Analyzing the Leader in Restaking: EigenLayer's Business Logic and Valuation Analysis

TechFlow Selected TechFlow Selected

Analyzing the Leader in Restaking: EigenLayer's Business Logic and Valuation Analysis

This article will outline the business logic of EigenLayer and provide a preliminary valuation estimate for the EigenLayer project.

Author: Alex Xu

Introduction

With the completion of Ethereum's Shanghai upgrade, many LSD projects have experienced rapid business growth, and both user numbers and net asset values of LSD assets have significantly increased. On the other hand, with the upcoming Dencun upgrade by year-end and the opening of OP Stack, this year marks a pivotal moment for Rollups. Services围绕Rollup modules—such as DA layers, shared sequencers, and RaaS—are also flourishing. Meanwhile, EigenLayer, which introduced the concept of Restaking based on LSD assets to provide security services for numerous Rollups and middleware protocols, has seen steadily rising attention. In March, it raised $50 million at a $500 million valuation, and its token reportedly trades OTC at an astonishing $2 billion, rivaling valuations of major Layer 1 blockchains.

In this article, I will analyze EigenLayer’s business logic and attempt to estimate its valuation, addressing the following questions:

-

What is Restaking service, who are its customers, and what problems does it solve?

-

What are the obstacles to widespread adoption of the Restaking model?

-

Is EigenLayer’s $500 million—or even $2 billion—valuation justified?

The views expressed below represent my current perspective as of publication and focus more on commercial analysis than technical details. There may be factual inaccuracies or biases in this article; it is intended solely for discussion and open to feedback from fellow researchers and investors.

EigenLayer’s Business Logic

Before diving into EigenLayer’s business model, let’s define several frequently used terms in the following sections:

Middleware: Refers to infrastructure services between blockchain base layers and dApps. In Web3, typical examples include oracles, cross-chain bridges, indexers, DID solutions, and DA layers.

LSD: Liquid Staking Derivatives—tokens representing staked ETH that maintain liquidity, such as Lido’s stETH.

AVS: Actively Validated Services—decentralized node systems that provide security and validation for protocols. The most common example is a PoS chain’s validator network.

DA: Short for Data Availability. It refers to storing transaction data from other chains (e.g., Rollups) on a dedicated layer so that historical records can be retrieved and reconstructed when needed.

