The Retail Investor Dilemma in RWA and Innovative Solutions Using DeFi

TechFlow Selected TechFlow Selected

The Retail Investor Dilemma in RWA and Innovative Solutions Using DeFi

The reason most RWA products can only target qualified or institutional investors is that compliant issuance to retail investors incurs high costs.

Author: DigiFT Ryan Chen et al.

Dilemma: Why Limited to Qualified Investors Only?

Except for a few projects that have achieved limited retail investor access to RWA offerings by complying with local laws, issuing special prospectuses, and registering specific securities (refer to the RWA Innovation module for details), most RWAs in today’s market are accessible only to qualified investors. Depending on regional regulations, investors must demonstrate a minimum level of financial assets to qualify—for example, Singapore requires individuals to possess S$1 million (approximately USD 730,000) in financial assets.

The primary reason most RWA products—including those tied to U.S. Treasuries—are restricted to qualified or institutional investors is the high cost associated with compliant retail issuance.

These costs stem from the lack of direct linkage between the underlying asset and the issued token.

Securities laws impose strict requirements when issuing securities to retail investors, including preparing and registering a prospectus. Additionally, in most jurisdictions, ownership of assets such as stocks and bonds must be recorded in specific ways—such as in a register maintained by the issuer. Regulatory authorities currently do not accept blockchain tokens as valid instruments for legal ownership registration, meaning that token ownership does not automatically equate to legal ownership of the underlying asset under existing regulations.

For asset-backed RWA models—such as RWA tokens backed by U.S. Treasuries—a "bridge" is required between the real-world asset and the tokenized representation. The RWA token itself constitutes a new security. This bridge can be established by treating the RWA token as an independent security, but this also means the token must independently comply with all applicable securities laws—requiring issuers to prepare and register a separate prospectus specifically for the RWA token.

To better understand this, consider the traditional model of securities issuance targeting retail investors. Whether issuing stocks or bonds, the process typically involves:

-

Internal preparation within the company to define the characteristics of the securities, selecting and hiring investment banks (underwriters) and other financial professionals such as lawyers and accountants to assist with the IPO process.

-

Selection of underwriters, who help the company prepare and execute the bond issuance.

-

Due diligence, audits, and credit ratings (for bonds), reviewing internal controls and governance structures to ensure compliance; for bonds, the rating affects their perceived credit quality.

-

Prospectus preparation, which must be approved by regulators if targeting retail investors, ensuring adequate disclosure to investors.

-

Pricing, where valuation and offering price are determined jointly with underwriters.

-

Marketing, including roadshows, engaging potential investors, and explaining the company's business.

-

Issuance and listing, requiring compliance with exchange listing standards.

-

Post-issuance management, such as ongoing financial disclosures and public announcements.

It is evident that enabling securities to be sold to retail investors involves a complex series of steps. Two key factors make it difficult for RWAs to directly target retail investors:

1. High costs, insufficient returns. Completing the full issuance process for retail investors can incur millions of dollars in expenses and require regulatory approvals. Given that the overall crypto market is relatively small compared to traditional markets, it cannot support large-scale fundraising needs. As a result, the compliance costs outweigh the potential benefits.

2. Inadequate infrastructure. There are no compliant securities exchanges providing trading services for tokens, and securities registrars do not yet recognize tokens as valid ownership records.

To avoid these high costs and transaction frictions, issuers opt to offer products exclusively to qualified and institutional investors. Most mainstream RWA assets in the current crypto market are issued by startups through SPVs (Special Purpose Vehicles). When using traditional capital market securities—like U.S. Treasuries—as collateral under an asset-backed model, investors purchasing these issued bonds are not buying Treasuries directly. Instead, they are purchasing corporate bonds issued by the SPV, backed by Treasuries. This introduces significant counterparty risk, downgrading the original AA+ rated U.S. Treasury to a BBB-rated corporate bond. Similarly, other directly issued corporate bonds are typically issued by smaller companies without going through the full retail issuance process, reducing costs but limiting access to qualified investors only.

RWA Business Innovation: Integrating RWA with DeFi

Since most security-like RWA assets are restricted to qualified investors, market reach remains highly limited. Numerous RWA protocols are exploring innovative legal and business models to integrate RWAs into DeFi, enabling permissionless access to U.S. Treasury yields or building infrastructure analogous to an on-chain Yu'ebao (money market fund).

Lending Model: Ondo OUSG — Flux Finance by Ondo Finance

Ondo Finance designed a lending protocol called Flux Finance for its U.S. Treasury token OUSG. Flux Finance is based on the code of Compound V2, modified to support whitelisted assets as collateral, with adjusted interest rate curves and loan-to-value (LTV) ratios tailored to OUSG’s characteristics. Currently, OUSG is the sole collateral asset on Flux Finance, with an LTV ratio of 92%.

