How RWA driven by high yields injects decentralized innovation vitality into DeFi?

TechFlow Selected TechFlow Selected

How RWA driven by high yields injects decentralized innovation vitality into DeFi?

Examine the RWA market structure, starting from the most stable aspects and extending toward yields and risks, progressively exploring its future development and trajectory.

Author: Nelson

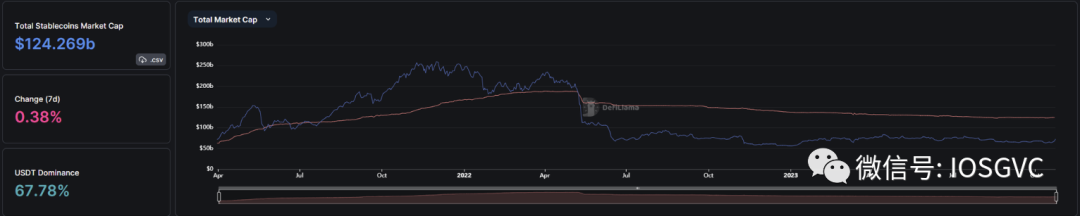

Until recently, stablecoins were the only real-world asset (RWA) category to gain significant attention. Introduced even before Ethereum’s inception, stablecoins replaced volatile cryptocurrencies as the standard medium of exchange on blockchains. Currently led by USDT with an $86.9 billion market cap and USDC at $24 billion, they collectively account for 7.5% of the entire crypto market’s $1.46 trillion valuation.

Over the past two years, as traditional finance abandoned zero-interest policies and government bond yields surpassed native DeFi yields, it became clear that the RWA story extends far beyond stablecoins.

Let us examine the RWA market structure, starting from the most stable aspects and extending toward yield and risk, progressively exploring its future development and trajectory.

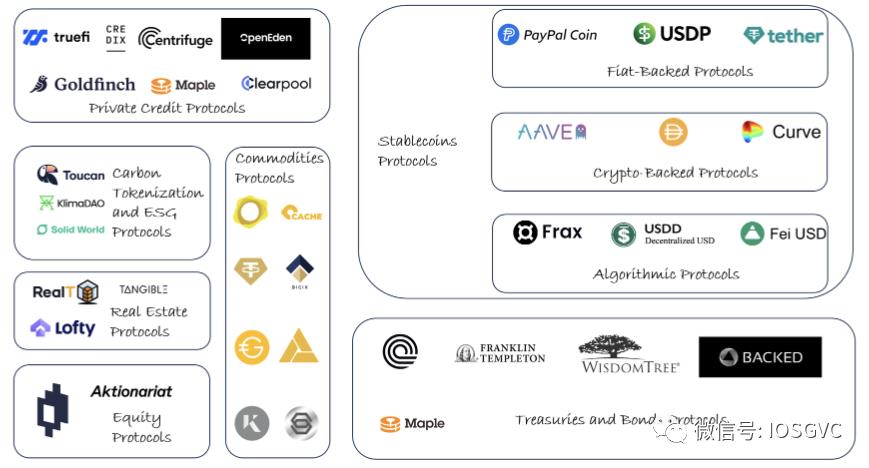

Types of RWA

Industry Development and Challenges

Stablecoins: The Pillar of RWA

In the ever-evolving cryptocurrency landscape, stablecoins have emerged as unsung heroes. Designed to maintain stability by pegging their value to traditional assets like the U.S. dollar, these digital currencies play a crucial role in channeling real-world capital into the crypto markets. Below are several observations about the stablecoin sector.

The Lucrative Stablecoin Ecosystem: Crypto’s Cash Cow

Stablecoins have proven to be a cash cow for the cryptocurrency industry, demonstrating clear product-market fit and presenting significant monetization opportunities. Indeed, they have become one of the most profitable segments within the crypto space.

