When Crypto "Hides" in Traditional Finance: Prediction Markets, Stablecoins, and Tokenized Stocks—How to Go Mainstream?

TechFlow Selected TechFlow Selected

When Crypto "Hides" in Traditional Finance: Prediction Markets, Stablecoins, and Tokenized Stocks—How to Go Mainstream?

It is impossible to make everyone actively enter Web3, but on-chain capabilities can be gradually embedded into familiar financial behaviors such as prediction, payment, and stocks.

Written by: imToken

For a long time, when the crypto industry talked about "mass adoption," it usually pointed to several relatively familiar metrics:

For example, how many people hold Bitcoin, how many addresses interact with on-chain protocols, and how many users have started using wallets, exchanges, and DeFi.

Behind this lies a relatively linear assumption, which is that ordinary users need to first understand Crypto, then purchase crypto assets, create wallets, and finally gradually enter the on-chain world.

But recent changes may be reversing this path. Users do not necessarily need to understand blockchain before accessing crypto infrastructure; instead, existing demands such as prediction markets, cross-border transfers, and stock trading are actively absorbing crypto technology. While these appear to belong to three different sectors and penetration is not happening along the same path, they point to the same change behind the scenes:

Crypto is transforming from a new financial system that users need to actively enter into infrastructure that traditional finance and mass-market applications can directly call upon.

I. Prediction Markets: From On-Chain Event Trading to Probability Pricing Tools

As everyone knows, prediction markets are not a new concept.

Especially in the crypto world, early in Ethereum's development, the prediction market Augur was the first DApp on Ethereum, which initially verified that any event with objectively verifiable results could be converted into an on-chain contract, and through the buying and selling of real funds, project the market's judgment on the future.

However, for a long time thereafter, prediction markets were simply summarized as "on-chain gambling" and did not truly break out of the crypto-native circle. Early users of platforms like Polymarket indeed mainly came from the crypto-native group familiar with wallets, stablecoins, and on-chain transactions:

On one hand, the usage thresholds of wallets, stablecoins, and on-chain transactions limited ordinary user participation; on the other hand, even though Polymarket once broke through with events like the US election, its core participants remained mainly traders familiar with Crypto.

But the 2026 USA/Canada/Mexico World Cup provides a more mass-market observation window for prediction markets (Further reading: "World Cup Carnival, Prediction Markets on the Table: How Polymarket and Others Tear Open the Mass Market?").

Compared to monetary policy, economic data, and political elections, football matches require almost no extra knowledge education; who will advance from the group stage, which team will enter the top four, whether a certain player can become the top scorer—these are questions fans discuss every day anyway.

What prediction markets do is simply convert these scattered opinions into a price that changes in real time. This is also why it is said that for prediction markets to truly break through, changes in the regulatory environment alone are not enough; they also need a sufficiently large and intuitive public event, and the World Cup happens to meet this condition.

Many of Crypto's past breakout moments often occurred when "high cognitive threshold technology" combined with "low cognitive threshold scenarios." For example, NFTs once broke through because they bound on-chain assets with avatars, art, and community identity; Memes were able to spread quickly because they compressed complex financial behaviors into simple emotions and cultural symbols.

Similarly, the entry point for prediction markets to reach wider users is not necessarily macroeconomic data or complex political contracts, but more likely scenarios like sports, entertainment, and events that the public is already willing to discuss.

The uniqueness of the World Cup lies in the fact that it naturally possesses three conditions.

- First, it has broad global consensus. Even if not a hardcore fan, one can understand basic questions like who wins or loses, who advances, and who wins the championship.

- Second, it has a high-frequency information flow. Pre-match lineups, player status, injury updates, tactical changes, and match progress will continuously change market expectations.

- Third, it has strong social attributes. Watching games is not an isolated behavior itself, but is accompanied by group chats, shares, discussions, arguments, and emotional resonance.

At the same time, the competitive boundaries of prediction markets are also continuously expanding. Especially recently, it is clearly no longer limited to vertical platforms like Kalshi and Polymarket, but is increasingly being integrated into traditional brokerages, crypto trading platforms, and even media products.

The reason is not complex. Although traditional financial markets already have many risk pricing tools such as options, futures, and interest rate swaps, these products usually have a high understanding threshold, and ordinary users find it difficult to read market judgments directly from prices, whereas prediction markets compress complex problems into a more intuitive probability.

This is also the key for prediction markets to potentially enter traditional financial infrastructure; what it provides is not just another way of betting, but a low-threshold, real-time updated expectation pricing tool.

Of course, this path is still accompanied by obvious controversies.

