Understanding SAFT and Web3 Token Investment through the Three-Token Model

TechFlow Selected TechFlow Selected

Understanding SAFT and Web3 Token Investment through the Three-Token Model

As the most common agreement in Web3 fundraising and investment, SAFT captures the value of Web3 projects through Tokens.

Author: Will Wang

Web3 is a value network built on blockchain, where all value can be tokenized. Tokens represent digital forms of value that freely, efficiently combine, circulate, and distribute across the Web3 value network. The "Three-Token Model" proposed by Dr. Xiao Feng of HashKey Group clearly explains the various dimensions of value—Utility Tokens, Security Tokens, and Non-Fungible Tokens (NFTs)—which respectively represent usage rights, ownership rights, and digital tokens.

SAFT (Simple Agreement for Future Tokens), the most common agreement in Web3投融资 (investment and financing), captures the value of Web3 projects through tokens. This article combines HashKey Group's whitepaper "Web3 New Economy and Tokenization" with Cooley LLP’s SAFT whitepaper to analyze SAFT, Web3 token investment mechanisms, and methods of value capture in token-based investments from the perspective of the Three-Token Model.

(from: How to Invest in Web3: The Next Phase of the Internet)

Summary

-

The Web3 new economy is a stakeholder economy, whose core lies in the system of usage rights;

-

In the three-token model, utility tokens, security tokens, and NFTs represent usage rights, ownership rights, and digital tokens respectively;

-

Usage rights cannot be securitized but can be tokenized—utility tokens represent such usage rights and capture the value derived from network benefits;

-

A SAFT itself is an investment agreement applicable only to utility tokens. Through a two-step mechanism, it enables the transformation of tokens from securities into utility tokens, thereby partially circumventing U.S. SEC securities regulation;

-

The goal of Web3 project investment and financing is to capture project value—the difference between equity and token investments lies in determining where value is realized and how it is captured.

The Three-Token Model of the Web3 New Economy

(from: Unpacking Tokenization, Leading the New Economy! The Whitepaper 'Web3 New Economy and Tokenization' Released at Hong Kong Web3 Festival 2023)

Deeply understanding the essence of the three-token model is highly beneficial for capturing different forms of value in Web3 investment and financing.

Whether under the economic models of Web1 or Web2 (surveillance capitalism), platforms hold ultimate ownership of information and data. These platforms generate enormous commercial value through monetization, giving rise to giants like Facebook and Google—but ordinary users are typically excluded from these gains. In contrast, Web3 based on blockchain networks operates under a value network economic model (stakeholder capitalism) emphasizing data trustworthiness, data sovereignty, and interconnected value. Under the premise that all value can be tokenized, value includes not just ownership, but more importantly, usage rights.

Ownership is exclusive and difficult to divide. Organizational structures under ownership systems (typically corporations) aim to maximize shareholder interests—a manifestation of shareholder capitalism. Usage rights, however, are non-exclusive and inherently shareable. They allow multiple authorizations, licensing, even open-source or CC0 perpetual reuse. The core of the usage rights system is stakeholder capitalism. Traditional organizational forms may no longer fit; decentralized autonomous organizations (DAOs) based on open-source or nonprofit foundations naturally align with stakeholder capitalism and have become the primary organizational form of the Web3 new economy.

Under the usage rights system, all participants act as stakeholders engaging in large-scale collaboration, contributing individually and sharing organizational value. In this context, the ownership represented by shareholders becomes irrelevant—the real value lies in project usage rights. Usage rights cannot be securitized but can be tokenized. Combined with blockchain's distributed ledger technology, usage rights can be standardized and fractionalized into tokens—directly linking each participant in the network to project value—this is the utility token (Utility Token).

(from: Web3 New Economy and Tokenization)

Built upon the Web3 economic model, the usage rights system, and stakeholder capitalism, the three-token model—utility tokens (Utility Token), security tokens (Security Token), and NFTs—enables value sharing among all participating stakeholders according to their respective value forms. For example, stakeholders must possess the token of a blockchain network, system, or application to gain access and use rights; or tokens may serve as voting instruments enabling participation in community governance—both are manifestations of usage rights.

-

Utility Tokens capture the network scale effect of the Web3 network, system, or application. The larger the ecosystem and user base, the higher the market demand for the token, with price determined by market valuation.

-

Security Tokens capture the future cash flow value of equity, debt, and other asset-backed securities.

