MakerDAO from a Monetary Perspective: Understanding the Significance Behind MakerDAO's Introduction of U.S. Treasury Assets

TechFlow Selected TechFlow Selected

MakerDAO from a Monetary Perspective: Understanding the Significance Behind MakerDAO's Introduction of U.S. Treasury Assets

This article will start from the perspective of money and guide you through exploring and understanding the significance behind MakerDAO's introduction of U.S. treasury assets.

Authors: DrSamo (Twitter: @BirkSamo), Bocai Bocai! (Twitter: @wzxznl)

As the leader in the DeFi (decentralized finance) space, MakerDAO has long been fascinated by U.S. Treasury bonds. Since formally incorporating RWA (real-world assets) into its strategic direction in 2020, MakerDAO has purchased nearly $1.2 billion worth of U.S. Treasuries. Why would a decentralized DeFi protocol integrate real-world assets? What is the rationale behind this move? And is creating DAI (the stablecoin issued by MakerDAO) after acquiring U.S. Treasuries equivalent to how the Federal Reserve creates money?

To answer these questions, we need to start with the nature of money.

This article will explore the significance behind MakerDAO’s integration of U.S. Treasury assets by starting from the concept of money—examining its essence and drawing parallels between the central bank-commercial bank dual structure and MakerDAO’s balance sheet architecture.

What is money? What is the essence of money?

There's a widely circulated saying: "The essence of money is credit." However, many people may know this without fully understanding why. On the question of what money really is, I'd like to quote Professor Zhai Dongsheng from his book *Money, Power, and People*: "Money is a social cooperation system and public good composed of three fundamental elements."

A legally backed abstract unit of value:

As an abstract unit of value, money derives its worth not from its physical form—for instance, the production cost of a banknote is far lower than its face value—but from the trust people place in it. This trust is largely established and safeguarded by national laws.

Firstly, national law establishes the legal tender status of money. In most countries, the state currency is defined as the sole legitimate means of payment. This means that if you use official fiat currency to buy goods or services, the seller must accept it.

Secondly, national law protects the credibility of money. Most countries entrust their central banks or similar institutions with maintaining monetary stability—controlling inflation and preventing severe economic crises. These efforts help preserve confidence in the currency and assure holders that keeping money is safe.

Lastly, national law grants money a unique status: only authorized government bodies can issue it. Unauthorized production or counterfeiting of money is illegal.

Therefore, when we say money is an abstract unit of value supported by national law, we are emphasizing its legal standing and how that status helps maintain its value and credibility.

A ledger system for tracking and recording credit/debt balances among members of society during transactions:

In ancient trade systems without money, how did people conduct exchanges? They might have used barter—for example, giving a chicken in exchange for a bag of rice.

However, such systems had obvious drawbacks. First, both parties needed to have mutual desires—a problem known as the **"double coincidence of wants,"** which was often difficult to achieve. Second, determining the exchange rate—how many bags of rice equal one chicken—was complicated.

To solve these issues, humans invented money. **Money can be seen as a ledger system that tracks and records credits or debts.** For example, if you provide me a service today, I may not immediately return the favor. Instead, I could give you a token of debt—money—that certifies my obligation. At a later time, you could redeem this token from me—or anyone else who accepts it—for an equivalent service.

Overall, money functions as a ledger system for tracking credit and debt balances among transacting individuals. It simplifies trade, makes value measurement easier, and enables smoother transfer of value.

A standardized representation (token) allowing creditors to transfer specific debt obligations to third parties:

To understand how money serves as a standardized representation through which creditors can transfer debt obligations, consider a simple analogy.

Imagine a small island where everyone engages in farming, fishing, or other productive activities. If you help me farm today, I might owe you a debt—say, promising to fish for you someday. But managing such informal debts is challenging—we’d have to remember who owes what and when repayment is due.

To address this, we introduce a standardized symbol or token to represent these debts—this is money. For instance, I give you a seashell representing my debt. You can later use this shell to claim fishing services from me, or pass it to someone else who can claim the service instead. Thus, the shell becomes a standardized representation enabling transfer of debt claims.

