Arthur Hayes: Even if I'm wrong about the Fed, I still believe cryptocurrencies will surge significantly

TechFlow Selected TechFlow Selected

Arthur Hayes: Even if I'm wrong about the Fed, I still believe cryptocurrencies will surge significantly

Even if the Federal Reserve has to continue raising interest rates, Bitcoin can still survive.

Compiled by GaryMa, WuShuo Blockchain

Note: This article is a translated version of the original. Some content has been edited or summarized during translation. Due to length constraints or other reasons, certain details or information may not have been fully retained or were omitted. We recommend readers refer to the original text alongside this translation for a more comprehensive understanding.

Market participants in the U.S. are rarely patient on their journey toward accumulating greater wealth. In our endless search for the next bull market, we often ask ourselves: "Are we there yet?" In the cryptocurrency markets, we frequently wonder when the junk coins in our wallets will once again approach their November 2021 highs.

More sophisticated traders are searching for leading indicators that might signal an approaching bull market, aiming to determine precisely when to go all-in on crypto assets. Like Pavlov’s dog, we’ve been conditioned by our central bank masters to buy financial assets whenever they cut rates or print money to expand their balance sheets. We hang on every word from these charlatans, hoping they’ll deliver free money to fuel returns in risk assets.

Fed Balance Sheet (white) and Bitcoin (yellow), indexed to 100

During the Fed's massive pandemic-era money printing spree, Bitcoin outperformed the growth of the Fed’s balance sheet by 129%, confirming that our reflexive investing based on declarations from the false prophet Chair Powell has been quite profitable.

Since the Federal Reserve began hiking interest rates in March 2022, a group of macroeconomic analysts have tried to predict when the Fed would stop. I’ve presented to readers a series of arguments suggesting that the Fed’s rate-hiking cycle will eventually trigger some financial disaster requiring them to cut rates and restart balance sheet expansion.

On March 10 this year, Silicon Valley Bank and Signature Bank ran into severe balance sheet problems under the Fed’s policy regime. By Sunday night that week, it was clear these banks were doomed unless the Fed and the U.S. Treasury truly wanted to uphold free-market capitalist values and allow a poorly managed traditional finance firm to fail—otherwise, some form of bailout was inevitable. As expected, the Fed and Treasury intervened, providing relief through the Bank Term Funding Program (BTFP). BTFP injected unlimited liquidity into the U.S. banking system, allowing banks to hand over their underwater U.S. Treasuries to the Fed in exchange for fresh dollars. These dollars were then provided to depositors fleeing to money market funds (MMFs), which offered interest rates above 5%, while bank deposits yielded nearly 0%.

This was a pivotal moment. I, along with many others, believed the Fed had certainly stopped hiking rates. The Fed’s true top priority was protecting banks and other financial institutions from collapse, as underwater bonds rotting across the financial sector threatened the entire system. It seemed the Fed’s only option was to cut rates, restore health to the U.S. banking system, and watch Bitcoin rapidly surge toward $70,000.

But that didn’t happen. Instead, the Fed hiked rates three more times from March to now.

When your predictions keep failing, it’s time to re-examine your assumptions and consider “what if I’m still wrong” scenarios. In this case, that means starting to think about whether my portfolio can survive if the Fed continues raising rates.

Last week, I delivered a keynote at Korea Blockchain Week, exploring the question of whether Bitcoin could still rise if the Fed and other major central banks continue tightening. For those who weren’t present—or thought I moved too quickly through certain concepts—here’s a short essay elaborating on that idea.

What If?

What if the U.S. doesn’t enter a recession?

What if inflation doesn’t come down?

What if the U.S. financial system doesn’t collapse?

If all these hold true, then we should expect the Fed and other major central banks not to cut rates—but rather to hike further.

Past and Present Real Yields

What are real yields? Real yield is a fairly fuzzy concept, defined differently by different people. My (slightly simplified) definition is this: if I lend money to the government, I should receive at least a return matching nominal GDP growth. If I earn less than that, the government profits at my expense.

