Stablecoin Depeg Emergency Escape Guide

TechFlow Selected TechFlow Selected

Stablecoin Depeg Emergency Escape Guide

What should you do when the stablecoin you hold faces a depegging risk?

By CapitalismLab

When the stablecoin you hold faces a de-pegging risk, what should you do? What's the logic behind Sun's seemingly useless move of swapping USDC for DAI?

From mainstream decentralized stablecoins and centralized stablecoins to hedging strategies via token holdings, this article combines underlying mechanisms, real data, and case studies to provide you with the most comprehensive emergency escape guide for stablecoin de-pegging.

Decentralized Stablecoins

The core goal of emergency escape is to reduce risk at the lowest possible cost, creating a time window for further actions and decisions. Therefore, beyond long-term logic, it’s more important that the solution holds its peg in the short term. We’ll break this down by different pegging mechanisms.

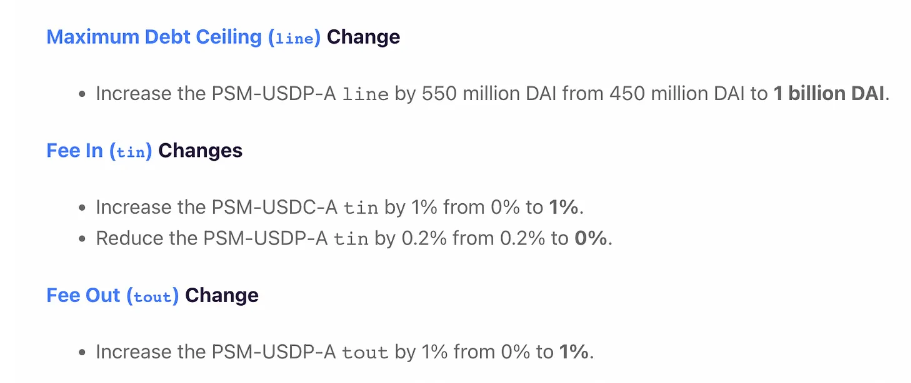

A. PSM

Direct exchange with other stablecoins to maintain peg, such as DAI supporting 1:1 swap with USDC/USDP.

If both are 1:1 swaps, why did Brother Sun exchange USDC for DAI?

There are actually benefits:

PSM capacity has an upper limit. Once reached, it becomes one-way conversion—only DAI → USDC, not USDC → DAI—making DAI ≥ USDC in value.

If USDC eventually can only be redeemed for dollars at $0.98, MakerDAO might absorb this loss to re-peg.

In a market crash scenario triggering mass repayments and liquidations, borrowers will need to buy back DAI to settle debts, pushing up DAI’s price.

In short, this is essentially a no-lose trade capable of absorbing large capital inflows, which naturally appeals to Brother Sun. In fact, on March 11, MakerDAO passed an emergency proposal increasing fees for USDC→DAI swaps, and due to PSM-USDC hitting its cap, DAI briefly traded at around a 2% premium over USDC. This escape route doesn't fully eliminate exposure to USDC but offers high capital capacity and strong short-term certainty.

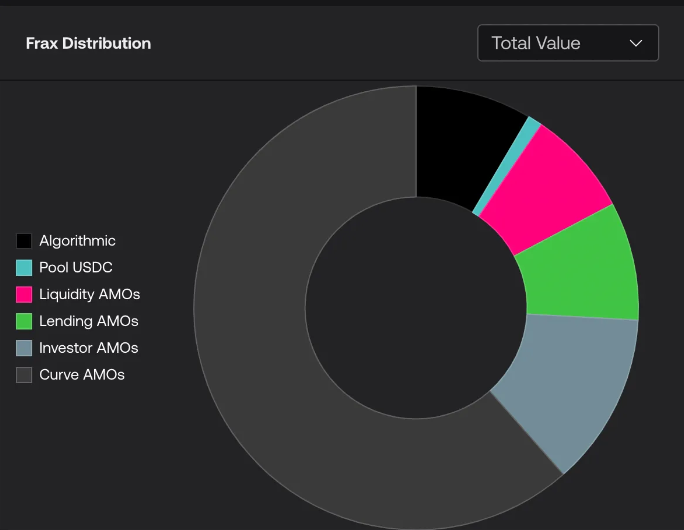

B. AMO

Public market price intervention, e.g., FRAX / crvUSD.

For example, FRAX holds most of its underlying assets in Curve AMOs, such as Curve FRAX/USDC LP tokens. When FRAX < $1, removing FRAX from the FRAX/USDC pool effectively buys FRAX and supports its price; when FRAX > $1, issuing new FRAX into the pool sells FRAX and suppresses the price.

Why did FRAX also de-peg this time?

Ultimately, it still relies on external assets for pegging—when USDC de-pegged, so too did the FRAX/USDC reserves. So while FRAX was unaffected during UST’s collapse, if the underlying AMO assets like USDC/USDT/DAI face issues, FRAX cannot avoid being impacted.