-

NFTs represent digitized forms of underlying assets, also known as “digital tokens.” The value of NFTs relates to their anchored physical or digital assets and has diverse sources.

Legal Nature of SAFT

SAFT (Simple Agreement for Future Tokens)—Future Token Investment Agreement—is an investment instrument specifically designed for Web3 projects built on blockchain networks. A SAFT allows a project team to raise funds from investors during development in exchange for the right to purchase future tokens once the network launches.

Because security tokens (Security Tokens) are heavily regulated across jurisdictions, SAFT establishes a contractual framework aiming to launch utility token (Utility Token) networks, thus avoiding regulatory scrutiny by the U.S. Securities and Exchange Commission (SEC) over Web3 token fundraising activities.

(from: https://saft-project.org/)

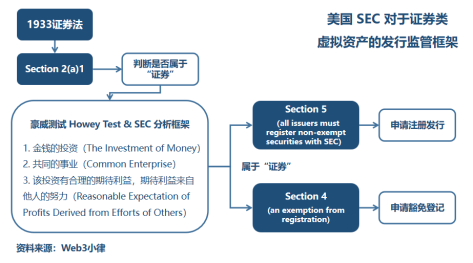

The SAFT whitepaper ("The SAFT Project: Toward a Compliant Token Sale Framework"), primarily drafted by U.S. law firm Cooley LLP, was released on October 2, 2017. It introduced the SAFT transaction model, aiming to provide Web3 projects with a compliant path for token issuance under the U.S. securities law regime. The process consists of two key steps:

(1) Project Development Phase: For Web3 projects still under development, investors contribute capital with profit expectations dependent on the project team’s management and development efforts. Since the token lacks actual utility at this stage, its nature resembles equity—as a representation of future value, capturing the Web3 project’s potential for future cash flows.

Such investment may satisfy the Howey Test criteria and qualify as an "investment contract," falling under strict SEC securities regulation. However, issuers may seek exemption under Regulation D Rule 506 of the U.S. Securities Act, avoiding registration by limiting investors to accredited investors only.

(2) Post-Launch Network Phase: Once the project is fully developed and launched, the issued tokens (Already-functional Utility Tokens) grant users access to various functionalities within the Web3 ecosystem (usage, consumption, governance, etc.). At this point, the token represents a usage right and is defined as a utility token (Utility Token).

Since the token now possesses practical utility, investors typically acquire it primarily to access network benefits rather than purely for speculative profit. Moreover, in a decentralized token economy or governance system, the token’s secondary market price is driven entirely by supply and demand dynamics, independent of the project team’s ongoing contributions. This fundamentally differs from the role of tokens during phase (1). Therefore, the SAFT whitepaper argues that such Utility Tokens lack the characteristics of “securities” and generally fall outside the scope of stringent SEC oversight. However, SAFT aims to comply with U.S. SEC regulations and strictly speaking applies only to accredited investors, making it unsuitable for most small and medium-sized retail investors.

(from: Kraken’s Legal Chief Has No Time to Educate Firms About Crypto)

Although we see the SEC challenging SAFT in recent cases like Kik and Telegram, the issues often stem from flaws in utility token design or token release timing. Even Marco Santori—one of the SAFT whitepaper’s drafters, a leading expert on crypto and U.S. securities law, and former general counsel at Kraken—faced regulatory action in February 2023 over Kraken’s Staking-as-a-Service product. This highlights how fragile compliance can be, especially given the vast differences among project networks, token functions, tokenomics designs, and investor profiles across various SAFT agreements.

There are multiple legal avenues for Web3 investment and financing, including equity-related instruments like SPA (Share Purchase Agreement), SAFE (Simple Agreement for Future Equity), token-related instruments like TPA (Token Purchase Agreement), SAFT (Simple Agreement for Future Tokens), or hybrid models such as SAFE + Token Warrant/Side Letter. The choice depends on the fundamental nature of Web3 investment and financing.

The Essence of Web3 Investment and Financing

The most important aspect of Web3 project investment and financing is determining where value is realized. When valuing equity-based projects, greater emphasis is placed on the company’s ability to generate future cash flows, since shareholders have legitimate claims to profit distribution. When valuing token-based projects, traditional cash flow valuation models do not apply. Instead, focus shifts to network scale effects, demand between the network and its token, and the token’s functionality. Thus, compared to token-funded projects, tokenomics becomes critically important.

