Digital Transformation Thoughts: Web3.0 and Banking

TechFlow Selected TechFlow Selected

Digital Transformation Thoughts: Web3.0 and Banking

Compared to virtual asset investments and RWA, stablecoins are best suited to the nature of banking operations and currently have the clearest entry path.

Author | Chan Chi Tong

Recently, OKLink Research Institute released a major report titled "Global Banking Crypto Landscape 2023", which has drawn significant attention from the banking sector and financial regulators. By analyzing the crypto strategies of over 70 global banks, the report concludes that with rising global adoption and technological maturity, crypto assets have become an innovation frontier that banks can neither ignore nor afford to miss.

A seasoned professional in traditional finance, Mr. Chan Chi Tong brings decades of banking experience alongside deep research and unique insights into Web3 and crypto assets. Like OKLink Research Institute, Mr. Chan believes that crypto assets represent an unavoidable market for banks, and Hong Kong can serve as a testing ground for crypto innovation, continuing its role as a bridge between East and West.

Based on his ongoing research and reflections on virtual assets, Web3.0, and banking, Mr. Chan recently completed an article titled "Digital Transformation Thoughts: Web3.0 and Banks." In it, he argues that compared to virtual asset investment and RWA (Real World Assets), stablecoins best align with the core nature of banking business and currently offer the clearest entry path. Hong Kong-based banks could participate in stablecoin operations by offering stablecoin-related services to individual clients, providing banking settlement services to qualified Virtual Asset Service Providers (VASPs), and eventually building a SEN-like payment and settlement system similar to Silvergate Bank as customer bases grow.

In Mr. Chan’s view, bank participation in virtual assets not only enhances brand visibility but also improves customer structure and diversifies revenue streams. More importantly, incorporating virtual assets will fundamentally reshape a bank's product ecosystem—insights that closely resonate with the conclusions drawn by OKLink Research Institute in its “Global Banking Crypto Landscape 2023” report.

We publish this article here for our readers.

Below is Mr. Chan Chi Tong’s article (edited).

Tracing Hong Kong Government's Web3 Policy Development

The Hong Kong government is advancing the construction of a global virtual asset hub at an unprecedented speed and determination.

According to PANews' compilation, Hong Kong began issuing policy guidelines related to virtual assets as early as 2018. However, prior to 2023, these policies did not attract significant market attention. Starting in 2023, due to a proactive shift in Hong Kong’s stance toward virtual assets and Web3.0, the government and regulatory bodies—including the Hong Kong Monetary Authority (HKMA) and the Securities and Futures Commission (SFC)—issued numerous meaningful declarations and policies, actively promoting real-world implementation of virtual asset businesses. These actions have significantly attracted global Web3.0 industry participants.

Hong Kong’s push for virtual assets stands out particularly against the backdrop of China’s domestic ban on cryptocurrency trading and the U.S.’s strict regulation of crypto exchanges. This inevitably raises speculation about whether the Hong Kong government has coordinated with central authorities regarding virtual asset development. Furthermore, amid the broader context of decoupling between China and the U.S., can Hong Kong maintain its status as an international financial center by leveraging virtual assets?The unified policy drive across Hong Kong’s administration at least demonstrates remarkable courage and resolve—something highly unexpected by both traditional financial institutions and Web3 players—and explains why the HKMA has unusually called on banks to open accounts for crypto service providers, yet still sees few takers.

In the shadows of formal policy, Hong Kong also hosts cryptocurrency or stablecoin exchange shops. The operational essence of these shops is no different from the scope regulated by the HKMA and SFC, yet there has never been any requirement for them to apply with these regulators. This may be related to the fact that traditional money changers are overseen by Hong Kong Customs.

Responses and Actions from Different Institutional Players

On August 7, 2023, U.S. payments giant PayPal announced the launch of its stablecoin, PayPal USD (PYUSD), becoming the first tech giant to issue a stablecoin. Patrick McHenry, Chairman of the U.S. House Committee on Financial Services, stated, “This is a clear signal that stablecoins—when issued under a clear regulatory framework—can become pillars of our 21st-century payment system.”

The choices made by asset management and payment giants underscore the growing appeal of virtual assets to traditional finance. Within the banking sector, both traditional commercial banks and modern tech-driven banks have pioneers actively positioning themselves.

In 2020, DBS Bank announced the launch of the "DBS Digital Exchange," aiming to build a comprehensive digital asset ecosystem for corporate, institutional, and accredited investors, offering services including security token offerings, cryptocurrency trading, and digital custody.

