Bitget UEX Daily Report | U.S.-Iran Peace Draft Unveiled, Spurring Oil Sanctions Relief; Waller’s First Fed Appearance Imminent; SpaceX Market Cap Soars Past Amazon’s

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S.-Iran Peace Draft Unveiled, Spurring Oil Sanctions Relief; Waller’s First Fed Appearance Imminent; SpaceX Market Cap Soars Past Amazon’s

Overall, the market is shifting from geopolitical shocks to macroeconomic policy and fundamental validation; investors are advised to focus on asset rotation opportunities driven by data verification.

I. Top News

Fed Updates

Warsh’s Debut Tonight; May Skip Dot Plot

- New Fed Chair Kevin Warsh will make his first public appearance tonight; markets are closely watching his policy remarks;

- He is widely expected to omit the interest-rate “dot plot” forecast, breaking a roughly 14-year tradition;

- This move may signal caution toward forward guidance and could affect market expectations on communication.

This development may amplify short-term rate volatility; investors should monitor Warsh’s latest signals on inflation and the path of monetary easing.

International Commodities

Full Text of U.S.-Iran Peace Agreement Draft Leaked: Immediate Oil Sanctions Relief & $300B Reconstruction Fund

- The draft agreement would allow Iran to resume oil exports immediately and unfreeze overseas assets, while establishing a private reconstruction fund of at least $30 billion;

- Trump referenced the potential reopening of the Strait of Hormuz; Iran emphasized troop withdrawal and other conditions;

- Related developments have already spurred some tanker activity; markets are watching the pace of long-term sanctions relief.

Geopolitical easing offers near-term upside for crude oil supply expectations, but lingering uncertainty over long-term implementation may continue to influence oil price volatility and energy-sector performance.

Macroeconomic Policy

U.S. Import Prices Post Largest YoY Gain in Nearly Four Years in May

- Import price index rose 1.9% MoM and 6.7% YoY; sharp increases seen in plastics, computers, and airfares;

- Data highlights inflationary transmission from the Iran-related conflict and surging data-center demand;

- Wells Fargo raised its S&P 500 year-end 2026 target to 7,800–8,000 points, reflecting optimism on corporate earnings.

Broadening inflation pressures may constrain Fed flexibility, offering near-term support to the U.S. dollar and precious metals—but also posing downside risks to highly valued assets.

II. Market Recap

Commodities & FX Performance

* Spot Gold: ~$4,330/oz, +0.09%

* Spot Silver: ~$70/oz, +0.02%

* WTI Crude: ~$76/bbl, +0.68%

* Brent Crude: ~$79/bbl, +0.57%

* U.S. Dollar Index (DXY): 99.509, -0.02%

Driver Analysis: The U.S.-Iran peace agreement draft signals increased supply, and the potential reopening of the Strait of Hormuz exerts short-term downward pressure on crude prices—though geopolitical tail risks remain. Import price data underscores persistent inflation, bolstering the dollar’s and precious metals’ safe-haven appeal. Institutional views suggest AI-driven demand and supply-chain factors will continue pushing select commodity prices higher, while shifting Fed policy expectations under Warsh’s early leadership may strengthen inter-asset correlations: gold benefits from real-rate considerations, while crude seeks equilibrium amid easing supply constraints. Near-term, markets will focus on progress in implementing the agreement and macro data’s impact on risk sentiment.

