In-Depth Analysis of Grayscale Trust: A 50% Discount on ETH – Opportunity or Trap?

TechFlow Selected TechFlow Selected

In-Depth Analysis of Grayscale Trust: A 50% Discount on ETH – Opportunity or Trap?

In 2023, the cryptocurrency market once again became a focal point for investors, with BTC and ETH leading gains among major global asset classes

Executive Summary

-

The crypto market rebounded sharply in 2023 from last year’s deep bear cycle. Many investors may have missed the boat, making Grayscale's trust shares—which still trade at around a 50% discount to net asset value (NAV)—particularly attractive;

-

Given Ethereum’s foundational role in Web3 infrastructure, we believe Grayscale’s Ethereum Trust (ETHE) stands out for strong performance potential in a future bull market;

-

Historically, ETHE has traded at long-term premiums or discounts. Premiums were driven by factors such as lock-up periods on subscriptions, greater accessibility compared to holding ETH directly, and lower custody costs—making ETHE appealing to traditional financial institutions and retail investors wary of managing private keys;

-

Current persistent discounts are mainly due to the product's inability to redeem underlying ETH directly—a structural feature similar to closed-end funds. Other contributing factors include limited arbitrage opportunities, forced liquidations by large speculators, opportunity cost discounting, and competition from alternative products;

-

After negative premiums became entrenched in mid-2021, market expectations for ETHE returning to parity with NAV have grown increasingly longer—reaching over 14 years by the end of last year. It now stands at around 10 years. We believe this expectation remains excessively long; under more optimistic sentiment, the implied recovery time could reasonably fall below two years;

-

Seven scenarios could narrow or eliminate the discount: enabling direct ETH redemptions (either via SEC exemption or successful ETF conversion), obtaining redemption waivers, trust dissolution and liquidation, share buybacks by Grayscale, development of arbitrage strategies, increased market confidence, and declining opportunity costs;

-

Since its inception in 2019, ETHE has not yet completed a full market cycle. A complete cycle should follow premium → parity → discount → parity → premium. So far, only half the cycle has played out. We argue that if one is betting on a potential bull run, ETHE offers superior leverage—evidenced by its YTD gains being 1.7x those of ETH;

-

However, historical data shows ETHE’s risk-return profile is suboptimal. As shown in Table 1, ETHE underperforms ETH/USD across nearly all metrics. This implies that long-term holders may need targeted yield-enhancement strategies, otherwise ETHE risks underperforming the broader market if the bull market does not arrive swiftly.

Overview

In 2023, the cryptocurrency market once again captured investor attention, with BTC and ETH leading global asset classes in returns. Yet many investors remain stuck in bear-market thinking and failed to seize this opportunity. However, within Grayscale’s trust offerings like GBTC and ETHE, investors can still gain exposure at nearly a 50% discount.

We believe Ethereum (ETH) will serve as core infrastructure for mainstream Web3 applications. Beyond capturing spillover capital from traditional finance like BTC, it also offers alpha from the growth of the Web3 ecosystem. This report focuses specifically on the discount phenomenon and investment potential of Grayscale’s Ethereum Trust (ETHE), analyzing scenarios under which this discount may shrink or disappear, and presenting reasons why professional investors might consider entering the crypto market through this vehicle. We also examine the product’s legal structure and associated risks.

Grayscale Bitcoin Trust was launched back in September 2013 and structured legally as a grantor trust—a setup where the creator (grantor) retains ownership and control over the assets. For practical purposes, this functions similarly to a closed-end fund. Under this unique structure, investors indirectly own the trust’s assets by purchasing beneficial interests. Like closed-end funds, grantor trusts typically do not allow shareholders to redeem their shares at any time.

Grayscale Ethereum Trust (ETHE) (formerly known as Ethereum Investment Trust) ("the Trust") is a statutory trust formed under Delaware law on December 13, 2017, and began trading publicly in July 2019, adopting the same trust structure as GBTC.

One advantage of this trust structure is that since the trust itself does not trade, buy, sell, or derivatives of Ethereum on exchanges, it avoids falling under the jurisdiction of certain regulatory bodies—enabling faster product launch—even though there remains ambiguity over whether ETH falls under CFTC or SEC oversight.

