5 Things You Need to Know About the FRAX Algorithmic Stablecoin

TechFlow Selected TechFlow Selected

5 Things You Need to Know About the FRAX Algorithmic Stablecoin

Is FRAX the new UST?

Written by: Ehsan Yazdanparast

Translated by: TechFlow Intern

Is FRAX the new UST?

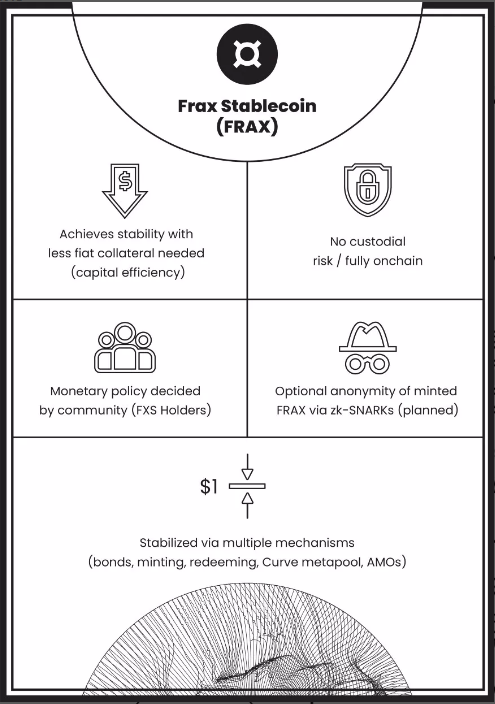

Frax is a fractional-algorithmic stablecoin. Frax’s stablecoin supply is partially backed by fiat-collateralized assets such as USD, while the remaining portion is algorithmically adjusted.

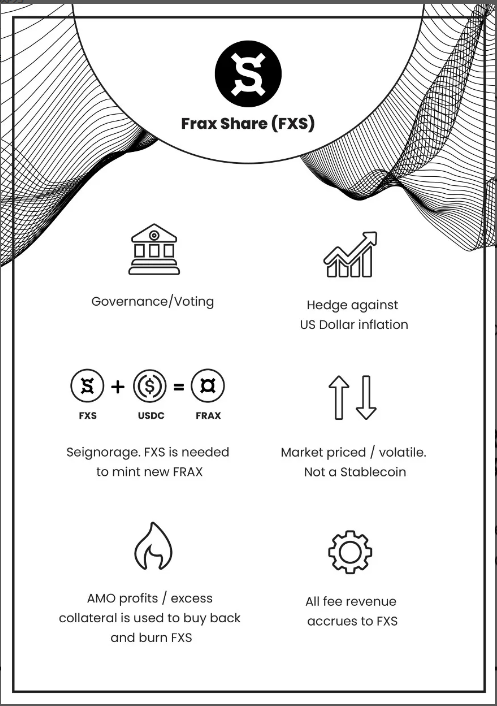

#1 — Frax Share (FXS)

The Frax Share token (FXS) is an unstable utility token within the protocol. It is designed to be volatile and holds governance rights and all system utilities.

Governance via FXS includes:

1. Adding/adjusting collateral pools.

2. Adjusting various fees (such as minting or redemption).

3. Refreshing the collateral ratio.

Beyond voluntary migration to new hard forks, no other governance actions are required—such as actively managing collateral or adding manually adjustable parameters.

In May 2020, the protocol allowed FXS holders to lock FXS tokens to generate veFXS and gain special upgrades, enhanced governance rights, and AMO profits.

The initial FXS supply was set at 100 million tokens, but due to FRAX being minted at higher algorithmic ratios, the circulating supply may become deflationary. The protocol is designed so that as demand for FRAX grows, the FXS supply becomes largely deflationary.

#2 — Fractional-Algorithmic Stablecoin Model

Fully collateralized stablecoins face custody risks or require on-chain over-collateralization, while purely algorithmic stablecoins are difficult to bootstrap, grow slowly, and often experience extreme volatility. For these reasons, FRAX adopted a fractional-algorithmic model—meaning it is partially backed by fiat currency and partially stabilized algorithmically.