Cryptocurrency Performance

* BTC: ~$65,818, -0.91%

* ETH: ~$1,798, +0.05%

* Total Crypto Market Cap: ~$2.34 trillion, -0.5%

* 24H Liquidations: ~$370 million total, with ~$200 million long liquidations

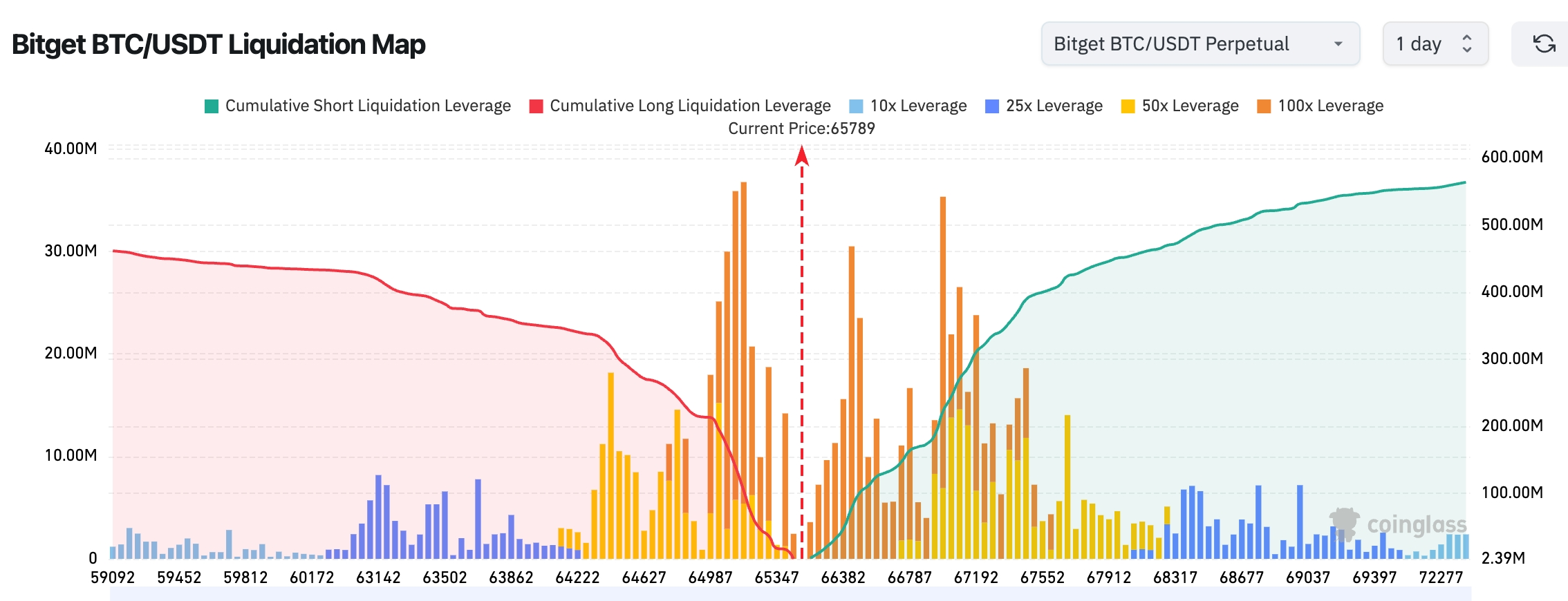

* Bitget BTC/USDT Liquidation Map: Current price ~$65,789 USDT sits between dense long and short liquidation zones. However, a large cluster of high-leverage short positions accumulates above $66,800–$67,800, with cumulative short liquidation volume notably exceeding that of longs below—suggesting upward momentum to “sweep” shorts. A breakout above ~$66,300 could trigger cascading short liquidations and accelerate upward movement; conversely, the $65,000–$65,300 zone represents recent dense long liquidation—acting as both support and key risk area.

* Spot ETF Net Inflows/Outflows: BTC spot ETFs saw net outflows of $64.8 million yesterday.

Driver Analysis: Geopolitical easing and macro-inflation data interacted to produce divergent crypto performance. BTC faced modest pressure amid risk sentiment and dollar correlation, while ETH held relatively resilient supported by staking dynamics and ecosystem activity. Leveraged liquidations were predominantly long-based, indicating profit-taking among elevated long positions. ETF flows remained cautious, reflecting institutional wait-and-see amid uncertainty. Technically, BTC is consolidating within a key range; attention centers on whether Fed communication may provide liquidity tailwinds. Overall, macro drivers dominate; near-term trends hinge on agreement implementation and data validation, with BTC/ETH divergence likely persisting amid shifts between AI and traditional narratives.