Clearly, governments want to borrow at rates below the economic value generated by their debt. Financial repression—ensuring nominal GDP growth exceeds bond yields—has been the policy of every successful post-WWII export-led Asian economy. Japan, South Korea, and others used this strategy to rebuild after wartime devastation. Governments rely on their banking systems to enforce this repression: banks are directed to offer low rates to depositors, face restrictions preventing capital flight, and are instructed to lend at low rates to state-backed or politically connected heavy industrial firms.

Deposit rate < corporate loan rate < nominal GDP growth

The result? Capital-intensive industrial companies gain cheap financing to rapidly build modern manufacturing bases. Governments use these factories to accumulate sovereign wealth, reinvesting it into U.S. Treasuries and other dollar-denominated financial assets—supposedly to be drawn upon during crises. Ordinary citizens get well-paid blue-collar manufacturing jobs with lifetime security. Compared to their previous lives as subsistence farmers, working eight-hour days at large corporations with full benefits represented a massive improvement.

Real yield = government bond yield – nominal GDP growth

This financial repression strategy only works when capital cannot exit the banking system. That’s why countries like South Korea maintain closed capital accounts. Or, in Japan’s case, foreign financial firms are effectively barred from marketing to or accepting deposits from Japanese savers, leaving ordinary investors trapped in domestic banks earning negative real returns. But in today’s digital age, this strategy is harder to enforce—especially with the rise of alternative decentralized financial systems like Bitcoin. When real yields stay negative for long, depositors can now leave before the door closes (or at least believe they can).

Let’s examine U.S. real yields from 2022 to the present.

U.S. 2-Year Treasury Yield Minus U.S. Nominal GDP Growth

I use the 2-year U.S. Treasury yield as a proxy for government bond rates because it’s the most popular and liquid instrument tracking short-term rates. As you can see, when the Fed started hiking in March 2022, real yields were indeed negative. Despite the unprecedented pace of rate hikes, real yields are now barely positive. If you substitute the 10-year or 30-year yield for the 2-year, real yields remain negative. This is why buying long-term bonds with your own money is foolish. Institutions still do it because fiduciaries managing other people’s money earn generous fees regardless of performance—financial responsibility disappears.

Looking at this chart, my next question is: “What kind of real yields can we expect going forward?” The Atlanta Fed publishes a “GDPNow” forecast—an instant estimate of current-quarter real GDP growth. As of September 8, the Fed projected third-quarter growth at an incredible 5.7%. To derive nominal growth, I added 3.7%—the average difference between nominal and real growth over the past six quarters.

GDPNow real growth 5.7% + GDP deflator growth 3.7% = Q3 nominal GDP growth of 9.4%

Projected Q3 real yield = 2-year U.S. Treasury yield 5% – Q3 nominal GDP growth 9.4% = -4.4% real yield

What’s going on here! Conventional economics says that when the Fed hikes rates, growth slows in credit-sensitive economies. Common sense suggests nominal GDP growth should fall and real yields should rise. But that’s not what’s happening.

Let’s explore why.

No Money, No Honey

Governments raise money through taxes and spend it on various things. If spending exceeds tax revenue, they issue debt to fund the deficit.

America’s main export is finance. Thus, the government earns substantial capital gains tax revenue from stock and bond markets.

The 2020–2021 pandemic bull market generated huge tax receipts from the wealthy. However, starting in early 2022, the Fed began hiking rates. Higher rates swiftly hit financial asset markets. This was the primary reason figures like Sam Bankman-Fried—a decent con artist—and crypto entrepreneurs like Su Zhu and Kyle Davies fell.

Below is a chart showing returns since 2022 (indexed to 100) for the S&P 500 (yellow), Nasdaq 100 (white), Russell 2000 (green), and Bloomberg U.S. Aggregate Total Return Bond Index (magenta).

As you can see, nobody has made money since early 2022. Consequently, capital gains tax revenue has plummeted. The Congressional Budget Office estimates that in 2021, realized capital gains amounted to about 9% of GDP. As the Fed moved to fight inflation, these tax receipts rapidly declined.

“IRS data processing shows realized gains surged in 2021, reaching 8.7% of GDP according to CBO estimates—the highest level in over 40 years.”

