconomic conditions, industries that once drove high GDP growth—such as real estate and (mobile) internet—are losing their luster. In contrast, sectors like intelligent manufacturing, AI, materials, and energy are on the rise. People in this region have finally resumed "normal" offline lives, attempting to recover lost years, while simultaneously grappling with massive layoffs and cost-cutting measures across companies.

Focusing on the Web3 domain, against this backdrop of fragmentation and change, small but constant efforts have emerged to bridge divides and adapt for survival.

Externally, progress accelerated toward Bitcoin spot ETF approvals, with institutional capital increasingly digesting the benefits; cryptocurrency adoption as a payment method steadily increased; Worldcoin collected over 2.53 million iris scans within 130 days; U.S. Treasuries found integration into DeFi through RWA; CZ stepped down, leaving other compliant participants to cautiously navigate turbulent regulatory waters following Binance’s path; amid ongoing confrontations between crypto firms and U.S. regulators, Hong Kong continued to roll out favorable policies; SBF was convicted, and the mess left from 2022 is being gradually cleaned up; the collapse of Silicon Valley Bank and USDC's de-pegging forced us to reassess the risk gap between traditional and crypto finance.

Bitcoin’s ecosystem experienced a renaissance, with renewed innovation in asset issuance methods and protocol standards, bringing fresh narratives back to the oldest and most consensus-driven public chain. Inscriptions and meme culture spread across multiple chains, as “innovators” wielding fairness as a pass sought to redistribute value. Ethereum completed its Shapella upgrade, ending mining and enabling staking withdrawals—Lido, the leading LSD protocol, rose to become the top DeFi TVL holder. EVM maintained its primacy while both established and emerging L2s intensified competition at the foundational layer.

On the application front, 2023 saw no summer boom. DeFi, NFTs, and GameFi remained largely stagnant with low-frequency minor innovations and stable market structures. Only the Blur+Blend+Blast family stirred mild interest. Fortunately, AI+Crypto applications gained momentum, integrating into social platforms, Q&A systems, data analytics, and trading tools.

This year also marked a shift where people questioned narratives, understood them, and ultimately became part of them. Critics, observers, and builders competed for control, weaving three thematic variations into a symphonic poem of Web3 in 2023.

In this long-form report, Odaily Planet Daily will review major events, interpret data, and analyze industry trends—from macro markets to micro sectors—to offer a panoramic reflection on 2023 and forecast developments for 2024.

Regulatory Policies: U.S. Tightens Grip While Hong Kong Moves Forward Boldly

In 2023, the U.S. Securities and Exchange Commission (SEC), along with other regulatory bodies such as the Department of Justice, adopted stricter oversight over the cryptocurrency industry.

From actions targeting Genesis Global Capital and Gemini Trust Company’s crypto lending programs, to enforcement against Kraken and SushiSwap, lawsuits filed against Tron founder Justin Sun, and legal proceedings involving Coinbase and Binance—these events highlighted regulators’ tough stance on an industry still perceived as operating in a “Wild West” environment, aiming to bring greater standardization to the entire sector.

Notably, even large exchanges like Coinbase and Binance, which had previously expressed willingness to cooperate with regulators, were not spared—demonstrating that scrutiny extends beyond smaller or marginal players to encompass the entire industry.

During bull markets, pressure from corporate legal teams, legislative bodies, and public opinion often restrained full regulatory enforcement since all parties benefited. However, during bear markets, regulators leveraged incidents like FTX’s collapse as justification to tighten oversight.

Yet, from another perspective, these legal actions and rulings brought a degree of clarity and predictability to the crypto space in 2023.

For instance, the Ripple case ruling clarified the legal status of digital assets like XRP, while Grayscale’s successful lawsuit demonstrated viable paths for legal challenges. Additionally, Binance and its CEO CZ reaching settlements with the U.S. Department of Justice showed that cooperation could lead to dispute resolution. This gradual clarification of the regulatory landscape signals positively for crypto firms, suggesting they can operate under clearer, more stable frameworks rather than in constant uncertainty.

Despite challenges, the industry appears to be maturing after navigating this wave of legal and regulatory scrutiny.

Across the Pacific, Hong Kong—the historic financial bridge between East and West—has opened its arms to Web3.

Top officials including Chief Executive John Lee and Financial Secretary Paul Chan frequently voiced strong support for Web3 development in Hong Kong, attracting global crypto enterprises and talent. On policy fronts, Hong Kong introduced a licensing regime for virtual asset service providers, allowed retail trading of cryptocurrencies, launched a multi-million-dollar Web3 Hub ecosystem fund, planned investments exceeding HK$7 billion to accelerate its digital economy and virtual asset industry, and established a dedicated Web3.0 Development Task Force.

On the institutional side, the first HK$800 million tokenized green bond offering was successfully issued. Regulated player Hashkey Exchange steadily expanded product offerings and plans to launch its platform token HSK. Crypto group BGX invested in licensed exchange OSL, which partnered with Victory Securities to provide BTC and ETH trading services to Hong Kong retail clients. Futu’s virtual asset trading platform PantherTrade submitted a license application to the SFC, and numerous virtual banks and insurers formed partnerships with trading platforms.

However, rapid advancement attracted risks. Unlicensed exchange JPEX was involved in cases exceeding HK$1 billion, HOUNAX fraud surpassed HK$100 million, and HongKongDAO and BitCuped were suspected of virtual asset fraud—prompting heightened attention from the SFC and police. The SFC stated it would collaborate with law enforcement to develop risk assessment criteria for virtual asset cases and conduct weekly information exchanges.

Beyond the U.S. and Hong Kong: In January, South Korea lifted restrictions on security token issuance; in August, Europe’s first spot Bitcoin ETF (Jacobi FT Wilshire Bitcoin ETF) launched; in September, Japan permitted startups to raise funds via crypto; in October, G20 leaders released a joint communiqué unanimously adopting a crypto regulatory roadmap; Singapore plans to ban margin or leveraged crypto trading by mid-2024 to curb retail speculation.

Secondary Market: Recovery, Preparation, and Structural Shifts

In 2023, the market gradually emerged from deep bear territory, transitioning from the post-FTX crypto winter into a modest spring rally.

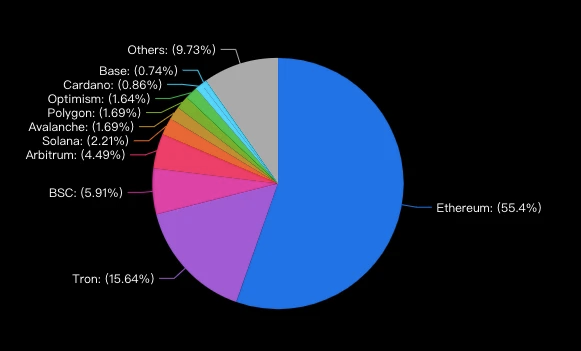

Overall, according to Coingecko, the total crypto market cap stood at approximately $831.7 billion at the start of the year. It then climbed steadily, surpassing $1.62 trillion by December 12—a near doubling from年初 levels, approaching the market cap of Alphabet ($1.67 trillion), the world’s fourth-largest company.