U.S. Equity Index Performance

* Dow Jones Industrial Average: Closed ~51,999 (+0.64%), hitting consecutive new highs

* S&P 500: Closed ~7,511 (-0.57%), exhibiting clear high-level consolidation

* Nasdaq Composite: Closed ~26,376 (-1.15%), weighed down by tech-sector divergence

Tech Giants Update

* NVDA: $209, -1.8%

* AAPL: $299, +0.9%

* MSFT: $391, -1.5%

* GOOGL: $373, +1.1%

* AMZN: $246, -0.01%

* META: $567, -1.5%

* TSLA: $405, -1.5%

Summary & Driver Analysis: Indices diverged—Dow advanced to new highs driven by value and defensive sectors, while Nasdaq lagged due to chip-stock pullbacks. Following its IPO, SpaceX’s market cap surpassed Amazon’s, ranking fifth globally—highlighting investor enthusiasm for aerospace and emerging tech. Google and Apple signaled AI hardware readiness via OS upgrades and product roadmaps, yet broad semiconductor declines reflect valuation and supply concerns. Overall, the tech sector presents structural opportunities amid the tension between AI’s long-term narrative and short-term geopolitical/inflation headwinds—not a monolithic trend.

Crypto-Linked Stock Futures Overview

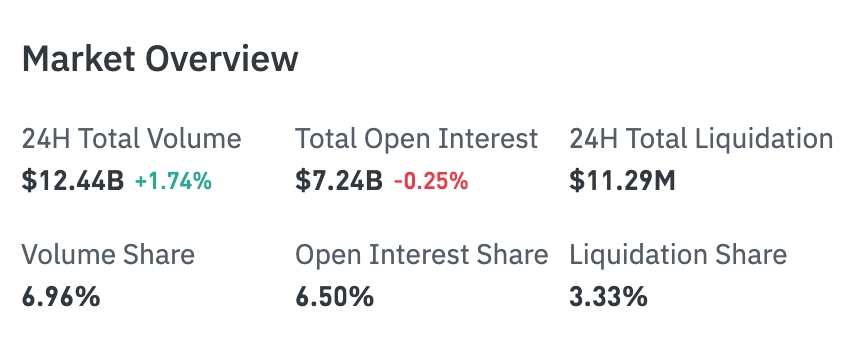

* 24H Total Turnover: $12.43 billion (+1.66%)

* Total Open Interest (OI): $7.235 billion (-0.28%)

* 24H Total Liquidations: $11.29 million

* Turnover Share: 6.96%

* OI Share: 6.50%

* Liquidation Share: 3.33%

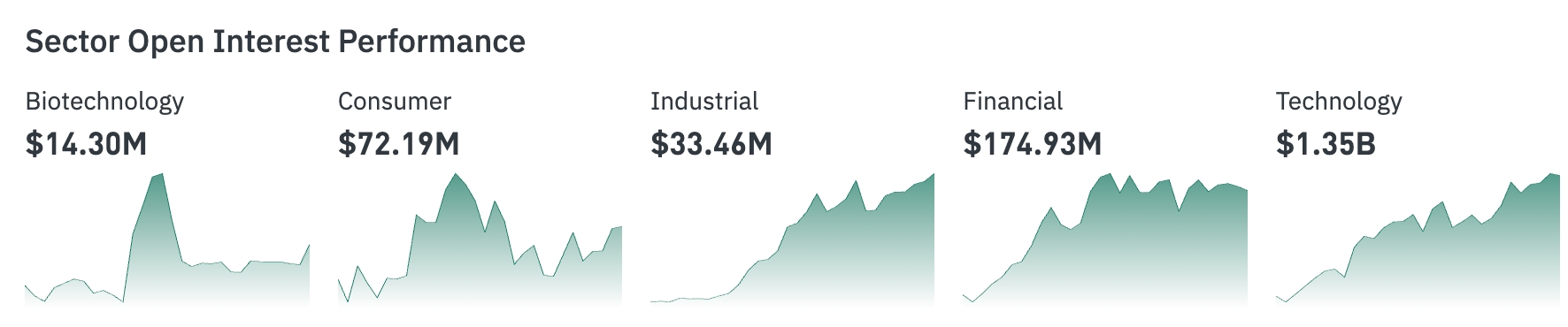

Sector Positioning

* Technology: $1.345 billion (largest position)

