OKX Ventures Latest Research Report: Understanding the Development Landscape and Future Direction of Stablecoins

TechFlow Selected TechFlow Selected

OKX Ventures Latest Research Report: Understanding the Development Landscape and Future Direction of Stablecoins

With the strengthening of regulatory discourse and the trend toward central bank digital currency issuance, centralized stablecoins are back in the spotlight.

Authored by: OKX Ventures

I. Summary

From the 2021 bull market to the 2023 bear market, the cryptocurrency market has undergone significant changes. The total market capitalization declined from $3 trillion to $1 trillion, while stablecoin market cap only decreased by 30%, demonstrating strong resilience and underscoring their critical role within the crypto ecosystem and their continuous rapid expansion.

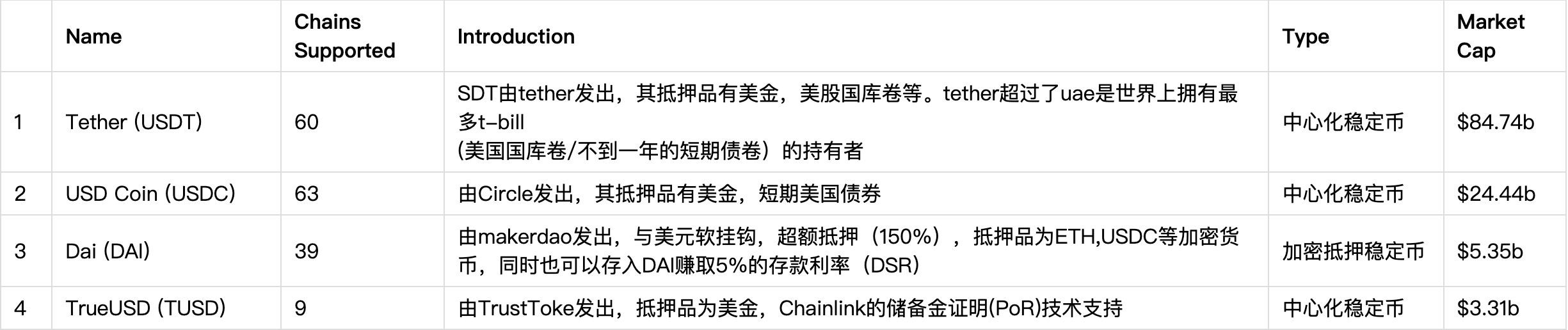

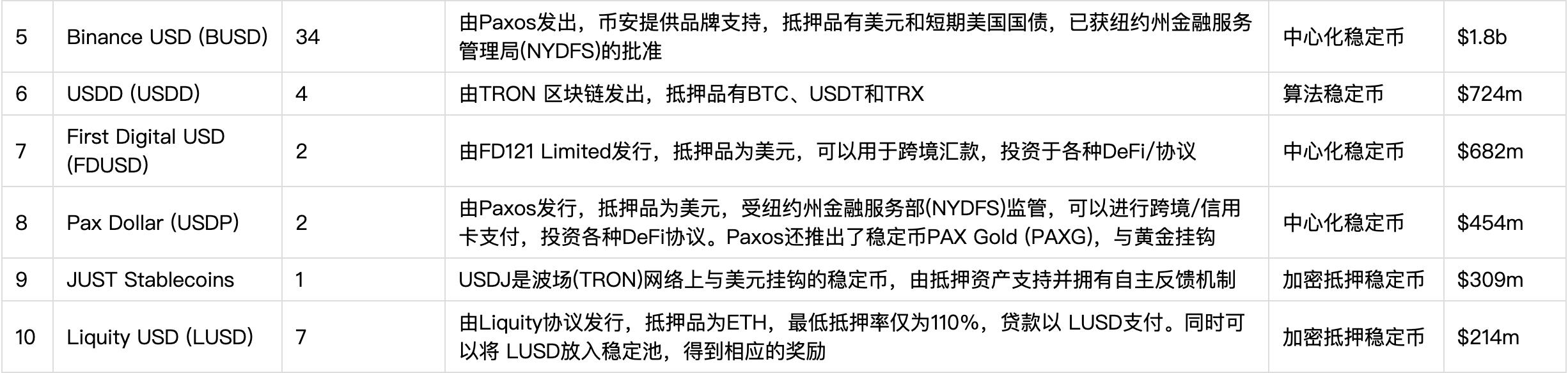

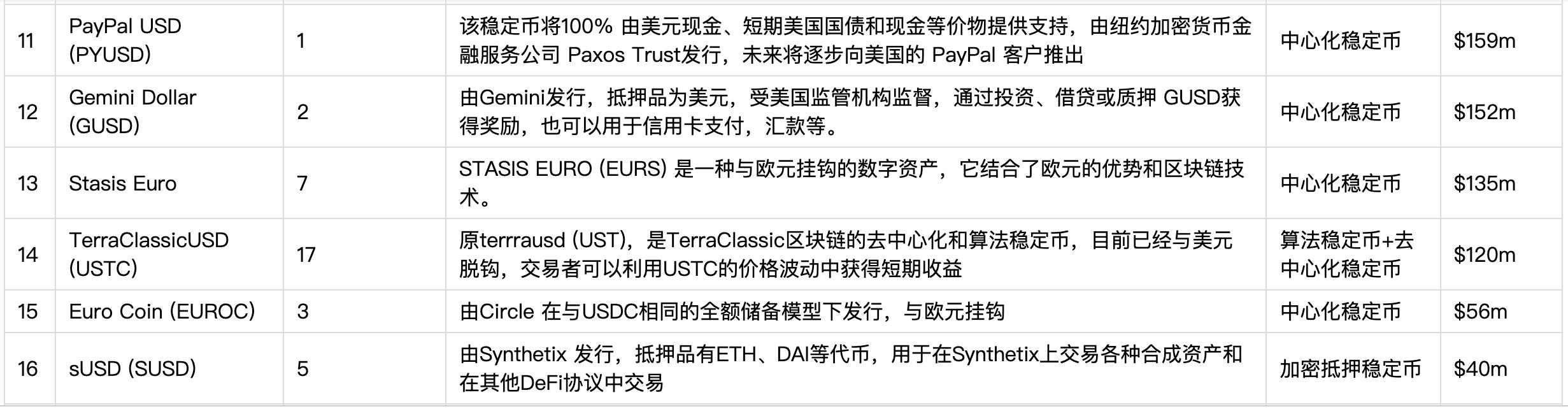

As of December 2023, CoinGecko data shows the total stablecoin market cap is approximately $130 billion, with Tether (USDT) accounting for about 70% and USDC around 20%. The remaining market share is distributed among other centralized and decentralized stablecoins. Especially in the current high U.S. Treasury yield environment (>5%), Tether can easily generate $3 billion in annual profits, making the stablecoin market highly attractive. Additionally, governments worldwide are formulating virtual asset transaction policies, and central banks are beginning to explore their own stablecoins—efforts that further accelerate the growth of the stablecoin market.

Beyond Tether and USDC, we have seen a surge of on-chain stablecoins emerge, reflecting DeFi’s demand for different types of stablecoins (collateralized, lending-based, "nested" structures). Innovations in these new stablecoins include diversified collateral types, liquidation mechanisms, and community-oriented revenue-sharing models. Their success depends on maintaining liquidity and integrating with major DeFi protocols.

Despite the proliferation of on-chain stablecoins, over 90% of the market cap remains concentrated in centralized stablecoins. With increasing regulatory scrutiny and the trend toward central bank digital currencies (CBDCs), centralized stablecoins are once again drawing attention. Some startups are attempting to challenge the dominance of Tether and USDC by leveraging high U.S. Treasury yields. However, long-term success for centralized stablecoins will depend more on collaboration with traditional financial institutions and regulators—including compliant custodians, capital inflows, and obtaining virtual asset trading licenses.