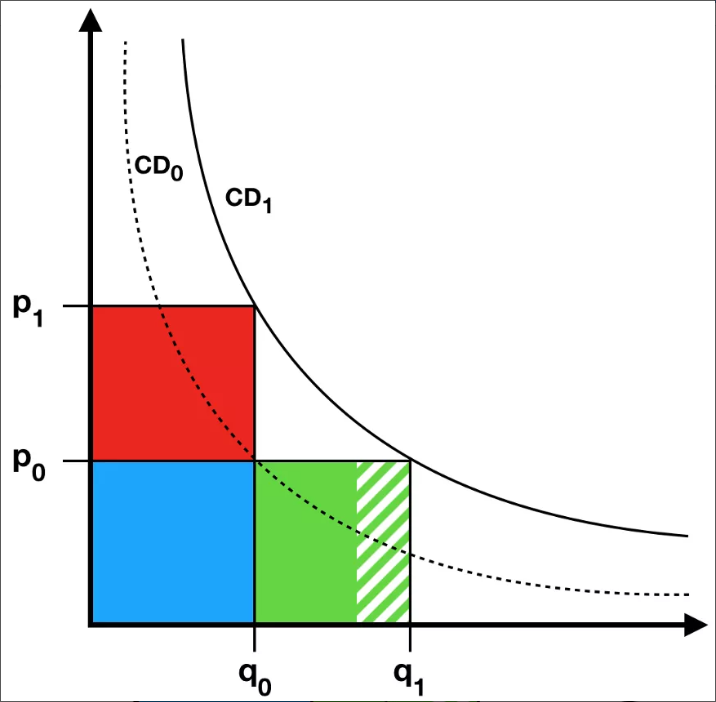

The value of the FXS token depends on the demand for FRAX. The market cap of FXS represents the sum of the non-collateralized value of the FRAX market cap. That is, the total area under the curve of all past and future shaded regions, as shown in the figure below.

At genesis, FRAX was 100% collateralized, meaning minting FRAX only required depositing collateral into the minting contract.

In the fractional-algorithmic phase, minting FRAX requires depositing a proportional amount of collateral and burning a corresponding proportion of Frax Shares (FXS).

For example:

-

1. If the market price of FRAX is above the $1 target: At a 98% collateral ratio, minting each FRAX requires $0.98 in collateral and burning $0.02 worth of FXS. At a 97% collateral ratio, each FRAX requires $0.97 in collateral and burning $0.03 worth of FXS, and so on.

-

2. If the market price of FRAX is below the $1 range: At a 98% collateral ratio, each FRAX can be redeemed for $0.98 in collateral and $0.02 worth of newly minted FXS. At a 97% collateral ratio, each FRAX can be redeemed for $0.97 in collateral and $0.03 worth of newly minted FXS.

#3 — Collateral Ratio and Oracles

The collateral ratio refresh function in the protocol can be called by any user once per hour. If the price of FRAX is above or below $1, this function adjusts the collateral ratio in steps of 0.25%.

-

1. When FRAX is above $1, the function decreases the collateral ratio by one level.

-

2. When FRAX is below $1, the function increases the collateral ratio by one level.

The refresh rate and step parameters can both be adjusted through governance (FXS).

Prices of FRAX, FXS, and collateral are calculated using time-weighted average prices from Uniswap pairs and Chainlink oracle ETH:USD data.

Chainlink oracles allow the protocol to obtain the true USD price rather than relying solely on the average price from stablecoin pools on Uniswap. This enables FRAX to remain stable relative to the USD itself, offering greater resilience compared to merely using a weighted average of existing stablecoins.

In future protocol updates, the price feed for collateral could be deprecated, and the minting process could shift to an auction-based system, reducing reliance on price data and further decentralizing the protocol.

