Bitget UEX Daily | Rocket Lab Plans to Acquire Iridium Communications; Optical Communication, Storage, and Space Sectors Rebound Strongly; Nike, Constellation Brands Report Earnings After Hours

TechFlow Selected TechFlow Selected

Bitget UEX Daily | Rocket Lab Plans to Acquire Iridium Communications; Optical Communication, Storage, and Space Sectors Rebound Strongly; Nike, Constellation Brands Report Earnings After Hours

The overall consensus is: the macro environment is showing marginal improvement, but caution is warranted regarding technical pullback risks, and a balanced allocation between growth and defensive assets is recommended.

I. Hot News

Fed Updates

Supreme Court Upholds Fed Independence, Trump Vows to Continue Push

The U.S. Supreme Court ruled 5-4 to block Trump's attempt to dismiss Fed Governor Cook. This move is seen as a significant check on the President's attack on the independence of the world's most important central bank. The court had previously limited presidential emergency tariff powers, further reinforcing central bank policy autonomy this time. However, the same ruling also cleared the obstacle for Trump to dismiss Federal Trade Commission (FTC) members without cause, showing the White House has expanded control over some independent regulatory agencies.

Trump subsequently stated that the Supreme Court remanded the case to the lower court based only on procedural grounds and he would take immediate action to ensure "misconducters" no longer participate in major decisions. Market interpretation suggests this case reduces the risk of sudden Fed policy changes in the short term, benefiting long-term interest rate expectation stability, but also highlights the ongoing game between executive and judicial power boundaries.

International Commodities

Trump Announces US-Iran Doha Talks Held Today, Iran Emphasizes Focus on Implementing Memorandum of Understanding

U.S. President Trump stated on the afternoon of June 29 local time that today (June 30) the US and Iran will hold talks in Doha, the capital of Qatar, and US representatives "may have already departed or are preparing to depart." Trump called the talks "possibly important or possibly not important," but emphasized that the US "has won militarily," "oil prices have fallen," and Iran has agreed not to possess nuclear weapons. The White House revealed that Presidential Envoys Witkoff and Jared Kushner will participate.

The Iranian Foreign Ministry spokesperson clearly stated that Iran will not hold negotiations with the US at any level in the coming days; the technical delegation sent to Doha this week aims to follow up on the implementation of the memorandum of understanding (including Oil export licenses and the release of frozen assets), rather than initiating final agreement negotiations. Israeli Defense Minister Katz stated that the IDF is prepared for independent military action against Iran but will not interfere with Trump's actions for now.

Market Impact: Geopolitical easing expectations heat up, short-term beneficial for risk assets, oil prices under pressure to fall back; if negotiations make substantial progress, it will further weaken safe-haven demand.

Macroeconomic Policy

SpaceX and Google Drive Record US Stock Issuance in First Half, BofA Warns S&P May See Three-Wave Correction

Bloomberg data shows that as of June 26, total US IPO and stock issuance reached $251 billion, exceeding the record from the first half of 2021. SpaceX and Google's record issuance activities were the main drivers, with AI hyperscalers continuing to seek funds for infrastructure such as data centers.

Bank of America Technology Research Head Paul Ziana warned that the S&P 500 has risen nearly 17% since the March low, but signs of fatigue have appeared since the June 2 high, possibly correcting to 6850 points (about 7.6% drop from current levels). He suggested investors hedge against further rebounds and take a defensive stance in July-September. The rebound after the US-Iran ceasefire has shown volatility, prices are "overstretched," and momentum deteriorating.

II. Market Review

Commodities & Forex Performance

- Spot Gold: 3972 USD/oz, -1.05%

- Spot Silver: 56.9 USD/oz, -2.4%

- WTI Crude: 70.22 USD/bbl, -0.7%

- Brent Crude: 73.52 USD/bbl, -0.5%

- US Dollar Index (DXY): 101.25, -0.11%

Driver Analysis: The start of US-Iran Doha talks and Trump's statement "oil prices have fallen" reinforced expectations of phased geopolitical risk easing, directly suppressing energy prices. Gold and silver fell slightly in an environment of rising risk appetite but remained in a high range, showing long-term inflation and central bank gold buying demand support remains. The US dollar index weakened slightly, reflecting the market's positive interpretation of the maintenance of Fed independence, reducing interest rate hike expectation disturbances in the short term. Overall, asset correlation logic is clear: geopolitical easing → risk assets up → USD and safe-haven commodities under pressure. In the short term, if negotiations proceed smoothly, oil price downside space may open further, but any negotiation breakdown signal will quickly reverse this logic.

