How to drive mass adoption of DeFi protocols?

TechFlow Selected TechFlow Selected

How to drive mass adoption of DeFi protocols?

Self-custody remains the main selling point, with stablecoins, SBTs, and regulatory dApps complementing each other.

Written by: Ignas

Compiled by: TechFlow

It's well known that DeFi protocols are difficult to use for people outside the crypto space. Concepts like seed phrases, public keys, and private keys are hard for most people to grasp—let alone our parents' generation.

Therefore, to achieve mass adoption of DeFi, we need to do better.

How?

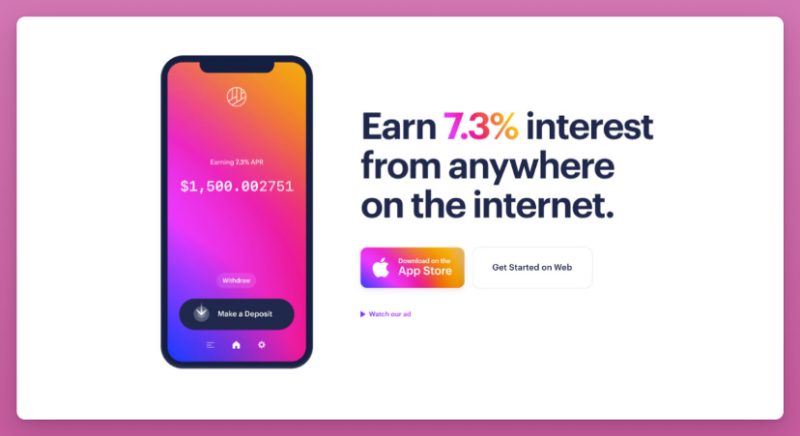

The Dharma app is a great example.

It was an iOS and Android mobile application offering 7.3% yield on USD deposits—simply transfer dollars from your bank account to your Dharma account.

Dharma deposited stablecoins into DeFi protocols and handled all the complexity in the background.

However, Dharma failed. It missed the right timing.

When DeFi Ponzi farms were offering APYs of 10,000%, their yields were only a few percent.

Eventually, Dharma was sold to Opensea and faded into obscurity.

If they could offer 7.3% APY today, I would be their most loyal customer.

Since then, DeFi has become even more complex, making it accessible to fewer people.

As we pursue higher capital efficiency, reduced slippage, and new feature development, complexity becomes inevitable.

Yet, the front-end user layer should remain easy to use. This means eliminating unnecessary crypto jargon and focusing on core value propositions.

Recently, Reddit launched Collectible Avatars, emphasizing collecting unique avatars and customizing them. This time, all crypto terminology was removed—no need for users to understand cumbersome seed phrases, private keys, or complex withdrawal processes from exchanges.

Self-Custody Is DeFi’s Key Selling Point

Self-custody ensures your assets cannot be taken away. Your assets remain yours—this is a key value proposition for millions globally.

Currently, cryptocurrency wallets are the biggest barrier to self-custody.

Argent Wallet is working to change this through account abstraction. It allows users to:

-

Create and recover a wallet using email or phone number.

-

Perform one-click transactions, so swapping on Uniswap doesn’t require three steps (approving two tokens plus the swap), but can be done in a single transaction.

-

Pre-approve apps and set rules limiting interactions with dApps, allowing unlimited usage within those rules without signing every transaction.

-

Enable 2FA protection, significantly enhancing fund security.

-

Support plugins like an app store, adding new functionalities to your account.

These improvements mean creating a wallet could be as simple as creating an email account.

Currently, when creating a wallet, we're greeted with 12 seed words that must be written down on paper. Lose them, and you lose your money.

Stablecoins—The Gateway to DeFi

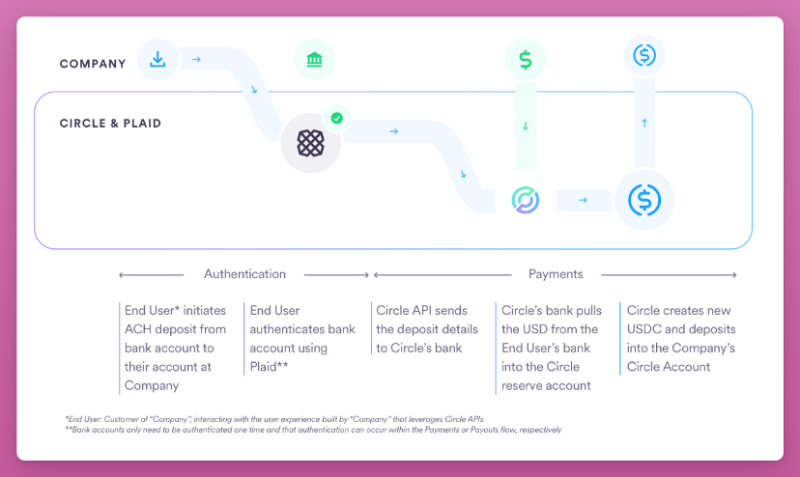

Additionally, we need a better way to convert fiat into stablecoins without relying on centralized exchanges.

dApps could support direct integration with Circle for USDC and EUROC. I could wire funds from my bank to Argent Wallet’s SEPA address, then EUROC would be deposited into Circle and integrated seamlessly in the backend. These stablecoins would reside in my self-custodied account, inaccessible to Argent.