To create the next super stablecoin comparable to USDC and USDT, the author believes at least four key conditions must be met to fully leverage both centralized and decentralized advantages:

1. USD-backed stablecoin: The U.S. dollar enjoys broad global acceptance, and its supporting assets have wide applicability.

2. Global regulatory recognition and licensing: A super stablecoin must be designed for global deployment from inception, gaining recognition and licenses from key regional regulators.

3. Innovative financial attributes: A super stablecoin should feature innovative financial properties such as revenue distribution mechanisms to build community support and drive sustained growth.

4. Integration into the DeFi ecosystem: A super stablecoin needs to become the default currency within DeFi protocols to ensure widespread adoption across DeFi applications.

In conclusion, stablecoins play a crucial role in the cryptocurrency ecosystem and are expected to continue evolving and expanding. Successfully launching the next super stablecoin requires combining DeFi innovations with strategic partnerships involving traditional financial institutions and regulatory bodies.

II. Stablecoin Classification

Decentralized Stablecoins

To address the limitations of centralized stablecoins, decentralized stablecoins introduce innovative solutions. These new stablecoins are built on blockchain protocols, offering greater security and transparency. For example, Curve’s crvUSD, Aave’s GHO, and Dopex’s dpxUSDSD are all protocol-based stablecoins that do not rely on central entities, thereby reducing financial and operational risks associated with centralization. Decentralized stablecoins can be broadly categorized into two main types:

1. Overcollateralized Stablecoins:

Collateralized stablecoins are the most common type of decentralized stablecoins, typically backed by other cryptocurrencies such as Ethereum or Bitcoin to maintain price stability. For instance, MakerDAO’s DAI is supported by Ether as collateral. The latest trend involves expanding collateral beyond traditional centralized stablecoins and large-cap digital currencies to include a broader range of digital assets or multi-layered nesting structures, aiming to increase liquidity and unlock additional use cases. For example, stETH is the largest collateral in Curve’s crvUSD, while Ethena’s stablecoin also relies on Ethereum and LSTs.

Advantages: Collateralized stablecoins transform decentralized stablecoins from mere payment tools into broader digital asset management and investment instruments, providing users with greater choice and flexibility.