* Financials: $175 million

* Biotech: $14.297 million

* Consumer: $72.178 million

* Industrials: $33.499 million

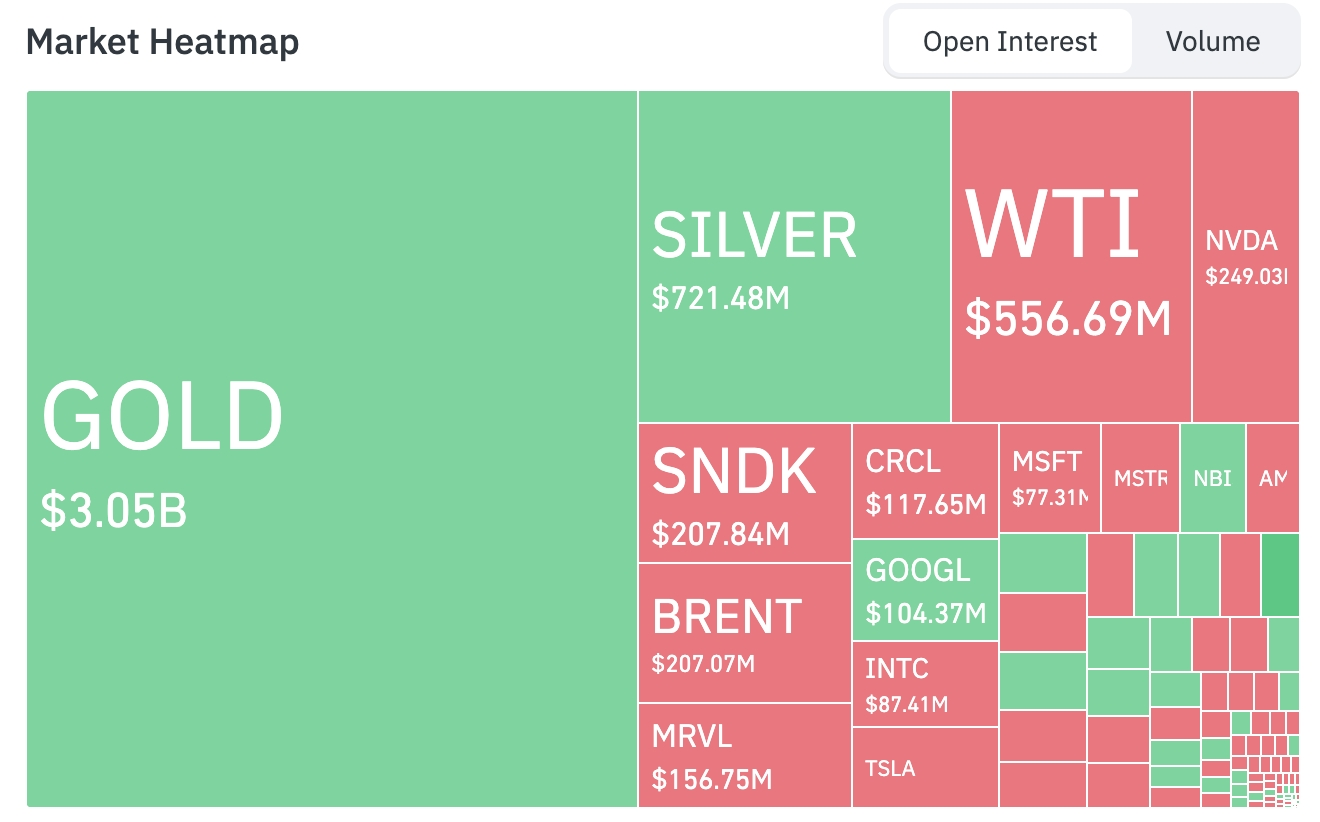

Position Heatmap

Top 9 Positions by Size

1. GOLD (Gold): $3.046 billion

2. SILVER (Silver): $721 million

3. WTI (WTI Crude): $557 million

4. NVDA (NVIDIA): $249 million

5. SNDK: $208 million

6. BRENT (Brent Crude): $207 million

7. MRVL (Marvell): $156 million

8. CRCL (Circle): $118 million

9. GOOGL (Google): $104 million

Market Capital Flow Observations

* Precious metals (gold and silver) dominate positioning, collectively holding nearly $3.8 billion—making them the largest capital concentration in the stock futures section.