During this critical transition phase, BTC and ETH saw significant shifts in their combined market dominance: Bitcoin rose from 38.31% at the beginning of the year to 49.5% currently; ETH initially increased from 17.45% to above 18%, before retreating to 16.2% today—failing to keep pace with BTC’s capital inflows.

In terms of price, Bitcoin rose from $16,615 at the start of the year, breaking $20,000 on January 14, surpassing $30,000 on April 11, adjusting throughout the next six months before reclaiming $30,000 on October 22, and officially crossing $40,000 on December 3. By December 12, it reached $41,890—2.5 times its年初 level. ETH similarly climbed from $1,200, breaking $2,000 on April 13, fluctuating between $1,500 and $2,000 until December when it stabilized above $2,000, closing at $2,232 on December 12—an 86% increase from年初.

By year-end, most top 100 market-cap tokens benefited from the rally with substantial gains—only a few, such as SUI, BLUR, APE, CAKE, and ALGO, declined.

Among the top 20 market-cap tokens, three notable performers stood out:

1. Solana (SOL): Benefiting from news about FTX relaunching, SOL surged from $9.97年初 to $66 now—a 579.57% gain—ranking sixth in market cap;

2. Chainlink (LINK): Riding the broader market recovery, LINK climbed from $5.62年初 to $14.17—a 154.46% increase—now ranked fourteenth;

3. Bitcoin Cash (BCH): Influenced by Bitcoin’s popularity, BCH rose from $95.96年初 to $227.48—a 134.33% increase—now ranked nineteenth.

L2-related concepts heated up this year. According to Coingecko, L2 tokens now have a combined market cap of $16.78 billion. The top five are Polygon ($7.89B), Immutable ($2.6B), Optimism ($1.95B), Mantle ($1.786B), and Arbitrum ($1.45B)—with IMX and OP seeing annual growth exceeding 80%.

Modular blockchains: Leading project Celestia launched its mainnet in late October, with its TIA token rising 188% within a month.

AI: Following ChatGPT’s release in late 2022, 2023 marked the dawn of large AI model applications. AI-themed tokens generally posted strong gains. High-market-cap representatives include Bittensor ($1.785B, +178%) and Render ($1.498B, +734%). In July, Sam Altman’s crypto venture Worldcoin officially launched, debuting around $2, dipping to ~$1 in September, then slowly recovering to $2.38.

Platform tokens: As of December 12, platform tokens had a total market cap of $65.321 billion. Top five: BNB ($37.962B), UNI ($4.58B), OKB ($3.605B), LEO ($3.449B), CRO ($2.584B). Best performers: RUNE (+297.61%), BGB (+168.79%), OKB (+117.03%). Notably, FTT, despite last year’s collapse, rose 246.49% due to FTX relaunch rumors.

Stablecoins: As of December 12, stablecoin market cap reached $129.8 billion, accounting for 8.0% of total crypto market cap. Dominated by USDT ($90.5B), USDC ($24B), DAI ($5.28B), TUSD ($2.6B), BUSD ($1.47B). Compared to last year’s tripartite balance among Tether, USDC, and BUSD, both USDC and BUSD saw significant declines this year.

In March 2023, Circle, issuer of USDC, faced turmoil when Silicon Valley Bank (SVB) encountered liquidity issues. With $3.3 billion held at SVB, USDC temporarily lost its peg. Circle’s close ties to the U.S. banking system damaged credibility, reducing USDC circulation. Both Circle and Tether invested reserves (Circle: $24B, Tether: $87B) in U.S. Treasuries for yield, but USDC’s shrinking share poses greater IPO challenges. Its market cap dropped from $44B in January to $24.5B by end-November—a 44.32% decline.

In February, the SEC issued a Wells Notice to Paxos, signaling potential litigation over Binance USD (BUSD) being unregistered securities. Simultaneously, NYDFS ordered Paxos to halt minting new BUSD. Paxos announced it would stop issuing BUSD from February 21 but continue supporting redemptions until at least February 2024. CZ believed the SEC’s move could profoundly impact the industry, expecting users to migrate to other stablecoins. Speculation suggests the action may relate to BUSD’s yield-bearing features or broader classification as a security. Since then, BUSD’s market cap plummeted from $16B年初 to ~$1.69B. In November, Binance announced phasing out BUSD and converting holdings to FDUSD.

Conversely, USDT’s market cap surged due to users fleeing other stablecoins, rising from $66B年初 to $90.5B by end-November—a 37.12% increase. PayPal’s PYUSD and Aave’s GHO also launched, diversifying the stablecoin ecosystem.

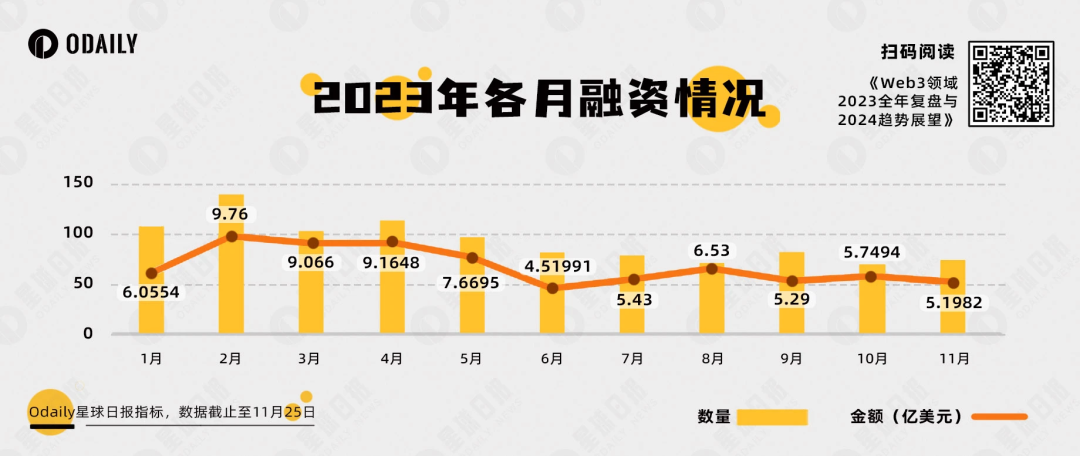

Primary Market: Over $7.4 Billion Raised Amid Low-Tide Anticipation

According to incomplete statistics from Odaily Planet Daily, as of November 25, 2023, the crypto industry disclosed 1,023 funding rounds—a 38.3% YoY decrease—with total disclosed funding amounting to ~$7.44 billion—down 78.74% YoY.

Number and value of funding deals Jan–Nov 2023

In 2023, Web3 primary market fundraising averaged nearly 100 deals per month, showing relative consistency but overall decline. Fundraising amounts were higher in the first five months compared to the latter six.