Disadvantages: The primary challenge lies in over-collateralization potentially lowering capital efficiency. In particular, when volatile assets like Ether serve as collateral, higher risk may trigger forced liquidations during market downturns.

2. Algorithmic Stablecoins:

Algorithmic stablecoins represent one of the most decentralized forms, using supply and demand dynamics rather than physical collateral to maintain a fixed price. These stablecoins employ algorithms and smart contracts to automatically adjust supply and stabilize prices. For example, Ampleforth is an algorithmic stablecoin designed to maintain a price close to $1 through an elastic supply mechanism—increasing supply when prices exceed $1 and decreasing it when below $1.

Additionally, hybrid algorithmic stablecoins combine algorithmic mechanisms with fiat reserves. Frax, for instance, uses a partially reserve-backed model where part of the supply is backed by cash equivalents and the rest managed algorithmically to maintain price stability.

Advantages: Algorithmic stablecoins offer the greatest decentralization potential and inherent scalability. Their transparent and verifiable code enhances trust and appeal.

Disadvantages: They are highly sensitive to market sentiment. If demand drops, prices may fall below target value, risking collapse. Furthermore, reliance on smart contracts and community consensus introduces governance risks such as coding vulnerabilities, hacking, manipulation, or conflicts of interest.

Centralized Stablecoins

Centralized stablecoins are typically backed by fiat currency held in off-chain bank accounts serving as reserves for on-chain tokens. They solve the problem of value anchoring for virtual assets by pegging digital tokens to real-world assets like USD or gold, ensuring price stability. They also address deposit and withdrawal challenges under regulatory frameworks, offering users a more reliable method for storing and transacting digital assets. Centralized stablecoins still dominate over 90% of the market share.

Currently, besides USD and GBP, many centralized stablecoin projects back their tokens with U.S. Treasuries. This means holding on-chain tokens equates to owning underlying U.S. Treasuries in traditional markets. These Treasuries are often institutionally custodied to ensure redeemability, and tokenizing them increases liquidity for underlying financial assets. Moreover, this setup enables interaction with DeFi components such as leveraged trading and lending. As a result, projects can obtain USD funding from crypto users at zero cost to purchase U.S. Treasuries and directly benefit from treasury yields.

However, centralized stablecoins come with several drawbacks:

1. Financial and regulatory risk: Relying on central issuers exposes users to issuer-level financial instability or regulatory penalties, which could impact the stablecoin's value and availability.

2. Limited application scope: Centralized stablecoins are primarily used in payments, lacking diversity and innovation in functionality.

III. Reasons Behind Recent Surge in Stablecoin Popularity

1. Rising U.S. Treasury Yields Exceeding DeFi Protocol Returns

Soaring Treasury yields have led TradFi returns to far outpace those in DeFi. Currently, the total stablecoin market cap stands at $130 billion, making it the 16th-largest holder of U.S. Treasuries, with annualized yields reaching 5% or higher. In contrast, DeFi platforms like Aave and Compound offer lending yields of around 3%, while AMMs on Uniswap provide approximately 2% returns. This disparity indicates that falling bond prices and rising interest rates are driving some investors toward traditional finance for better yields, while DeFi faces relatively lower returns.

2. New Stablecoin Projects Offering Revenue Sharing to Boost Market Share

Currently, most centralized stablecoin profits flow primarily to issuers and investors. For example, USDC shares some profits with its investor Coinbase, allowing users who hold USDC on Coinbase to earn up to 5% APY, attracting more users. Innovative projects are now emerging that extend profit-sharing beyond investors to include broader ecosystem participants.