How events should be defined and settled, whether insiders can participate, whether financial event contracts constitute insider trading, and whether sports contracts should be subject to federal derivatives regulation or state gambling regulation are currently not fully clear. As the market scale expands, some Wall Street institutions have also begun to restrict employees from participating in prediction market transactions involving economic data and corporate events.

But in any case, the process of prediction markets gaining mainstream recognition is also the process of it gradually transforming from an "open event trading experiment" into financial market infrastructure.

II. Stablecoins: From Crypto Assets to Payment and Settlement Infrastructure

If prediction markets are bringing a crypto-native product into the mainstream, then stablecoins are taking another path; they are gradually hiding behind traditional payment products.

For most crypto users, stablecoins have long served as a medium of exchange. Users buy and sell other tokens with USDT or USDC, transfer funds between different exchanges, or put them into DeFi protocols to earn yields. Therefore, issuance scale has long been seen as the main indicator measuring stablecoin competitiveness.

But entering the next stage, the focus of stablecoin competition may no longer be just on-chain volume, but who can complete compliance positioning earlier and dive deeper into real scenarios such as payments, clearing, and cross-border transfers.

One of the recently highly discussed cases is Open Standard launching Open USD, participated by over 140 payment, banking, technology, and crypto enterprises.

Unlike the traditional model where reserve yields are mainly held by a single issuing institution, Open USD allows partner enterprises to mint and redeem for free, and plans to distribute income generated from reserves to partners who drive its usage after deducting management fees.

Relevant introductions from Visa and Stripe also define OUSD as shared infrastructure for global capital flow. What is truly worth paying attention to in this design is not that another USD stablecoin has been added to the market, but that it attempts to adjust the long-standing profit distribution method of stablecoins—in the past, issuers usually could obtain most of the yields generated from reserve assets, but wallets, exchanges, payment companies, and fintech platforms often bore the costs of user acquisition, product integration, and actual distribution.

If reserve yields can be further tilted towards channels and usage scenarios, the competition logic of stablecoins will also change accordingly, which also explains why the entry of institutions like Stripe, Visa, Mastercard, and Zelle is more worth paying attention to than simply adding another on-chain asset.

Ultimately, stablecoins are transforming from a Crypto product that users need to actively hold and manage into a capital flow component that traditional enterprises can directly call upon. What users see may be cross-border remittances, merchant settlements, corporate payments, payroll distribution, or a payment card, but what is used in the backend may be stablecoins and public chain settlement networks. Users may already be using the settlement capabilities it provides without even knowing the existence of stablecoins.

At the same time, some stablecoin products lacking actual distribution channels and usage scenarios are also exiting. This further illustrates that completing issuance does not mean stablecoins naturally possess value.

When underlying technology gradually becomes standardized, the real barriers will come more from licensing and regulatory adaptation capabilities, and whether it can be embedded into a business scenario that continuously generates transaction demand.

This also means that what stablecoins ultimately need to compete with in the future may not just be another stablecoin, but possibly bank card networks, cross-border remittance systems, bank deposits, and corporate treasury infrastructure.

III. Tokenized Stocks: Traditional Assets Begin to Enter On-Chain Accounts

Compared to prediction markets and stablecoins, the convergence direction presented by tokenized stocks is more direct.

It is not about introducing a crypto product to traditional users, but moving stocks, ETFs, funds, and other traditional assets into accounts originally used mainly for storing and trading crypto assets.

In the past half year, almost all head crypto trading platforms have been rushing to enter the market; at the same time, NYSE parent company ICE also made a strategic investment in OKX, and both parties plan to cooperate around US regulated crypto futures, ICE market products, and NYSE-related tokenized stocks. As of the time of writing, OKX has just planned to launch tokenized US stock products.

From a market structure perspective, this cooperation has strong symbolic significance, after all, in the past it was crypto exchanges attempting to provide users with stock price exposure through synthetic assets, perpetual contracts, or third-party issuers, whereas now traditional exchange operators are directly participating in product design, price data, compliance, and on-chain market infrastructure construction.

At the user-facing entry point, similar changes have already begun to occur; besides vertical applications, from trading platforms to wallets to on-chain DEXs, from Robinhood to Interactive Brokers, everyone is trying to expand into comprehensive financial accounts capable of holding crypto assets, stocks, and even commodity trading simultaneously.

However, tokenized stocks are also the most prone to conceptual confusion.

A token with Apple, Nvidia, or Tesla in its name does not necessarily equate to users directly holding common stock of the corresponding company, after all, different products may represent direct ownership of real stocks, beneficial equity formed after stocks are held by an SPV, debt instruments promised by issuers for redemption, or simply derivatives tracking stock prices.