Cryptocurrency Performance

- BTC: 59846 USD, +0.31%

- ETH: 1594 USD, +1.33%

- Total Crypto Market Cap: Approx 2.16 trillion USD, +0.8%

- Market Liquidation Situation: 24h total liquidation approx 297 million USD, short liquidation 158 million USD

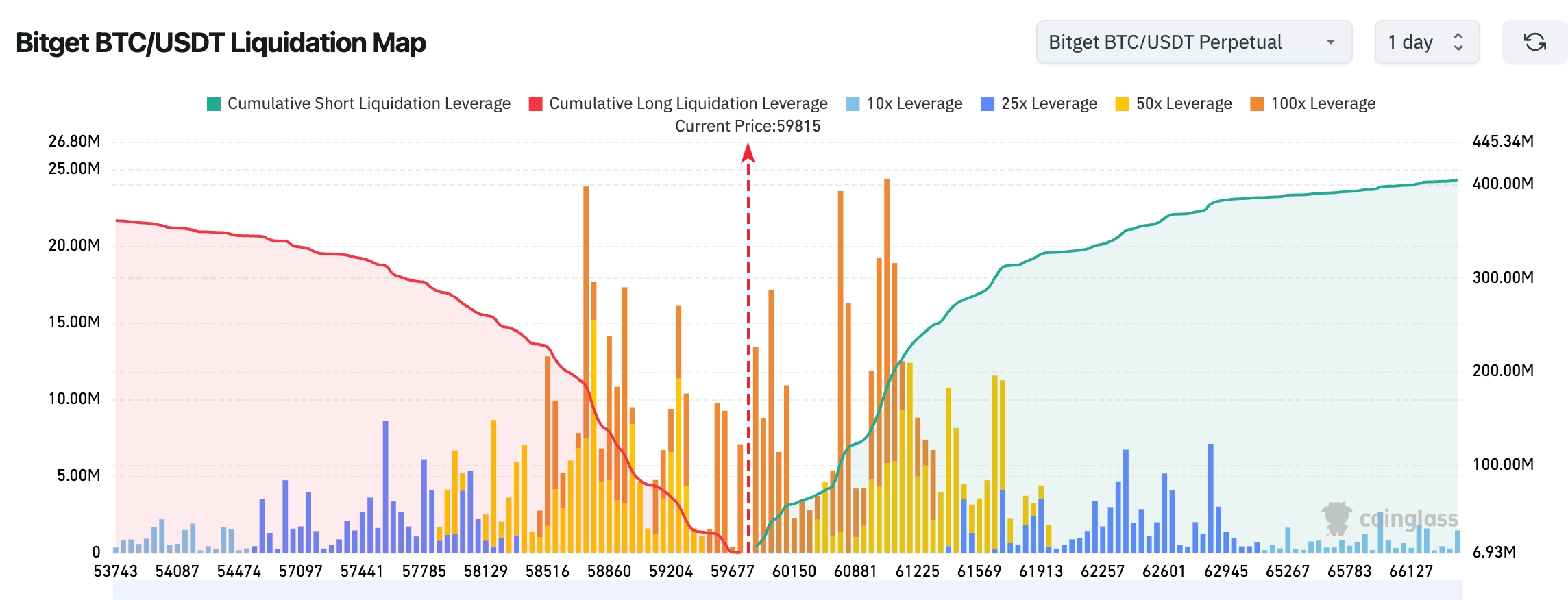

- Bitget BTC/USDT Liquidation Map: Current BTC price approx 59,815 USD, large short liquidation positions clustered in the 60,800–61,600 USD range above. If holding above 60k USD and continuing to advance, it may trigger concentrated short covering, pushing price acceleration upward. Below long liquidation mainly concentrated in 58,500–59,300 USD, above short liquidation scale significantly larger than below long liquidation, short-term market more concerned about risk of triggering short covering after upward breakthrough.