On the fintech banking front, although Silvergate Bank and Signature Bank failed during this year’s U.S. dollar interest rate hiking cycle, their success stories within the crypto industry remain important blueprints for bank participation in virtual assets.

Take Silvergate Bank: it did not originate in the crypto space but started as a real estate financing bank. In January 2014, Silvergate identified an opportunity as most banks were unwilling to provide virtual asset-related services—a situation very similar to Hong Kong today:

Most banks then refused to engage with virtual assets; some even closed personal accounts upon detecting fund transfers to or from crypto exchanges.

Buying and selling cryptocurrencies using USD is a 24/7 global activity, but traditional financial systems for handling fiat currency are slow and bound by official clearing hours.

Silvergate therefore built a real-time payment system—the Silvergate Exchange Network (SEN)—to facilitate crypto trading, enabling seamless 24/7 inter-account transactions with instant settlement, unlike traditional banks that halt cross-border operations after business hours. This attracted a large number of institutional traders and crypto exchanges.

The SEN system led customers to voluntarily deposit tens of billions of dollars into Silvergate, often without demanding interest—resulting in massive low-cost and zero-cost deposits. Since 2017, customer deposits at Silvergate grew nearly sevenfold, peaking above $11 billion.

Signature Bank similarly developed its own real-time payment system, Signet.

Although both banks ultimately collapsed in 2023, the low-cost funding base and profitability enabled by being crypto-friendly remain an attractive prospect for every bank.

On the local Hong Kong front, Bloomberg reported that ZA Bank—the city’s largest virtual bank—is pushing forward fiat-to-crypto exchange services. On April 11, CEO Yao Wensong said ZA Bank would act as a settlement bank, allowing customers to deposit crypto tokens via licensed exchanges and withdraw funds in HKD, USD, or other fiat currencies.

This business model is already operational on HashKey and OSL, Hong Kong’s two most prominent licensed crypto exchanges. ZA Bank plans to extend the same service to other exchanges once they obtain licenses.

Possible Participation Paths for Hong Kong-Based Banks

Judging from Hong Kong’s policy direction and the strategic moves of major international players, virtual asset investment, stablecoin operations, and real-world asset tokenization (RWA) stand out as three primary business avenues. From a banking perspective, compared to virtual asset investment and RWA, stablecoins best align with the fundamental nature of banking and currently offer the clearest entry path.

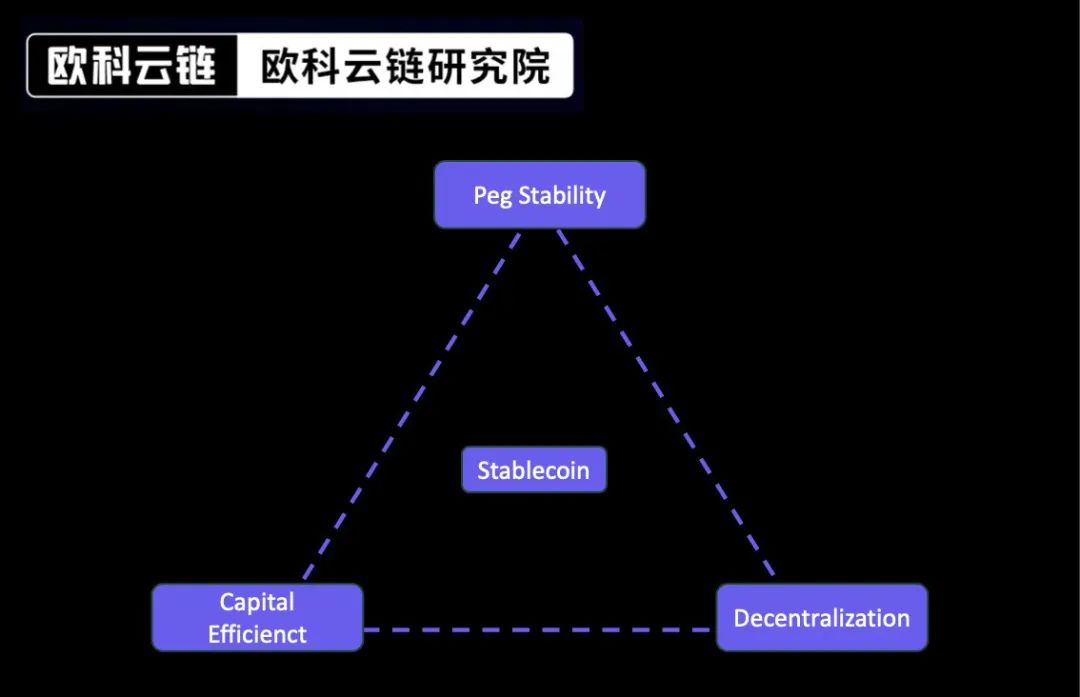

There are currently three mainstream approaches to developing stablecoins: asset-backed stablecoins like USDT and USDC, crypto-collateralized stablecoins like DAI, and algorithmic stablecoins like UST.

