Which U.S. stocks could emerge as winners amid the crypto boom?

TechFlow Selected TechFlow Selected

Which U.S. stocks could emerge as winners amid the crypto boom?

What real value will remain if the market gradually moves beyond the late-stage bubble?

Author: RockFlow

Key Takeaways

① Coinbase has carved out a unique niche in the complex world of crypto. Its future trajectory will largely depend on two questions: whether it can dominate U.S. crypto infrastructure and whether the crypto economy will become a meaningful part of the real economy.

② As one of the largest publicly traded corporate holders of Bitcoin, MicroStrategy’s core SaaS business limits its downside risk, while its strategy of continuously purchasing Bitcoin with low-cost capital offers substantial upside potential.

③ Marathon, as a leading Bitcoin mining company, operates fundamentally on energy arbitrage. Differentiated operational capabilities, hardware upgrades, and energy utilization strategies will be key competitive advantages enabling miners to outperform Bitcoin’s returns and survive across market cycles.

Every innovation cycle begins with speculation. Speculation often precedes reality, and fundamentals take time to catch up.

This was true for the internet over the past few decades. Despite suffering through the dot-com bubble burst in the late 1990s, it eventually gave rise to some of the world’s most valuable and profitable companies.

The crypto market may face similar challenges. To claim that the sector’s rapid expansion over the past decade was driven purely by fundamentals rather than speculation would clearly be false. The real question now is: if the market gradually moves beyond the post-bubble phase, what lasting value will remain? And which companies will represent this industry?

From today's vantage point, the RockFlow research team highlights which U.S.-listed companies are best positioned to survive as long-term players in the crypto space and potentially grow into true giants.

1. COIN: A Key Player in Infrastructure and Institutional Adoption

Coinbase has established a unique niche within the complex world of cryptocurrency. Its origins trace back to 2012, starting as an early Bitcoin-focused platform incubated by Y Combinator. Over a decade later, Coinbase has become a leading exchange for buying and selling digital assets, consistently pursuing a path of regulatory compliance.

In recent years, Coinbase has actively diversified beyond just being an exchange, expanding into broader blockchain technology—ranging from wallet infrastructure and staking services to layer-2 scaling solutions. The launch of Base, its L2 rollup, is a prime example.

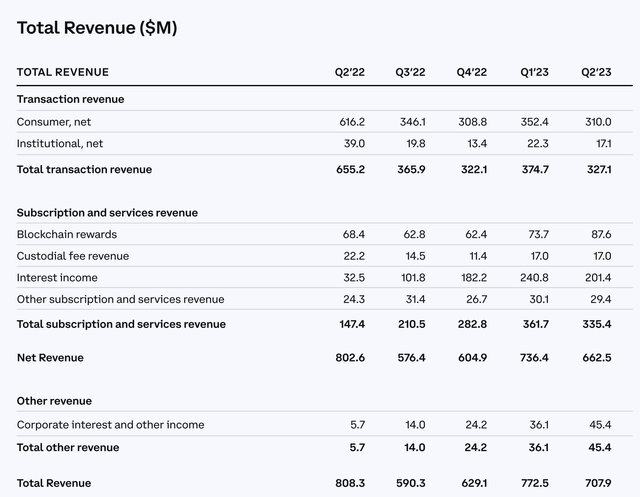

At the same time, its revenue streams have significantly diversified: transaction revenue from retail users has steadily declined (mainly due to sharp drops in BTC and ETH prices over recent quarters), while other revenue lines are surging. Interest income, in particular, jumped from $32.5 million in Q2 2022 to $201.4 million in Q2 2023. Below are Coinbase’s key financial metrics over the past five quarters:

In this volatile and nascent industry, Coinbase is building a reputation for trustworthiness—a product of unwavering commitment, transparent operations, and a user-first approach. This trust extends beyond its trading platform to a growing suite of diversified products—from multi-functional financial offerings like savings and rewards, to the Coinbase debit card, and further into Web3. Coinbase’s evolving ecosystem strategy is gradually unfolding.

Objectively speaking, Coinbase’s future valuation hinges largely on answers to four key questions:

First, can Coinbase dominate U.S. crypto market infrastructure?

Second, is Coinbase more than just an exchange?

Third, will the “crypto economy” become a meaningful component of the real economy?

Fourth, will Bitcoin and Ethereum prices continue to rise?

These four questions encapsulate nearly all of Coinbase’s narrative.