- Spot ETF Net Inflow/Outflow: BTC Spot ETF net inflow approx $65 million yesterday

Driver Analysis: Driven by the strength of US stock tech and space sectors, the crypto market shows signs of warming risk appetite, with BTC and ETH rebounding simultaneously. ETF fund flows remain hovering at low levels but have stabilized from previous consecutive days of large outflows, showing institutional sentiment repair. Leverage liquidation data is mild, indicating current leverage levels are not high, liquidations mainly come from long profit-taking rather than systemic short squeeze. Technically, BTC found support near 60000 USD, ETH relative strength reflects market preference for Ethereum ecosystem and institutional adoption expectations. Macro level, Fed independence maintenance reduced policy uncertainty, coupled with US-Iran easing signals, jointly constitute short-term beneficial environment. But need to guard against BofA and other institutions' warning on US stock correction, if risk assets overall correct, crypto may face synchronous pressure. Overall trend bullish, but divergence obvious, ETH performs better under AI and institutional narrative support.

US Stock Index Performance

- Dow: Approx 52300 points (+0.59%)

- S&P 500: Approx 7430 points (+1.18%)

- Nasdaq: Surged (+2.07%)

Tech Giants Dynamics

- NVDA: 194.63 USD (+1.5%)

- AAPL: 281.74 USD (-0.7%)

- MSFT: 368.57 USD (-1.2%)

- GOOGL: 353.50 USD (+4.8%)

- AMZN: 240.12 USD (+3.2%)

- META: 562.60 USD (+2.24%)

- TSLA: 411.84 USD (+8.46%)

- MU: 1,145.28 USD (+1.14%)

- SPCX: 158.52 USD (+3.5%)

Performance Summary and Driver Analysis: Tech giants overall followed Nasdaq strong rebound, but internal divergence appeared. Tesla and Google led gains, the former benefited from comprehensive market risk appetite recovery, the latter may have AI search and cloud business catalysts. Nvidia gains relatively mild, reflecting previous high valuation pressure and HBM supply concerns remain. Amazon and Meta moderate, showing advertising and e-commerce recovery steady but lacking better-than-expected catalysts. Core divergence lies in: AI infrastructure and commercial space theme (SpaceX related concepts) gained fund favor, while pure consumption or traditional tech stocks lagged relatively. Futu Morning Brief mentioned SpaceX and Google issuance boom, further reinforced market long-term allocation willingness for AI and space economy, avoided "one-size-fits-all" interpretation.

Crypto Market Stock Contract Overview

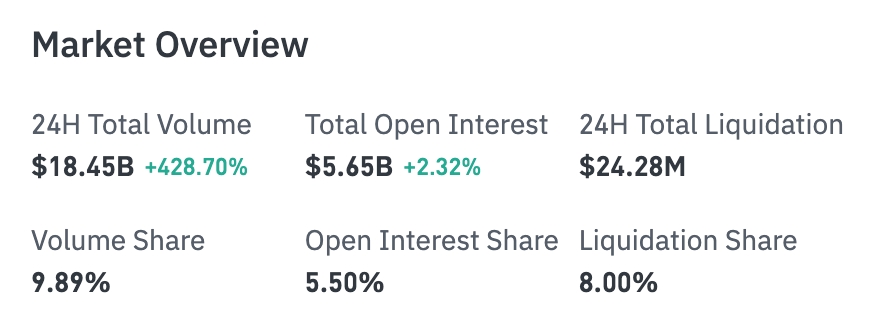

- 24H Total Turnover: 18.457 billion USD (+428.80%)

- Total Open Interest (OI): 5.649 billion USD (+2.39%)