First, let's briefly compare ETHE and ETH:

Different Investment Methods

ETHE is a listed trust fund regulated by the U.S. Securities and Exchange Commission (SEC), making it easier for institutional investors to manage on balance sheets. ETHE trades through standard brokerage accounts—simpler and cheaper than using crypto exchanges. It qualifies for Individual Retirement Accounts (IRAs) and 401(k)s, offering tax advantages. Investors avoid learning how to manage crypto wallets and eliminate risks related to losing private keys or hacking attacks.

Different Supply Mechanics

ETH has no hard cap on total supply, whereas ETHE’s supply depends entirely on Grayscale’s issuance schedule.

Different Market Demand

As an investment product, ETHE serves different demand dynamics than ETH. Institutional and novice investors may prefer ETHE, while active crypto traders often favor direct ETH trading.

Other Differences

ETHE investors currently cannot redeem underlying ETH or equivalent USD from Grayscale. The trust charges an annual management fee of 2.5% of NAV. ETHE cannot participate in DeFi staking or other on-chain activities.

Theme 1: Why Such a Deep Discount?

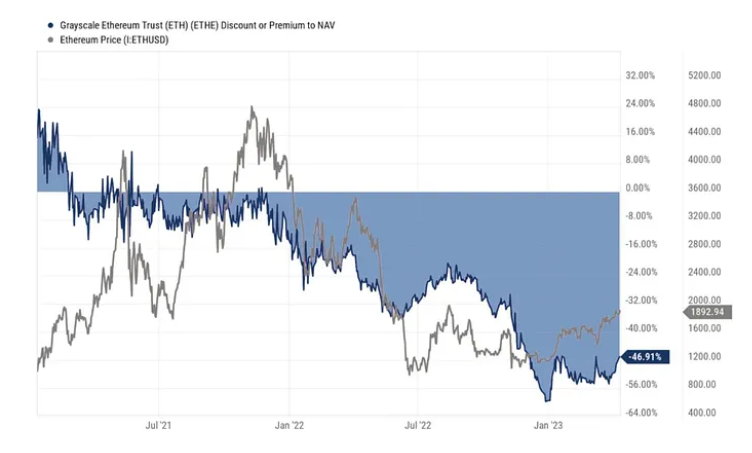

In theory, ETHE’s price should fluctuate around the value of its ETH holdings. In practice, however, secondary market pricing doesn’t always reflect NAV accurately. Since ETHE’s public listing in 2019, it experienced prolonged periods of positive premium—peaking above 1000% shortly after launch. Starting February 2021, ETHE entered a sustained phase of negative premium (discount), which continues today.

Figure 1: Historical ETHE Premium/Discount vs. ETH Price Trend

Source: Grayscale, Trend Research

Grayscale’s crypto trust shares resemble closed-end funds, resulting in limited initial market supply. Additionally, due to the immaturity of the crypto market, many investors didn't know how to purchase or store cryptocurrencies, so Grayscale’s trusts—which could be bought directly via U.S. brokerages—traded at a premium.

Notably, ETHE reached its highest absolute premium on June 21, 2019. Until February 2021, when it first turned negative, ETHE consistently traded at high premiums. Afterward, during a bull market and amid increasing availability of Bitcoin/Ethereum-tracking index products, investor options expanded, pushing ETHE toward fair-value pricing in secondary markets.

On June 29, 2021, the SEC rejected GBTC’s application to convert into an ETF. Within an hour, Grayscale sued the SEC—an event that further widened ETHE’s discount. From mid-2021 to late 2022, as the digital asset market peaked and weakened, several high-profile failures—including Three Arrows Capital (3AC) and BlockFi)—led to forced selling by leveraged speculators who had to exit positions regardless of prevailing discounts, further expanding ETHE’s discount.