Can Coinbase dominate U.S. crypto infrastructure? Currently, Binance and others remain strong competitors in terms of trading volume and scale. However, a critical differentiator in crypto is trust—users need confidence in asset security and exchange compliance. Binance faces significant hurdles operating in the U.S., entangled in ongoing disputes with regulators like the SEC. In contrast, Coinbase operates under strict oversight from the CFTC, SEC, and financial regulators in the UK and Europe. Given this, Coinbase is likely to remain the preferred choice for both individual and institutional investors seeking secure exposure to Bitcoin.

Second, Coinbase is more than just an exchange. In traditional U.S. finance, institutions typically specialize in specific roles: Robinhood, TD Ameritrade, and Schwab focus on retail brokerage; State Street and BNY Mellon handle asset custody; PayPal, Visa, and Mastercard dominate payments; NYSE and Nasdaq operate stock exchanges.

The current crypto financial system looks very different. Coinbase already combines retail brokerage, custodial solutions, exchange operations, and is a leading player in crypto payments. It wouldn’t be inaccurate to describe Coinbase as the “crypto equivalent of NYSE + Robinhood + State Street + PayPal.”

Third, will the “crypto economy” become a meaningful part of the real economy? There is significant disagreement on this. Mature real-world markets—like agriculture, oil, and gas—thrive because industry participants profit from selling essential commodities. The oil market isn’t just about speculating on oil prices—it supports real businesses across the energy supply chain. The corn market isn’t just speculation—farmers and large institutions trade and hedge risks to deliver stable food prices. So, how many real commercial participants exist in crypto?

Currently, few people use Bitcoin as a payment method, and mainstream cryptocurrencies are unlikely to serve as everyday payment tools. Broader adoption and circulation will likely require final approval of a U.S. Bitcoin spot ETF, which could expand crypto’s practical “commercial use cases,” such as allowing individuals and institutions to hold Bitcoin directly. The crypto economy may persist as a speculative vehicle and emerging asset class, but achieving genuine commercial viability remains challenging.

Fourth, will Bitcoin and Ethereum prices continue to rise? Coinbase earns fees based on the value of assets traded or held on its platform, and it also holds a substantial amount of Bitcoin on its own balance sheet. Therefore, rising cryptocurrency prices directly boost its market value. Historically, persistent inflation and continuous fiscal and monetary stimulus have strengthened consensus around two primary safe-haven assets: gold and Bitcoin.

While the crypto industry faces challenges, this also means fewer remaining players can capture greater benefits. Coinbase is one of the few exchanges capable of genuinely attracting institutional investors. In the long run, it may outperform even the cryptocurrencies themselves.

2. MSTR: A Better Bet Than BTC

The SEC’s prolonged delays in making formal decisions on multiple Bitcoin spot ETF proposals have disappointed most investors. However, for those familiar with MicroStrategy and Bitcoin investors, this only enhances MSTR’s appeal—as it currently offers the most accessible way to gain Bitcoin exposure through a U.S. stock account.

MSTR is one of the largest publicly traded corporate holders of Bitcoin, thanks to its strategic decision in August 2020—to use excess cash, debt, and equity financing to buy Bitcoin continuously and hold it long-term.

According to its Q2 2023 earnings report, as of July 31, MSTR held 152,800 Bitcoins at a total cost of $4.53 billion, averaging $29,672 per Bitcoin. Of these, 15,731 were pledged as collateral for the company’s 2028 secured notes, while the remaining 137,069 (about 90%) remained unencumbered.

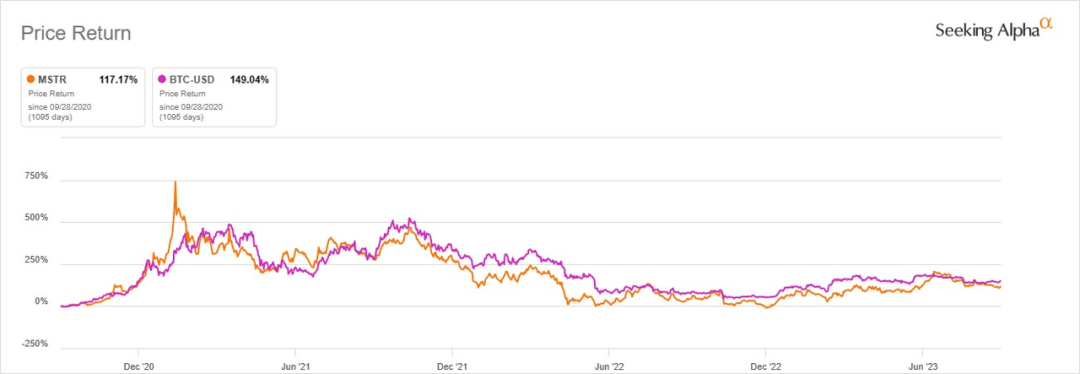

Since launching its “buy and hold” Bitcoin strategy three years ago, MSTR’s stock price has shown a strong correlation with Bitcoin’s price. As shown in the chart below:

For investors seeking gains from rising BTC prices, MSTR is not the only option. Stocks like Marathon Digital and Riot Platforms—Bitcoin miners—and exchanges like Coinbase also move in tandem with Bitcoin. However, unlike these, MSTR possesses a foundational core business, which is a significant competitive advantage.