Consider Tether (USDT), for example—during the first quarter of this year, its profits exceeded those of financial giant BlackRock. Tether achieved an impressive $1.48 billion in profit compared to BlackRock’s $1.16 billion. More remarkably, Tether manages funds that are 120 times smaller than BlackRock’s: $70 billion versus $8.5 trillion. Most of Tether’s revenue comes from reinvesting its fiat collateral, and recently, its balance sheet has increasingly favored U.S. Treasury bonds. Thanks to its network effects and users’ sole interest in exposure to stable products, Tether captures 100% of the underlying yield, resulting in extraordinary profitability.

However, this also brings up the first issue with existing stablecoin providers. Centralized stablecoins like Tether and Circle have been criticized for privatizing profits while socializing losses, raising fairness concerns. In March this year, the market suddenly realized that holding stablecoins is not risk-free, and holders could face losses due to issues related to collateral management—yet they receive no compensation for taking on such risks.

Additionally, there are widespread concerns regarding lack of transparency and exposure to undisclosed risks, as seen during the collapse of Silicon Valley Bank. At the time of the bank’s failure, the market was unaware that Circle had any exposure to SVB. On the other hand, although Tether remained unaffected by recent traditional bank failures, its balance sheet still carries exposure to illiquid venture-capital-style investments and lending activities—risks clearly not intended by USDT holders.

Both Circle and Tether are designed under the assumptions that their collateral will not depreciate and will remain 100% liquid—assumptions that do not hold in reality. This makes both Circle and Tether vulnerable to bank runs during black swan events. Only by luck did Circle avoid such a scenario following SVB’s collapse.

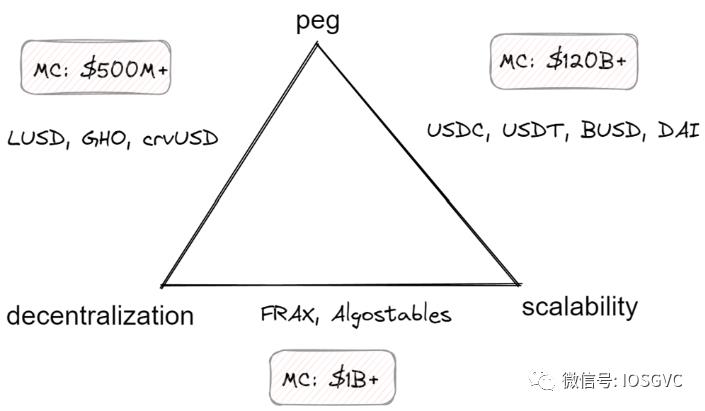

Crypto-native stablecoins attempt to mitigate the above risks; however, each design ultimately confronts the stablecoin trilemma—requiring a choice between two out of three:

-

Peg stability

-

Decentralization

-

Scalability

Bridging Traditional Finance and Decentralized Finance

The RWA sector has offered various products and protocols for years, but until recently, it received little attention beyond the aforementioned stablecoins—which function more as safe havens than funding tools within the crypto market. A key catalyst behind the recent surge is high-interest-rate policy.

The growing gap between native DeFi yields and traditional finance returns has sparked interest in solutions capable of bridging this divide. Once again, stablecoins take center stage—but this time, it's through DeFi-native stablecoin protocols, particularly MakerDAO.