3. Payment Companies Entering the Stablecoin Market

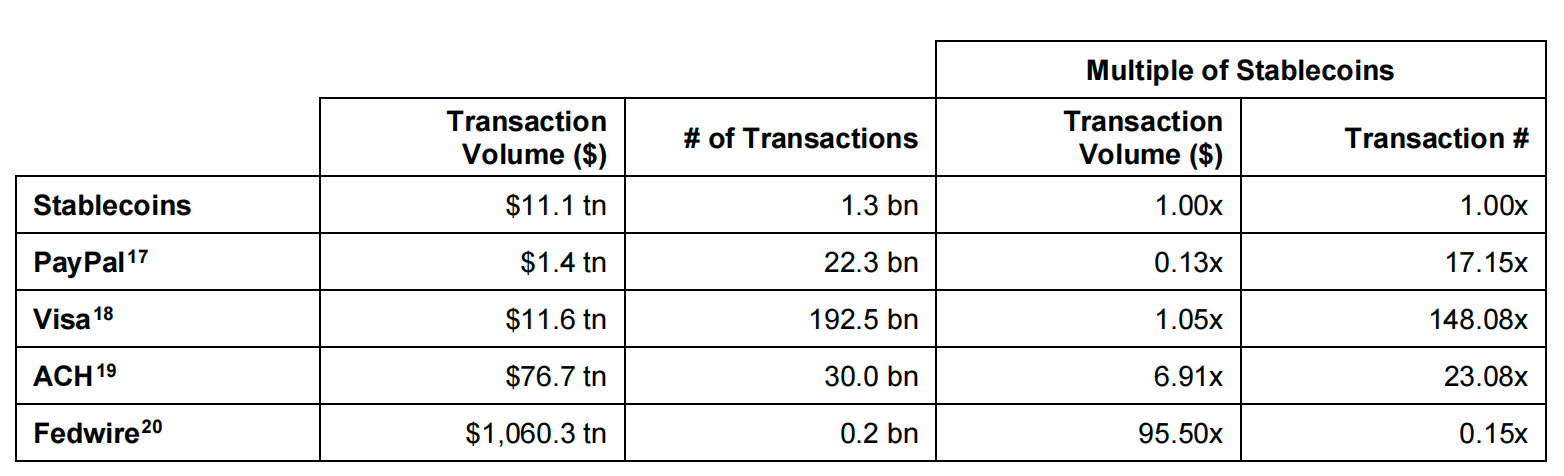

According to Brevan Howard’s report, stablecoins settled $11.1 trillion in on-chain transactions in 2022—surpassing PayPal’s $1.4 trillion and approaching Visa’s $11.6 trillion. This highlights the immense potential of stablecoins in payments, particularly in enabling efficient on-chain settlement systems. Stablecoins help projects hedge against revenue risks caused by declining Treasury yields. Additionally, in developing countries with underdeveloped payment and banking infrastructures, stablecoins are especially valuable, meeting local demands for fast, low-cost payment solutions. Thus, stablecoins are playing an increasingly vital role in the global financial ecosystem, particularly in advancing financial inclusion and economic growth.

Several companies focused on money movement rails are entering the stablecoin space, including well-known firms like PayPal and Visa. PYUSD is a stablecoin launched by PayPal in partnership with Paxos, backed by U.S. dollar deposits, short-term Treasuries, and cash equivalents. It can be exchanged within the PayPal app and interoperates with other cryptocurrencies and Venmo, one of the most popular payment apps in the U.S.

PYUSD is designed for seamless redemption via PayPal, providing a solid foundation for PayPal’s 431 million users to enter the Web3 world. As of now, PYUSD’s circulating supply is approximately $114.46 million, ranking fourteenth globally and representing 0.1% of total stablecoin circulation—still relatively small compared to other centralized stablecoins issued by trusted custodians like Paxos and First Digital, such as USDP and FDUSD.

The launch of PYUSD holds potentially significant implications for mass Web3 adoption. As a stablecoin backed by a renowned fintech company, it has the potential to bring millions of new users into the cryptocurrency ecosystem—a major step forward in mainstream acceptance. By combining the convenience of traditional financial services with the innovation of crypto, PYUSD could become a key product in future digital currency and payment landscapes.

IV. Impact of Ecosystem Participants on Stablecoin Projects

1. Exchanges

In the current high U.S. Treasury yield environment (>5%), according to H1 2023 financial reports, USDC contributed nearly half of Coinbase’s revenue—approximately $399 million. Meanwhile, Tether generates roughly $3 billion in annual profit effortlessly.

A. Close Exchange–Issuer Partnerships Drive Revenue

Coinbase’s Q1–Q2 2023 earnings revealed a substantial portion of its income came from a revenue-sharing agreement with Circle. By the end of Q3 2023, USDC balances on Coinbase reached $2.5 billion, up from $1.8 billion at the end of Q2. Circle and Coinbase jointly manage USDC through the Centre Consortium, sharing revenue based on USDC holdings. In August 2023, Coinbase Ventures acquired a minority stake in Circle, deepening their strategic alliance.

Moreover, Circle is actively expanding its Web2 business, positioning USDC as a key instrument for cross-border settlements. In September 2023, Visa announced the extension of Circle’s USDC settlement capabilities to the Solana blockchain, enhancing the speed of international payments. Visa became one of the first major companies to widely adopt Solana for settlements, contributing to a short-term rise in SOL’s price.

Market observations indicate that USDT is primarily used in derivatives trading on centralized exchanges, whereas USDC sees more frequent usage in Web3 dApps, with multiple stablecoin/RWA protocols accepting USDC as a settlement asset. For exchanges, selecting trustworthy stablecoin issuers is crucial. Traditional institutions like BNY Mellon carry higher credibility. Meanwhile, native crypto leaders like Tether and Circle face extremely high default costs and broad systemic impacts, resulting in relatively low incentives to default.

B. Payment Potential Drives Traffic for Exchanges and Issuers

Long-term, stablecoins hold the greatest potential in payments, especially cross-border transactions. Stablecoin issuers can collaborate with Web2 payment providers to integrate stablecoins into consumer payment flows, particularly in international transfers.

PayPal’s influence in Web2 is evident. As of Q4 2023, PayPal serves 4.33 million active retail accounts and 35 million active merchant accounts globally. Merchants can buy, hold, and send PYUSD via PayPal. Users on PayPal, Venmo, and Xoom platforms can purchase, receive, and transfer PYUSD. Venmo has about 80 million users in the U.S., while PayPal has around 320 million globally. Currently, PYUSD is only available to U.S. PayPal accounts due to PayPal’s Money Transmitter License. Given its massive Web2 user base and use cases, PYUSD retains growth potential. However, a key risk is that its issuer Paxos might halt issuance or freeze assets under regulatory pressure.