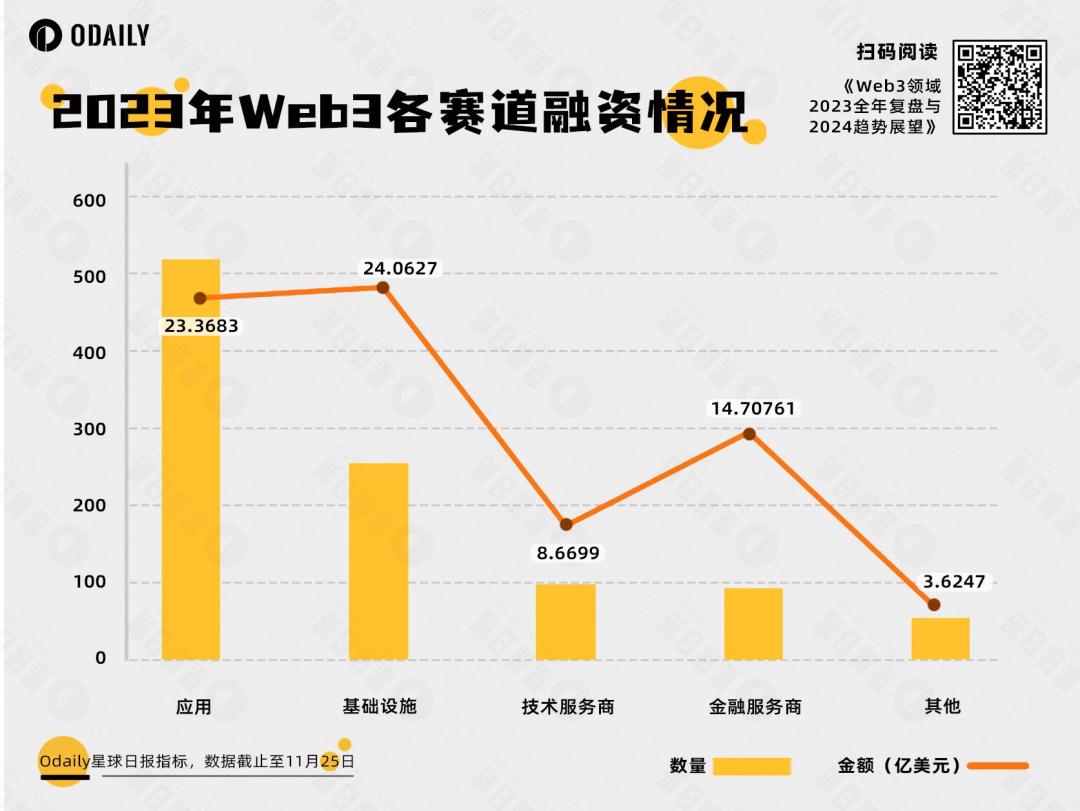

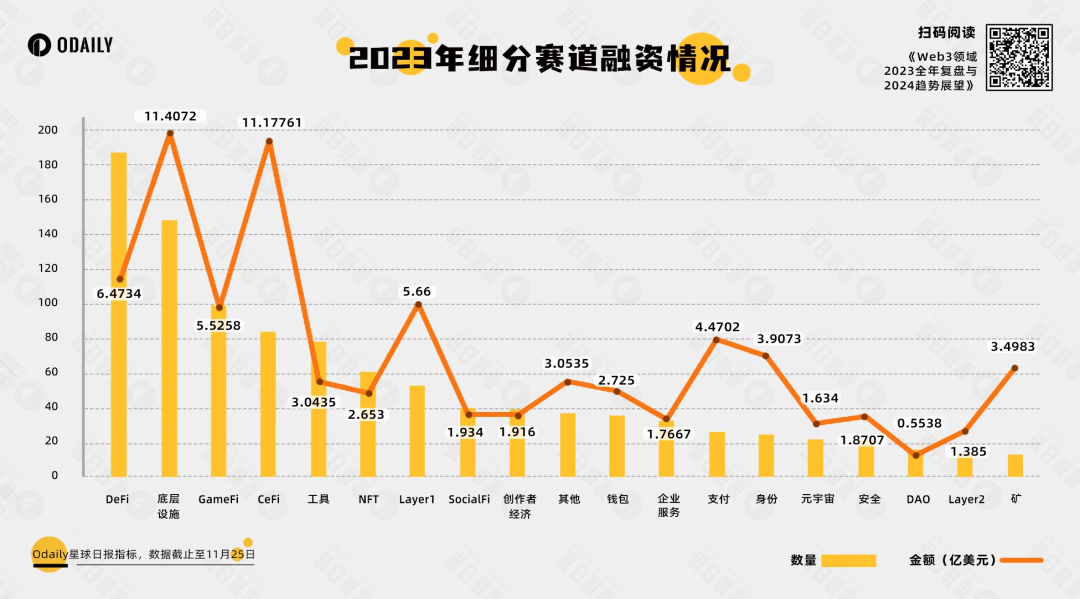

Analyzing funded projects based on business type, target audience, and business models, Odaily Planet Daily categorized disclosed projects into five major sectors—infrastructure, applications, technology service providers, financial service providers, and other service providers—and further细分 into DeFi, base infrastructure, GameFi, CeFi, tools, NFTs, and Layer 1.

As shown above, application-focused projects dominated 2023 with over 500 funding rounds—indicating a slowdown in Web3 infrastructure development and urgent demand for “fat apps” with mass adoption potential.

In terms of sub-sector deal counts, DeFi led with 187 rounds. Institutional trading platforms and order-book-based DEXs built on high-performance blockchains gained traction.

Base infrastructure, perennially favored by investors, secured 148 rounds. More projects began serving traditional industries, diversifying revenue streams.

GameFi and CeFi followed closely with 99 and 84 rounds respectively. GameFi remains a frontline gateway for new Web3 adopters due to gameplay and returns—its consistent ranking reflects investor preference for shorter return cycles.

Emerging patterns included Telegram bots, portal-style platforms, and AI-integrated projects. Telegram bots and app portals offered simple entry points to Web3 for newcomers, while AI+ projects rode the momentum of rapid advancements in artificial intelligence.

During bear markets, capital deployment grew cautious: ~200 projects raised over $10 million each—a 58.68% YoY drop. Yet some still secured nine-figure valuations.

