As institutional interest grows, where is the Ethereum staking landscape headed?

TechFlow Selected TechFlow Selected

As institutional interest grows, where is the Ethereum staking landscape headed?

Ether ETFs with rewards are a natural extension of non-staked ether ETFs.

Author: Ronan

Translation: TechFlow

This article focuses on overlooked but critically important factors for the decentralization of Ethereum's staking layer. These include the impact and implications of Ethereum ETFs, challenges to decentralization, the scale of institutional capital flows, and the role of protocols like Lido.

I. Ethereum ETF Will Follow Bitcoin ETF Approval

Attention is turning toward spot Ethereum ETFs, with confidence in approval stemming from the SEC’s inconsistency in approving futures-based products while rejecting spot-based ones. BlackRock’s filing for a spot Ether ETF on November 9 further intensified this focus.

Given the existence of the CME Ether futures market and multiple futures-based Ethereum ETFs, the logic for approval appears highly transferable. Even the regulatory treatment of Ether in the U.S. leans away from classification as a security. A shift by Gensler or future regulators from prior positions seems unlikely for several reasons.

Indeed, the SEC recently excluded Ether from its legislation targeting securities listed on Coinbase.

II. Yield-Bearing Ethereum ETF Is a Natural Extension of Non-Staked ETH ETF

Before spot Ethereum ETFs are approved, issuers will rush to implement solutions allowing them to earn staking yield. Yield-bearing ETH is superior to non-yielding ETH and may attract new investors who have so far remained on the sidelines.

Issuers will compete to be the first to offer staking yield. Initially, it seems irrational for issuers to run their own validators due to knowledge barriers, business model challenges of node operation, and increased regulatory risk.