The borrower side of the protocol is permissionless—any DeFi user can participate. Users deposit stablecoins into Flux Finance’s lending pool and earn interest. The platform currently supports four stablecoins: Frax, USDC, USDT, and Dai, with a utilization cap of 90%. OUSG holders can pledge OUSG to borrow stablecoins from Flux Finance, gaining liquidity. Flux Finance ensures borrowing rates remain below the yield generated by OUSG, thereby passing OUSG’s yield to stablecoin holders in a permissionless manner, while maintaining 10% liquidity in the pool for withdrawals.

Token Wrapping and Lending Model: MatrixDock — TProtocol

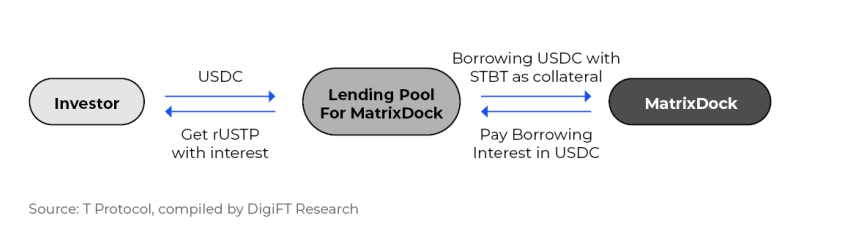

Recently, TProtocol announced a collaboration with MatrixDock to provide a lending pool within TProtocol V2, helping channel the yield from MatrixDock’s U.S. Treasury token STBT into DeFi applications.

TProtocol v1

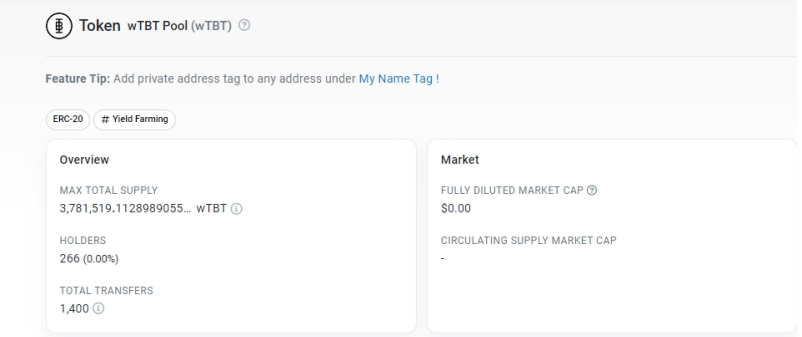

In TProtocol V1, secondary wrapping of MatrixDock’s STBT enabled permissionless distribution of its U.S. Treasury token. TProtocol purchased STBT and minted a corresponding token wTBT, whose supply adjusts based on the amount of STBT held. Without whitelist restrictions, wTBT integrates more seamlessly with various DeFi applications and can be bridged across different blockchains. The wTBT token currently has a circulating supply of 3.7M.

T Protocol V1 wTBT token, source: Etherscan, data as of November 27, 2023

TProtocol v2

T Protocol V2 Product Flowchart

In September 2023, TProtocol partnered with MatrixDock to create a lending pool for MatrixDock’s STBT. STBT is a rebasing token, with each unit pegged to $1. Its underlying assets consist of a basket of short-term U.S. Treasuries and money market funds, generating yield for holders, reflected through daily rebasing adjustments to the token balance.

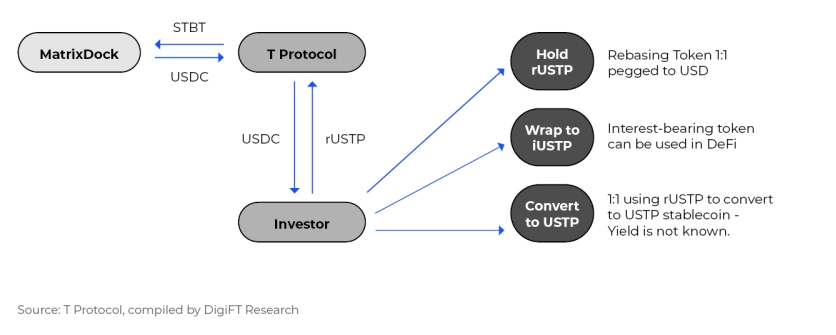

TProtocol will open lending pools for partner institutions; currently, only MatrixDock’s STBT is supported. Users deposit USDC into the pool and receive an equivalent amount of rUSTP tokens. STBT holders can use their tokens as collateral to borrow USDC at a 99% LTV ratio.