- 24H Total Liquidation: 24.2758 million USD

- Turnover Share: 9.89%

- OI Share: 5.50%

- Liquidation Share: 8.00%

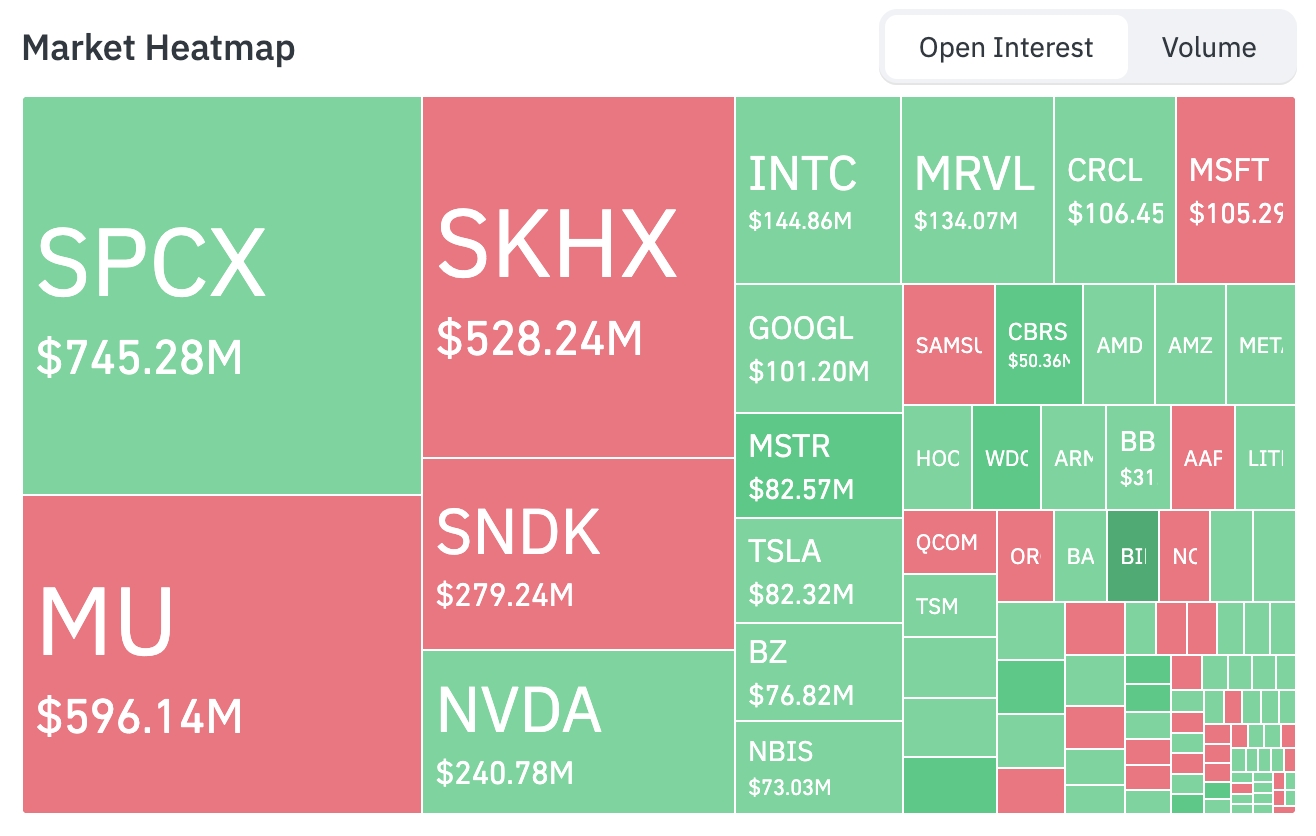

Position Heatmap

- SPCX Position 746 million USD.

- MU Position 597 million USD.

- SKHX Position 530 million USD.

- SNDK Position 280 million USD.

- NVDA Position 241 million USD.

- INTC Position 145 million USD.

- MRVL Position 134 million USD.

- CRCL Position 106 million USD.

- MSFT Position 105 million USD.

- GOOGL Position 101 million USD.

Stock contract market 24-hour turnover surged 428.80% to 18.457 billion USD, total open interest synchronized growth 2.39%, market trading activity significantly improved.

Positions still concentrated in SpaceX concept, AI computing power and semiconductor related targets, among which SPCX, MU, SKHX, SNDK, NVDA occupy market core positions, funds continue to focus on AI industry chain.