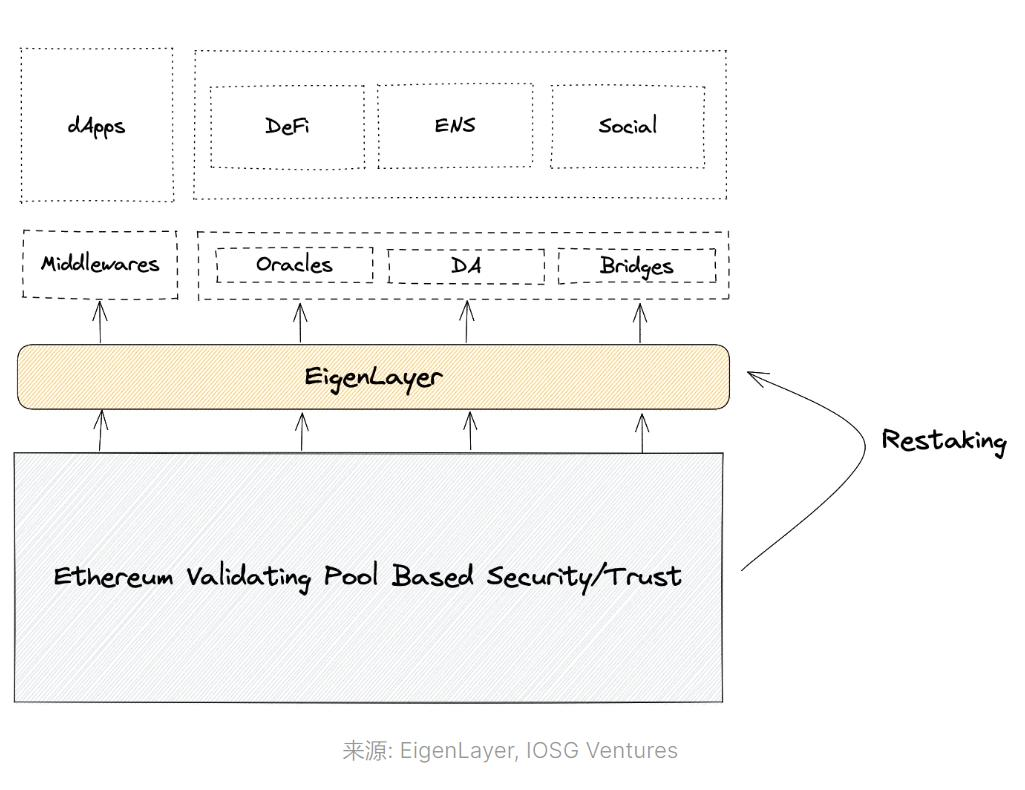

Business Scope

EigenLayer operates a marketplace for renting cryptoeconomic security.

Cryptoeconomic security means that Web3 projects ensure reliability, permissionlessness, and decentralization by requiring key participants (validators) to stake tokens. If validators fail their duties, their staked tokens are slashed.

As a platform, EigenLayer raises capital from holders of LSD assets and uses these LSDs as collateral to offer convenient and low-cost AVS services to middleware protocols, sidechains, and Rollups that require AVS. EigenLayer acts as a matchmaker between LSD providers and AVS consumers, while specialized staking service providers handle the actual security operations.

Additionally, EigenLayer’s parent company is developing a DA layer called "EigenDA," providing data availability services to Rollups and appchains. This creates strong synergies between EigenDA and EigenLayer.

EigenLayer aims to address three core pain points:

1.For project teams: Reduce the high cost of building independent trust networks by paying to use existing staked assets and node operators on EigenLayer instead of building their own.

Source: EigenLayer Whitepaper

2.For Ethereum: Expand use cases for Ethereum LSDs, enabling ETH to serve as security collateral for more projects, thereby increasing demand for ETH.

3.For LSD holders: Further improve capital efficiency and yield on LSD assets beyond basic PoS rewards.

User Base

EigenLayer serves three parties with distinct needs:

1.LSD Providers: Users seeking additional returns on top of standard PoS yields from their LSD holdings, willing to accept slashing risks by staking them through EigenLayer.

2.Node Operators: Entities that obtain LSD assets via EigenLayer to run nodes for AVS-consuming projects and earn revenue from fees and rewards paid by those projects.

3.AVS Consumers: Projects (e.g., Rollups or bridges) that need secure validation but want to avoid the cost and complexity of building their own AVS. They can outsource this function via EigenLayer.

EigenDA’s primary users are Rollups and appchains.

Operational Details

Users can re-stake their Ethereum-locked tokens—including stETH, rETH, and cbETH—into the EigenLayer market. Staking service providers then match these tokens with corresponding AVS demands, offering security services backed by these deposited assets. In return, projects pay users a “security fee.”

