Bankless: Why We Believe ETH Has a 99% Chance to Outperform BTC?

TechFlow Selected TechFlow Selected

Bankless: Why We Believe ETH Has a 99% Chance to Outperform BTC?

Ethereum is generating more revenue and significantly strengthening its position in the competition with BTC. Does this mean ETH's market cap will eventually surpass BTC's?

Written by: Ryan Berckmans

Compiled by: TechFlow

The Merge is over. Ethereum's tokenomics have undergone a massive transformation, and ETH supply has significantly decreased.

Ethereum is now generating more revenue and has greatly improved its competitive standing against BTC.

So, does this mean ETH’s market cap will eventually surpass BTC’s?

Certainly, people like me who own ETH hope so—but beyond our personal financial interests, would this actually benefit the broader cryptocurrency ecosystem? What’s wrong with BTC being number one? Hasn’t it worked well so far? And if it’s good for crypto, why hasn’t it happened yet?

These questions are deeply intertwined, and perhaps best explored by diving into the details of BTC's returns.

Reliability Does Not Equal Investability

BTC is the most credible neutral asset. This is because the Bitcoin protocol is mature and unchanging, and proof-of-work substantially reduces risk through its simplicity and proven track record.

Over the years, it has withstood dozens of failed attempts by organizations to unilaterally modify Bitcoin’s core code or expand its node requirements. Regardless of Satoshi Nakamoto’s original intentions, BTC’s reliability has become a core intrinsic value proposition.

However, Bitcoin’s reliability does not mean the asset will retain or accumulate value in terms of purchasing power or fiat currency.

On the contrary, Bitcoin’s core design—being non-programmable and offering no value accrual to holders—combined with its mining cost structure, leads to severe value leakage.

This is why, for Bitcoin, reliability does not equate to investability.

With that context established, let’s begin understanding how BTC works by looking at its historical returns.

What happened in 2016?

From 2013 to 2016, if you bought low and sold high, BTC returned about 6x.

But if you bought BTC at the 2013 peak and sold in 2016, you made nothing—zero.

After 2016, things were completely different. If you bought BTC in 2016 and held until today, you earned 20x to 40x. Buying at the 2016 low and selling at the new 2021 highs? You made 130x.

One might protest, "Pre-2016 was the dark age of crypto—back then didn’t matter; we were just getting started."

Are you sure that explains everything?

What changed around 2016 that caused BTC to perform better in subsequent years? Did anything fundamentally change with Bitcoin before or after 2016 that created these massive returns?

In fact, Bitcoin itself did not change—after all, immutability is a feature of Bitcoin and part of its top-tier reliability.

Sure, the Lightning Network launched after 2016, but it has had almost no impact.

What else could have happened around 2016 to unlock Bitcoin’s potential? Or did BTC nurture something invisible that matured in 2016?

All such explanations fall short. The idea that Bitcoin evolved or unlocked potential around 2016 simply cannot be reconciled with the narratives and data we’ve observed over the past decade.

BTC Rode the Web3 Wave

So what actually happened?

In my view, the most factually consistent explanation with both historical narrative and data is that every major catalyst in the crypto market since 2016 has been driven by the promise or realization of Web3 applications—applications that Bitcoin does not support.

In 2016, a small project called Ethereum began gaining massive traction by striving to make public blockchains function as computers.

Up to now, BTC has merely been surfing the wave of genuinely useful innovations created by the Ethereum community (and a few others) during recent bull markets.

At this point, Bitcoiners or diversified crypto investors might reasonably object: “Wait—if BTC is just a bystander, why do investors buy it? BTC still commands about 38% dominance today.” “Are you joking? Do you think a $400 billion market cap is just a mistake?”

Yes, that’s exactly what I’m saying—and I’ll endeavor to prove it below.

This is precisely why BTC is an unsustainable investment, why ETH overtaking BTC in market cap is possible, and why this shift would benefit crypto overall—because it would remove an uninvestable asset from leadership in our industry.

Unsustainable Investment

Bitcoin fits the definition of an unsustainable investment.

If we closely examine Bitcoin’s use of proof-of-work, it becomes difficult to defend Bitcoin’s sustainability in terms of value preservation or accumulation.

Bitcoin’s fees go directly to miners, providing zero value accrual to BTC holders. This means BTC generates no revenue—especially considering the high costs of mining.

BTC’s annual inflation rate was around 2% before the 2024 halving. That sounds acceptable—what harm could 2% inflation cause?