Figure 2: Premium/Discount Changes Since First Negative Premium in Early 2021 vs. ETH Price

Source: Tradingview, Trend Research

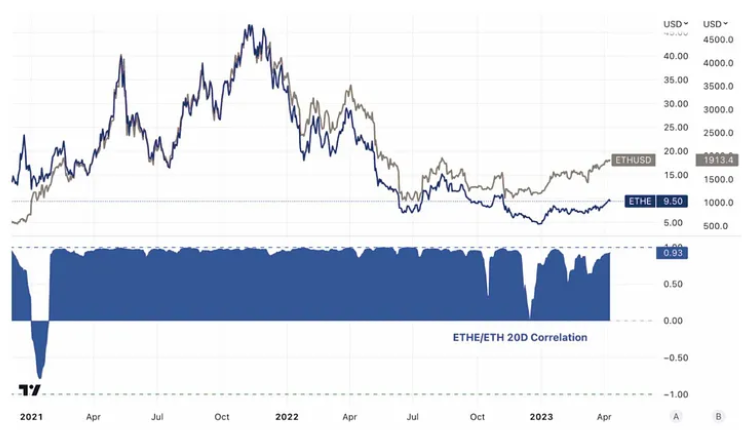

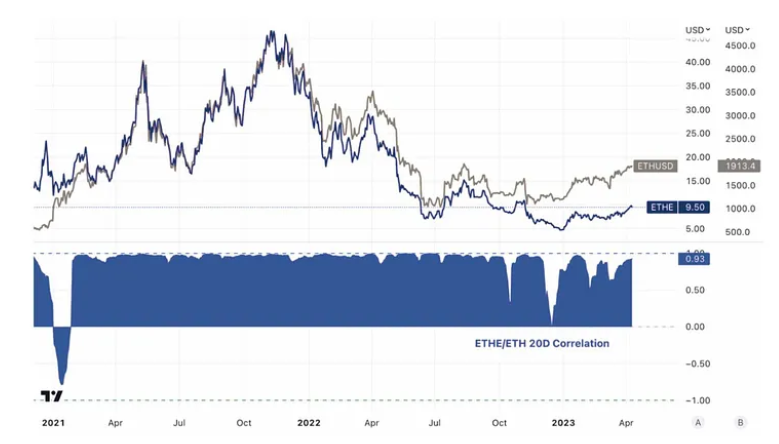

Figure 3: ETHE and ETH prices have remained highly correlated most of the time

Source: Tradingview, Trend Research

In summary, both positive and negative premiums stem from ETHE’s inability to directly redeem shares. Positive premiums arose because ETHE offered better accessibility than holding ETH spot, lower custody costs, balance sheet accounting ease, tax benefits, and compliance simplification. Negative premiums result from four main factors: non-redeemable structure, limited arbitrage, opportunity cost discounting, and competitive pressures—discussed in detail below.

1. Non-Redeemable Fund Structure

According to legal documents, only Authorized Participants (APs) designated by Grayscale can directly purchase or redeem ETH from the trust. APs must meet specific qualifications and regulatory standards, including registration as broker-dealers and adherence to applicable regulations. Per rules, trust shares are issued in blocks of 100 units, and each subscription requires ETH spot collateral.

To date, only two entities have served as APs. Prior to October 3, 2022, Genesis Global Trading, Inc., a subsidiary of DCG, was the sole AP. After that date, Grayscale Securities replaced it as the exclusive AP.

Effectively, Grayscale acts as its own primary dealer, and other investors can only acquire shares distributed by them. While some institutions may access near-primary-market pricing, they are not direct subscribers and hold no redemption rights. There are likely two reasons why these institutions engage: first, to capture arbitrage opportunities during periods of premium; second, to use Grayscale as a custodian to avoid private key management risks and costs.

Currently, the trust lacks an operational share redemption program, meaning neither APs nor their clients can redeem shares through the trust. Consequently, participants cannot exploit arbitrage opportunities when secondary market prices deviate from the NAV per ETH share, preventing effective correction of discounts. If direct redemptions were allowed, market participants could buy discounted shares on the secondary market and redeem higher-valued ETH from the fund, narrowing the discount.

2. Limited Arbitrage Opportunities

The lack of direct redemption restricts arbitrage, a factor less impactful during bull markets with positive premiums but significantly pronounced during bear markets with negative premiums.

In traditional ETF markets, demand imbalances cause prices to diverge from NAV, creating arbitrage opportunities that quickly correct mispricing.

There are two primary forms of arbitrage:

Basic Arbitrage

-

During premium: Investors subscribe to new ETF shares and sell them on the secondary market—reducing ETF demand/price.