In modern society, our money works similarly. Holding a $100 bill means possessing a claim (a liability for the issuing central bank) entitling you to goods or services of equivalent value. You can also transfer this claim to others by handing over the bill.

In short, money is a standardized representation of debt that allows efficient management and transfer of credit relationships. When we say “the essence of money is credit,” we mean money itself is a transferrable debt or transferrable credit. Its value does not come from material substance but from social consensus and trust in the issuing institution (like a central bank). Once we examine the process of money creation more closely, this idea becomes even clearer.

How is money created?

Types of Money – Base Money and Credit Money

Money generally falls into two categories: base money and credit money:

Base money, also called high-powered money or central bank money, is directly issued by the central bank and possesses final settlement power. It includes coins and paper currency in circulation, as well as commercial banks’ reserves held at the central bank. The value of base money stems primarily from legal backing and societal trust. Due to its finality in payments, it forms the foundation of the money supply. While base money underpins the system, in modern economies, most of the actual money supply consists of credit money.

Credit money is mainly created by commercial banks through lending and deposit activities. When a bank issues a loan, it effectively creates new money.

In today’s monetary system, the vast majority of money is credit money—in other words, most money in existence is created not by central banks but by commercial banks. This occurs via the “money multiplier effect,” where banks lend out portions of deposits, thereby generating additional money.

For example, when someone deposits $1,000 into a commercial bank, assuming a reserve requirement of 10%, the bank holds $100 in reserve and lends out $900. When that $900 is eventually deposited in another bank, that bank keeps $90 in reserve and lends out $810. This cycle repeats, each round creating new money.

Under this model, while each bank generates new money through loans, the total amount is limited because each subsequent loan decreases in size. This implies that although commercial banks can create money, their capacity is constrained—not unlimited—by central bank policies, Basel accords, and other regulatory factors.

The Central Bank–Commercial Bank Dual Structure

In the modern monetary system, central banks and commercial banks together form a dual structure designed to balance money issuance and circulation.

The central bank plays a crucial role. It formulates and implements monetary policy, controls the supply of base money, regulates interest rates, and maintains financial stability. Through open market operations—such as buying or selling government bonds—the central bank influences the overall money supply.

When the central bank buys government bonds, it injects base money into the market, increasing liquidity. Conversely, selling bonds absorbs base money, reducing the money supply. Additionally, the central bank sets the reserve requirement ratio—the percentage of deposits commercial banks must hold in reserve—which affects banks’ ability to create credit money.

Commercial banks are the primary source of money creation. They operate by accepting deposits and issuing loans. When a commercial bank gives out a loan, it creates new money because the loan amount appears as a deposit in the borrower’s account, increasing the economy’s money supply. However, this money-creation ability is constrained—by central bank policies and international regulations like the Basel Accords.

This dual structure ensures flexibility and stability in the monetary system. The central bank adjusts monetary policy to control base money, influencing general interest rates and helping manage risks like inflation or deflation.

Meanwhile, commercial banks adjust credit money supply through lending, meeting economic demand for capital. Because their money creation is bounded, excessive expansion leading to inflation or asset bubbles is mitigated.

The Process of Money Creation

To better visualize how money is created, balance sheets serve as excellent tools—they offer a magnified view into financial behavior (the following diagrams are simplified for clarity).