Also remember: every politician’s top priority is re-election. The older “baby boomer” generation keeps promising relatively free healthcare, and the average American public enjoys consuming energy at per-capita levels far exceeding the rest of the world. Given these two facts, it’s safe to assume politicians proposing cuts to healthcare or defense spending won’t get re-elected. Instead, with aging populations and a more multipolar world, governments will keep increasing spending in both areas. If spending rises while revenue falls, deficits must grow. And since GDP merely measures economic activity, government spending increases GDP by definition—regardless of whether the spending is actually productive.

U.S. Government Deficit as Percentage of Nominal GDP

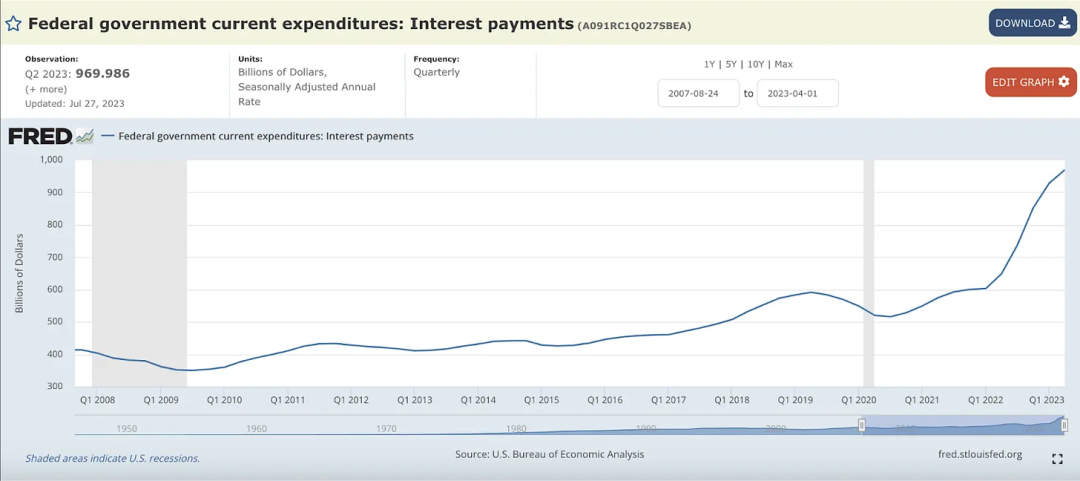

Rising deficits must be financed by selling more bonds. By year-end, the U.S. Treasury must sell an additional $1.85 trillion in bonds to repay old debt and cover budget deficits. Moreover, beyond issuing these bonds, the Fed is also hiking rates, further increasing the interest burden on the U.S. Treasury.

As of the end of Q2, the U.S. Treasury spent $1 trillion annually servicing debt holders. Since most wealth is concentrated among the top 10% of households (who also hold most government debt), the U.S. Treasury is effectively distributing welfare to the rich via interest payments.

When the wealthy have already accumulated enough money to cover life’s essentials (housing and food), what do they buy? They spend on services. About 77% of the U.S. economy is service-related. In summary: when rates rise, the government pays richer people more interest, those individuals spend more on services from their interest income, and GDP grows further.

The Circle Jerk

Let’s tie it all together step-by-step to see how Fed rate hikes increase nominal GDP, thus necessitating even more monetary tightening.

The Fed must hike rates to fight inflation.

I’ll never tire of this photo. Powell looks like a fool, while Biden points a pen at him, instructing the Fed to tackle inflation.

Financial asset prices fall, so tax revenues fall.

Except for standout tech stocks like Nvidia, most companies producing physical goods struggle due to higher credit costs and tighter credit supply, dragging down their share prices. Globally, the largest asset market—bonds—is poised to lose money for a second consecutive year on a total-return basis. With broader equity and bond markets still below 2021 highs, government capital gains tax revenue plummets.

While tax revenue falls, government spending increases, widening deficits. More spending = bigger deficits. If more spending also = higher nominal GDP growth, then logically, bigger deficits = higher nominal GDP growth.

Due to high rates, the U.S. Treasury must issue more bonds at higher yields.

Wealthy savers haven’t seen this much interest income in over two decades.

The wealthy spend more on services using their interest income, further boosting nominal GDP growth.

About 77% of U.S. GDP consists of services.

Inflation becomes stubborn because nominal GDP growth > government bond yields.