The problem is, due to mining economics, inflation (issuance) in PoW directly consumes capital—the most direct drag on BTC’s valuation. Combined with thin spot liquidity, miner selling severely damages BTC’s market cap.

Over the medium term, miners must sell most of the BTC they earn because they spend up to $1 in hardware and energy costs to compete for $1 worth of BTC. This is a massive issue for BTC (and previously for ETH before yesterday’s Merge), because selling X% of supply harms market cap far more than X%.

According to some estimates, selling $1 of BTC could erase $5–$20 from its market cap.

The open secret in crypto is that you can’t sell more than a tiny fraction of total supply at the spot price—order books are thin, liquidity weak.

Therefore, not everyone can exit at today’s price—so by definition, miners are consuming scarce resources through constant selling.

That said, BTC miners may only sell 2% of total supply annually, but their net fiat inflows far exceed 2%. Given BTC’s low fees—all paid to miners—two critical implications, often overlooked by BTC holders, emerge:

1. On average, someone must purchase large amounts of BTC daily to keep prices stable. In 2021, approximately $46 million in daily net fiat inflow was required to maintain BTC’s parity. In other words: “I have this great investment for you—we just need $46 million in fresh money from others every day to avoid losing our principal…”

2. When a BTC investor earns 50%, 5x, or 40x returns, those profits come exclusively from new entrants. No meaningful fee revenue accrues to holders, no meaningful applications exist on Bitcoin, and due to mining costs, BTC’s price cannot stabilize itself. Therefore, by definition, anyone buying BTC at new highs cannot profit sustainably.

Social Imbalance

Who would intentionally buy an unsustainable long-term investment? Who recommends doing so? Last year, BTC reached a $3 trillion total crypto market cap with ~40% dominance—how did we get here?

To my knowledge, a few distinct types of buyers likely drove capital into BTC, each with their own rationale—and most unaware of the true risk profile they’re investing in. Below are some investor types:

1. Newcomers buying BTC. For example, seasoned hedge fund managers transitioning into Web3, long-term institutional investors, ultra-high-net-worth individuals, and retail investors. These newcomers arrive in Web3—statistically more during bull runs—excited, aware that crypto is novel and complex, and rationally allocate proportionally across a basket of top crypto assets.

“Proportional” is an investment term meaning “I’ll buy assets according to today’s market cap weights.” These newcomers are often the sacrificial lambs—the ones slaughtered due to BTC being an unsustainable investment.

2. Long-term holders buying BTC. These may be early crypto OGs or crypto VCs with greater connections and capital. They buy BTC because they truly lack—or don’t want to build—confidence in the direction of the space, and they don’t want to appear wrong. Worse, these individuals are often authorities who play a key role in pushing newcomers to invest in BTC.

3. Speculators buying BTC. They may sell entirely at the next new high. Often, these are the smartest, savviest, and/or hungriest among crypto OGs, VCs, and finance professionals transitioning into Web3. Yet they feel compelled—often for self-interest—to avoid controversy and actively promote Bitcoin.

They believe that if BTC crashes, it would mean massive losses for some of crypto’s largest and most powerful investors, potentially damaging the entire space and their portfolios.

4. Traders. They buy BTC and rotate profits into BTC as crypto’s de facto reserve currency. Traders simply follow trends—they know that in this era, BTC performs better in downturns and worse in rallies. With very short time horizons, they treat BTC as a safe base for riskier plays. In a way, traders are the most rational and/or least destructive of all BTC buyers.

5. BTC Natives. These are die-hard BTC fans who believe BTC is the most reliable monetary asset in human history. They not only believe in BTC’s top-tier reliability but also believe this reliability must inevitably translate into superior long-term investment performance and/or the best risk-adjusted crypto investment to date.

Among these five types of BTC buyers, only BTC natives might hold on after BTC dominance collapses. Overall, Bitcoin buyers are playing one of modern finance’s largest speculative games—and among them, only the speculators have even a vague sense of the game’s nature.

Admittedly, this categorization of BTC buyers is overly simplistic, but I find it useful. At this point, BTC natives and skeptics alike may feel emboldened:

“If you claim BTC as an investment vehicle is doomed to fail, then why hasn’t ETH already overtaken it?”

Because: numbers. That’s why.