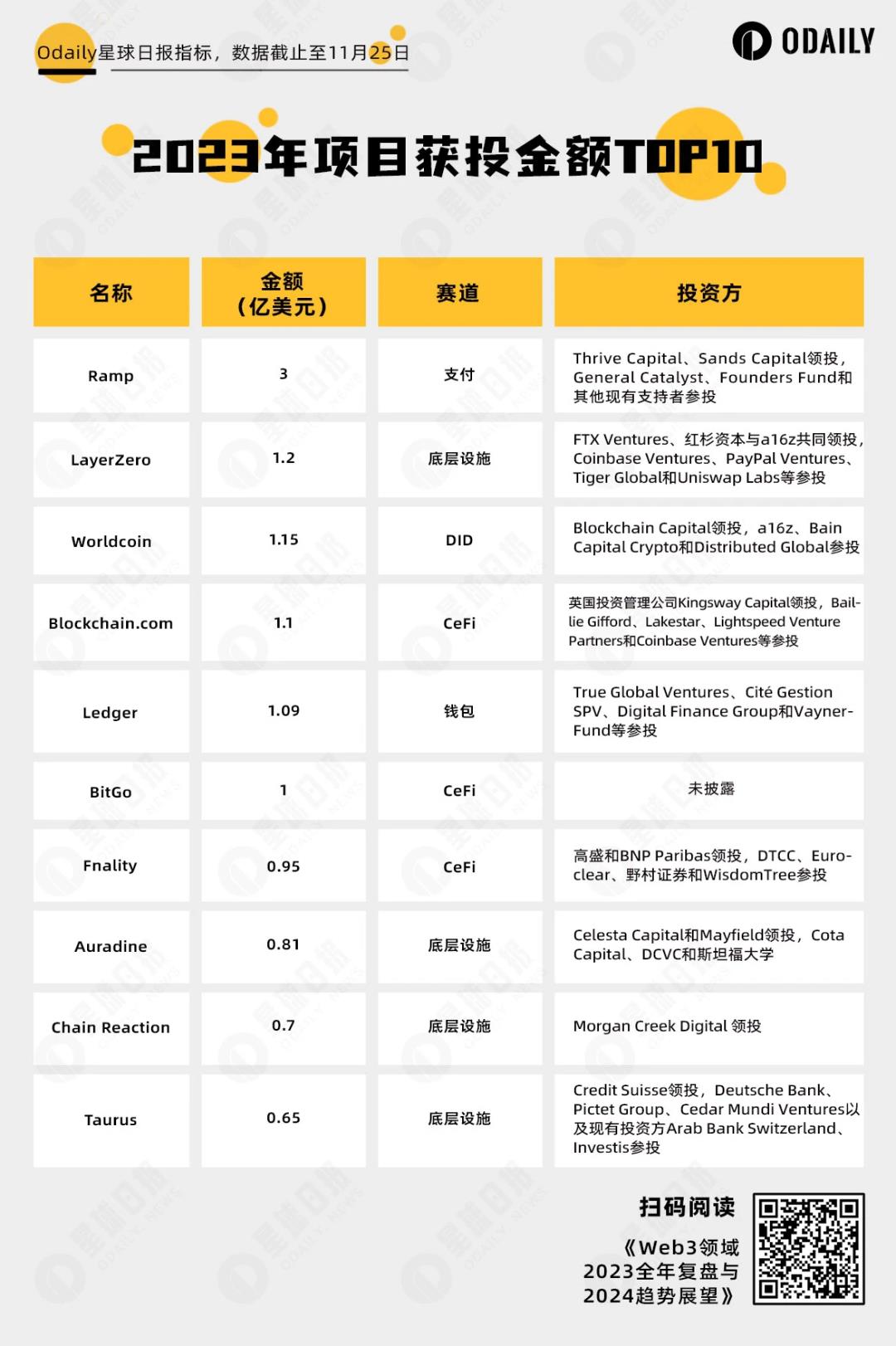

Top 10 Funded Projects in 2023

Ramp, LayerZero, and Worldcoin topped the list by funding amount:

Ramp facilitates fiat payment channels between crypto and traditional markets, providing infrastructure for Web3 capital inflows.

LayerZero attracted backing from prominent Web3 firms like a16z and Coinbase Ventures, as well as traditional institutions like Sequoia Capital and PayPal Ventures.

Worldcoin captured market attention with its team background and futuristic vision of identity in the AI era, positioning itself as a new leader in the DID space and sparking anticipation for AI-era identity systems integrated with Web3.