Core Business Stability Limits Downside Risk

MSTR is also a SaaS company, having provided enterprise analytics software and services for decades. It serves a solid customer base—including major names like Hilton and Sony—with highly predictable annual revenue: $499 million in 2022, $511 million in 2021, $481 million in 2020, and $486 million in 2019. Analysts project $501 million in revenue for 2023.

MSTR is migrating its enterprise software clients to the cloud, shifting revenue from product licensing to subscription models. So far, this transition has proven successful, with high renewal rates: 93% in Q2 2023, marking the sixth consecutive quarter above 90%.

To keep pace with technological trends, MSTR’s core analytics platform is exploring integration with AI. The company is expanding its partnership with Microsoft, integrating its analytics capabilities with Azure OpenAI and Microsoft 365. MSTR is also pursuing further innovation through MicroStrategy Lightning, aiming to leverage the Bitcoin network for new e-commerce applications and cybersecurity solutions.

While these initiatives are unlikely to generate explosive revenue growth, they signal healthy development in MSTR’s core business, meaning it can reliably generate sufficient cash flow to cover operating costs—thereby limiting its stock’s downside risk.

From a valuation standpoint, MSTR’s current stock price appears reasonable compared to other software companies. The key difference is that MSTR is not just another software firm—it holds over 137,000 unpledged Bitcoins. This gives its stock significant potential to outperform other tech giants and SaaS peers.

Advantage of Accessing Low-Cost Capital

Another key reason investors favor MSTR is its ability to raise capital under attractive terms. The company currently has $2.2 billion in outstanding debt and convertible notes, with a weighted average interest rate of approximately 1.6%. Compared to a 2.1% average rate at the end of 2022, this reduces annual interest expenses by over $15 million.

Using low-cost debt to continuously acquire BTC is a smart strategy. As the crypto market improves in the coming quarters—potentially catalyzed by SEC approval of a Bitcoin spot ETF, the April 2024 halving, and declining interest rates amid lower inflation—Bitcoin’s capital appreciation is expected to exceed debt and interest costs.

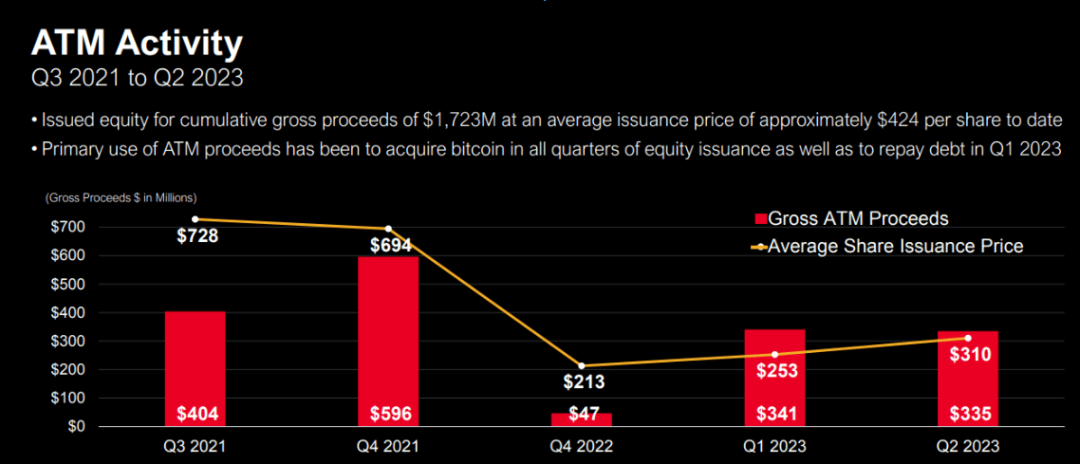

Issuing new shares is another funding avenue for MSTR. Since Q3 2021, it has raised $1.7 billion through its ATM program, with an average share price of around $424. The proceeds have primarily been used to purchase more Bitcoin.