-

During discount: Investors buy ETF shares cheaply on the secondary market and redeem them for higher-value underlying assets—increasing ETF demand/price.

CTA Strategy Arbitrage

For ETFs with delayed subscription/redemption, traders can bet on convergence between the underlying asset and ETF share prices.

-

When premium reaches a threshold: go long the underlying asset, short the ETF shares.

-

When discount reaches a threshold: short the underlying asset, go long the ETF shares.

This strategy’s effectiveness depends on the convergence mechanism. In ETHE’s case, since value reversion relies heavily on regulatory decisions rather than predictable market actions (like redemptions), uncertainty is high, allowing wider spreads to persist.

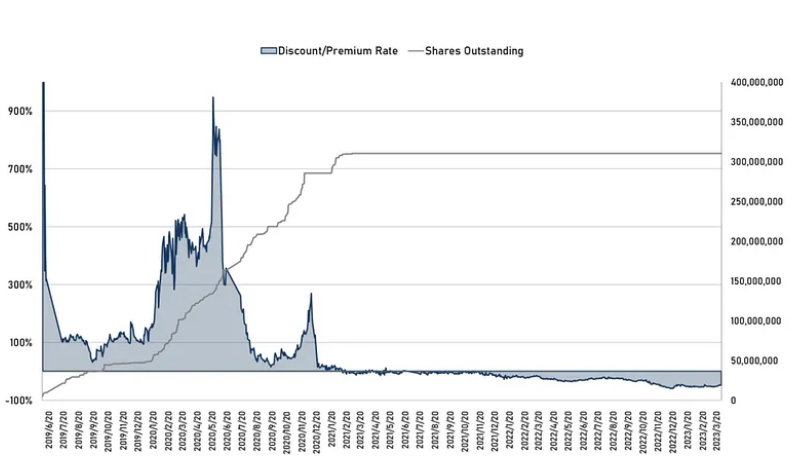

Figure 4: ETHE Historical Premium/Discount Rate vs. Circulating Shares

Source: Grayscale, Trend Research

From the chart above, we see that after the premium narrowed, basic arbitrage vanished post-spring 2021, and new share creation halted.

Traditional markets offer a classic analogy: Berkshire Hathaway stock. As an investment firm, its shares reflect portfolio valuations, but ordinary investors cannot demand asset redemption or issue new shares at will.

Yet for decades, Berkshire Hathaway stock has traded at a premium to its net asset value, largely due to Warren Buffett’s proven track record and market credibility. Still, premiums have contracted during certain periods reflecting shifting investor sentiment.

For example, in March 2020, Berkshire’s stock dropped ~30%, briefly trading at a significant discount—likely reflecting concerns over the pandemic and its exposure to travel, aviation, and finance sectors.

Returning to ETHE: after initial purchases, shares must be held for at least six months before secondary market resale. Thus, basic arbitrage during premium phases exists, albeit delayed. But after ETHE first showed a discount in February 2021, primary market subscriptions nearly ceased—because discount arbitrage requires redemption mechanisms, and Grayscale’s timeline for reopening such programs remains unclear. Without clear advantages over holding spot ETH, ETHE struggles to regain premium status like Berkshire Hathaway.