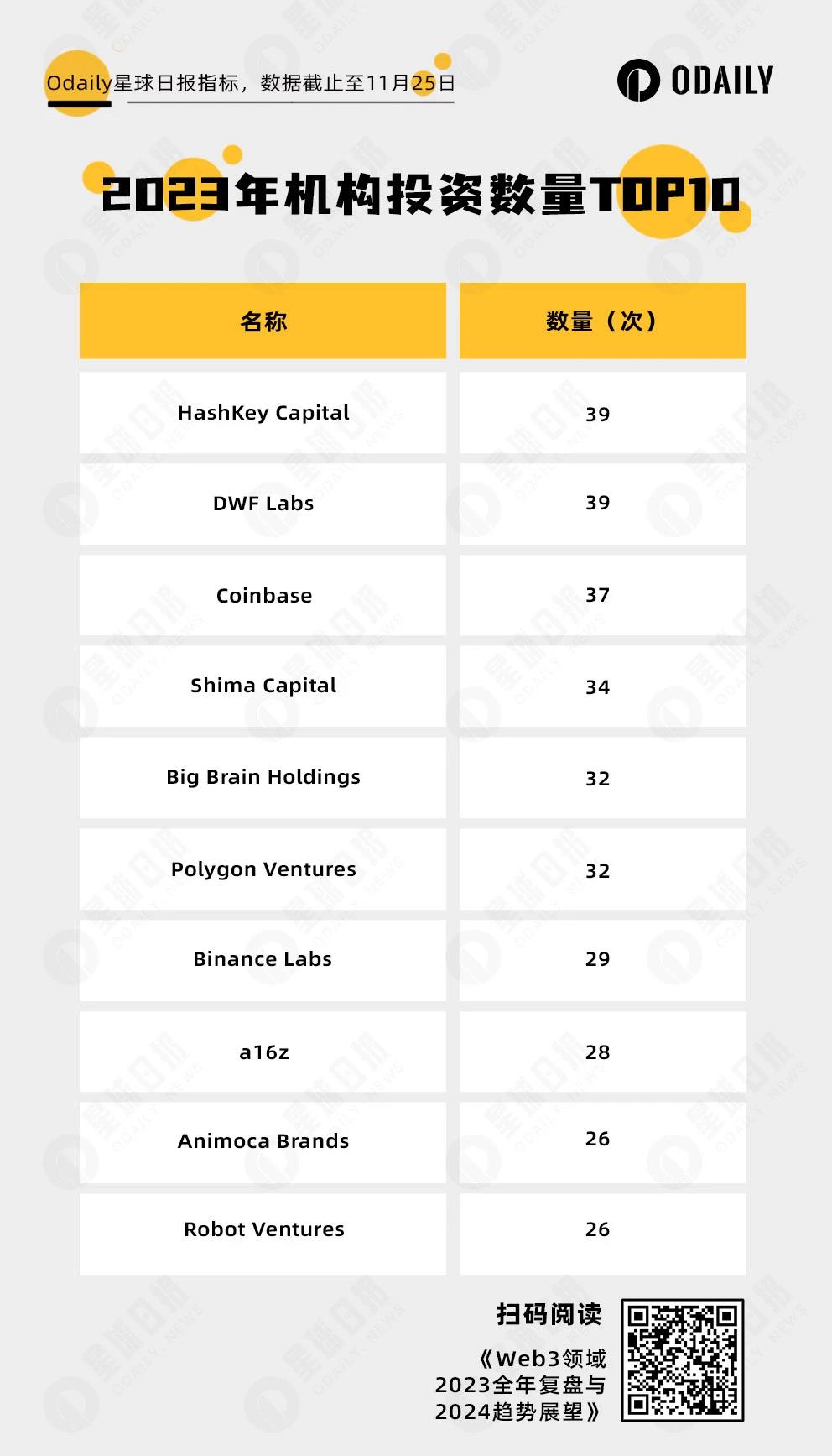

As seen above, HashKey Capital and DWF Labs tied for most active investors this year. Infrastructure and DeFi accounted for nearly two-thirds of HashKey’s portfolio. DWF Labs, known for its market-making style and vertical business approach, focused heavily on Layer 1 and GameFi (combined: 17 deals).

Additionally, several institutions that featured prominently last year—including a16z, Animoca Brands, Shima Capital, and Coinbase—continued making impactful investments despite fewer deals. Projects like Worldcoin, LayerZero, and YGG received notable attention.

Finally, although not topping rankings, Paradigm achieved remarkable results with only six public investments—Friend.tech, Blast, and Flashbots garnered exceptional attention.

Overall, 2023’s primary market fundraising saw severe declines in both volume and value compared to last year, largely due to bearish secondary markets. But the bottom has likely formed, setting the stage for a rebound. Institutions planting seeds today will witness saplings grow into trees tomorrow.

Bitcoin: Two Forces—Bottom-Up Ecosystem Growth and External Capital Inflows

On January 30, Casey Rodarmor’s “Ordinals” protocol launched on the Bitcoin mainnet, charting a bold course for Bitcoin’s ecosystem revival in 2023.

Initially centered on NFTs, Ordinals introduced the “sub10K” concept (inscriptions numbered below 10,000). Early projects varied widely, mostly created organically by community members.

Later, Yuga Labs joined as an early institutional entrant, launching its TwelveFold series. “TwelveFold explores relationships between time, mathematics, and variability,” with artworks internally produced using 3D modeling, algorithmic generation, and advanced rendering tools—paying homage to hand-crafted inscriptions.

Early Bitcoin NFTs primarily mirrored existing collections from other chains—e.g., Ordinal Punks and Bitcoin Punks reused Ethereum’s CryptoPunks images. Verification was rudimentary: comparing images and checking if hashes were original.

Then, BRC-20 mania erupted.

On March 9, Domo proposed a token standard embedding specific text onto Bitcoin as tokens—ORDI, the first BRC-20 token, was born. Soon after, community members deployed meme, punk, pepe, and other ownerless community tokens—sats also emerged on March 9.

In March, BRC-20 tokens drew little attention, traded OTC. By late April, ORDI hit $1, triggering broader BRC-20 rallies. Popular trades remained community-driven—meme, punk, domo, nals, etc.

ORDI later surged past $4, fueling growing enthusiasm. Project-backed tokens emerged—IDO platform TURT, gaming concept ORDZ, etc.

Meanwhile, influential X figures joined in—XEN founder Jack Levin’s related tokens (PUSY, EPIC, DRAC) and his public launch of VMPX caused Bitcoin network fees to spike above 400 sats/byte. Similarly, user BitGod went viral through marketing campaigns, making his OXBT token one of the hottest BRC-20s.

Extreme FOMO signaled an impending turning point. On May 8, Gate.io listed ORDI, peaking at $29.5 USDT, closing at $17.8 USDT. Network congestion prevented users from placing orders—Unisat briefly showed ORDI above $30 USDT. On May 20, OKX listed ORDI, peaking at $17.1 USDT, closing at $12.5 USDT.

The second wave of BRC-20 began on September 25, when the final sats inscription was completed—total mints reached 21,107,258, holders totaled 36,061. Minting started March 9, took six months, and cost over $20 million. That day, the Corsican monster landed at Golfe-Juan, with ORDI closing at $3.6 USDT.

On October 30, UniSat Wallet announced inclusion of 14 inscriptions—sats, ordi, oxbt, meme, vmpx, pepe, etc.—in brc20-swap’s initial mainnet support list.

In early November, sats rallied again, reigniting BRC-20 interest. Animal-themed tokens (“zoo”) rose to prominence—rats, cats, bear, etc.—dominating trading charts.

His Imperial Majesty arrived in faithful Paris on November 7: Binance listing ORDI helped it reclaim ground—peaking at $27.8 USDT on November 24, regaining position as the largest BRC-20 by market cap. On December 7, ORDI hit a record high of $69.7 USDT, surpassing $1 billion in market cap.

On November 16, regular Bitcoin transaction fees rose to 186 sats/byte. Despite soaring inscription costs, user enthusiasm remained undimmed—high-supply BRC-20s like MMSS and Bear quickly completed minting.

With BRC-20 flourishing, competing protocols gained visibility:

Taproot Assets (formerly Taro): A Taproot-powered protocol for issuing assets on Bitcoin, enabling Lightning Network transfers for instant, scalable, low-cost transactions.

Atomicals Protocol: A simple, flexible protocol for creating, transferring, and updating digital objects (NFTs) on UTXO blockchains like Bitcoin. Unlike Ordinals, Atomicals rethinks centralized, immutable, fair token issuance on BTC from the ground up.

BRC-420: Introduces a metaverse digital asset management method, giving creators comprehensive systems to manage, share, and monetize creations via recursion, permissions, and royalties.

While native Bitcoin ecosystems evolved, external conditions shifted dramatically—spot Bitcoin ETF applications paved a compliance path for Bitcoin, while top whales aggressively accumulated, increasing their holdings and influence.

As early as June 29, 2021, Cathie Wood’s ARK Invest filed a Bitcoin ETF application. After multiple delays, it was formally rejected in April 2022. ARK’s second attempt in early 2023 was again denied, submitting a third application in May. Some asset managers remained skeptical about spot Bitcoin ETFs. During this period, spot ETFs had limited market impact.

Until June 15, when reports surfaced that BlackRock—the largest asset manager—would submit a Bitcoin ETF application, igniting market excitement. BTC bottomed at ~$24,800 shortly after—becoming the market’s lowest point post-June. Subsequently, Fidelity (third-largest asset manager) joined the filing queue. News of Franklin Templeton’s application on September 12 triggered the final market bottoming phase. The anticipated inflows from these financial giants made spot ETFs a key factor influencing Bitcoin’s short- and long-term volatility.