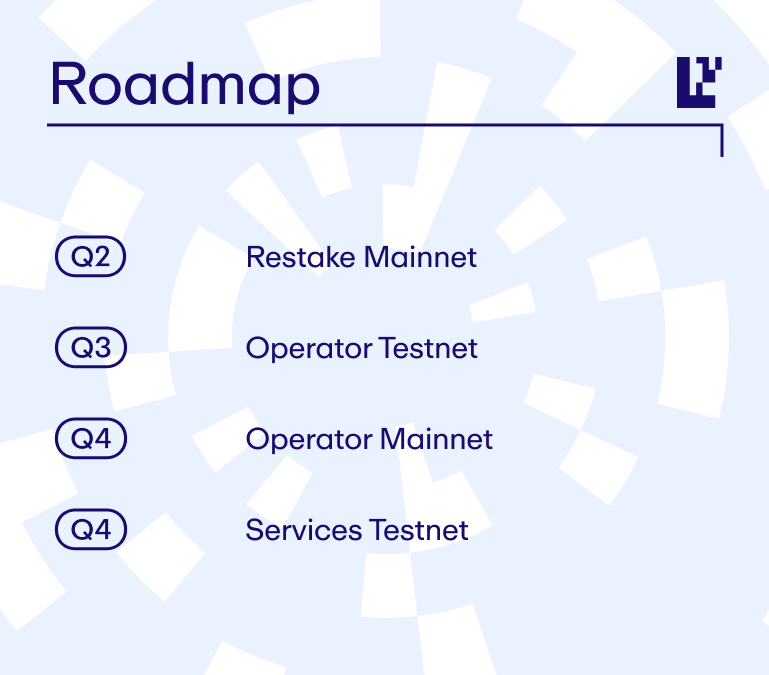

Product Progress

Currently, EigenLayer only supports restaking of LSD assets and has not yet launched node operator staking or full AVS services. It ran two deposit campaigns, both of which quickly reached capacity—mainly driven by users hoping to qualify for potential future token airdrops. Users can also directly deposit whole multiples of 32 ETH to participate in restaking. Despite capped deposits, EigenLayer has already accumulated around 150,000 staked ETH.

According to EigenLayer’s official roadmap, Q3 focuses on launching the Operator testnet, followed by development of the AVS testnet in Q4.

Mantle, a Rollup built using a fork of the OP Virtual Machine, is the first confirmed user of EigenDA and currently uses the test version for its DA needs.

Tokenomics

EigenLayer is a tokenized project, though specific details about its token and economic model have not yet been disclosed.

Team and Funding Background

Core Team

Founder & CEO: Sreeram Kannan

Associate Professor of Computer Engineering at the University of Washington and founder and controlling person of Layr Labs, EigenLayer’s parent company. He has published over 20 blockchain-related research papers. He completed his undergraduate studies in telecommunications at the Indian Institute of Science, earned a master’s in mathematics and a PhD in information theory and wireless communications from the University of Illinois Urbana-Champaign, and was a postdoctoral researcher at UC Berkeley. He now leads the UW Blockchain Lab.

Founder & Chief Strategy Officer: Calvin Liu

Graduated from Cornell University with a degree in Philosophy and Economics. After years in data analytics, corporate consulting, and strategy roles, he served nearly four years as Head of Strategy at Compound before joining EigenLayer in 2022.

COO: Chris Dury

Holds an MBA from NYU Stern School of Business. Experienced in cloud product management. Prior to joining EigenLayer in early 2022, he was Senior VP of Product at Domino Data Lab (a machine learning platform), and previously held leadership roles at Amazon AWS, managing cloud services for game developers.

EigenLayer’s team is rapidly growing, with over 30 employees, mostly based in Seattle, USA.

Layr Labs, founded by Sreeram Kannan in 2021, is the parent company behind EigenLayer. Besides EigenLayer, it also develops EigenDA and Babylon—a similar cryptoeconomic security project focused on the Cosmos ecosystem.

Funding History

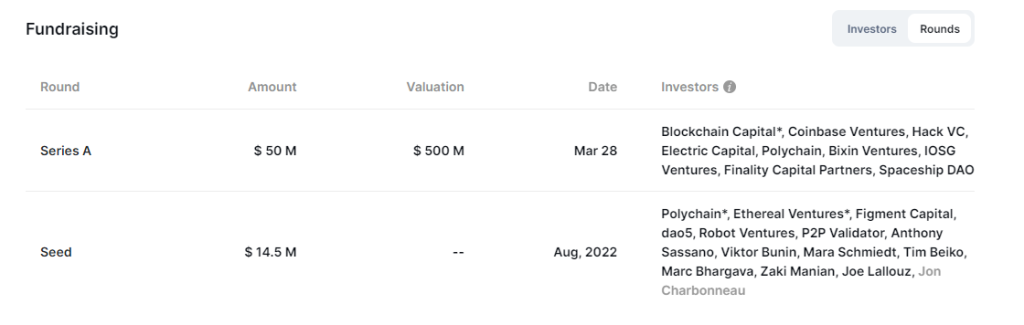

EigenLayer has completed two public funding rounds: a seed round of $14.5 million in 2022 (valuation undisclosed) and a Series A round of $50 million in March 2023 at a $500 million valuation.

Notable investors include:

In 2023, its parent company Layr Labs also raised approximately $64.48 million in equity financing—details available in its SEC filing.