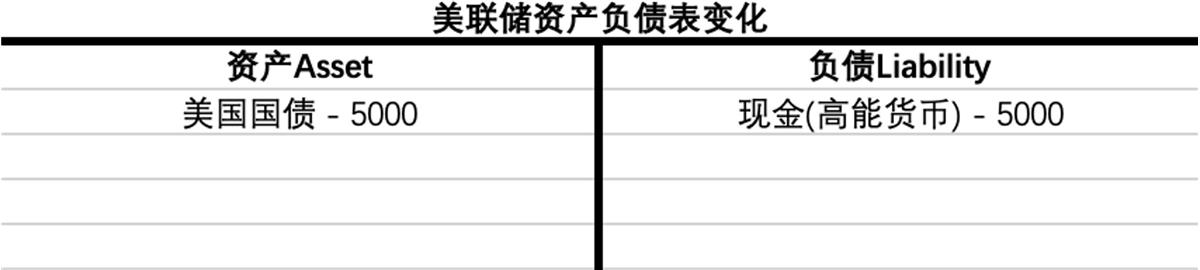

Central bank money creation: Take the Federal Reserve as an example. The Fed typically creates dollars through open market operations—purchasing assets like Treasury bonds from market participants. This process “creates” dollars out of thin air. During the pandemic, the Fed’s massive quantitative easing involved buying various assets and injecting newly created dollars into the economy.

Suppose the Fed purchases $5,000 worth of Treasury bonds from a commercial bank. The change on the balance sheet would look like this:

When the Fed buys $5,000 in Treasuries, its balance sheet shows an increase of $5,000 in bond assets and $5,000 in liabilities (base money). At this point, $5,000 in high-powered money has been “created,” adding $5,000 in liquidity to the market.

From the Fed’s balance sheet, we see how dollars are created—an action that expands the balance sheet and increases dollar liquidity in the market, commonly referred to as “balance sheet expansion.” You’ve probably also heard the term “quantitative tightening” or “balance sheet contraction.” The “sheet” refers to the balance sheet. Recent talk about rate hikes and QT indicates the Fed withdrawing liquidity. Just as buying assets creates money, selling them “destroys” money, shrinking the balance sheet and reducing money supply.

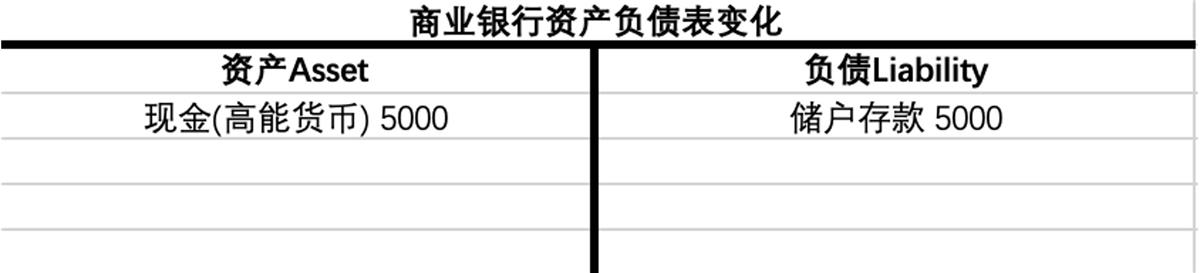

Commercial bank money creation: For commercial banks, money is created through the lending process. Suppose a customer deposits $5,000. To the depositor, this is an asset; to the bank, it’s a liability since the bank must pay interest.

Banks don’t just sit on deposits—they earn profits by lending at higher interest rates than they pay depositors, capturing the spread. Suppose the bank decides to lend $5,000. Notice there’s no physical cash transfer—instead, the bank simply adds a loan (asset) and a deposit (liability) to its balance sheet. New money is thus born (though it still needs to set aside required reserves). In reality, most bank deposits are self-created by banks, and this type of money is called credit money—constituting the bulk of money we use daily.

This process can repeat across multiple banks, each round creating more money. So even though initial base money was only $5,000, through repeated lending, total money supply grows significantly—this is the money multiplier effect. Assuming a 10% reserve ratio, once all $5,000 ends up back in reserve accounts, the total deposits become $5,000 ÷ 10% = $50,000—a tenfold expansion.

However, commercial banks’ money creation isn’t infinite. Their capacity is constrained by central bank reserve requirements and financial regulations. In cases of mass withdrawals (bank runs) or widespread loan defaults, banks may face liquidity issues or even collapse. Therefore, while banks can create money, this power is neither unlimited nor risk-free.