Therefore, using AMO-based stablecoins for emergency escape requires verifying whether the underlying AMO assets are sound—suitable only for those who deeply understand the internal mechanics of these coins.

C. Debt/Collateral Pricing Conversion

Two-way conversion like Luna/UST, one-way conversion like LUSD→ETH.

LUSD is an over-collateralized stablecoin backed solely by ETH, emphasizing purity.

Since launch, LUSD has never significantly stayed below $1 for long, often trading above $1. Why? Because users can redeem 1 LUSD plus a fee for ETH worth exactly $1. Yes, similar to UST exchanging for Luna at $1, except you can’t directly swap ETH for LUSD at $1. Thus, whenever LUSD trades below $1*(1−fee%), a clear arbitrage opportunity arises. Combined with low-risk ETH-only collateral and borrowers’ unwillingness to see prices fall further, prompt arbitrage keeps the peg intact.

As for why it frequently trades above $1, during ETH price drops, many borrowers are forced to buy back LUSD to repay loans, driving up its price. You could argue that one could borrow and sell LUSD to profit—but there’s no certainty about when the price will drop again. With high liquidation risks in bear markets, this leads to persistent premiums. What’s the upper bound? Since LUSD’s minimum collateral ratio is 110%, meaning $110 worth of ETH can mint 100 LUSD, once LUSD exceeds $1.10, immediate arbitrage becomes certain. Hence, the ceiling is $1.10.

Therefore, for small-to-medium-sized funds, buying LUSD at ≤$1 is a relatively solid escape option. Of course, extreme conditions leading to massive defaults are uncontrollable—but relatively speaking, LUSD remains a good choice.

D. Random Pegging

Simply put, they have a pegging mechanism but weak enforcement.

For example, MIM—an over-collateralized stablecoin without PSM—works on the principle that when the price falls below $1, borrowers can cheaply buy MIM to repay debt and reclaim collateral for arbitrage.

Yes, the theory holds—but what if borrowers believe the coin will keep falling or won’t rebound soon? Given MIM accepts complex collaterals like Curve LP or GLP, which carry higher risks, lack of confidence in bear markets naturally results in prolonged de-pegging.

DAI has already walked this path, proving ineffective at maintaining a peg. Considering most current projects differentiate themselves from DAI/LUSD by adding riskier collateral types to expand use cases, they’re unsuitable for emergency escapes—likely jumping from one hole into another.

Centralized Stablecoins

Centralized stablecoins rely on USD reserve assets to maintain their dollar peg, so analysis must focus on the quality of these reserves. Reserve safety ranking (high to low): Treasury bonds = Repo agreements > Cash (bank deposits) > Low-quality assets (commercial paper, corporate bonds). Additionally, bonds have maturity dates—the shorter the maturity, the better the liquidity.

Based on the Twitter threads analyzing BUSD/USDC/USDT reserve compositions below, overall safety and liquidity rank as BUSD > USDC > USDT. However, USDT benefits from long-term testing and opacity advantages, whereas BUSD has become a target of U.S. regulators.

Other lesser-known options like USDP and GUSD operate similarly. After announcing zero exposure to Silicon Valley Bank, their risks diminished. Still, note that widespread bank failures inevitably impact centralized stablecoins—surviving this round doesn’t guarantee safety next time.

Currently, stablecoins with higher allocations to Treasuries and repos remain more reliable. If you're willing to hold dollar assets, short-term Treasury risks shouldn't be overweighed—they represent the highest tier of safety among dollar assets. If concerned, converting to RMB may be wiser.

Further Reading:

Could U.S. Treasury defaults trigger USDC/USDT collapse?

BUSD hit by U.S. regulatory crackdown—how risky is it really?

Hold Tokens + Short Hedge

Buy 1 ETH spot and short 1 ETH in futures—seems perfect, but problems arise:

You must trust the exchange. Many exchange balances are denominated in stablecoins. Solana’s UXD once held SOL and shorted SOL on perp DEX Mango, which不幸遭遇黑客攻击…

If you short ETH/USDT pairs, you’re effectively holding USDT; shorting ETH/BUSD means holding BUSD—ultimately circling back to square one.

However, for coin-margined contracts like Binance, where Index prices are derived from real USD pairs, this appears feasible.

Note that coin-margined contracts are denominated in USD—so you can’t short exactly 1 BTC, only $10,000 worth of BTC. Under high volatility, perfect hedging isn’t maintained. Also, coin-margined contracts aren’t widely understood—test thoroughly before large-scale deployment.

Summary

From the strategies outlined above, you can choose the best escape path based on your situation. But any indirect USD holding within crypto inherently carries extra risk. The safest way to hold USD assets is undoubtedly buying U.S. Treasuries. For proper execution, refer to the thread below. If you're a qualified investor with substantial funds, feel free to contact Miaowaziseed—my friend Pikachu offers premium, crypto-native U.S. Treasury services.

Further reading: How to cash out and buy U.S. Treasuries?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News