For Web3 users, PYUSD’s impact remains limited. It is listed on several exchanges, with a total circulation of approximately $158.9 million as of mid-November 2023, ranking 13th globally with a 0.15% market share. Due to its centralized nature and issuer-related risks, users may lack motivation to adopt PYUSD without additional incentives. Unless PYUSD establishes beneficial relationships with exchanges to gain traction among Web3 users, adoption may remain constrained.

2. Public Blockchains:

Table: TVL Rankings of Leading Stablecoin Projects on Major Public Blockchains

A. BUSD’s Impact on BSC’s TVL

BUSD operates across six blockchains, primarily circulating on Ethereum and BSC, with total market cap now down to $2 billion. The decline in BSC’s stablecoin market cap is largely attributed to the drop in BUSD’s value. On November 29, 2023, Binance announced plans to delist BUSD and fully convert it into FDUSD.

Native stablecoins significantly influence a blockchain’s TVL and overall ecosystem development. When stablecoin market cap dropped by 44%, corresponding protocol TVLs fell by 66%. This illustrates how stablecoin performance directly affects BSC’s ecosystem health.

Following BUSD’s exit from Binance’s stablecoin basket, Binance has increased support for the FDUSD ecosystem, allocating significant weight in its Launchpool and Earn programs.

B. TUSD’s Impact on Tron’s Ecosystem

After a series of strategic moves post-February 2023, TUSD’s market cap rose from around $1 billion to $2–3 billion.

Table: TUSD’s Series of Compliance Initiatives

C. USDC and Public Blockchains

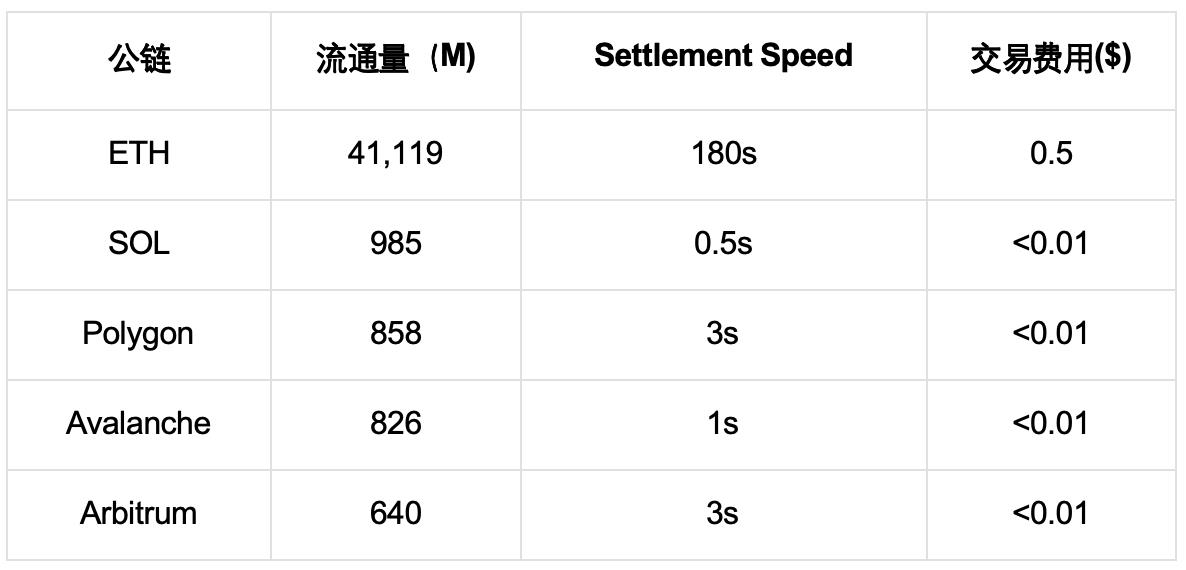

USDC has been issued across 15+ blockchains, with top three TVL concentrations on ETH, Solana, and Polygon. USDC is actively expanding its use cases, particularly in payments, including cross-border transactions.

Table: USDC TVL Distribution Across Different Blockchains

• USDC <> Solana: Recently, Visa partnered with Circle to use USDC on the Solana blockchain for on-chain settlements. This marks a significant integration between traditional finance and blockchain technology, aiming to deliver faster, cheaper cross-border payments. Solana was chosen for its high throughput and low fees, ideal for processing large volumes of microtransactions. This innovation is expected to significantly impact global payments, especially in accelerating cross-border transaction speeds.

• USDC <> Polygon: In October 2023, Circle announced native USDC issuance on the Polygon PoS mainnet. Major protocols in the Polygon ecosystem—including AAVE, Compound, Curve, QuickSwap, and Uniswap—have committed developer resources to support native USDC. Additionally, Circle expects to complete CCTP integration with the Polygon PoS Bridge by end of 2023, enabling cross-chain interoperability.