Though the SEC repeatedly postponed decisions on spot Bitcoin ETFs in September and November, and false rumors circulated on October 16 about approval of BlackRock’s iShares Bitcoin ETF, most analysts believe approval is inevitable—it’s just a matter of timing.

CME, a traditional financial gateway to crypto options, saw open interest in Bitcoin futures climb, surpassing Binance to rank first—approaching 2021 highs.

MicroStrategy, representing whale accumulation, had acquired 174,530 BTC cumulatively by December 7 at a total cost of $5.28 billion—averaging $30,252 per BTC. At current prices (~$44,000), unrealized profits stand at ~$2.4 billion.

Once viewed as a contrary indicator due to heavy paper losses, MicroStrategy’s continuous buying paid off as the market reversed. The company remains bullish on Bitcoin’s future. During a CNBC interview, co-founder Michael Saylor shared key views:

-

May continue buying—you never say “own too much Bitcoin”;

-

Approval of a Bitcoin spot ETF won’t threaten MicroStrategy—MicroStrategy offers a differentiated product;

-

Post-halving selling pressure will drop from $12B/year to $6B/year—optimistic about the next twelve months;

-

Predicts SEC approval of Bitcoin spot ETFs in Q1 2024 or sometime within the next 12 months.

Ethereum: Maturing Bravely Amid Old Rivals and New Challenges

As a cornerstone of the crypto ecosystem, Ethereum underperformed in 2023. Despite completing the Shapella upgrade (Shanghai + Capella), the subsequent Cancun upgrade was repeatedly delayed, resulting in minimal technical breakthroughs and lackluster news flow. Its price languished until year-end, trailing behind Bitcoin’s rally.

1. Data: Price Stagnation, Declining ETH/BTC Ratio

Throughout 2023, ETH’s price performance can best be described as “flat”—neither matching its 2021 surge from $750 to $4,860 nor its 2022 plunge below $900.

Starting the year at $1,200, ETH moved upward with the broader market but stayed range-bound around $1,500. Seemingly unaffected by external catalysts or headwinds, ETH briefly breached $2,000 after Shanghai’s April launch, peaking near $2,150—but failed to sustain momentum, falling back below $2,000. Only near year-end, as bullish signals solidified, did ETH decisively break above $2,000 again, reaching $2,400—a cumulative gain of 83%.

ETH price trend

ETH’s “flatness” extended beyond price—its market cap share remained consistently around 17%-18% all year, while BTC’s surged, exceeding 50% by year-end. This divergence was starkly visible in the ETH/BTC ratio, which declined from 0.072年初 to below 0.05 in December, stabilizing around 0.052. While longer-term charts show ETH/BTC recovering from lows, whether it can stabilize and resume upward momentum remains uncertain.

ETH/BTC ratio, weekly chart

Ethereum’s DeFi Total Value Locked (TVL) grew roughly in line with price—from $3.4B年初 to $6.4B年末, less than doubling. Given 2023’s harsh industry winter, DEXs, lending, and other Ethereum-based sectors cooled significantly, weakening the once-powerful DeFi ecosystem.

Another notable trend: Ethereum’s LSD (liquid staking derivatives) sector became a market favorite in Q1. With Ethereum’s shift from PoW to PoS, users could stake 32 ETH as validators. However, staking reduced asset liquidity, creating strong demand for liquid staking solutions—hence the rise of LSDs.

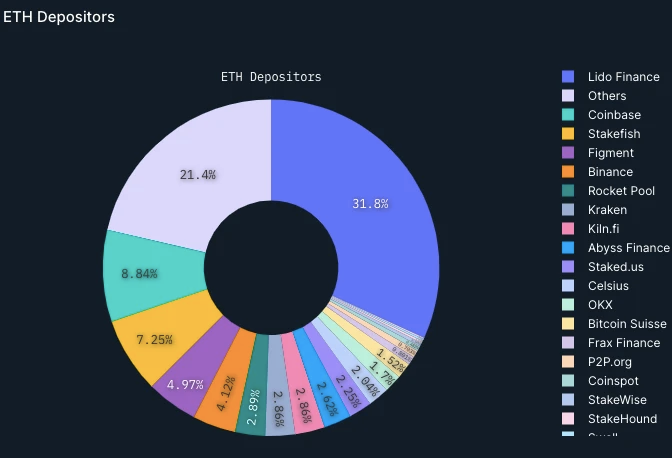

But after the Shanghai upgrade enabled withdrawals, the LSD sector cooled quickly. Except for top players, latecomers struggled to gain traction. Today, Lido leads decisively with 31.8% share among staking providers, followed by Coinbase (8.84%) and Stakefish (7.3%).

2. Technology: Two Major Upgrades, Building Anticipation

Technologically, Ethereum’s two biggest milestones in 2023 were upgrades: Shapella and Cancun.

On April 12, seven months after “The Merge,” Ethereum executed simultaneous Shanghai and Capella upgrades—collectively called “Shapella.” The key outcome: enabling withdrawal functionality for stakers who hadn’t previously set withdrawal credentials. This brought withdrawal capabilities to the execution layer, allowing nearly 20 million ETH locked since 2020 to be withdrawn from the Beacon Chain to the execution layer—either fully or partially (including rewards)—releasing staked token liquidity.

Although Shapella didn’t reduce gas fees, implemented EIP-3651, EIP-3855, and EIP-3869 lowered costs for developers and block proposers. More importantly, it marked the final step in Ethereum’s transition from Proof-of-Work (PoW) to Proof-of-Stake (PoS).

After implementation, though some early stakers withdrew, net inflows turned positive within two weeks, with staking volume and validator count accelerating upward.

Another highly anticipated upgrade: Dencun (Deneb + Cancun)—a milestone event where Cancun focuses on the Execution Layer and Deneb on the Consensus Layer.

Dencun will bring tangible benefits: enhanced scalability, lower gas fees, improved security, efficient data storage, and stronger cross-chain connectivity. Post-upgrade, Ethereum L1 and L2 ecosystems—alongside bridges, storage, and GameFi—could experience explosive growth.

Originally scheduled for November, Dencun followed Ethereum’s tradition of delays. Developers now suggest postponement to early 2024. If completed alongside Bitcoin’s halving and spot ETF momentum, Ethereum could see outsized rewards in 2024.

3. Other Developments: Vitalik’s Concerns, Spot ETF Awaits Approval

In 2023, Ethereum seemed focused on internal refinement—digesting past achievements while exploring new technologies.

For example, in Vitalik’s 30 public opinions collected by Odaily this year, eight concerned wallets—especially account abstraction. In mid-to-late 2023, this sparked an industry-wide debate on account abstraction vs. EOA wallets. While account abstraction offers clear advantages, Vitalik’s statement at an Ethereum community meeting—that “account abstraction could attract billions to use Ethereum”—may explain his personal enthusiasm.