* Energy commodities show divergence: both WTI and BRENT rank highly, signaling strong trading interest in crude oil products.

* Tech stocks remain core trading themes—NVIDIA (NVDA), Google (GOOGL), Microsoft (MSFT), and Tesla (TSLA) all appear prominently on the heatmap.

* Green-colored assets slightly outnumber red ones on the heatmap, suggesting overall positive risk appetite—though signs of capital outflows emerged for select AI- and semiconductor-linked names.

Energy Sector: Minor Volatility

* Key stocks: XOM (+0.8%), CVX (-0.5%), etc.

* Drivers: U.S.-Iran peace draft improves supply outlook, suppressing oil prices short-term but supporting long-term stability expectations.

Tech Hardware / Semiconductor Sector Pullback

* Key stocks: INTC (-8.5%), AMD (-7.2%), MU (-6.3%), etc.

* Drivers: Sector rotation, profit-taking, and valuation pressure—new entrants like SpaceX draw capital away.

Defensive / Financial Sector Relatively Strong

* Key stocks: JPM (+1.5%), GS (+2.0%), etc.

* Drivers: Supporting Dow performance, benefiting from value rotation and active M&A.

III. Deep Dive: U.S. Equities

1. SpaceX – Robust First-Day Trading

Event Summary: Following its IPO, SpaceX shares surged over 16% intraday before closing up ~4.8%, reaching a market cap of $2.65 trillion—surpassing Amazon to rank fifth globally. Despite limited float amplifying volatility, revenue remains below traditional giants. Options trading has commenced; market participants watch long-term growth potential.

Market Interpretation: Institutions widely attribute short-term price gains to constrained float, but long-term valuation hinges on commercial space milestones—including launch frequency, Starlink monetization, and broader aerospace adoption. Its high-growth profile resonates with defense/space-economy trends; initial volatility may gradually subside as liquidity improves.

Investment Implications: Investors should track trading volume expansion and financial validation. Suitable for higher-risk portfolios as a core exposure to emerging tech—combined with prudent position sizing to manage IPO-phase uncertainty.

2. Apple (AAPL) – 2027 Product Roadmap Unveiled

Event Summary: Apple plans to launch AI-powered AirPods (with cameras), a foldable phone, and commemorative iPhone models by late 2027—and continues advancing smart glasses.

Market Interpretation: Analysts see AI wearables further blurring hardware-service boundaries, potentially boosting accessory and subscription revenue. Smart glasses represent a strategic bet on metaverse/AR futures—but supply-chain maturity and consumer adoption remain critical variables.

Investment Implications: Hardware innovation cycles offer mid-to-long-term catalysts; dynamic allocation aligned with product launches is advised. Monitor execution delays or intensifying competition as potential margin risks.

3. Google (GOOGL) – Android 17 Launches

Event Summary: Google launched Android 17, optimizing multitasking, video creation, and gaming—while laying groundwork for intelligent agent AI capabilities. It also unveiled the Brazos liquid-cooling system to manage high-density AI chip heat.

Market Interpretation: This strengthens Android’s ecosystem dominance and reinforces Google Cloud’s infrastructure edge—particularly for AI training and edge computing. Analysts expect concurrent growth in ad targeting precision and enterprise cloud demand, though open-source strategies may accelerate industry competition.

Investment Implications: Ecosystem upgrades deliver tangible core-business tailwinds—ideal for stable tech allocations. Watch cloud-revenue share growth, but weigh long-term competitive risks from open-source technology spillover.

4. Snap (SNAP) – Consumer AR Glasses Launch

Event Summary: Snap launched Specs AR glasses priced at $2,195, positioning them as next-generation computing devices—intensifying competition with Apple and Meta in AR/XR.

Market Interpretation: As a major consumer-facing AR hardware initiative, this product tests mass-market readiness and builds proprietary data advantages. Views are split: optimists highlight advertising platform upside; skeptics cite premium pricing and immature ecosystem.

Investment Implications: High-uncertainty hardware bets warrant satellite allocations. Focus on user adoption metrics and developer ecosystem progress—and track evolving competitive dynamics against Meta and Apple.