Ultimately, you realize that commercial banks can “create” money out of thin air, yet the amount of physical cash (high-powered money) available for withdrawal is far less than the total credit money created—similar to playing a “ten bottles, nine caps” game. That’s precisely why even the most honest banks cannot survive a full-scale bank run.

Before the modern credit money system matured, nations could freely print money. Today’s fiat system ties new money issuance to sovereign debt—each unit of base money corresponds to an equivalent amount of government bonds, which carry interest obligations. This makes money printing costly in theory, potentially curbing governments’ impulses to overissue currency.

But when the Fed creates money by buying Treasuries, doesn’t this mean the U.S. government can keep printing money endlessly—issuing new debt to repay old ones, with the Fed continuously purchasing them and paying interest?

The modern credit money system actually incorporates a checks-and-balances mechanism: the U.S. Treasury cannot print money but can issue debt; the Federal Reserve can create money but cannot spend it freely. The Treasury must borrow at market rates—excessive debt issuance raises borrowing costs. Moreover, U.S. debt issuance faces a legal debt ceiling.

Set by Congress, the debt ceiling limits total government borrowing. Once reached, the Treasury cannot issue new bonds, forcing budget balancing via spending cuts or tax increases. Failure to resolve the ceiling may lead to technical default on U.S. debt, with serious global consequences.

Understanding how central and commercial banks create money reveals institutional safeguards against unchecked government money printing. Yet loopholes remain—like rolling over debt to avoid true cost accountability. Historically, whenever the U.S. hits the debt ceiling, Congress usually raises it at the last minute.

Ultimately, the entire modern monetary system resembles a game of musical chairs. Government debt requires interest payments. What happens when it can’t pay? Keep printing money to cover interest and keep spending. If you’re a small country like Venezuela, such practices cause local currency depreciation and fail to resolve foreign-denominated debts.

But if your currency is the world’s strongest hard currency, and rolling over debt incurs no external penalty, then “borrowing feels great—and keeps feeling great.” By now, you realize the anchor behind modern money is essentially debt—and debt is a form of credit. This deepens your understanding of the phrase “the essence of money is credit.”

Does MakerDAO have the ability to create money?

Introduction to MakerDAO

MakerDAO is a project built on the Ethereum blockchain that combines over-collateralized stablecoins, lending, savings, and community governance. Its core component is the Maker Protocol—also known as the Multi-Collateral DAI (MCD) system—which allows users to generate the decentralized stablecoin DAI by locking approved collateral assets. For example, a user can lock $10,000 worth of ETH to mint $6,500 in DAI.

In 2022, MakerDAO passed a proposal to use funds from its Peg Stability Module (PSM) to purchase U.S. Treasury bonds [1]. This decision marked a significant milestone for MakerDAO.

Let’s briefly explain PSM (Peg Stability Module), a key part of MakerDAO. Its main function is to help DAI maintain its 1:1 peg with the U.S. dollar. When DAI’s market price deviates from $1, PSM adjusts DAI supply to bring the price back in line.

Specifically, here’s how PSM works: when DAI trades above $1, arbitrageurs can swap USDC (currently the only approved stablecoin voted by MKR holders) 1:1 for DAI via PSM—effectively getting a discount—and sell DAI on the open market for profit. Conversely, when DAI trades below $1, users can swap DAI 1:1 for USDC through PSM, reducing DAI circulation and pushing its price back up. This mechanism leverages market forces to automatically stabilize DAI’s price.

Looking at MakerDAO’s balance sheet in 2022, we see that PSM assets accounted for over half of MakerDAO’s total holdings—all mostly centralized stablecoin USDC. This suggests DAI, to some extent, is merely a wrapper around USDC.

However, after MakerDAO began purchasing U.S. Treasuries, an interesting observation emerged: the structure of MakerDAO’s balance sheet—on both asset and liability sides—began to resemble that of the Federal Reserve (U.S. Treasuries : High-Powered Dollars vs. U.S. Treasuries : DAI Stablecoins):

So here arises the question: Does this mean MakerDAO is sharing the right—previously monopolized by the Federal Reserve—to create money backed by U.S. Treasuries? What exactly does MakerDAO’s purchase of Treasuries signify?