• USDC <> Sei: In mid-November 2023, Circle made a strategic investment in Sei Network, supporting native USDC issuance. The announcement highlighted Sei’s superior performance compared to Sui, Solana, and Aptos, with a TTF (Time to Finality) of 0.25 seconds.

D. DApp-Issued Stablecoins and Public Blockchains

The impact of stablecoins issued by leading DeFi protocols on public blockchains is a noteworthy area. Take Curve and Aave as examples—their initiatives in the stablecoin space carry significant implications for the broader crypto market and blockchain adoption.

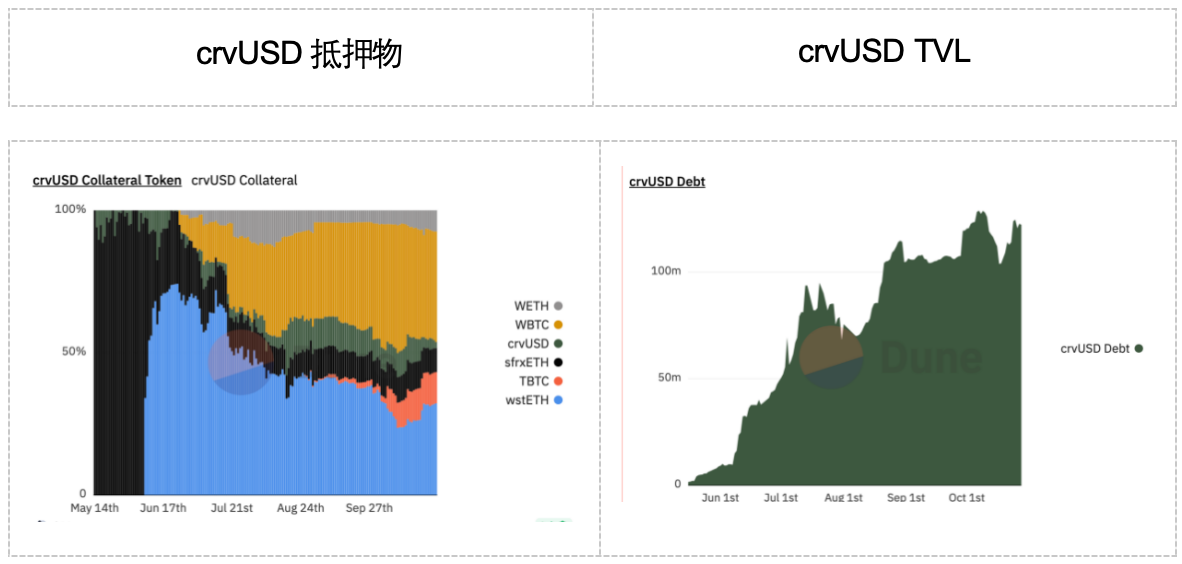

Curve launched its crvUSD stablecoin in May 2023—a protocol enabling users to mint crvUSD using various crypto assets (e.g., ETH, WETH, wstETH, WBTC) as collateral. Notably, after enabling WBTC as collateral in June 2023, crvUSD experienced significant growth. By November 2023, collateral value exceeded $100 million.

In May 2023, FRAX’s sfrxETH constituted most of Curve’s collateral. Subsequently, support for Lido’s wstETH and BitGo’s WBTC rapidly captured dominant market share. This demonstrates Curve’s substantial influence over which tokens gain widespread collateral adoption. Curve’s strategy not only strengthens its position in DeFi but may also profoundly affect asset liquidity and stablecoin usage patterns across blockchains.

These actions by top-tier DeFi protocols highlight the sector’s innovation and dynamism, reinforcing their pivotal roles in the crypto ecosystem. As more DeFi protocols engage in stablecoin issuance and management, we can expect new developments and challenges in blockchain usage, crypto liquidity, and overall market stability.