Higher bond yields don’t suppress U.S. government spending because the government profits net from this situation. When the government funds itself at rates below the growth generated by its debt, the debt-to-GDP ratio actually declines. This is exactly the same policy the U.S. government used after WWII to pay down massive domestic war debts.

The Fed must hike rates to fight inflation.

As GDP growth continues to outpace bond yields, inflation will rise from its current “low” levels and stay elevated. As long as inflation remains far above the Fed’s 2% target, they must keep hiking.

The Fatal Flaw

Mr. Powell can keep hiking as long as markets accept Treasury yields below nominal GDP growth. But Mr. Satoshi Nakamoto gave the world an alternative financial system—including a fixed-supply currency and a decentralized, near-instant payment network called Bitcoin. Banks now face unprecedented competition. (Of course, you could previously withdraw cash to buy gold, but using heavy gold in daily life isn’t practical.)

If the market demands 9.4% yield on U.S. Treasuries (equal to projected nominal GDP growth), the situation flips. Then the Fed must either ban banks from transferring funds to digital fintech firms offering physical crypto, or restart QE (aka money printing) to buy bonds and cap yields below nominal GDP growth. I’ll keep reminding you: buying ETFs does not remove your money from traditional finance. The only escape is buying Bitcoin and withdrawing it to your own wallet where you control the private keys.

It’s reasonable to assume that with a financial escape hatch like Bitcoin, markets will grow tired of handing profits to the government. But for the remainder of this analysis, I’ll assume the Fed can continue hiking without significant capital fleeing the U.S. banking system.

Changing Financial Climate

We’re taught to believe that when interest rates rise, prices of risky financial assets like Bitcoin, stocks, and gold should fall. But because the government continues its spending spree and inflates GDP, the seemingly attractive ~5% yield on government bonds may actually represent a real yield closer to -4%—meaning risk assets remain highly attractive to investors.

Investor demand for positive real yield sparked the Bitcoin bull market, which officially began on that fateful weekend of March 10, 2022. Since then, Bitcoin has risen nearly 29%. Though price has repeatedly tested $30,000 without breaking through, Bitcoin still trades above its pre-bailout level of $20,000.

Markets are quietly telling us that if the Fed continues hiking, real yields will turn even more negative and stay that way for the foreseeable future. If not, shouldn’t Bitcoin be hovering around $16,000? The reason we haven’t hit $70,000 is that everyone focuses on the nominal federal funds rate, not real rates relative to America’s shockingly high nominal GDP growth. But this message is slowly leaking through mainstream media propaganda outlets like The Washington Post:

Furman said: “Seeing this in an economy with low unemployment is really shocking. This has never happened before—a strong, healthy economy, no new emergency spending—but deficits this large. They’re so big within a year that you think something strange must be going on.”

As it becomes clearer that holding bonds is a fool’s game—even with short-term nominal rates at 5.5%—marginal capital will begin seeking hard-core financial assets. Certain assets—like Bitcoin, large-cap tech/AI stocks, and productive farmland—will keep rising, baffling most financial analysts (who are actually just average-intelligence, average-ability fiduciaries earning fat management fees from other people’s money). They don’t understand why Bitcoin holds up because they look at manipulated markets controlled by Fed asset purchases, such as TIPS yields—which (seemingly) are positive and rising.

Setting aside the flawed analyses we’ll surely read in mainstream financial media, I believe I’ve demonstrated that Bitcoin can survive even if the Fed must continue hiking. This comforts me because although I still view the base case as the Fed being forced to cut rates to near zero and restart the QE money printer, even if I’m wrong, I still believe cryptocurrencies can rise substantially.

The reason Bitcoin has such positively convex exposure to Fed policy is that with debt-to-GDP so high, traditional economic relationships have broken down. It’s like heating water to 100°C—it stays liquid until suddenly boiling into gas. Under extreme conditions, things become nonlinear—sometimes binary.

The U.S. and global economies are in such an extreme state. Central banks and governments are trying to apply yesterday’s economic theories to today’s new realities, while a 360% global debt-to-GDP ratio creates inverted conditions demanding a rethink of asset correlations.

Indeed, teaching an old dog new tricks is possible—but only if the dog wants to learn. The scoundrels ruling in our name have no such desire. Therefore, Master Satoshi will punish them with mighty Bitcoin.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News