Is MakerDAO creating money?

Let’s state the conclusion upfront: MakerDAO is not creating money. Where’s the error in reasoning?

To clarify, let’s lay out three distinct concepts:

-

Central Banks: Represented by the Federal Reserve, they possess the strongest money-creation capability. Newly issued money takes the form of high-powered money.

In the simplest model, the Fed can create money out of nothing, but in practice, it cannot directly inject newly printed dollars into the economy. The U.S. Treasury can issue debt but cannot print money; the Fed can print money but cannot freely spend it. This separation ensures fiat issuance is anchored to sovereign debt, theoretically curbing reckless money printing. -

Commercial Banks: Possess the ability to expand money supply through credit. The money they create is credit money.

As previously discussed, when a loan is approved, there isn’t necessarily a physical transfer of funds—rather, the bank simply records a new asset (loan) and a new liability (deposit) on its balance sheet. As long as banks maintain adequate “capital adequacy ratios”—typically 8%—they can continue expanding credit. -

Stablecoin Issuers: Have the simplest business model: receive dollars from customers and issue 1:1 stablecoins, ensuring redemption.

Examples include Circle issuing USDC and Tether issuing USDT. They do not possess credit expansion capabilities—they merely hold customer dollars and issue corresponding digital tokens. MakerDAO’s issuance of DAI is quite similar, especially given the PSM module’s 1:1 DAI-USDC swap function. If USDC is viewed as a “dollar voucher,” then DAI within PSM could be considered a “USDC voucher.”

The PSM module can be misleading during periods of high liquidity, consistently offering smooth swaps between DAI and USDC. But fundamentally, it is a “reserve vault.” If everyone simultaneously tries to exchange their DAI for USDC via PSM, the vault would quickly deplete.

The USDC in this vault belongs to MakerDAO. But MakerDAO lacks a lending protocol and therefore has no ability to extend credit. It should not—and must not—re-lend this USDC. These reserves should remain locked, only used when providing 1:1 DAI-USDC conversions, just as Circle cannot freely access customer dollars.

Where did the money for MakerDAO’s U.S. Treasury purchases come from?

You can’t buy U.S. Treasuries directly with DAI. MakerDAO converted USDC from its DAO treasury into U.S. dollars and then used those dollars to purchase Treasuries.

Understanding the modern credit-based monetary system centered on the “central bank–commercial bank” duality reveals that stablecoin issuers operate very differently. Compared to the central bank’s power to create base money or the commercial bank’s 8% capital adequacy rule enabling credit expansion, stablecoin issuers’ money-creation ability is negligible. They are like Nongfu Spring: “We don’t make water—we just move it.”

Even viewed over longer horizons, stablecoin issuers supply money in a fundamentally different way. Under the Bretton Woods system, the U.S. issued dollars backed by gold reserves. Over time, this evolved into a “ten bottles, nine caps” scenario—more dollars printed, fewer gold reserves to back them, until the cap count dwindled.[2]

Of course, if stablecoin issuers only acted as passive custodians, they wouldn’t survive financially. So we accept Circle investing part of its customer deposits into short-term U.S. Treasuries. This involves swapping highly liquid dollar checking deposits for slightly less liquid but higher-yielding Treasuries, using the income to fund operations. MakerDAO is doing something similar—swapping non-interest-bearing USDC reserves for interest-bearing Treasuries to generate revenue and sustain the protocol.

Such actions mean USDC can no longer withstand a 100% redemption event (which was theoretically possible when earning minimal interest). They also weaken DAI’s peg to USDC. Ultimately, this is trading liquidity for yield—less extreme than “ten bottles, nine caps,” but closer to “100 bottles, 99 caps.”