Sector Movement Observation

Space Concept Sector Surged (Representative stock IRDM up over 25%, RKLB up nearly 16%)

- Representative Stocks: Rocket Lab (RKLB) +16%, Iridium (IRDM) +25%

- Drivers: Rocket Lab announced acquisition of Iridium Communications via cash plus stock, total transaction value approx 8 billion USD, becoming one of the largest integrations in commercial space field in recent years. Market optimistic about satellite communication and launch capability synergy, coupled with overall risk appetite recovery.

Storage Concept Sector Rose (Representative stock WDC up over 11%)

- Representative Stocks: Western Digital (WDC) +11%, Seagate +8%

- Drivers: Semiconductor and AI data center storage demand expectations steady, coupled with US stock overall rebound sentiment.

Optical Communication Sector Rose Together (Representative stock ALAB up over 16%)

- Representative Stocks: Astera Labs (ALAB) +16%, Corning +16%

- Drivers: AI infrastructure capital expenditure continues, data center optical modules and connection demand robust.

III. In-depth Interpretation of US Stock Individuals

1. Rocket Lab (RKLB) - Announces Acquisition of Iridium Communications

Event Overview: Rocket Lab announced on Monday it will acquire satellite communication service provider Iridium Communications via cash plus stock, total transaction value approx 8 billion USD. This is one of the largest integration actions in commercial space field in recent years. According to agreement, Iridium shareholders will receive 27 USD cash per share plus Rocket Lab stock.

Market Interpretation: Institutions generally believe this acquisition will significantly enhance Rocket Lab's satellite communication and launch integration capabilities, expanding its competitiveness in low-orbit satellite constellation market. Combined with space economy boom pushed by head players like SpaceX, market remains optimistic about commercial space long-term growth prospects, but also concerns integration execution risks and valuation digestion pressure.

Investment Implications: Short-term event drive obvious, long-term bullish on aerospace industry chain integration and government/commercial order landing, suggest following up on subsequent execution progress and order landing situation.

2. Tesla(TSLA) - Excess Returns Under Risk Appetite Recovery

Event Overview: Under macro background of US-Iran geopolitical easing and Fed independence maintenance, Tesla stock price surged over 8%, leading tech giants. Market did not appear company-specific major negative or positive, gain mainly comes from overall risk asset sentiment repair.

Market Interpretation: Institution views diverged, one part believes Tesla as high beta tech growth stock has largest elasticity when risk appetite warms; another part points out its valuation still at high level, needs to rely on Robotaxi, energy or AI robot etc. long-term narrative realization. Short-term fund flow shows growth style dominant.

Investment Implications: Suitable for investors with higher risk appetite to participate in thematic rebound, but need to guard against correction risk, focus on company second half product and policy catalysts.

3. Alphabet(GOOGL) - AI Search and Cloud Business Dual Wheel Drive

Event Overview: Google stock price rose nearly 5%, outstanding performance among tech giants. Market associates it with AI infrastructure continuous investment and search business AI upgrade expectations.

Market Interpretation: Institutions bullish on Google's long-term competitiveness under AI search (Gemini) and cloud service (Google Cloud) dual wheel drive, especially in AI hyperscalers capital expenditure wave, cloud business growth certainty relatively high. Some views believe its relative to Nvidia's "infrastructure + application" dual attributes make it more defensive and offensive balance in current environment.

Investment Implications: One of AI theme core targets, suitable for medium-long term allocation, short-term can focus on search advertising recovery data and cloud revenue growth rate.

IV. Market & Project Dynamics

1. Strategy announces launch of digital credit capital framework, and authorizes 2 billion USD stock repurchase plan, to strengthen capital structure and support Bitcoin monetization strategy.

2. Tether and crypto lending platform Ledn reach cooperation, launch interest-free loan product fully supported by Tether Gold (XAUT), expanding physical asset and stablecoin combination scenarios.

3. BlackRock's corporate investment and portfolio management platform Aladdin will include Ethena stablecoin USDe into its supported crypto asset list, and provide 100 million USD liquidity tool via Securitize to serve BlackRock's BUIDL fund. New arrangement allows qualified BUIDL customers to exchange BUIDL for USDC, USDtb etc. stablecoins during OTC time and can exchange back to BUIDL, to enhance interoperability between on-chain US treasury fund and stablecoins.