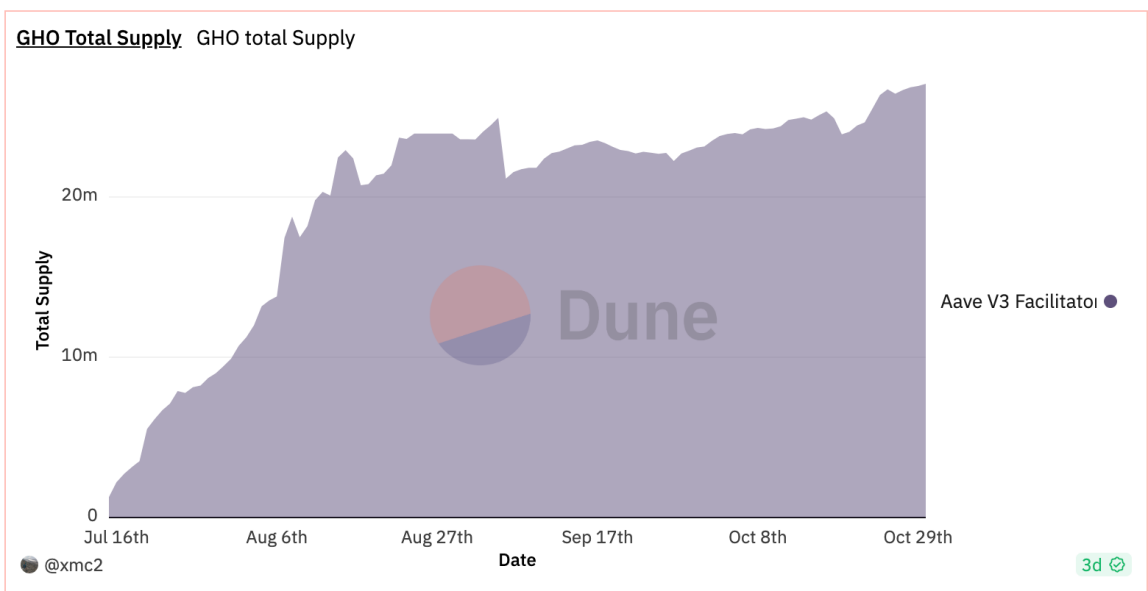

Aave, the largest lending protocol with $5.64 billion in TVL, introduced GHO—an overcollateralized stablecoin. All tokens supported by Aave v3 can serve as collateral, continuing to generate yield within the lending protocol. Since its July launch, GHO has accumulated over $20 million in TVL.

3. Stablecoin Issuers

Most stablecoin projects today are backed by highly liquid short-term assets such as USD and U.S. Treasuries, with near-zero default risk on underlying assets. As centralized entities, stablecoin issuers must ensure smooth entry and exit channels for users. The biggest risk lies in failing to honor redemptions during withdrawals, which could lead to ecosystem collapse.

Identifying trustworthy stablecoin issuers is a critical concern for ecosystem participants. Reviewing both the crypto ecosystem and traditional financial markets, native crypto custodians and traditional financial institutions—including banks, asset managers, and custodial platforms—such as Fireblocks, BitGo, BNY Mellon, and BlackRock—are best suited as stablecoin issuers due to their strong reputational credibility.

Adopting ETF-like asset management practices, where multiple parties share oversight via “joint monitoring agreements,” can enhance transparency and trust in fund storage and withdrawals. Complementing this with third-party on-chain audits and blockchain data tracking platforms like OKLink further strengthens fund security.

4. Regulatory Bodies:

The U.S. regulatory framework for cryptocurrencies has not yet been formally established. Until then, under U.S. federal securities law, a digital asset may be classified as a “security” if it meets the four-part Howey Test (a legal standard determining whether a transaction qualifies as an investment contract). The SEC first applied the Howey Test to digital assets in 2017. Although the 2019 framework outlined numerous non-determinative factors the SEC might consider when assessing whether a digital asset is a security, SEC Chair Gary Gensler stated in April 2022 that he believes nearly all digital assets qualify as securities.

Some U.S. senators are working to establish a comprehensive regulatory framework for digital assets, proposing to grant the Commodity Futures Trading Commission (CFTC) primary oversight authority. In April 2023, the first bill regulating payment stablecoins was introduced and revised in July 2023. This indicates no specific stablecoin regulation exists yet. However, stablecoin issuers must comply with existing laws, including anti-money laundering (AML) and Know Your Customer (KYC) requirements from FinCEN, and obtain state-level money transmitter licenses. Nevertheless, the bill does not clearly designate a federal regulator for payment stablecoins.

The SEC’s approach to regulating centralized stablecoin projects has sparked industry debate. Its “regulation by enforcement” strategy is viewed skeptically by some. For example, in June 2023, the SEC instructed Paxos to halt BUSD issuance, classifying it as a security. In response, Circle defended USDC’s purpose, emphasizing its primary use in payments rather than investment, arguing it should fall outside SEC jurisdiction. Additionally, in November 2023, PayPal’s PYUSD came under SEC scrutiny. In an April 2023 interview with New York Magazine, Chair Gensler noted that most cryptocurrencies could be considered securities and thus subject to regulation. The regulatory outlook for the U.S. stablecoin market remains uncertain, prompting ongoing industry vigilance.

Under current regulations, stablecoin issuers face both challenges and opportunities. Adhering to best practices—particularly securing crypto licenses from state authorities, especially the “Money Transmitter License” and New York’s “BitLicense”—is essential.

Paxos has obtained both the New York BitLicense and Money Transmitter Licenses from multiple states, establishing a compliant operational foundation. These licenses ensure strict legal compliance and bolster customer trust. For future stablecoin development, companies focusing on interoperability with traditional finance, real-world asset (RWA) backing, and long-term sustainability will gain competitive advantages by swiftly acquiring licenses and regulatory approvals. Such strategies may enable emerging players to challenge dominant incumbents like Circle.

Furthermore, the IRS classifies digital assets as property and includes them in the tax system—a critical consideration for stablecoin issuers and the broader crypto industry. Tax compliance in crypto transactions is a key domain, likely to evolve alongside market growth and regulatory tightening.

Therefore, stablecoin issuers must not only meet current regulatory requirements but also closely monitor upcoming rules and changes to adapt their operations accordingly.

