SignalPlus Macro Research Report: As Year-End Approaches, the Crypto Market Stalls

TechFlow Selected TechFlow Selected

SignalPlus Macro Research Report: As Year-End Approaches, the Crypto Market Stalls

Traders have begun gradually reducing trading volumes, and cross-asset volatility has started to decline, leaving the Bank of Japan as the only remaining "event risk" this year.

Written by: SignalPlus

These days, many people have started their holiday breaks for the dual festivals. Exchange block trades have dried up— the largest trade I’ve seen recently was less than $250,000, buying puts at 37,000 for March expiry.

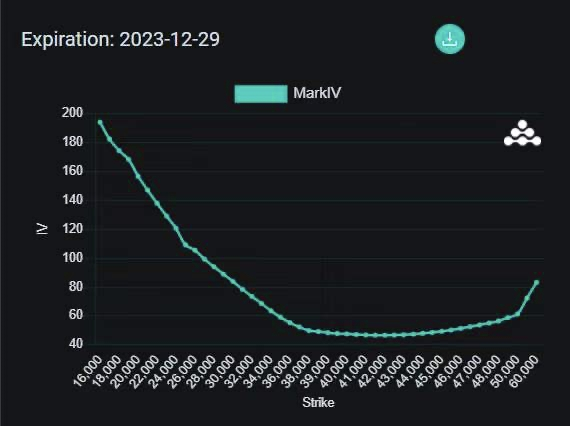

The BTC volatility smile curve for year-end expiry! Dear investors, do you really need to be this pessimistic? The left side (put options) shows significantly higher implied volatility than the right—clearly reflecting strong demand from put buyers.

The market appears to have entered the final chapter of the year. Traders are gradually reducing positions, and cross-asset volatility is declining. The Bank of Japan has become the only remaining "event risk" of the year. Softening U.S. manufacturing data (December New York Fed Manufacturing Index improved from -23.6 to -14.5) further supports the argument for a Fed pivot. As the Fed abandons caution despite core inflation still being far above long-term targets, FOMO sentiment in markets continues to build. Even the most committed bears are starting to wonder whether this could mark the beginning of the next asset inflation cycle.

Last week, as traders piled into bullish positions following the Fed's dovish statement, SPX options open interest hit a record high, surpassing pre-pandemic peaks. Additionally, the Russell 2000 index surged from its 52-week low to its 52-week high within just 1.5 months—a dramatic move that once again renders traditional labels like “bull” or “bear” market meaningless.

Historically, the period leading up to the first rate cut tends to be favorable for equities. Price action after rate cuts, however, depends on whether the economy actually falls into recession. The current cycle seems to sit at the midpoint of a typical easing cycle. The path ahead hinges on whether the ongoing slowdown in hard data evolves into a full-blown recession.

In crypto, prices continue to stagnate. Optimism around ETF approvals may already be fully priced in—the GBTC NAV discount has narrowed sharply. While ETF approval will undoubtedly boost market sentiment, it’s important to note that initial inflows may largely come from outflows from GBTC and publicly listed miners. However, as investors return to the “cash is trash” mindset, the sharp decline in global bond yields could offset some of these dynamics—though this also means we remain vulnerable to shifts in bond yields.

Moreover, sell-side analysts expect that much of the current move is driven by retail speculation on institutional re-engagement. Once news is officially announced, selling pressure might actually emerge. Given BTC’s current overbought condition, perhaps an ETH/BTC spread trade could be a viable strategy? Only time will tell…

[Disclaimer] Markets involve risk; investment requires caution. This article does not constitute investment advice. Readers should consider whether any opinions, viewpoints, or conclusions expressed herein are suitable for their particular circumstances. Investment decisions based on this information are at the reader’s own risk.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News