Vitalik is anxious—for multiple reasons. First, Bitcoin’s ecosystem resurgence, with various consensus protocols making it faster and cheaper to deploy applications, is diverting attention from Ethereum. Second, high-performance new L1s like Aptos, Sui, Ton are maturing, while L2s are siphoning away users and capital originally destined for Ethereum.

At year-end, another major development: Ethereum spot ETFs may soon arrive. Alongside Bitcoin ETF filings, BlackRock and ARK began applying for Ethereum spot ETFs. If approved, this would significantly boost chances for Ethereum ETFs, potentially unlocking massive inflows and sending ETH prices soaring.

As the most complete Web3 ecosystem and prime ambassador of Web3 to the traditional world, Ethereum—having spent a year accumulating strength—awaits full societal acceptance to unleash its true potential. It will then face old rivals and new challengers with renewed vigor.

Layer 2: Flourishing Diversity, Tides Rising

In 2023, Layer 2 became the mainstream choice for execution-layer scaling.

Over the past year, we’ve seen several L2s surpass legacy L1s in key metrics, witnessed central entities like Coinbase and ConsenSys experiment with L2s, and even observed L1s like Celo pivot toward becoming L2s.

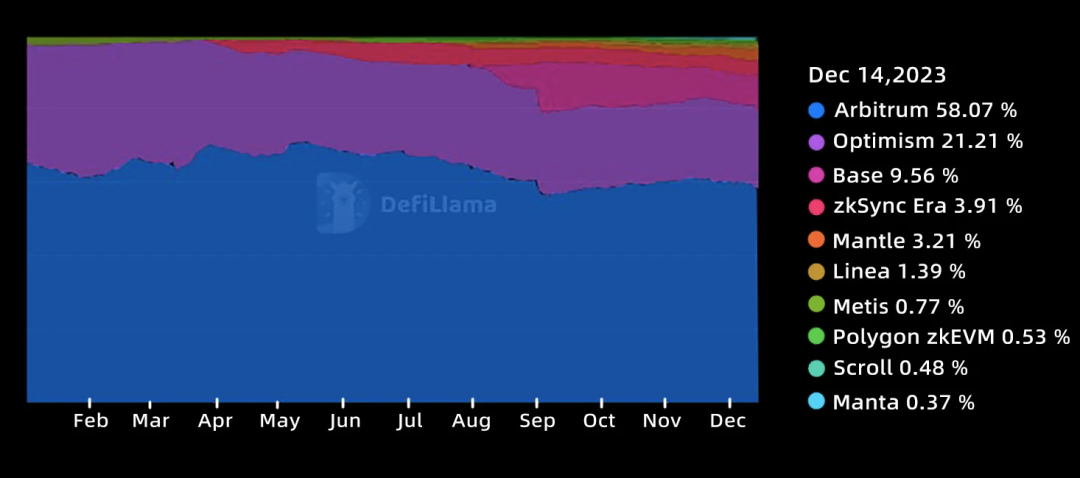

Odaily Planet Daily note: Comparison of TVL across major L1/L2 ecosystems—Arbitrum ranks top five, Optimism and Base in top ten

Within the L2 sector, Optimistic Rollup leaders Arbitrum and Optimism continue to dominate TVL thanks to first-mover advantage—but their development strategies have diverged sharply.

Odaily Planet Daily note: Yearly changes in TVL among top 10 L2s—Arbitrum and Optimism remain leaders; ZK-based chains gradually expand share from mid-year onward

Arbitrum launched its governance token ARB in March, triggering the largest airdrop in L2 and wider crypto industry history. Now, Arbitrum continues stimulating activity via frequent ARB incentives, explores vertical scaling via Arbitrum Orbit, and actively builds a new development environment Stylus—supporting additional programming languages to extend EVM capabilities.

Optimism, leveraging OP Stack, advances horizontal expansion, gaining strong allies like Base and Zora. In August, Optimism and Base signed a governance and revenue-sharing agreement—revealing the blueprint for a future “Superchain” ecosystem: Law of Chains framework enables OP to govern the entire ecosystem; mainchain Optimism expands the ecosystem via OP distribution while advancing decentralization; Base and other chains channel revenues back to support the mainchain.

Notably, Blast—a purported auto-yield Optimistic Rollup with only smart contracts so far—suddenly disrupted the L2 market late in the year. Through aggressive marketing tactics by founder CX Iron Mountain, it attracted hundreds of millions in capital, becoming the third-largest “L2” by TVL after Arbitrum and Optimism.

ZK-Rollups: The mythical zkEVM is no longer just narrative fiction. zkSync Era, Polygon-zkEVM, Linea, Scroll launched mainnets this year and achieved meaningful scale. Starknet completed its “Quantum Leap” upgrade, drastically improving execution efficiency.

These networks have become battlegrounds for airdrop hunters—countless farmers and bots work round-the-clock accumulating interaction data, hoping to claim future airdrops whose details remain unclear.

Another focal topic in 2023: projects like Celestia and Eigenlayer fueled discussions on modularity. As some rollups began using third-party networks instead of Ethereum for data availability (DA), the definition of a “pure” L2 sparked intense debate.

Vitalik’s recent article seems pointed—first redefining various L2 types, then proposing exploration of ZK+Plasma feasibility—implicitly guiding the market away from third-party DA solutions.

Looking back at 2023, it’s regrettable that the long-awaited Cancun upgrade was delayed—but this delay now fuels our greatest hope for L2 developments in 2024.

Looking ahead, the expected Cancun upgrade could drive massive fee reductions and speed increases across L2s—potentially ushering in a new growth peak.

Additionally, L2 decentralization progress deserves attention in 2024—whether ZK-Rollups will widely launch tokens and完善governance systems, and how decentralized sequencer development progresses.

Tides are rising—will 2024 be the year of Layer 2? We’ll watch with cautiously optimistic eyes.

Layer 1: Shrinking Diversity, “Ethereum Killers” Lose Luster

With L2s maturing, today’s market sees numerous L2s fiercely competing. According to DeFiLlama, among the top 10 chains by TVL, L2s occupy three spots—and may displace even more L1s in the future.

Against this backdrop, how have former “Ethereum killers” fared?

Most emerging L1s have drifted far from their heydays over the past year. But this doesn’t mean the L1 space stagnated—many “new” L1s still delivered innovations and changes.

Examining the L1 landscape, the most notable story is Solana’s resurgence. After FTX’s collapse, Solana endured prolonged silence but steadily rebuilt from the rubble.

Solana started poorly in 2023. In February, the network suffered a fork incident. A node failure caused a split—creating two independent versions of the Solana blockchain. Nodes couldn’t reach consensus, causing network failure. Transaction processing capacity dropped below 100 TPS.

The outage lasted hours, severely disrupting users and developers. Though engineers quickly identified and fixed the issue, reputational damage lingered. Doubts arose about platform scalability and reliability. Community confidence wavered, and SOL’s price plunged.