These models may have significant differences in dividends, voting rights, redemption rights, bankruptcy isolation, and investor protection. Even if tokens circulate on public chains, the legal relationships determining users' ultimate rights still often exist in off-chain issuing entities, custodial institutions, and legal contracts; currently, most RWA systems also adopt hybrid architectures.

Therefore, tokenization does not automatically equal liquidity, nor does it automatically mean users possess exactly the same rights as traditional shareholders, but these restrictions do not prevent tokenized stocks from becoming an important entry point.

Once compliance, custody, and shareholder rights issues are gradually resolved, stocks will no longer exist only in brokerage accounts. They can be in the same on-chain account as stablecoins, can be split into smaller units, can be traded in different regions and time periods, and may also be further used for collateral, lending, automated investment, and programmatic asset allocation.

At that time, what wallets and trading platforms compete for will no longer be just the storage and trading of crypto assets, but who can become the unified entry point for users to manage global assets.

Concluding Remarks

To speak realistically, this is a bit like when Zhang Sanfeng taught Zhang Wuji Tai Chi in "The Heaven Sword and Dragon Saber," repeatedly asking how much he remembered, until Zhang Wuji answered that he had forgotten it all, only then was he considered to have truly grasped the essence.

Crypto mainstream adoption may also undergo a similar process—the mark of true maturity is not everyone remembering the concepts of blockchain, wallets, and stablecoins, but users gradually becoming unaware of the existence of these technologies, letting everything about Crypto gradually disappear behind the products.

Of course, if examined closely, from prediction markets, stablecoins to tokenized stocks, the ways crypto technology enters traditional finance are not exactly the same:

- Prediction markets bring the product logic formed in the crypto world into the mass market, converting events and uncertainty into probabilities that can be traded in real time;

- Stablecoins embed on-chain settlement capabilities into payments, remittances, and corporate capital flows, allowing users to use new capital networks without needing to understand blockchain;

- Tokenized stocks bring traditional assets into on-chain accounts, making wallets, exchanges, and public chains gradually become new issuance, trading, and settlement channels for traditional securities;

They correspond to penetration at the product, capital, and asset levels respectively. For the industry, this may mean a new path to mass adoption, which is no longer requiring every user to become a Crypto user first, but letting on-chain technology actively adapt to financial demands users are already familiar with.

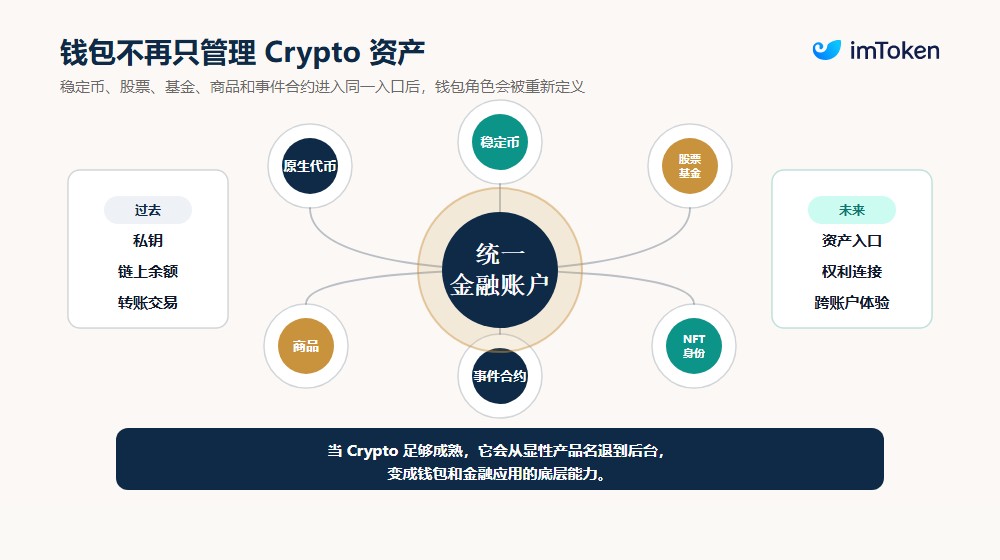

Correspondingly, the role of wallets will also change.

After all, when wallets no longer contain only native tokens and NFTs, but gradually include stablecoins, stocks, funds, commodities, and event contracts, what they need to handle is not just private keys and on-chain balances, but also how to lower the usage threshold for different assets and better connect on-chain and off-chain account systems.

Just imagine, when a person can use a wallet to instantly remit money to overseas friends and relatives, trade the probability of an event occurring on the wallet, or when purchasing a small portion of US stocks, they may not necessarily think they are "using Crypto."

It is precisely under this state where it no longer needs to be repeatedly emphasized that crypto technology can truly move from a relatively independent niche market into the broader financial and commercial world.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News