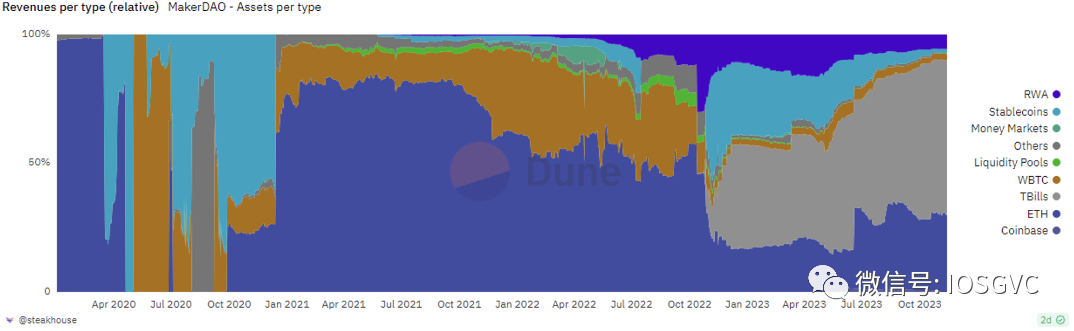

Specifically, MakerDAO—the third-largest DeFi protocol by total value locked (TVL)—strategically shifted its asset management approach by significantly increasing exposure to real-world assets (RWAs). Essentially, Maker’s governance was dissatisfied with holding non-productive and “risky” USDC on its balance sheet when productive and risk-free alternatives existed. This move directly exposed Maker to U.S. Treasuries, necessitating the construction of extensive off-chain infrastructure and legal frameworks. Fortunately, Maker is one of the better-resourced DAOs and successfully built this bridge. So far, it has succeeded. Over the past year, nearly 65% of MakerDAO’s fee income—amounting to $130 million—has come from RWAs.

Allocating part of Treasury yields to the DAI Savings Rate (DSR) module has created a major shift in DeFi, putting significant pressure on smaller competitors unable to keep pace with rising yields—such as Liquity’s LUSD and AAVE’s [GHO]—and pushing up overall interest rates in stablecoin money markets.

Blast, a recently announced Layer 2 solution, plans to allocate all stablecoins bridged to its rollup to the DSR, suggesting that Maker’s RWA strategy may drive increased demand for DAI and broader adoption across DeFi protocols.

However, despite helping Maker achieve scalability and optimize its finances, the RWA strategy has clearly moved it away from the status of a trustless DeFi protocol.

Challenges in Adopting Tokenized T-Bills in DeFi

Within the DeFi ecosystem, no project matches Maker’s $3 billion RWA balance sheet. One of the main challenges hindering broader RWA adoption is the limited transferability of tokenized Treasury bills within the DeFi ecosystem. Existing infrastructure often restricts their movement between different DeFi protocols and externally owned accounts (EOAs). As a result, tokenized RWA Treasuries face limitations in terms of their **utility as collateral** within the DeFi space.

For DAOs, direct access to RWA exposure is hindered by legal complexities and the inherent risks associated with the lack of off-chain representation. However, innovative solutions like Centrifuge Prime are addressing this issue. Centrifuge Prime has established legal structures enabling DAOs and individuals to securely access tokenized Treasuries, mitigating the traditional risks and legal barriers associated with such transactions. This development marks a significant step forward in expanding the investment capabilities of DAOs in secure and regulated assets.

Credit Markets: Higher Yields Come With Higher Risks

Credit markets aim to serve those seeking higher-risk opportunities and diversified solutions beyond Treasury bonds.

While DeFi protocols like Aave and Compound strive to build fully trustless and permissionless systems, projects like Centrifuge and Goldfinch introduce stablecoin holders to opportunities in off-chain lending markets. By relinquishing trustless and permissionless characteristics, they achieve greater capital efficiency, serve a wider range of use cases, and offer customized products for individual borrowers.

Borrowers, typically off-chain asset originators, must undergo traditional due diligence and/or provide some form of RWA collateral to support their borrowing activities. For instance, Goldfinch’s “trust through consensus” model allows borrowers to establish creditworthiness via collective third-party assessments. These projects resemble fintech companies more than pure DeFi protocols, primarily aiming to fill gaps in financial infrastructure in emerging markets. However, this also introduces a notable risk: these platforms may end up attracting high-risk borrowers rejected by traditional institutions, effectively creating a “lemons” market.

The current high-interest-rate environment has also dampened some credit market activity, making lenders reluctant to participate in alternative markets.

High interest rates have placed growth pressure on credit markets like Maple and Centrifuge’s invoice financing business, as investors currently prefer direct participation in bond markets. This is why both Centrifuge and Maple have added Treasury investment pools alongside their core offerings to diversify platform growth pressures.

Overall, this direction has yet to demonstrate strong product-market fit among crypto audiences. We observe that existing projects increasingly emphasize lower-risk alternatives such as investment-grade bonds, senior structured credit, commodity tokenization, and even real estate.