From a balance sheet perspective

Additionally, from a balance sheet standpoint, DAI is a liability for MakerDAO, while USDC in the PSM module is an asset. This transaction is essentially MakerDAO replacing part of its asset portfolio—swapping USDC for U.S. Treasuries. This is a routine asset reallocation for any company or DAO. No new DAI is created, nor is DAI used as high-powered money to amplify the money multiplier through credit expansion.

In summary, MakerDAO does not share the Federal Reserve’s money-creation power. Creating a strong, widely accepted unit of account like the U.S. dollar is extremely difficult. This was BTC’s original vision—to replace fiat as the anchor for all economic activity, freeing people from the exploitation of sovereign money printing. Even BTC still has a long way to go in displacing fiat, and DAI faces an equally long journey in replacing fiat or centralized stablecoins.

What does MakerDAO’s purchase of U.S. Treasuries really mean?

We’ve clarified that during MakerDAO’s addition of Treasuries to its asset side, the liability side (DAI supply) did not increase—it was purely an asset swap.

But from another angle, could we argue that previously, part of DAI was backed by USDC reserves, and now, after the swap, part of DAI is indirectly backed by U.S. Treasury debt—thus benefiting from the creditworthiness of the U.S. sovereign?

This shift in backing is valid—and similar phenomena have occurred repeatedly in the real world.

Fiat currencies partially backed by the U.S. dollar

Historically, smaller economies have frequently anchored their currencies to the U.S. dollar to enhance credibility.

- Post-WWII European Nations

After WWII, European nations were devastated—with little gold reserves and weak government credit, making stable currencies difficult. Unchecked, this could lead to competitive devaluations. The U.S. dollar stepped in as a stabilizing bridge: the U.S. held gold, and other nations held dollars—effectively borrowing the dollar’s credibility to strengthen their own fragile currencies.

The U.S. clearly benefited—through the Marshall Plan, Europe rebuilt productivity, working hard to earn greenbacks while paying interest, effectively paying seigniorage. But the U.S. undeniably provided a stable environment for global recovery, cementing the dollar’s position as the world’s core currency.

Translated into Web3 terms: the U.S. holding gold is like MakerDAO over-collateralizing ETH to mint DAI; other nations holding dollars is like DAI holding USDC.

- China After Reform and Opening-Up

The roles of money differ greatly between planned and market economies. During China’s transition, monetary policy was chaotic. Authorities quickly recognized the dangers of hyperinflation and retracted excess money. Yet economic growth required capital—a scarce resource at the time. How should newly issued RMB be anchored?

Again, by reserving U.S. dollars to bolster RMB credibility. China encouraged foreign investment—foreign capital (mostly USD) entered but couldn’t circulate freely. The State Administration of Foreign Exchange collected the dollars and issued RMB at the prevailing exchange rate to investors, who then used RMB for domestic investment. After joining the WTO, this trend accelerated—meaning much of the newly issued RMB was effectively backed by dollars. Of course, SAFE didn’t just hold idle dollars—it invested heavily in U.S. Treasuries, earning interest and indirectly anchoring the RMB to U.S. government credit.

In Web3 terms, these targeted RMB issuances resemble wrapped USD—RMB issued against dollar reserves borrows the dollar’s credit.

- Countries and regions with currency pegs

The most notable example is Hong Kong. The Linked Exchange Rate System has been in place since October 17, 1983, maintaining a stable HKD/USD rate between 7.75 and 7.85 via a transparent, robust monetary framework fully backed by foreign reserves. The HKD effectively became a dollar voucher—not strictly 1:1, but tightly linked.

Under normal conditions, the Hong Kong Monetary Authority (HKMA) doesn’t intervene—the exchange rate is stabilized by arbitrage activities conducted by three note-issuing banks (Bank of China Hong Kong, HSBC, Standard Chartered). When HKD approaches the band limits, the HKMA uses dollar reserves to buy or sell HKD, forcibly locking the exchange rate.[3]

In Web3 terms: pre-1983 HKD was gold-backed, like DAI minted via over-collateralization; the three banks’ arbitrage mirrors on-chain bots minimizing DAI-stablecoin spreads; the HKMA’s role resembles MakerDAO’s PSM module.