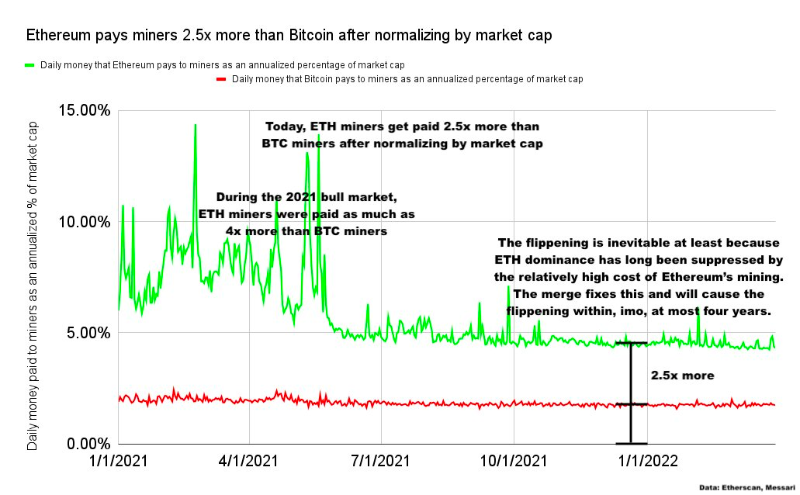

Historically, ETH miners were paid significantly more than BTC miners. If the two chains had swapped cost structures—if BTC miners earned what ETH miners did, and vice versa—or if The Merge had occurred two years earlier, I believe ETH’s market cap would already have surpassed BTC’s.

Let’s explore these numbers…

Standing on the Shoulders of a Heavy Giant

If miner selling matters—and it does, as shown above—then it’s significant that over recent years, ETH miners were paid 2.5x to over 4x more than BTC miners (normalized by market cap):

Last year, BTC miners earned $16.6 billion in rewards, while ETH miners earned $18.4 billion.

Conversely, if we swapped Bitcoin and Ethereum’s cost structures last year, ETH miners would have earned and sold ~$6 billion, while BTC miners would have earned and sold ~$50 billion.

This is a crucial point, so let me repeat: Last year, Ethereum miners earned and sold $1.8 billion more in ETH than Bitcoin miners sold in BTC. If we imagine reversing the cost structures between the two chains, in 2021 alone, BTC miners would have earned and sold ~$44 billion more in BTC than Ethereum miners did in ETH.

To illustrate: in 2021, Ethereum operated at extremely high costs relative to Bitcoin. Had the situation been reversed, Bitcoin would have required an additional ~$45.8 billion in net fiat inflow (i.e., new BTC buyers) to maintain both chains’ market caps at current levels, all else equal.

These enormous figures—especially ETH’s higher miner sell pressure relative to its market cap—are a key reason why the flippening hasn’t occurred yet.

No Eternal Emperor

What happens next?

Ethereum has now transitioned to PoS via The Merge, eliminating miner dumping. We are now on a path toward positive income, scaling with L2s, and Web3 is going global.

Ethereum has become a positive-sum, productive economy.

For the reasons outlined above, I believe ETH has a 99% chance of surpassing BTC in market cap over the coming years—the remaining 1% reserved for unknown unknowns, like aliens appearing and forcing us to adopt BTC as the sole global currency.

ETH’s profitability, low validation costs, explosive dApp growth, and the favorable environment fostered by credible neutrality will usher our industry into a post-BTC era.

The Fall of Rome

That day will be explosive and spectacular.

Of course, we might only briefly surpass BTC. But zooming out, this marks a one-way transition of BTC into the antique wing of crypto investing.

Unfortunately, crypto and Web3 investors may suffer heavy losses during BTC’s slow decline and violent collapse.

Today, the probability of overtaking is close to 50%.

As ETH slowly climbs against BTC, we’ll reach a tipping point—then, the flippening ratio will jump from 70% to 100%, or 80% to 120%, or whatever final outcome—marking the end of the BTC era.

Why This Is Good for Crypto: A Healthy New Era

I suspect that eventually, years from now, all of us—including most BTC holders today—will look back and realize how naive it was to believe BTC could remain first forever.

BTC’s fate will undergo a radical transformation, ultimately becoming a living fossil of the crypto world. Only after ETH takes the lead will the truly healthy era of cryptocurrency begin.

An eco-friendly era, lean cost structure, profit generation from valuable applications, Web3 becoming globally ubiquitous, Ethereum becoming the world’s settlement layer—a fair and level playing field for all of humanity.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News