A unique aspect of MSTR’s ATM program is that, compared to other Bitcoin players like MARA and RIOT who frequently issue new shares, its increase in outstanding shares has been minimal.

MSTR’s total shares outstanding rose from 11.3 million in 2021 to 14.1 million in the latest quarter. In contrast, MARA’s shares jumped from 102.7 million to 174.2 million, and RIOT’s increased from 117.3 million to 185.3 million over the same period.

Slower share count growth means MSTR retains greater capacity to issue additional shares for future fundraising. Additionally, on September 24, MSTR sold 403,362 shares, generating net proceeds of $147.3 million, all used to buy Bitcoin.

Risk Factors

It’s important to note two potential risks for MSTR. First, any future decision to sell part or all of its Bitcoin holdings could trigger an overly negative investor reaction. Thus, the company must continue taking on debt and issuing shares to sustain its Bitcoin strategy. However, there’s no guarantee it can keep raising capital on attractive terms, especially if Bitcoin prices remain flat—or worse, decline sharply. Recall that during the 2022 bear market, many leveraged crypto firms went bankrupt.

The second risk involves valuation. While investors can use P/E ratios to assess its software business value, GAAP accounting requires MSTR to recognize impairment charges quarterly whenever the fair value of its Bitcoin holdings declines. This leads to frequent impairment expenses on its financial statements. Given Bitcoin’s extreme short-term volatility (e.g., $24 million in Q2 2023 vs. $918 million in Q2 2022), this complicates an already difficult valuation process.

3. MARA: Is Mining a Good Business?

Marathon is a Bitcoin mining company offering investors indirect exposure to Bitcoin. Miner stocks generally show strong positive correlation with Bitcoin prices, and mining firms effectively act as leveraged plays on cryptocurrency.

Historically, when Bitcoin rises, miner stocks tend to rise even more, as investor sentiment becomes extremely bullish, anticipating a multiplier effect. Conversely, when Bitcoin falls, miners suffer disproportionately.

Mining is fundamentally an arbitrage business. Rather than focusing solely on Bitcoin’s technical details, miners need operational expertise—specifically, mastering how to efficiently run energy arbitrage operations. Top-tier mining companies get excited about innovations in cooling systems, new architectures, advanced transformers, or novel energy arbitrage strategies.

Arbitrage is crucial—it’s one of the key differentiators allowing miners to outperform competitors. Leading miners require top-tier equipment, the lowest production costs, and, most importantly, leadership that understands energy arbitrage—especially a skilled CFO.

They may sometimes shut down machines when energy recovery programs offer higher profits. An experienced CFO is vital for guiding a mining company through cyclical bear markets and "crypto winters."

Marathon’s Q2 2023 earnings report, released on August 8, revealed its current state: revenue grew 228.5% year-on-year, but net loss widened to $21.3 million (nearly double Q1’s $7.2 million). This reflects high Bitcoin production costs, suboptimal market prices, and heavy operational expenses including energy.

Despite missing expectations, MARA’s performance still shows significant year-over-year improvement. Bitcoin production surged 314% year-on-year, averaging 32 BTC per day, though lower average BTC prices (down 14%) dampened revenue.

The production increase stemmed from a 54% rise in computing power during Q2, reaching 17.7 EH/s—a record high. Operational hash rate continued climbing after Q2, hitting ~19 EH/s in July.

Profitability is tougher for miners than for exchanges or asset managers. Beyond common regulatory headwinds in crypto, since Bitcoin is their primary revenue source, price volatility heavily impacts miners’ profits and cash flows.

Moreover, the next Bitcoin halving is expected around April 2024. With block rewards cut in half, miner revenues may shrink. The halving also increases mining difficulty, forcing miners to upgrade to more powerful hardware. Stronger hardware drives up energy costs and overall operating expenses—challenges miners cannot easily avoid.

Therefore, compared to exchanges and asset management, mining represents a higher-risk crypto investment.

4. Final Thoughts

The crypto industry itself has gone through multiple hype cycles, each fueled by speculation around innovative triggers. These cycles have brought greater attention, users, and capital to the ecosystem, building upon previous progress to expand the possibilities of crypto technology.

Now, the industry may have reached a pivotal stage—where enough puzzle pieces exist to be reassembled in ways that meet broader needs and enable real-world use cases, potentially propelling the sector into a new era.

Throughout this journey, even if you’re not directly involved in crypto, you can still support the companies you believe in through investment. Below is a selection curated by the RockFlow research team of leading crypto-related U.S. stocks and crypto strategy ETFs:

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News