4. GameStop committed last Friday to continue advancing approx 56 billion USD cash plus stock acquisition offer for eBay, although eBay board previously rejected the proposal. GameStop CEO Ryan Cohen proposed this acquisition scheme in May, stating merged company will more powerfully challenge Amazon, and expressed intention to operate new entity.

5. According to SemiAnalysis analysis, US latest four economic data affected by one-off factors obviously: Q1 GDP revised up from 1.6% to 2.1% mainly comes from import revision down, while real domestic demand growth revised down to 1.7%. May personal income month-on-month +0.7%, among which approx 59.6 billion USD is one-off agricultural disaster subsidy; PCE inflation 4.1% almost completely driven by energy, and oil prices June already fell approx 40% compared to April peak. Tariffs lifted goods inflation to approx 4.8%, constituting one-off price level shock rather than continuous inflation. Outside noise, AI related capital expenditure became main substantive drive, Q1 equipment, software and IP contribution to GDP growth approx 1.55 percentage points, is resident consumption contribution approx 4 times.

V. Today's Market Calendar

Data Release Schedule

Important Event Preview

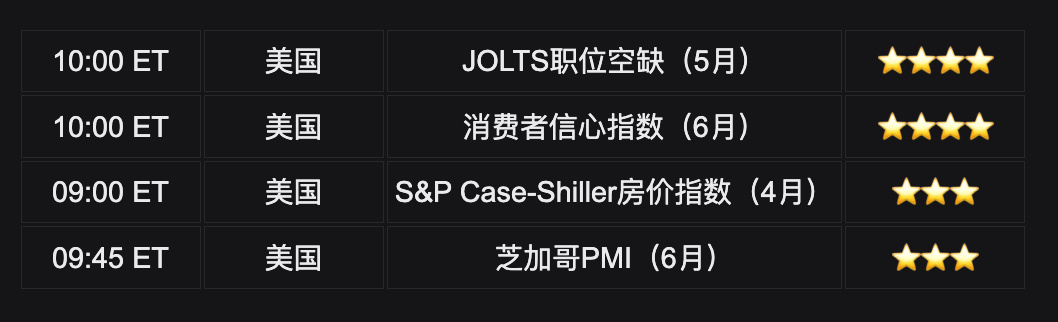

June 30 (Tuesday)

- US June Chicago PMI, US May JOLTs Job Openings, US June Conference Board Consumer Confidence Index announced;

- Nike (NKE), Constellation Brands (STZ) announce earnings after hours; ★★ (Nike earnings is important barometer for consumer stocks)

July 1 (Wednesday)

- US June ADP Employment Change announced;

- US June ISM Manufacturing PMI announced;

- Fed Chair Wash speaks at ECB Forum; (Wash speech is biggest highlight this week, may hint second half policy direction (hike/maintain/pivot).

July 2 (Thursday)

- US June Non-farm Payrolls, Unemployment Rate, Initial Jobless Claims announced, market expects new employment 113k, unemployment rate 4.3%; ★★★

July 3 (Friday)

- US stocks closed due to Independence Day holiday;

*This week US stock core highlights: Key window for first half closing and second half policy tone, employment data and Wash speech will decide market short-term direction. Focus on whether employment data supports Fed policy pivot, and Nike etc. consumer stock earnings guidance for sector.

Institutional Views

Multiple investment banks believe Supreme Court ruling upholding Fed independence is positive signal, helps reduce policy uncertainty and stabilize long-term interest rate expectations. BofA tech team maintains defensive stance, warns S&P 500 may see three-wave correction in July-September, suggests hedging or reducing risk exposure. Geopolitics aspect, US-Iran talks start seen as short-term risk appetite catalyst, oil prices and safe-haven assets under pressure, but any negotiation reversal may quickly reverse sentiment. Crypto market aspect, institutions continue to focus on ETF fund flows and Bitcoin "digital gold + payment" dual narrative, although early June appeared large outflows, but recent stabilization coupled with MSTR etc. company capital moves, shows long-term adoption trend unchanged. Overall consensus is: macro environment marginal improvement, but need to guard against technical correction risk, suggest maintaining balanced allocation between growth and defense.

Disclaimer: Above content organized by AI search, manual verification only for publication, not as any investment advice. Data in text inevitably exists deviations, please refer to market instant data as standard.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News