5. Fox Corporation (FOXA) – $22B Roku Acquisition

Event Summary: Fox announced a $22 billion acquisition of streaming platform Roku to enhance targeted advertising and digital distribution—positioning the combined entity as the third-largest U.S. TV audience player.

Market Interpretation: This signals accelerated digital transformation among legacy media players; Roku’s platform significantly boosts sports/news content reach. Synergies may improve ad monetization efficiency, though regulatory scrutiny and integration costs pose execution risks.

Investment Implications: M&A injects growth momentum into the media sector—monitor post-deal synergy realization. Assess debt impact and cultural integration challenges; long-term value depends on streaming market-share gains.

IV. Market Updates

1. According to CoinDesk, Strategy’s Bitcoin-collateralized preferred stock STRC closed Tuesday at $91.79—the third-lowest close since its March 2025 listing—down nearly 8% from its $100 par value. STRC has not traded at $100 since its May 15 ex-dividend date. Contributing factors include: BTC price pressure near $65,000—a ~50% drop from last October’s all-time high—and growing concerns over dividend coverage, as Strategy now holds only ~7 months of dividend-paying capacity versus 24 months previously.

2. VanEck reported that Bitcoin miners face a ~$50 billion short-term funding gap in transitioning to AI infrastructure, with longer-term capital needs estimated at ~$22.1 billion. Analysts note investor focus has shifted from contract signings to execution risk: industry delivery of leased AI and HPC capacity stands at only ~25%, and companies missing construction milestones risk “structural downgrades” from investors.

3. Ki Young Ju, CEO of CryptoQuant, posted on X that “altcoins haven’t died—only those propped up solely by narrative have.” The era of profiting purely through token issuance is over. He identifies three categories of viable altcoins: global internet companies with tokenized market layers, DeFi services generating real revenue, and projects aligned with broader financial trends.

4. The Wall Street Journal reported, citing insiders, that under the agreement the U.S. will permit Iran to immediately resume oil and fuel export sales—providing Tehran an upfront economic incentive to de-escalate conflict. Provisions exempting oil sales from sanctions will take effect immediately upon signing this week.

5. Bloomberg ETF analyst Eric Balchunas noted that two-times-leveraged SpaceX-related ETFs recorded over $1 billion in combined first-day trading volume—of which LeverageShares’ product accounted for ~$281 million—setting a new record for highest first-day ETF volume since Bitcoin spot ETF IBIT launched, surpassing ETHA and DRAM.

V. Market Calendar

June 17 (Wednesday)

1. U.S. Economic Data: May Retail Sales (watch for consumer resilience). ★★★★

2. Fed FOMC Rate Decision & Economic Projections (Kevin Warsh’s first meeting as Chair): Markets broadly anticipate no change to current rates (~3.75%). Key focus: Warsh’s press conference tone, comments on inflation/employment, and any hint of future hikes. ★★★★★

3. U.S. Earnings: Jabil (JBL), etc.

June 18 (Thursday)

1. U.S. Economic Data: Weekly Initial Jobless Claims (June 13), Philly Fed Manufacturing Index, etc.

2. U.S. Earnings: Accenture (ACN), Kroger (KR), etc.—key names in consumer and tech services. ★★★★

June 19 (Friday)

1. U.S. Markets closed for Juneteenth federal holiday.

Key U.S. Equity Themes This Week: “Fed Focus Week”—Kevin Warsh’s inaugural FOMC meeting + retail sales data + ACN/KR earnings—to shape macro-policy expectations and market sentiment. SpaceX (SPCX)’s first full trading week post-IPO (impacting space/tech-related equities).

VI. Institutional Views

Top-tier investment banks generally agree the U.S.-Iran framework injects clarity into energy markets, but sticky inflation and communication from the Fed’s new leadership will drive near-term volatility. Wells Fargo’s S&P upgrade reflects confidence in corporate resilience; Goldman Sachs’ M&A data underscores AI-fueled strategic consolidation. In crypto, ETF flows and leveraged liquidations signal institutional caution—BTC seeks support at key levels, while gold retains safe-haven appeal. Overall, markets are pivoting from geopolitical shocks toward macro-policy calibration and fundamentals verification—opportunities lie in data-driven asset rotation.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data herein may contain inherent discrepancies; please rely on real-time market data for decision-making.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News