Market Size, Growth Narrative, and Challenges of Restaking

Market Size Estimation

EigenLayer introduces the novel concept of restaking, offering “cryptoeconomic security as a service.” Its target customers include middleware (oracles, bridges, DA layers) and sidechains/appchains/Rollups, aiming to reduce the cost of decentralized network security compared to building standalone trust networks.

In theory, any protocol that relies on token staking and game-theoretic mechanisms to maintain consensus and decentralization could be a potential user. The exact size of this market is hard to quantify, but optimistically, it could reach tens of billions of dollars within three years.

Ethereum currently has around $42 billion in staked ETH, with a total market cap of ~$200 billion (as of August 30, 2023), and total on-chain value estimated between $300–400 billion. Given that EigenLayer’s main clients will likely be smaller, newer projects, its total staking volume should remain between $10–100 billion in the near term—far below Ethereum’s ~$40 billion PoS staking scale.

Growth Drivers and Market Narratives

Demand Side:

-

The upcoming Dencun upgrade and the open-sourcing of OP Stack are accelerating the growth of small-to-mid-sized Rollups and appchains, increasing overall demand for affordable AVS solutions.

-

The modularization trend in blockchains increases demand for cheaper DA solutions beyond Ethereum. EigenDA’s expansion complements EigenLayer’s offerings, creating business synergy.

Supply Side:

Rising Ethereum staking rates and growing numbers of stakers provide abundant LSD assets and holders eager to boost capital efficiency and yields. In the future, EigenLayer may expand to support LSDs beyond ETH.

Challenges and Risks

-

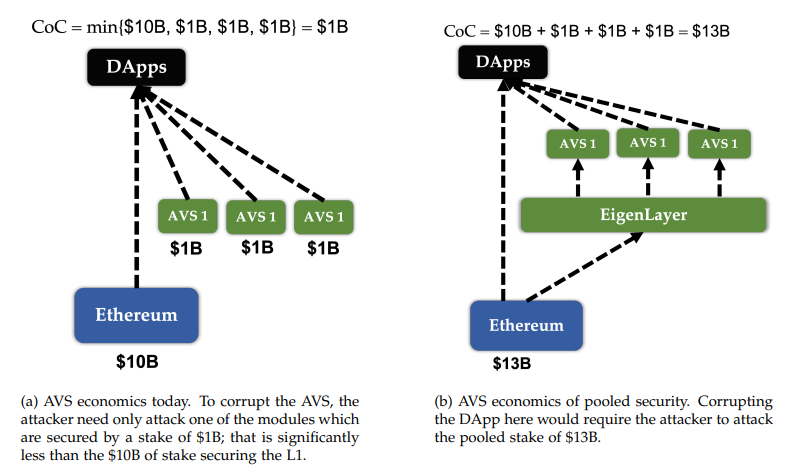

For AVS consumers, how much cost savings do they actually achieve by sourcing staked assets and professional validators via EigenLayer? It’s unclear. Using Ethereum LSDs doesn’t automatically inherit Ethereum’s massive security budget. A project’s actual security depends on the total value of borrowed LSDs plus the quality of node operators. While faster and easier than building AVS from scratch, cost savings may be limited.

-

Using external assets as AVS collateral weakens the utility of a project’s native token. Although EigenLayer supports hybrid models (native token + EigenLayer), this still poses significant adoption friction.

-

Projects relying on EigenLayer for AVS may fear long-term dependency and vendor lock-in. Once mature, they may switch back to using their own tokens for security.

-

Using LSDs as collateral introduces additional counterparty risk tied to the LSD provider’s credibility and security.

Competitors

Restaking is a new concept pioneered by EigenLayer, with few direct followers so far. However, for potential customers, the real choice remains whether to build their own security network or outsource it to EigenLayer. For now, EigenLayer needs more real-world case studies to prove its advantages and convenience.

Valuation Analysis

As a novel business, EigenLayer lacks clear comparables. We estimate its valuation by projecting annual protocol revenue and applying a PS (price-to-sales) multiple.