Easily accessible stablecoins serve as gateways into the DeFi ecosystem. They enable:

-

Earning yield via lending or integrating with DeFi yield aggregators.

-

Supporting wallet-to-wallet transfers and payments, enabling me to send money to my mom without bank wires.

-

Trading cryptocurrencies or tokenized stocks (if supported by regulations in your country).

Of course, perhaps we also need an upgrade: paying gas fees in stablecoins.

Regulate dApps, Not Protocols!

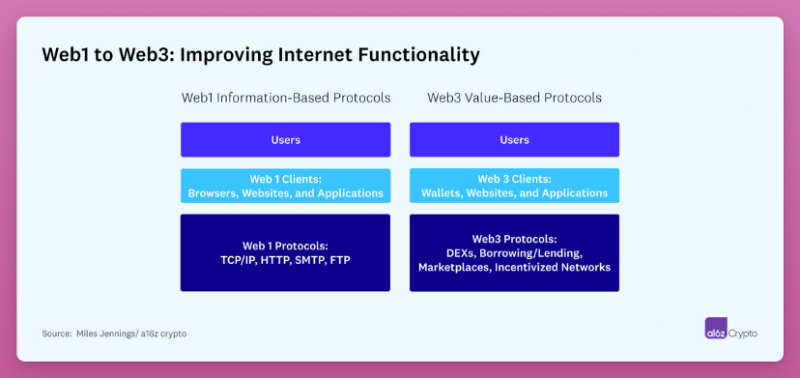

Mass adoption won't happen without regulation. A16z advocates regulating user access to Web3 applications (clients), but not the underlying protocols.

Early internet proponents argued for keeping it forever free, open, and unregulated—a borderless tool for humanity. They were partially successful: communication protocols like HTTP (web data exchange), SMTP (email), and FTP (file transfer) remain free and open.

The same logic can apply to crypto.

Thus, while you may need KYC to deposit fiat into Argent, smart contract protocols themselves should not be regulated. Regulating front-end user applications would allow continued innovation in DeFi protocols as we see today.

There are several reasons why regulating protocols is a bad idea:

-

They technically cannot comply with subjective regulations. What defines a security token for a smart contract protocol?

-

They cannot adhere to global regulations. Can you adapt a smart contract to 195 different national rules?

Such regulation does not imply universal KYC. Regulating dApps still allows privacy-seeking users to interact with DeFi protocols as they do today, while most people prefer usability over privacy. Otherwise, everyone would use TOR or VPNs.

Soulbound Tokens: Your On-Chain Credentials

The next step is bringing people into DeFi.

Currently, we interact with protocols through semi-anonymous accounts (e.g., 0x2c9...1w2), each treated equally by smart contracts. These are easy to create and often disposable.

"Yet, the economic value of financial transactions arises from humans and their relationships." — Vitalik Buterin and colleagues in a paper introducing Soulbound Tokens.

Soulbound Tokens (SBTs) represent identity on-chain. They can record education, employment, medical history, or even credit history, forming native Web3 identities.

The coolest part about SBTs is their ability to capture both on-chain and off-chain credentials. You could link your bank account and import your credit history directly into your crypto wallet.

This enables DeFi to penetrate the real-world economy by enabling:

-

Unsecured lending

-

Credit scoring, qualifying users for lower interest rates on future loans.

-

Portable KYC, eliminating repeated verification across platforms.

-

Human DAOs, potentially even voting in elections.

Is This Still DeFi?

This level of mass adoption may challenge decentralization, but self-custody remains unchanged.

ChainLinkGod wrote about how "financial institutions will continue serving as consumer touchpoints while increasingly using crypto on the backend."

According to him, the benefits of on-chain finance are clear:

-

Increased liquidity (larger buyer's market)

-

Greater composability (enabling new financial products)

-

Single source of truth (reducing reconciliation costs)

All of this happens while you retain full control over your assets.

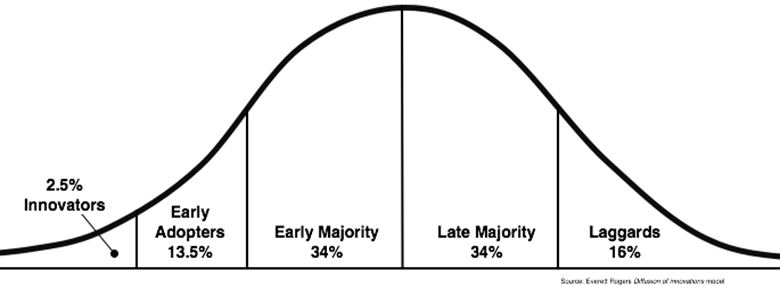

When Will We See This?

The diffusion of innovations theory suggests adoption occurs when people do something differently than before.

As innovators and early adopters, we need to show more people the benefits of DeFi, communicate the value of self-custody, and reduce dApp complexity.

The arrival of that moment depends on our efforts. I hope to see mass adoption of DeFi soon.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News