Outside the U.S., the MiCA (Markets in Crypto-Assets) regulation, specifically targeting EU member states, introduces clear rules for stablecoins and related crypto assets, significantly impacting the industry. MiCA prohibits algorithmic stablecoins and bans stablecoins from generating yield, arguing that yield-bearing tokens should be classified as securities. This poses challenges for centralized stablecoins whose underlying assets naturally generate returns. If yields are passed to users, stablecoins resemble money market funds and are more likely to be deemed securities. Consequently, newly issued tokenized projects are often treated as securities. To comply, industry players typically partner with exchanges, payment processors, wallets, and DeFi protocols to offer indirect incentives. Other jurisdictions like Singapore and Hong Kong are also developing their own frameworks—for example, HKMA plans to release its stablecoin regulation in Q1 2024. These measures aim to increase market transparency and security, while presenting new challenges regarding stablecoin definitions and operations. As global regulatory frameworks clarify, issuers and users must stay vigilant to ensure compliance.

5. Custodial Service Providers:

The 2023 USDC depeg event triggered by Silicon Valley Bank’s collapse underscores the importance of secure underlying asset management.

Some stablecoin projects, such as PYUSD, mitigate risk by delegating asset management to Paxos—a licensed custodian provider holding New York’s BitLicense and regulated by the NYDFS—effectively isolating custody risks through third-party compliance.

Additionally, Circle partnered with BlackRock, the world’s largest asset manager, to establish the Circle Reserve Fund—a SEC-registered and regulated vehicle dedicated to managing USDC reserves, currently holding about 94% of USDC’s backing assets.

6. Traditional Trust Companies:

Based on research into multiple stablecoin issuers, most store underlying assets within trust companies, commonly employing SPV (Special Purpose Vehicle) structures to legally protect and isolate user assets. Establishing an SPV ensures complete separation between user assets and corporate balance sheets—a robust risk management practice. Legally, user assets belong to the SPV, insulating them from parent company bankruptcy, achieving “bankruptcy remoteness.”

Delaware is favored for entity formation due to its experienced bankruptcy courts and extensive case law guidance, enhancing legal safeguards.

For centralized stablecoins, since their underlying assets are typically off-chain, human involvement should be minimized and processes automated wherever possible. This reduces human error, increases transparency and efficiency, improves consistency and reliability, and lowers risks of manipulation or fraud—offering stronger protection for users and investors. In sum, establishing SPVs in Delaware, isolating assets, and automating operations greatly enhance the safety and stability of centralized stablecoins—critical for the healthy development of the crypto industry.

7. On-Chain Infrastructure:

M^ZERO Labs’ on-chain infrastructure stands out as a prime example. M^ZERO focuses on building decentralized infrastructure enabling institutional participants to allocate and manage assets on-chain. The platform operates in a fully transparent, open-source, and composable manner, connecting regulated financial institutions with decentralized applications to facilitate on-chain value transfer and collaboration.

V. Conclusion

As the cryptocurrency market transitioned from the 2021 peak to the 2023 bear market, stablecoins have emerged as a unique and vital category—demonstrating remarkable resilience amid volatility and highlighting their central role in the broader crypto ecosystem. While the total market cap shrank from $3 trillion to $1 trillion, the relative stability of stablecoin valuations reveals their potential as a “safe haven” within crypto. Dominant stablecoins like USDT and USDC, with their stability and high liquidity, have become indispensable components of the crypto market.

At the same time, the rapid evolution and diversification of the stablecoin market reflect ongoing innovation in the crypto space. From overcollateralized to algorithmic models, this diversity reflects responsiveness to diverse financial needs. Innovations in collateral types, liquidation mechanisms, and yield distribution strategies not only strengthen DeFi’s robustness but also serve as experimental grounds for future market shifts.

The rapidly shifting regulatory landscape remains a key factor shaping the future of stablecoins. As governments and regulators gradually intervene to establish policies for crypto and stablecoins, their development will inevitably be influenced by external forces. Increased regulation may push the market toward greater centralization, but it also opens new avenues for collaboration—especially between stablecoin projects, traditional financial institutions, and regulators.

Looking ahead, the role of stablecoins in the crypto ecosystem is expected to grow further. With technological advancements and maturing regulations, we may see wider adoption of stablecoins in financial services—especially in cross-border payments and clearing. Achieving this, however, will require continued progress in transparency, security, and compatibility with existing financial systems.

In summary, stablecoins are more than just a niche segment—they serve as a vital bridge connecting traditional finance and the digital currency world. Their development will be an ongoing journey requiring continuous innovation, adaptation, and cooperation to find their place in a dynamic market and regulatory environment. For market participants, understanding and adapting to these changes will be essential for long-term success. (This article is intended solely for industry ecosystem research, based on publicly available commercial and policy information. It does not endorse or promote any project.)

Appendix: Comprehensive Stablecoin Overview

Disclaimer: This article is intended solely for industry ecosystem research, based on publicly available commercial and policy information. It does not endorse or promote any project.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News