The yield offered to USDC providers is variable but will not exceed STBT’s own yield. The protocol aims to pass as much yield as possible to USDC users. The rUSTP tokens received upon depositing USDC are rebasing tokens, each pegged to $1, with yield reflected in daily increases in token quantity. In theory, rUSTP’s yield tracks the yield provided by STBT.

MatrixDock maintains a reserve of USDC in the lending pool. When users request redemption, redemptions are first fulfilled from this reserve. For excess amounts, small redemptions are covered by direct sales of STBT on Curve, while large redemptions go through MatrixDock’s redemption process, which currently takes T+3 under the existing design.

rUSTP can be converted into USTP, a non-yielding stablecoin. The remaining yield portion is not explicitly allocated (possibly retained by TProtocol itself). Users can also convert rUSTP into iUSTP at an internal exchange rate—an accrual-based token whose quantity remains constant but whose value grows over time, making it more compatible with various DeFi protocols.

The overall flow is as follows:

T Protocol V2 Product Flowchart

TProtocol V2 uses a lending model to avoid potential compliance issues associated with directly introducing securitized tokens, similar in structure to Ondo Finance and Flux Finance. According to TProtocol documentation, users will eventually be able to deposit USDC into institution-managed pools and earn yield from RWA assets—part of a broader plan involving RWA-backed stablecoins.

RWA-Based Stablecoin: MatrixDock — USDV

The stablecoin project USDV (Verified USD) uses STBT as its underlying asset to issue USDV, an RWA-backed stablecoin. Compared to centralized issuers like Circle and Tether, USDV offers greater transparency due to its on-chain assets, providing a stronger foundation of trust.

Typically, stablecoin issuers acquire fiat dollars, mint an equivalent amount of stablecoins, then invest those dollars in U.S. Treasuries or high-grade bank bonds to generate yield—one of their revenue streams. Some issuers, like Circle, distribute a portion of this yield to ecosystem partners. USDV follows a similar approach, using smart contracts to directly share underlying asset yields with ecosystem participants—such as minter, market makers, and liquidity providers—to foster growth within the stablecoin ecosystem.

STBT holders who complete KYC verification can become USDV minters, depositing STBT into the contract to mint new USDV. USDV employs a unique coloring mechanism, akin to Bitcoin’s UTXO model, allowing on-chain identification of the minter. Yield generated from the dynamic adjustment of the underlying STBT assets is retained in the contract, with 50% distributed to the corresponding minters and the remaining 50% allocated to market operators and liquidity providers. These participants can claim their yield or use it to further incentivize ecosystem development.

Bearer Instruments: Backed Finance

The previous models transfer yield permissionlessly into DeFi via token wrapping or lending mechanisms, preserving the original issuer’s compliance obligations. In contrast, Backed Finance and Ondo Finance’s USDY represent breakthroughs at the legal and regulatory level.

Before diving into Backed Finance’s implementation, let’s clarify registered vs. bearer instruments:

-

Registered instruments: Most tradable instruments, especially securities, are registered. The issuer or authorized registrar must record every transfer and track the holder.

-

Bearer instruments: The issuer or registrar only needs to know the holder’s identity during subscription, redemption, or trading. During circulation, there is no requirement to continuously track ownership.

Backed Finance issues “tracker certificates,” a type of derivative that tracks the price of underlying real-world assets. Each token represents a tracker certificate, giving token holders contractual rights to the value of the underlying asset.

Backed Finance has registered the “base prospectus” for these tracker certificates with Liechtenstein’s Financial Market Authority. Since Backed Finance is incorporated in Switzerland, Swiss law restricts promotion to qualified investors only. However, “authorized participants”—licensed banks, securities firms, and non-Swiss regulated financial institutions—can purchase from Backed Finance and resell to retail clients. On the Backed Finance platform, token subscriptions are limited to qualified professional investors, but retail investors who acquire the product elsewhere can redeem after completing KYC with Backed Finance.

In the prospectus, Backed Finance designs its tokens as bearer instruments. The token contract includes only a blacklist mechanism, enabling permissionless transfers post-issuance and direct interaction with DeFi protocols. Identity verification is required only during subscription or redemption with Backed Finance.

Transaction history of Backed Finance tokens on Ethereum, showing liquidity on Uniswap. Source: Etherscan, data as of November 27, 2023

From subscription and redemption data, Backed Finance’s short-term Treasury ETF token bIB01 shows only two subscription addresses: 0x43 and 0x5f, with no redemptions. After subscription, tokens are transferred to other investors, suggesting these addresses may belong to authorized dealers distributing tokens to DeFi protocols or end users. Dealers may perform KYC once, allowing downstream users to bypass individual qualified investor or institutional investor requirements.