(from: Connecting Web3 Wallet to Twitter Account)

(1) A Web3 Thought Experiment with Twitter

Currently, Twitter—the Web2 internet giant focused on creator ecosystems—operates as a corporate entity aiming to maximize shareholder value, reflecting shareholder capitalism. Investment value lies in the company’s ability to capture future cash flows, with stock prices reflecting the present value of those future cash flows. Now imagine a Web3 version of Twitter based on the new economic model: it incentivizes all participants in the ecosystem (content creators, developers, validators, other market actors) via tokens, collectively maintaining and governing the Twitter network. The token would not only serve as a medium of exchange but also enable access to the Twitter ecosystem, consumption of products/services within it, and participation in decision-making and governance.

This Web3 economic model redistributes economic benefits and governance power from centralized entities to the entire decentralized ecosystem. All participating stakeholders can share in the value they help create—reflecting stakeholder capitalism. In such a model, Twitter’s equity may become less meaningful, while its token could replace equity in capturing far greater value across the Twitter ecosystem. The token price would reflect supply and demand dynamics within the ecosystem.

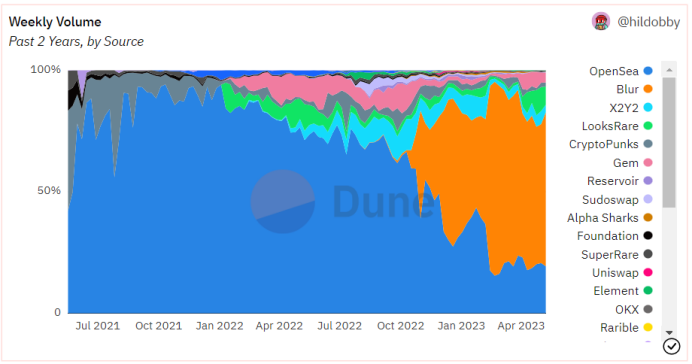

(from: https://dune.com/hildobby/NFTs)

(2) Opensea vs. Blur

In January 2022, OpenSea—the then-largest global NFT marketplace—raised $300 million from Paradigm and Coatue at a $13.3 billion valuation. OpenSea’s cash flow primarily comes from trading fees. Projects like OpenSea can be seen as typical examples of equity-based Web3 investment, compatible with traditional business models where investors capture the value of future corporate cash flows—making equity investment more appropriate.

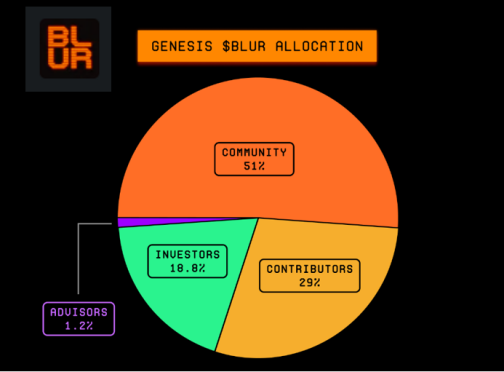

Around the same time, in March 2022, Blur secured $11 million in funding from Paradigm. Despite OpenSea’s dominance, Blur leveraged community activation—through token airdrops to early participants—to ignite liquidity in the NFT market, achieving a breakthrough in network effects and overtaking OpenSea within a year. Blur exemplifies a typical token-based Web3 investment, where investors capture the scale effect of the Blur ecosystem: the larger the ecosystem and user base, the higher the market demand for its utility token, with price emerging from market-driven valuation.

However, considering Blur’s lackluster token performance post-launch and limited token utility, it becomes evident that designing robust token functionality and sustainable tokenomics is crucial for long-term project success.

(from: https://docs.blur.foundation/tokenomics)

Thus, it is clear that the purpose of Web3 project investment and financing is always to capture project value—the difference lies in identifying where value is realized and through which mechanism it is captured.

Final Thoughts

The significantly enhanced liquidity of Web3 project value places higher demands on project teams, requiring them to clearly articulate the project’s future model and tokenomic design even at the whitepaper fundraising stage—otherwise, subsequent SAFT execution and development plans will be difficult to implement.

Therefore, during early stages when the project model is not yet solidified, hybrid approaches such as equity financing combined with token provisions (e.g., SAFE + Token Warrant/Side Letter) can be adopted. This achieves both compliance with U.S. securities regulations similar to SAFT, provides access to equity financing, and preserves the possibility of future token fundraising.

There are many possible approaches, but Web3 projects must generate real value—otherwise, everything remains illusory.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News