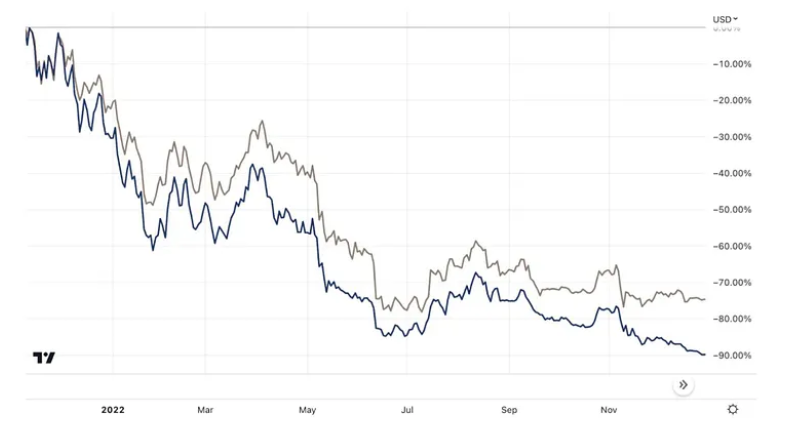

Moreover, as the crypto market peaked and declined, major players like 3AC and BlockFi—who previously profited from GBTC/ETHE premium arbitrage via "subscribe-and-wait-six-months" strategies—were forced to dump shares due to excessive leverage or liquidity issues, even at steep discounts. Public reports indicate DCG recently sold about 25% of its ETHE holdings at roughly half price due to financial stress, widening ETHE’s discount.

Figure 5: ETHE vs. ETH Performance Comparison from Mid-2021 Peak to Late-2022 Trough:

Source: Tradingview, Trend Research

3. Opportunity Cost Discounting

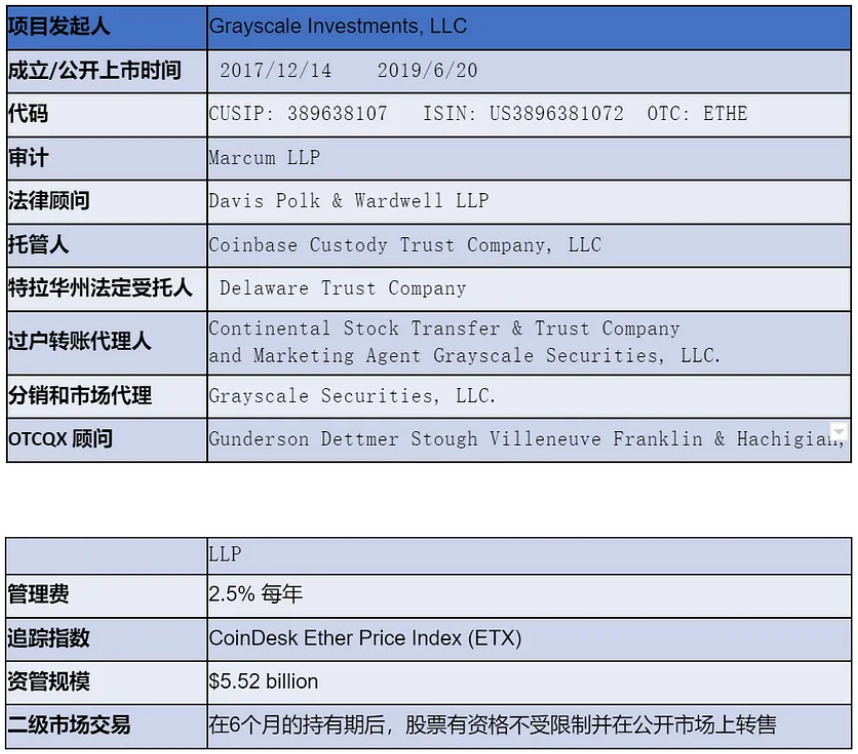

Table 1: ETHE Legal/Financial Information (As of March 31, 2023)

Source: Grayscale, Trend Research

Grayscale Ethereum Trust charges an annual management fee of 2.5% of NAV. Public data shows Grayscale deducts accrued but unpaid fees daily from its ETH holdings—meaning the amount of ETH represented per ETHE share gradually decreases, as illustrated below.

Figure 6: ETHE Circulating Shares (Left) vs. ETH Held Per Share (Right)

Source: Grayscale, Trend Research

Ignoring other risks, today’s discount can be interpreted as a discounting of holding opportunity costs. Using the current discount rate X and holding cost Y, we can estimate the implied market expectation T for redemption or NAV parity restoration. Assuming zero expected NAV growth and defining:

Holding cost = 10-year Treasury yield + 2.5% management fee, then: (1-Y)^T = 1+X

Solving: T = ln(1+X)/ln(1-Y)

Figure 7: ETHE Historical Discount Rate vs. Implied Market Expectation for Redemption (Parity Restoration Time in Years)

Source: Grayscale, Trend Research

The chart shows that after mid-2021, market expectations for ETHE returning to parity lengthened steadily—exceeding 14 years by year-end due to regulatory pressure and cold markets—now down to about 10 years. We believe this remains overly pessimistic. With renewed optimism, the implied recovery time could plausibly drop below two years. Only in worst-case liquidation scenarios would a >10-year horizon make sense—consider Mt. Gox took just nine years to settle.