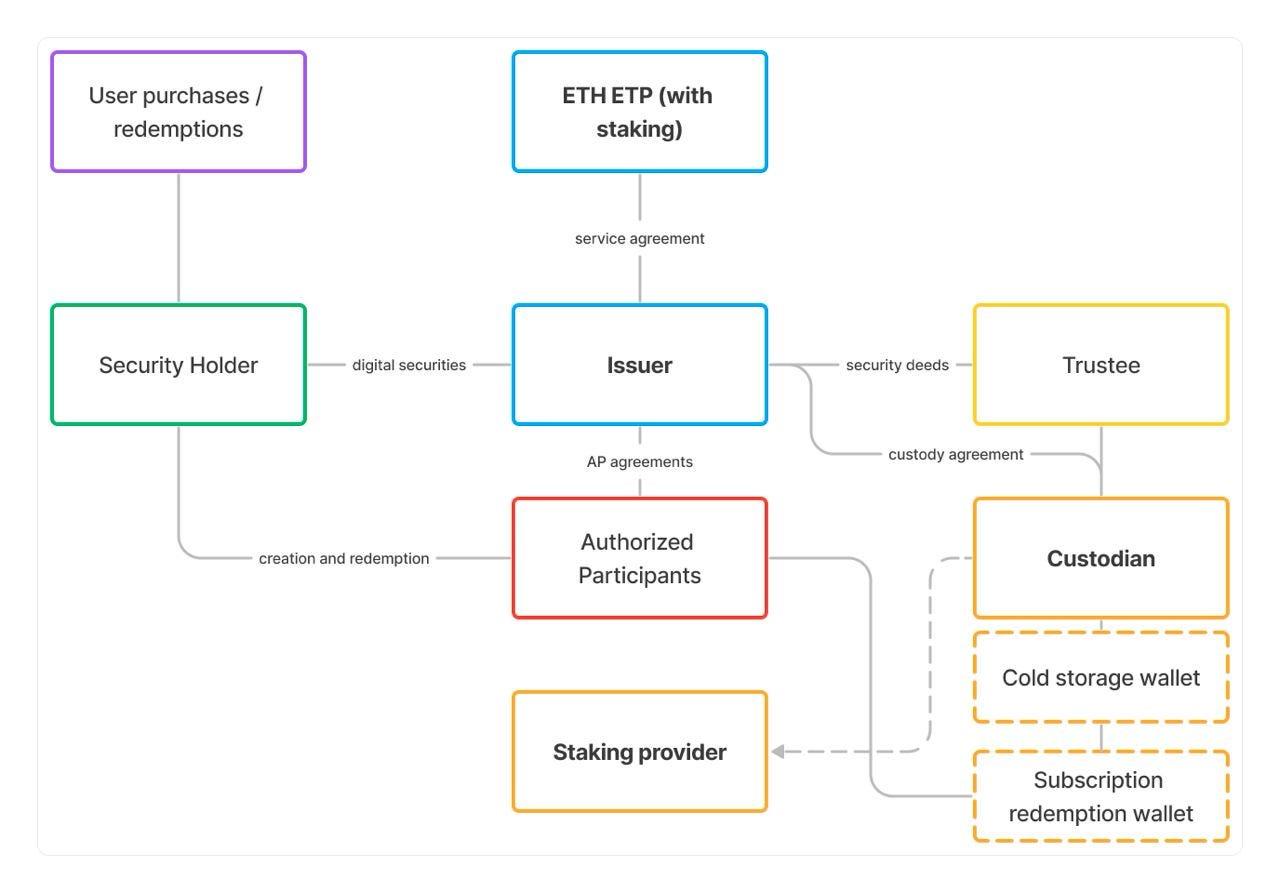

To enter the market quickly, issuers must propose a solution that fits within existing regulatory frameworks and can gain approval swiftly. The least burdensome path is for ETF issuers to contract with third-party centralized staking providers—including lending arrangements—where the provider takes a small fee.

This is already the approach taken by 21Shares’ staked Ethereum ETF, AETH. 21Shares custodies its ETH with Coinbase Custody and likely lends the underlying ETH to providers such as Coinbase Cloud, Blockdaemon, and Figment.

AETH has attracted $240.77 million in net assets, equivalent to 121,400 ETH, all staked via centralized providers. These inflows are entirely decoupled from yield, as a fixed percentage is programmatically staked regardless of return.

It is reasonable to assume U.S. ETF issuers will likely adopt similar lending arrangements as 21Shares’ AETH. This programmed capital flow could drive centralized providers to capture disproportionate market share compared to decentralized alternatives, especially since many custodians offer vertically integrated staking products (e.g., Coinbase Prime → Coinbase Cloud) or have existing service-level agreements (SLAs) with centralized staking providers like Figment. For example, given ARK’s partnership with 21Shares, it is plausible they would use the same providers as the AETH product.

III. Institutional Staking Will Shift Toward Liquid Alternatives, Presenting New Challenges for Ethereum Decentralization

Sophisticated institutions may seek staking providers outside ETF wrappers that offer better cost structures and greater utility. Decentralized protocols like Lido are already accessible to institutional clients across various custody, qualified custodian (QC), and regulated environments. As decentralized protocols, they provide a consistent experience and institutional-grade security, while remaining open to all market participants wishing to stake any amount of ETH.

Meanwhile, some new projects are positioning themselves specifically for institutional needs. Companies like Liquid Collective are building a “liquid staking solution designed for institutional compliance requirements.” Institutions can mint lsETH, which is staked through one of three centralized providers (Coinbase, Figment, and Staked), all of whom also govern the project. The rationale here is twofold:

-

Liquid staking is a superior product to standard staking—it preserves the monetary properties and most of the yield of your ETH.

-

Institutions must stake with KYC/AML-compliant providers, or else face civil and criminal liability.

The first point is fairly clear.

Liquid staking tokens (LSTs) can serve as collateral across DeFi, form the base asset in liquidity pools, and avoid withdrawal queue delays.

Moreover, institutional products like ETFs benefit from liquidity to manage fund redemptions smoothly—ideally within less than a day. For illiquid funds, this is typically managed by keeping a portion of ETH unstaked in custody. However, this introduces risks: a surge in withdrawals could trigger a de facto bank run as the rest of the ETH unstakes, while also dragging down yield during normal operations.

Holding liquid staking tokens enables smoother redemption management and allows a higher proportion of the fund’s ETH to be staked at any given time. For this to be viable, the LST must itself be liquid. Simply offering a token is insufficient if there isn’t sufficient on-chain and off-chain liquidity. Currently, the only LST with meaningful liquidity used by institutions is Lido’s stETH.

The second point is less clear. Regulated institutions typically have obligations to reduce the risk or possibility of money laundering or criminal facilitation. KYC/AML requirements exist to maintain an auditable trail of fund flows between institutions and their clients. Additionally, there may be higher standards for "qualified custodians." However, qualified custodians and institutions generally should be able to meet their KYC/AML obligations without compromising asset choice—whether that’s an LST or the staking provider.