Yield-Bearing Stablecoin: Ondo USDY — Mantle by Ondo Finance

The newly launched USDY has gone live on the Layer 2 network Mantle as its yield-bearing stablecoin. Mantle users can now directly purchase USDY on decentralized exchanges. While Backed Finance leverages European legal frameworks to embed RWA into DeFi, Ondo Finance has chosen a different path.

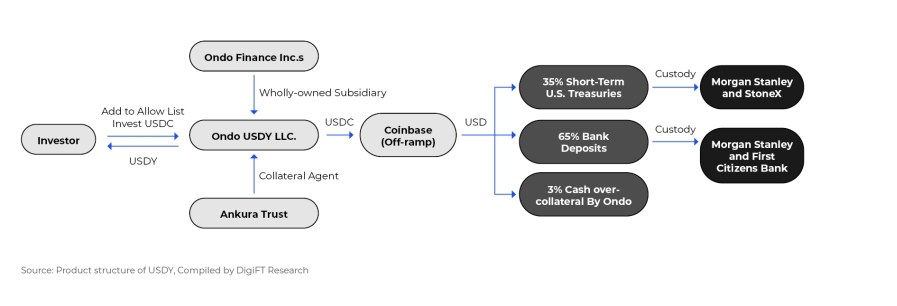

USDY Product Structure Diagram

USDY is issued by Ondo USDY LLC, a wholly-owned subsidiary of Ondo Finance Inc., structured as a bankruptcy-remote SPV. USDY is a token backed by short-term U.S. Treasuries and bank demand deposits. It is registered under U.S. Regulation S, allowing sales to non-U.S. retail investors under certain restrictions. Current limitations include a 40–50 day holding period post-purchase—meaning users must wait until the lock-up ends before receiving tokens on-chain—and a one-year restriction on resale to U.S. investors.

The USDY token contract on Ethereum features both whitelist and blacklist mechanisms. Unlike other RWA tokens, USDY’s whitelist is uniquely designed: anyone can call the contract to add their address to the whitelist—a user experience similar to an authorization transaction. The USDY website provides a built-in function to send this transaction, and after IP detection, users can agree to terms and add their address without undergoing KYC. Additionally, the USDY token contract references a legal document stored on IPFS, implying that adding one’s address constitutes agreement to these terms.

Currently, USDY is an accrual-style token, accumulating yield over time. Later, Ondo Finance launched USDY and mUSD on Mantle, removing the whitelist and retaining only the blacklist. mUSD is a rebasing token, pegged to $1, with balances periodically adjusted based on yield. mUSD can be exchanged for USDY at the prevailing rate directly on the Ondo Finance platform.

These five models—leveraging technology, business innovation, and legal structuring—address the qualified investor barrier in RWA compliance, bringing RWA assets into DeFi and expanding access to broader audiences. For RWA projects, this increases platform adoption; for DeFi, it introduces new asset classes with stable baseline yields, enabling diversified financial product creation through asset combinations.

However, challenges remain across all models:

1. AML constraints. DeFi protocols cannot prevent non-compliant assets—such as stablecoins from sanctioned addresses—from entering their systems. Yet RWA protocols must convert stablecoins into fiat to purchase real-world assets, necessitating rigorous KYC and AML checks on fund sources. This mismatch pressures some DeFi protocols to strengthen source-of-funds verification. As more RWAs enter DeFi, compliance scrutiny over fund origins will intensify.

2. Time mismatch. Traditional financial markets operate only five days a week, for limited hours per day, and close on holidays. Transactions rely on banking and brokerage systems, often requiring T+1 or longer settlement times. In contrast, DeFi operates 24/7. During liquidity events—such as market volatility over holidays—DeFi protocols may need to liquidate positions, but RWA assets require lengthy processing times. Protocols incorporating RWAs must carefully manage liquidity risks.

3. Sales restrictions. Many RWA projects restrict participation from residents of certain countries due to tax complexity (e.g., U.S. tax systems), AML sanctions, or complicated financial regulations. Through DeFi, there is a risk of inadvertently selling to prohibited jurisdictions. Since most RWAs are classified as securities, such violations could expose projects to legal penalties in those regions.

4. Asset ownership clarity. It is unclear how DeFi protocols should legally establish KYC for RWA purchases, how to custody acquired assets, and how ownership of RWA assets purchased with user-deposited stablecoins should be recognized under law. Typically, DeFi protocols use foundations or SPVs as legal entities to open accounts and purchase RWA assets on behalf of users. Legally, the RWA assets belong to the foundation or SPV, with ultimate beneficiaries being the entity’s shareholders—not the DeFi users. However, DeFi users are often anonymous or organized as DAOs, possessing only code-enforced claims, not legal ownership. Protecting user asset rights remains an unresolved challenge.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News