4. Competitive Product Pressure

Before 2019, Grayscale faced little competition. On February 18, 2021, Purpose Bitcoin ETF—a Canadian fund directly investing in Bitcoin—began trading and rapidly amassed over $1 billion in AUM within a month. With a 1% fee—less than half of GBTC’s—and an ETF structure enabling tighter tracking, it proved more attractive than Grayscale’s offering.

Just two months later, on April 17, Canadian regulators approved three Ethereum ETFs simultaneously: Purpose Investments’ ETHH, Evolve Capital Group’s ETHR, and CI Global Asset Management’s ETHX—all listed on April 20. According to official websites, management fees vary: CI Global charges 0.4%, Evolve 0.75%, and Purpose 1%. On day one, Purpose ETH ETF attracted CAD 26.46 million (~$21.32M), ETHR raised CAD 2.22M (~$1.79M), and ETHX reached CAD 2.25M (~$1.81M).

Three days later, on April 23, Canada’s fourth Ethereum ETF started trading on the Toronto Stock Exchange—a joint venture between digital asset manager 3iQ and CoinShares, offering CAD (ETHQ) and USD (ETHQ.U) share classes.

Additionally, growing availability of ETH futures ETFs, related equities (including public companies holding ETH, mining firms, and asset managers) has diversified investment avenues—eroding Grayscale’s uniqueness among traditional finance institutions and retail investors, becoming a critical competitive challenge.

Theme 2: When Could the Discount Narrow or Disappear?

Seven scenarios could narrow or eliminate the discount: enabling ETH redemptions (via SEC exemption or ETF conversion approval), obtaining redemption waivers, trust dissolution, Grayscale-led buybacks, development of arbitrage strategies, improved market confidence, and declining opportunity costs.

1. Regulatory Improvement—ETF Approval

According to Grayscale’s latest Form 10-K filed at year-end 2022, they maintain that upon SEC approval of ETF conversion, the trust could initiate a redemption program. Although the SEC rejected GBTC’s ETF application, a U.S. federal appeals court judge questioned the SEC’s decision in March, noting prior approvals of Bitcoin futures ETFs.

Note: Grayscale has only applied to convert GBTC into an ETF—not ETHE. Still, recent developments are encouraging. At a hearing on March 7, Grayscale argued that the SEC applies inconsistent standards—approving Bitcoin futures ETFs while rejecting spot-based ones despite identical underlying assets. They claim this arbitrary treatment violates federal law. The SEC counters that it applies consistent criteria, arguing futures and spot markets differ fundamentally due to CFTC oversight of the former, while claiming spot crypto markets remain unregulated.

Prior to the hearing, Bloomberg analyst Elliot Stein believed the SEC held the upper hand, given courts usually defer to expert agencies. However, after reviewing arguments, Stein revised his view, assigning Grayscale a 70% chance of winning. A GBTC approval would positively impact ETHE sentiment. However, unlike BTC, which already has SEC-approved futures ETFs, no Ethereum-based fund has been approved—partly due to ongoing debate over Ethereum’s legal classification.

2. Regulatory Improvement—Registration as Investment Company or Commodity Classification

Grayscale Ethereum Trust (ETHE) is a registered investment trust, not an investment company. Specifically, it’s established under state law and registered with the SEC under exemptions from the 1933 Securities Act—meaning it’s exempt from certain disclosure and registration requirements.

However, if the SEC determines the trust must register under the 1940 Investment Company Act, Grayscale believes the trust could dissolve, with shares converted into equity—though this remains speculative, dependent on final regulatory views and exchange policies.

Alternatively, if ETHE is deemed a commodity portfolio by the CFTC, it would fall under the Commodity Exchange Act (CEA), requiring registration and oversight—a possible regulatory path forward.

3. Obtaining Redemption Exemption

Grayscale once offered a redemption program, but it was suspended in 2016 after SEC alleged violations of Regulation M. The SEC feared simultaneous share creation and redemption could manipulate prices, enabling insider trading or unfair practices. Since then, Grayscale paused GBTC redemptions and extended the policy to BCH and ETHE trusts to comply with regulations.