Each design comes with inherent flaws. In the industry, this trade-off is commonly referred to as the “stablecoin trilemma,” as it is impossible to simultaneously achieve all three desirable properties—peg stability, decentralization, and capital efficiency. Current projects typically prioritize two of the three, meaning advantages in two areas require compromise in the third. In summary:

-

Asset-backed stablecoins such as USDC and USDT are known for their stability and capital efficiency, backed 1:1 by reserves, but are centrally controlled—introducing dependency risks, as seen in USDC’s exposure to Silicon Valley Bank and USDT’s lack of transparency.

-

Crypto-collateralized stablecoins like DAI offer stability and decentralization, but require higher collateral ratios for minting, resulting in lower capital efficiency than other options.

-

Algorithmic stablecoins like UST offer decentralization and high capital efficiency with unique peg-maintenance mechanisms, but lack operational history and carry inherent structural vulnerabilities that pose potential price instability risks.

Due to this trilemma, stablecoins are often called the “holy grail” of Web3, with each issuer seeking its own solution.

According to the HKMA’s policy direction, only asset-backed stablecoins are permitted, to ensure a 1:1 peg mechanism with fiat currencies and avoid volatility issues. Among asset-backed stablecoins, USDT—issued by an unregulated entity—would necessarily be excluded. Therefore, compliant stablecoin issuers like Circle and Paxos, which already hold regulatory licenses, would be the preferred partners for banks.

Business Directions and Revenue Analysis for Banks Entering Stablecoins

Banks entering stablecoin operations could consider the following business directions:

1. Providing stablecoin-related services to individual clients

One of the most promising use cases in the crypto ecosystem is on- and off-ramps. For individual investors, remittance and exchange services between fiat and stablecoins are in high demand. Yet, apart from ZA Bank, no major Hong Kong bank has clearly committed to offering such services.

In practice, banks can gradually roll out stablecoin services for individuals.

First, facilitating wire transfers between individual customers and compliant stablecoin issuers. Outbound transfers involve minimal compliance costs—banks simply verify the source of funds under existing AML/CFT requirements, just like standard fiat remittances.

Second, accepting inbound USD transfers (or other compliant fiat currencies in the future) from compliant stablecoin issuers to individual customers. Since individuals must undergo KYC/AML procedures at the stablecoin issuer, and the sending bank performs KYC/AML checks during remittance, this process is theoretically no different from conventional inbound fiat transfers.

Finally, banks could partner with compliant stablecoin companies to offer direct fiat-stablecoin exchange services for retail customers, with the stablecoin issuer acting as the counterparty.

2. Providing banking settlement services to qualified Virtual Asset Service Providers (VASPs)

The current market situation in Hong Kong mirrors what Silvergate faced in the U.S.: banks remain hesitant to provide bank accounts to VASPs. Even after two meetings convened by the HKMA, no bank has stepped forward—an unusual reluctance in any business context.

Banks could initiate discussions with licensed exchanges like HashKey and OSL to provide bank accounts, primarily supporting remittances between these platforms and compliant stablecoin issuers, on/off-ramp activities for individual users, and potentially custodial services if these exchanges issue their own stablecoins in the future.

3. Building a Silvergate-style SEN-like payment and settlement system as the customer base grows

As a bank’s crypto client base expands, it could consider establishing a SEN-like payment and settlement system modeled after Silvergate Bank. Structurally similar to internal bank clearing systems, the initial development cost would not be prohibitively high if limited to intra-bank settlements.

Bank benefits would include:

1. Strong brand marketing effect

Similar to ZA Bank’s announcement, positioning oneself as crypto-friendly generates significant media exposure and user traffic. For small- and medium-sized traditional banks, this presents a golden opportunity to rebrand and enhance visibility. Even if compliance costs limit full-scale rollout, early movers gain a distinct identity and first-mover advantage.