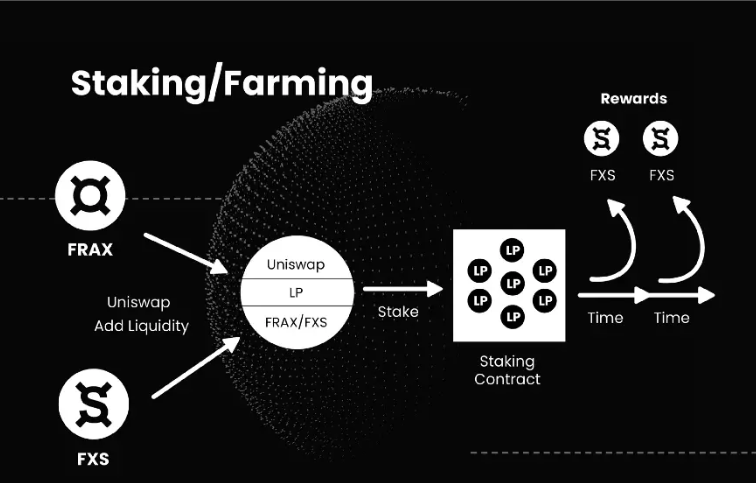

#4 — Liquidity Programs and Staking

Users who deposit Uniswap LP tokens into incentivized pairs receive FXS rewards, which helps increase liquidity for those token pairs on Uniswap. Each incentivized pair has its own emission rate, and the total FXS rewards across all incentivized pairs were initially emitted at a base rate of 18M FXS in the first year. As FRAX becomes more algorithmic, the FXS emission rate across all pools doubled.

-

1. Collateral Ratio Boost (deprecated on April 17, 2021): Each pool’s emission rate was multiplied by a CR Boost constant inversely proportional to the collateral ratio. This meant that as FRAX became more algorithmic, the FXS emission rate for all pools increased. The CR Boost constant was capped at a 2x multiplier—meaning if FRAX became fully algorithmic (0% collateral), the FXS emission rate would double.

-

2. Time-Locked Staking: Any LP can lock their LP tokens for 3 years. LP shares benefit from two multiplicative boost factors: time lock and collateral ratio. The collateral ratio boost applies to the base FXS emission rate, increasing overall FXS distribution across the system. The time-lock boost applies to individual stakes proportionally among all stakers in the pool, making it a zero-sum game when someone gains a boost from a time-locked position.

-

3. veFXS Boost: veFXS holders receive additional weight multipliers when farming.

#5 — Algorithmic Market Operations Controller (AMO)

Frax v2 expanded the concept of fractional-algorithmic stability by introducing the "Algorithmic Market Operations Controller" (AMO).

An AMO module is an autonomous contract that can execute arbitrary monetary policies as long as it does not alter FRAX’s peg. This means AMO controllers can perform algorithmic open-market operations without minting FRAX out of thin air and breaking the peg. This keeps FRAX’s base-layer stability mechanism pure and unchanged—a core feature that has made the protocol stand out.

Thus, each AMO can be seen as a monetary Lego block for central banking. Each AMO has four attributes:

-

1. De-staking: The strategy component that reduces the collateral ratio (CR).

-

2. Market Operations: The equilibrium part of the strategy that maintains the current CR.

-

3. Re-staking: The strategy component that increases the CR.

-

4. FXS1559: Formal accounting for the AMO balance sheet, precisely defining how much FXS can be burned when profits exceed the target CR.

AMOs make FRAX one of the most powerful stablecoin protocols by creating maximum flexibility and opportunity without altering the fundamental stability mechanisms that have made FRAX a leader in the algorithmic stablecoin space. The AMO module opens up a modular design space, enabling continuous upgrades and improvements without compromising elegant design, composability, or technical sophistication. Finally, since AMO is a complete “black-box mechanism,” anyone can propose, build, and create AMOs, which can then be deployed through governance as long as they adhere to the above specifications.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News