Two forms of monetary backing

From these examples, we can abstract two sources of backing:

-

Backing by hard currencies (mainly USD) or precious metals (mainly gold) constitutes “hard backing.”

-

Backing by the weaker credit of smaller nations constitutes “soft backing.”

Almost all small-nation fiat currencies work by enhancing their credibility through “hard” reserves, then quietly diluting it with “soft” domestic credit to collect seigniorage.

If a nation is irresponsible—like Venezuela—it may hold some foreign hard currency, but after hyperinflating its currency by adding zeros, even that small “hard” portion becomes meaningless. Such inflation fails to resolve foreign debt and only exploits domestic citizens.

But responsible nations can fully benefit from “hard backing,” maintaining relative stability while gradually introducing “soft” domestic credit—expanding sovereign credit incrementally. Like Rome in late antiquity, which slowly debased its silver coinage over a century, collecting seigniorage along the way.

Viewing DAI as a small nation’s currency

For DAI, if we consider USDC and Treasuries as imported “hard backing,” what is its “soft backing”? Clearly, it’s the over-collateralized issuance mechanism. This isn’t truly “soft”—it’s the only issuance method in decentralized stablecoins proven resilient over time. It’s more like “hard + hard”—replacing the typical “soft” inflationary element with transparent, fully reserved, over-collateralized rules.

The challenge with over-collateralized stablecoins is that rapid price swings in underlying assets can trigger mass liquidations, destabilizing DAI’s exchange rate and supply. Also, money supply grows relatively slowly. For DAI, this “hard + hard” approach leverages the inflow of vast amounts of dollar liquidity into the decentralized world to rapidly scale DAI issuance (via 100% reserve expansion in PSM) and improve exchange rate stability.

The ability to grow issuance rapidly through external credit is vital. One reason gold exited international settlements was industrialization-driven productivity explosions—goods and services grew faster than gold’s supply, causing deflation. Deflation, like hyperinflation, harms economies. Beyond maintaining its peg, DAI’s ability to scale issuance alongside crypto market growth is crucial.

The significance of reserve diversification

Having examined these examples, we see that MakerDAO’s so-called “money creation” is actually just rebalancing its balance sheet—changing the composition of its reserves.

-

Adding USDC reserves: As real-world dollars flow into crypto via stablecoins, DAI gains the ability to rapidly expand supply—no longer constrained by slower growth when relying solely on ETH and other crypto as over-collateral.

-

Adding U.S. Treasury reserves: By bypassing intermediaries like Circle, DAI directly benefits from the credit backing of U.S. Treasury debt. Had more Treasuries backed DAI during the recent USDC depeg crisis, DAI would have weathered the storm better—demonstrating the stabilizing power of diversified reserves.

We can clearly observe in MakerDAO’s asset breakdown that the proportion of real-world assets (RWA)—such as U.S. Treasuries—is steadily rising, while dependence on stablecoin assets declines.

Conclusion

After analyzing the question “Does MakerDAO share the Federal Reserve’s money-creation power?” from two perspectives, we find the answer less critical. MakerDAO’s purchase of U.S. Treasuries reflects its role as DAI’s “central bank” reallocating assets on its balance sheet—and this autonomy is the key takeaway.

In fact, real-world central banks already have discretion over their asset portfolios. In 2008, to rescue the subprime crisis, the Fed began accepting mortgage-backed securities (MBS) onto its balance sheet. Japan’s central bank uniquely holds large stakes in Japanese corporate stocks via trust funds—making it the largest single shareholder in many major firms.

In conclusion, MakerDAO’s purchase of U.S. Treasuries allows DAI to diversify its backing through external credit. The steady returns from Treasuries help stabilize DAI’s exchange rate, increase issuance elasticity, reduce reliance on USDC, and mitigate single-point risks. Overall, this strengthens DAI’s development. We look forward to greater achievements in the evolution of decentralized stablecoins.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News