Exploring the Demand Side of RWA

Crypto-Native Users

Over the past nearly 15 years, crypto-native users have accumulated substantial on-chain wealth and developed habits of keeping most of their assets on-chain. For those accustomed to crypto rails, returning to cumbersome traditional finance (tradFi) infrastructure has become highly inconvenient. Yet, many are seeking to diversify their wealth into assets uncorrelated with cryptocurrencies. Tokenized real-world assets (RWA) allow them to enjoy the benefits of diversification while preserving the convenience and experience of staying on-chain.

Moreover, the growth of the on-chain economy has led multiple DAOs to manage eight- to nine-digit treasury budgets, mostly concentrated in volatile crypto assets. As part of prudent fiscal management, we expect to see more DAOs allocating portions of their balance sheets to RWAs.

Can the RWA Category Attract Traditional Finance Audiences Onto Crypto Rails?

For us, yes.

Some tokenized RWAs can be traded around the clock—for example, [Backed](https://backed.fi/) tokens can be freely traded anytime on decentralized exchanges (DEXs). This gives markets another venue to respond to new information in real time, even when traditional financial exchanges are closed.

As cryptocurrencies become a more mainstream asset class, overlap between crypto and stock investors will only increase. Traditional finance holders may become interested in leveraging DeFi’s composability and innovation—imagine a product similar to Liquity that allows users to take out zero-interest loans against their retirement investments in S&P 500 index ETFs. Such a product would undoubtedly find an audience.

Conclusion

Many people are wondering how these protocols will evolve when the high-interest-rate environment changes. We believe that while elevated rates provide short-term revenue relief, the long-term focus remains on each protocol’s core business. For example, MakerDAO’s primary long-term goal continues to be expanding the influence of DAI—both in issuance volume and use cases. Although Centrifuge earns revenue from its Treasury bill operations, its main future efforts will center on invoice finance (building programmable, decentralized invoice finance infrastructure). Similarly, Maple Finance’s long-term value lies in improving credit lending and borrowing—after past missteps, Maple is actively seeking credit strategies that better balance risk and capital efficiency. Ultimately, all these projects will return to or extend from their original missions.

Furthermore, since the rise of cryptocurrency, real-world assets (RWA) have gained significant traction within the crypto domain, especially following the success of stablecoins like USDT and USDC, which have become lucrative sectors in the crypto market. The RWA landscape within crypto is undergoing a transformative journey, revealing a nuanced picture filled with challenges and opportunities. At the forefront of this evolution are stablecoins, serving as the primary RWA and seamlessly integrating into the crypto market. Their widespread adoption signifies a proven product-market fit, offering a stable bridge between traditional financial systems and the dynamic world of decentralized finance (DeFi).

Yet, stablecoins also face challenges and risks—including profit distribution, lack of transparency, and scalability issues. A deeper look reveals a complex narrative. Centralized stablecoin entities generate substantial profits by investing user-deposited fiat, yet they face scrutiny for transferring underlying investment risks to users without sharing any of the returns. This dynamic highlights the delicate balance between entity profitability and fair treatment of their user communities.

Tokenized Treasury bills, acting as a bridge between traditional finance and DeFi, have drawn interest under favorable conditions, bringing credit lending protocols into focus. Tokenization of various assets—such as equities, real estate, and commodities—is expanding, offering broader investment opportunities. Despite integration limitations, DeFi protocols are making significant progress in building bridges for easier access. This evolution opens unique opportunities for DeFi-native users who have accumulated substantial on-chain wealth over the past decade.

The convergence of traditional financial products with blockchain technology signals innovation, unlocking novel financial instruments and strategies. As overlap between traditional and crypto investors grows, synergies between these two worlds are poised to redefine the financial landscape. The potential for collaboration offers prospects for tapping into previously untapped markets and creating new, inclusive financial ecosystems.

Overall, the future of RWA lies in asset and capital expansion, along with overcoming current challenges. Such progress is essential for diversification, convenience, access to restricted geographic regions, and regulatory support. However, it must be acknowledged that the process of RWA tokenization, while opening new pathways, also introduces trade-offs. Effective RWA integration inevitably compromises the trustlessness that has long defined the crypto space. Finding the right balance between innovation and decentralization will be the key challenge as we navigate this evolving domain.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News