2. Opportunity to improve customer mix

Virtual asset investors tend to be young, especially Gen Z born after the 1990s. Given the scarcity of crypto-friendly banks, institutions offering on/off-ramp services will strongly attract these younger customers—offering traditional banks, whose clientele skews older, a valuable chance to rejuvenate their customer base.

For corporate clients, take Cyberport’s 150 resident firms as an example: a bank declaring itself crypto-friendly could achieve powerful network effects, attracting entire sectors to open accounts.

For cross-border clients, given China’s domestic ban on crypto trading, opening a Hong Kong account with access to virtual asset trading holds strong appeal for mainland residents. It’s no exaggeration to predict that tourists’ spending in Hong Kong—from luxury goods to insurance and time deposits—will soon extend to virtual assets.

3. Potential profit opportunities from stablecoins

Beyond simple exchange spread income—which is already substantial—stablecoins offer exceptional profit potential.

Take Tether, issuer of USDT: according to its Q2 2023 report, USDT’s total assets grew from $66 billion at the start of the year to $86 billion, with over $55 billion invested in risk-free assets like U.S. Treasuries—the main source of profits.

Reports indicate Tether earned over $1 billion in Q2 and $1.48 billion in Q1, potentially reaching $4 billion in annual profit—surpassing even BlackRock, despite having fewer than 50 employees.

Similarly, Silvergate Bank’s SEN system attracted vast zero- and low-cost deposits, fueling its bond investments and lending activities.

Smaller banks face significant disadvantages versus larger peers in funding sources—for instance, they are disadvantaged in competing for CASA deposits due to inferior clearing systems, lose out in bidding for large corporate deposits due to loan pricing limitations, and face higher borrowing costs in interbank markets due to lower credit ratings.

Therefore, accessing large volumes of low-cost funding through the virtual asset sector would strongly support asset growth and improve net interest margins.

4. Virtual asset integration will reshape the bank’s product ecosystem

The operation of distributed ledgers in virtual assets will fundamentally transform a bank’s product architecture.

In clearing and settlement, stablecoins operating on Ethereum networks can function entirely outside the traditional SWIFT system, enabling new models where information flows and fund flows converge.

In lending, crypto-collateralized personal loans could improve Hong Kong’s current personal credit offerings, which are dominated by unsecured and mortgage loans. Even 100% time-deposit collateral loans involve complex processes. Leveraging DeFi or even Web2.0-based crypto-collateralized lending can greatly enhance personal asset liquidity while generating new asset classes and revenue streams for banks.

Asset tokenization can bring transformative changes to banking services. For example, tokenizing time deposits would allow holders to make partial payments with precise interest accrual, enabling divisibility, transferability, and infinite extensibility of assets.

In customer KYC, adopting the concept of “Soulbound Tokens (SBTs)” could enable unified identity authentication across a bank and its partner ecosystem based on completed KYC results.

Even the most traditional safe deposit box service evolves with virtual assets—banks could offer private key custody services to clients.

All of this leads to profound, real-world transformations driven by the concept of virtual assets.

Risks and Choices

The banking industry’s sluggish response to virtual assets stems partly from its traditionally conservative, heavily regulated nature. However, the following risk factors also contribute to hesitation.

1. Compliance Risk

Virtual assets carry higher anonymity than traditional assets. Even basic remittance services make it difficult to trace fund origins. Under increasing anti-money laundering (AML) pressure, banks naturally hesitate due to additional compliance costs and potential AML risks.

Beyond urging banks to open accounts, the HKMA should proactively collaborate with the industry to establish AML standards for virtual assets, co-developing direct, clear, and enforceable AML guidelines to facilitate bank participation.

2. Technology Risk

Virtual assets operate very differently, posing new challenges in fraud prevention, key management, and asset custody. Given that most bank staff still lack understanding of crypto assets, managing technology risks remains a major hurdle, contributing to banks’ reluctance to enter the space.

To launch such services, banks need to build internal expertise and rely on external support ecosystems—such as specialized tech firms and structured custody providers.

3. Strategic Risk

Mainland China’s strict ban on virtual assets is a critical consideration for Hong Kong banks. Most Hong Kong banks have operations or branches on the mainland, especially Chinese-owned banks. Therefore, Hong Kong banks must consider not only local policy but also mainland regulatory risks.

The Hong Kong government should communicate with central authorities and clearly inform the industry that Hong Kong banks operating virtual asset businesses in compliance with local regulations do not violate mainland policies—thereby alleviating concerns.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News