Before estimating, we make the following assumptions:

-

EigenLayer earns a commission from security fees paid by AVS users—90% goes to LSD depositors, 5% to node operators, and 5% to EigenLayer (matching Lido’s fee structure).

-

AVS users pay an average annual security fee of 10% on the value of borrowed LSD capital.

We use 10% because mainstream PoS projects typically offer 3–8% staking rewards. Since early EigenLayer adopters are likely newer projects offering higher incentives, 10% seems reasonable as an average security fee rate.

PoS reward rates across major L1s

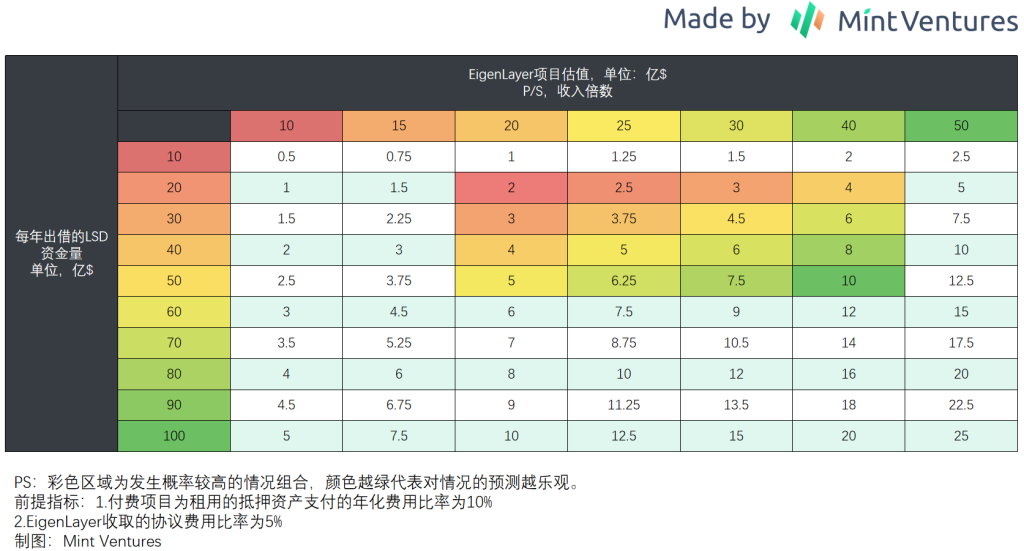

Based on these assumptions, I derive the following valuation ranges according to EigenLayer’s lent LSD volume and applicable PS multiples. The colored regions indicate higher-probability estimates, with greener shades reflecting more optimistic scenarios.

I consider the range of “$2–5 billion in annual LSD lending” and “PS multiples of 20–40x” as most probable because:

-

The combined market cap of PoS-staked tokens among the top 10 L1s is ~$73 billion (~$82 billion including Aptos and Sui). However, since most stakes on these two come from unvested team and institutional tokens, I exclude them as outliers. Assuming EigenLayer captures 2.5%–6.5% of the total PoS staking market (a rough estimate), that translates to $2–5 billion in value. Whether this share is realistic is up to interpretation.

-

A PS multiple of 20–40x is anchored to Lido’s current 25x PS (as of August 30, 2023, based on fully diluted market cap), with newer narratives potentially commanding premium valuations.

Based on this analysis, a $2–10 billion valuation range appears reasonable for EigenLayer. Early investors who participated at a $500 million valuation may not have left much margin of safety, especially considering token unlock constraints. Any investor considering an OTC purchase at a rumored $2 billion valuation should proceed with extreme caution.

It must be noted that the above valuation applies to the entire EigenLayer project. The actual token market cap will depend on how effectively the token captures value within the ecosystem—for example:

-

What percentage of protocol revenue flows to token holders?

-

Beyond buybacks or dividends, does the token have essential utility that drives demand?

-

Will EigenDA share the same token as EigenLayer, expanding its use cases and demand?

If points 1 and 2 lack strong value accrual, the intrinsic worth of the EigenLayer token will be weakened. Conversely, positive surprises in point 3 could enhance its value.

Moreover, EigenLayer’s eventual market cap will also depend on broader macro market conditions—bullish or bearish—at launch.

Let’s wait and see what the market decides.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News