Even if staking providers establish contractual relationships with asset owners or custodians, I do not believe regulators will create entirely new KYC/AML compliance obligations specific to Ethereum staking. I believe regulators will come to understand that Ethereum staking is a specialized computational activity that does not align with traditional or financial notions of “fund flows.” LST holders and custodians should be able to perform KYC/AML checks on assets within their purview and fulfill compliance duties to mitigate money laundering or terrorist financing risks.

Concentration of staking within centralized entities raises urgent challenges for the integrity of the Ethereum blockchain. Broadly speaking, the potential for disrupting the blockchain increases at different levels of staking concentration:

-

Block reorganization attacks

-

Finality delay

-

Fork choice manipulation

-

Coercion

The first two attack types disrupt normal blockchain operations. Ethereum already includes built-in incentives to deter such attempts—for example, gradually diluting the attacker’s rewards and stake balance. However, when a single operator controls 33% or more of staked ETH, even if attacking becomes costly, they may still begin delaying finality. At higher concentrations, such as 50%, an attacker can effectively fork the chain and select which fork to support. At 67% or above, the blockchain effectively becomes a centrally controlled delegated database.

These attacks are not merely theoretical—they strike at the core value proposition of Ethereum as a settlement layer.

Ethereum’s proof-of-stake mechanism allows centralized players to accumulate a large—and potentially controlling—share of total staked Ether through market forces alone. Centralized entities are already well-positioned to rapidly convert multi-line businesses (including custody relationships) into staking relationships, consolidating their dominance in staking. One such entity is already the largest validator on the network, with a 16% market share, operating multiple acquisition channels: cbETH and Coinbase Earn for retail users, and Coinbase Cloud and Coinbase Prime for institutions.

Behind this wave of new capital lies a potentially dangerous challenge to Ethereum’s neutrality—or what the Ethereum Foundation describes as a “Layer 0” attack on the “social layer.” Even with good intentions, introducing assumptions that only KYC/AML-compliant staking providers are “allowed,” despite no legal or technical basis, would accelerate adoption by centralized players who lock in market share through regulation.

Increased market share by centralized entities poses risks to Ethereum’s staking layer. They fundamentally operate under a different set of obligations than decentralized protocols. Decentralized protocols exist as incentive layers via smart contracts, coordinating activities among many participants.

For example, Rocket Pool’s rETH has nearly 20,000 holders, 9,000 RPL holders, and over 2,200 staking deposit addresses representing unique node operators. Or consider Lido, a smart contract layer coordinating 39 globally distributed node operators, nearly 300,000 stETH holders, and about 41,000 LDO holders.

In contrast, corporations have fiduciary duties to shareholders and are accountable to local legal authorities and regulators. While Ethereum’s decentralization might be somewhat relevant to corporate businesses (like exchanges), it does not supersede these two primary obligations.

There are also broader risks of overregulation—a soft “Layer 0” attack, even with good intentions. If Ethereum is to become the world’s settlement layer, it must possess nuclear-grade censorship resistance and credible neutrality. If centralized entities grow large enough, they will undermine Ethereum’s core mission.

IV. The Scale of Institutional Flows Could Be Substantial

Some may dismiss the arrival or impact of spot Ethereum ETFs due to perceived lack of institutional interest. However, precedents in commodities offer useful insights into how exchange-traded products (ETPs) can generate significant interest in new asset classes. As financial instruments, ETFs and ETPs are highly effective at providing standardized and democratized access for both institutional and retail investors. When these tools enter distribution channels used for institutional allocations, pension funds, or social security contributions, substantial capital flows into the underlying asset class.

The same benefits apply to spot Ethereum ETFs as seen with spot BTC ETFs. For instance, approximately 80% of U.S. wealth is controlled by financial advisors and institutions who can participate, with general regulatory and governmental recognition. We can expect this increased legitimacy and recognition to drive demand for Ethereum beyond ETF wrappers. Early signs of institutional interest are already visible. Intermediaries like Bitwise report potential allocations increasing from 1% to 5%. Brian Armstrong noted in Coinbase’s Q3 earnings that the number of institutional users had doubled to over 100.