Currently, Grayscale does not expect the SEC to consider reinstating continuous redemptions, so no efforts are underway to seek such approval.

Still, actively seeking such an exemption remains possible, though timing and success are uncertain. Moreover, enabling redemptions would reduce Grayscale’s revenue as trustee, so current incentives to pursue this waiver appear weak.

If such an exemption is granted and Grayscale agrees to enable redemptions, a redemption program could launch. This would allow APs to arbitrage whenever share market value diverges from ETH holdings (net of fees). Such arbitrage might remain exclusive to APs or be passed to clients—but with only Grayscale-affiliated firms serving as APs, exclusivity raises fairness concerns.

4. Market Sentiment, Arbitrage Development, and Confidence

Earlier we discussed how broken arbitrage channels prevent effective discount correction. However, CTA strategies suggest that even without redemption, rising market momentum could compress the discount. Since ETHE’s 2019 launch, it hasn’t completed a full “cycle.” We define a full cycle as premium → parity → discount → parity → premium. So far, ETHE has only completed the first half.

Figure 8: Annual Return Comparison – ETHE vs. ETH (shows ETHE underperforms ETH over annual cycles)

Source: Grayscale, Trend Research

Figure 9: Monthly Return Comparison – ETHE vs. ETH (shows ETHE has higher short-term elasticity than ETH)

Source: Grayscale, Trend Research

Annual and monthly return charts show that from 2019–2022—the 'premium → parity → discount' phase, effectively a deflationary bubble period—ETHE delivered no excess returns, making it a poor investment choice. However, due to ETHE’s higher elasticity versus ETH, the upcoming “discount → parity → premium” recovery phase should generate stronger positive returns. Indeed, in the first three months of this year, ETHE gained 1.7x more than ETH—already evident.

5. Trust Dissolution if ETF Conversion Fails

If neither redemption exemption nor ETF conversion is achieved, prolonged fee deductions may fuel investor dissatisfaction, pressuring Grayscale toward liquidation. Once dissolution is confirmed, the NAV discount could rapidly close.

Indeed, bankrupt FTX affiliate Alameda Research sued Grayscale Investments and parent DCG in March 2023, accusing Grayscale of charging excessive fees and blocking redemptions from GBTC and ETHE, claiming “hundreds of millions in losses.” Similar lawsuits may increase over time.

Per filing disclosures, key triggers for early termination and liquidation of ETHE include:

-

Federal or state regulators mandating closure, forced liquidation of ETH holdings, or seizure/restriction of trust assets;

-

If CFTC, SEC, FinCEN, or others determine the trust must comply with specific rules, Grayscale may choose dissolution to avoid liability;

-

Grayscale deems asset risk, cost, and return disproportionate;

-

Trust license revoked;

-

Conversion of trust assets to USD becomes impractical;

-

Custodian resigns or is dismissed without replacement;

-

Trust becomes insolvent or bankrupt.

6. Grayscale Self-Buyback

Consider an extreme scenario: Grayscale buys back all outstanding shares below NAV, choosing to privatize or liquidate the trust—a clearly profitable move. Announcing a large buyback program could boost market confidence and help narrow the discount.

Digital Currency Group (DCG), Grayscale’s parent, announced up to $1 billion in trust share buybacks from 2021–2022. Yet GBTC continued trading below NAV—likely because the scale was small relative to multi-billion-dollar AUM, though secondary market buybacks do help narrow gaps.

Additionally, CEO Michael Sonnenshein mentioned in his 2022 letter to investors that if GBTC fails to become an ETF, one solution could be a tender offer—for example, repurchasing up to 20% of outstanding shares. If implemented, such measures might extend to all旗下 trusts, potentially narrowing ETHE’s discount.

7. Declining Opportunity Costs

As discussed in Theme 2, today’s discount partly reflects discounted opportunity costs. Therefore, if Grayscale reduces fees or risk-free rates decline, the discount could narrow even with unchanged recovery timelines. Indeed, CEO Sonnenshein noted in March that fee reductions are possible.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News