Since then, the Solana Foundation and developers doubled down on improving network stability and resilience. By Q4, Solana experienced strong recovery and robust growth.

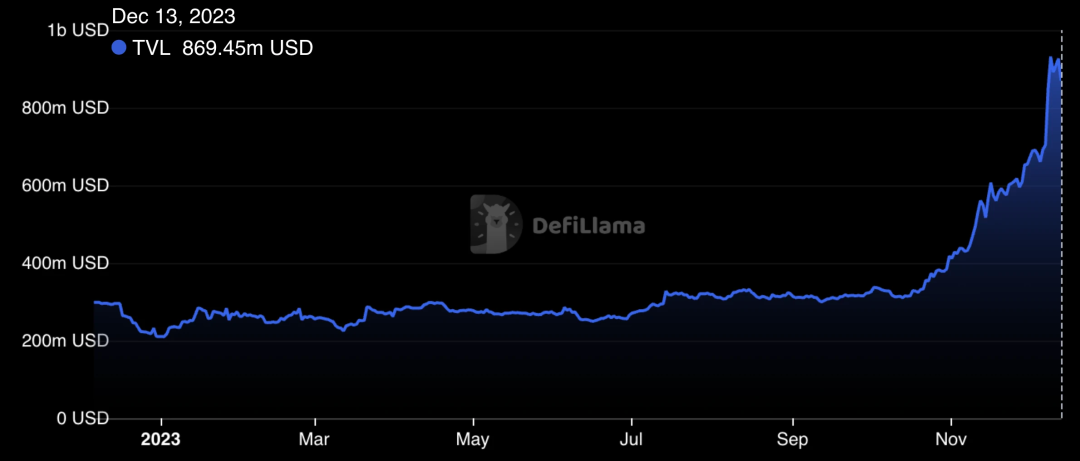

For example, DeFiLlama shows Solana’s TVL hovered around $300M in the first three quarters of 2023. But in Q4, TVL surged—exceeding $800M, an increase of ~200% from pre-rally levels.

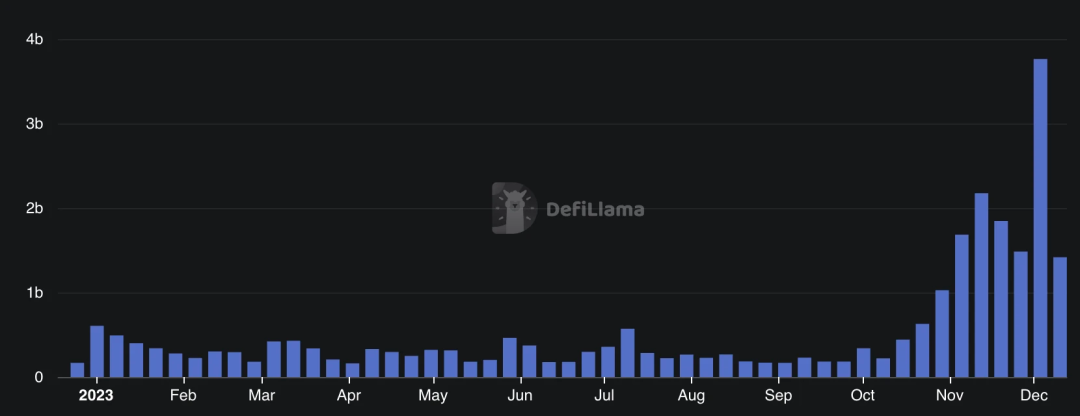

Solana’s DEX trading volume also soared—reaching a record high of over $3.7 billion in mid-December.

In crypto, temporary surges aren’t rare—most tokens enjoy moments of glory. What makes Solana unique is its ability to stage a “second comeback”—a rarity in the space.

Amid scattered non-EVM networks, “Move twins” Aptos and Sui emerged as standout new L1s this year.

In April, Aptos launched delegated staking, letting users delegate rights to trusted validators and earn individual rewards.

In May, Sui launched mainnet. Though lagging behind Aptos (which launched last year), Sui achieved solid results. In an era where L2s dominate headlines and L1 narratives fade, what makes these Move-based chains—backed by massive capital—so special?

Their origin traces back to Facebook. The social giant once aimed to enter crypto with its innovative Diem blockchain. But repeated regulatory setbacks doomed Diem. Developers realized escaping regulatory constraints required moving closer to crypto-native roots—thus birthing Sui and Aptos.

Due to ties with Facebook’s Diem, both inherited Move language as their smart contract foundation.

Move differs greatly from Solidity—not judged here, but the difference makes Sui and Aptos distinctive products in the market.

DeFiLlama data shows Sui’s TVL reached ~$150M, Aptos ~$78M. Block explorers indicate Sui has over 9.11M total accounts, Aptos over 9.9M.

Overall, Sui made a strong start in 2023—achieving progress technically and ecologically, earning support from investors and developers.

Other “legacy” L1s also performed well.

Filecoin took major steps as a non-EVM network. In March, the Filecoin Virtual Machine (FVM) launched successfully—enabling smart contracts and programmability on the Filecoin blockchain.

A mature network long dominant in storage, FVM added computational power. EVM compatibility eases developer and dApp adoption—setting a new milestone for Filecoin’s future.

Similarly, in April, EOS EVM Mainnet Beta launched—enabling interoperability between Ethereum and EOS ecosystems.

Looking at non-EVM L1s in 2023, we observe an interesting phenomenon.

L2 momentum not only propels Ethereum forward but subtly influences the L1 landscape. Solidity’s vast developer base draws more non-EVM networks to embrace EVM compatibility. Smaller, niche networks unable to support EVM struggle increasingly in the market.

Ethereum’s gravity is so powerful that other public chains—actively or passively—fall under its influence. In November, EVM L1 Celo made a poignant decision. Its main developer cLabs initiated a forum thread titled “Choosing an L2 Protocol Stack,” inviting community feedback and discussion.

Celo seeks repositioning—adopting a mature stack to build an L2 network while migrating its ecosystem. Priorities include “simple migration, minimal downtime, low gas fees, and Ethereum compatibility.”

This means one fewer competitor in the L1 arena—and users gain a new L2.

Celo’s strategic shift suggests more L1 projects may approach their twilight. For niche networks, the choice narrows: either get absorbed by Ethereum or go fully independent—like Solana, Aptos, and Sui.

Ethereum-like L1s face shrinking survival space.

Given this, how have those once-prominent high-efficiency, low-gas, EVM-compatible “Ethereum killers” fared?

Take Fantom: during the previous bull run, backed by AC, it shone brightly. Fantom relied on Multichain as its primary cross-chain bridge. In July, impacted by the Multichain incident, Fantom faced crisis—~$118M assets drained from Multichain’s Fantom bridge contract, stablecoins issued via the bridge severely de-pegged.

This dealt a heavy blow—Fantom’s TVL collapsed and remains unrecovered.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News