Estimating the exact net inflow from institutions is difficult. However, gold’s GLD ETF attracted $3.1 billion in net inflows in just its first year. Buying any amount of physical gold before ETFs was far more challenging than buying BTC/ETH—you had to physically transport and store it, verify purity, and pay high dealer premiums. Gold ETFs improved upon the asset’s inherent characteristics and democratized its value proposition through massive fund allocations, making it accessible to millions of individual investors.

Bitcoin and Ethereum are digital native assets, capable of transferring billions of dollars in minutes. The entry barriers of physical gold simply do not exist. While ETFs don’t necessarily improve the fundamental value proposition of Bitcoin or Ethereum—and may even threaten it—they offer a similar degree of democratization and access to both asset classes.

In fact, the vast majority of people worldwide may never directly hold cryptocurrency, but could gain some financial exposure through pension allocations, private savings, or investments. Regulated financial channels in the developed world already have high penetration and capillarity. ETFs can help demystify the asset class, enabling cautious investors to participate easily within familiar frameworks like banks or brokerages.

V. What Does This Mean for Ethereum’s Staking Layer?

Large-scale, yield-insensitive inflows from institutions could push the total amount of staked ETH above levels suggested by economic principles or endogenous crypto variables. The vast majority of these inflows are likely to accumulate disproportionately with centralized providers, both inside and outside ETF wrappers. Greater staking concentration within centralized entities would weaken Ethereum’s censorship resistance and credible neutrality, with no credible counterbalance in sight.

VI. Lido as an Effective Counterbalance

Public discourse today largely centers on Lido—whether it controls too much staking and the potential attack vectors this might introduce in worst-case scenarios. Below is a brief overview of i) how much control Lido governance actually has over node operators, if any; ii) how the DAO handles governance risk; and iii) how the DAO plans to expand the node operator (NO) set and decentralize the validator pool.

-

Governance Risk: Hasu’s GOOSE submission + dual governance proposal

-

Expanding NO Set: Staking Router + DVT module

-

Decentralizing Validator Set: Jon Charbonneau’s PoG + Grandjean paper.

Also see this excellent article by Mike Neuder of the Ethereum Foundation on the real risks of Lido’s dominance.

Criticism of Lido largely rests on a static view of the staking market. It fails to account for how the staking market evolves and its actual dynamics. To fully assess the staking landscape, we must consider future growth and market forces:

-

Future Growth: Institutional adoption may accelerate centralization among centralized entities

-

Market Forces: (Liquidity) Staking exhibits winner-takes-most dynamics.

Much of this article outlines future growth—an often overlooked but crucial dimension. The winner-takes-most dynamic has been widely discussed in digital public spaces, but often lacks context around future expansion. Rational market incentives—including those aimed at preserving a decentralized Ethereum network—may not prevent institutions from taking the path of least resistance when deploying new capital into Ethereum.

The only effective check is increasing the market share of decentralized liquid staking protocols at the expense of centralized players. While multiple decentralized protocols may eventually gain sufficient share to form a robust backstop, Lido is currently the only viable option to maintain resilience and decentralization in Ethereum’s staking layer:

-

It has objectively succeeded in attracting new ETH holders, as the Lido smart contract now secures over 30% of all staked ETH, with stETH held by nearly 300,000 individuals

-

It has objectively succeeded in limiting the growth of individual node operators—while all operators use Lido to attract new staking deposits, none can grow their individual market share within Lido beyond others

-

Its governance is currently objectively minimal, and initiatives like dual governance will further reduce it.

Although Ethereum’s base layer is designed to be “governance-free” or to have very limited fork-choice governance, having one or more decentralized protocol layers can fill essential gaps that Ethereum cannot. As Jon Charbonneau described:

“In particular, LST governance can manage the additional subjective incentives needed for decentralized operators (e.g., different modules may receive different fees). A free market economy won’t lead to independent stakers or uniform staking distribution over the long term. Ethereum’s core protocol is largely built on the idea that it should be objective and opinionless wherever possible. However, achieving a diversified operator set will require subjective management and incentives.

While governance minimization is generally desirable, LSTs may always need some minimal form of governance. Some process is required to match demand for staking with the need to run validators. LST governance will always need to manage objective functions of the operator set (e.g., staking distribution targets, weights for different modules, geographic goals, etc.). This fine-tuning may not happen frequently, but such high-level goal-setting is crucial for monitoring and maintaining decentralization of the operator set.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News