Bitget UEX Daily Report | Trump Says U.S.-Iran Deal Could Be Reached Within a Week; Google Raises $80 Billion to Support AI Infrastructure; Anthropic Secretly Files IPO Prospectus

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Trump Says U.S.-Iran Deal Could Be Reached Within a Week; Google Raises $80 Billion to Support AI Infrastructure; Anthropic Secretly Files IPO Prospectus

Overall, the Federal Reserve’s policy flexibility combined with the AI theme is expected to continue driving U.S. equities and related assets upward, though investors should remain vigilant against volatility risks arising from excessively rapid valuation expansion.

I. Top News Highlights

Federal Reserve Update: Fed Holds Rates Steady, Monitoring Geopolitical Developments and New Inflation Signals

- Markets still anticipate limited rate cuts by the Fed this year; however, near-term policy caution is driven by easing Middle East tensions and AI-fueled economic growth.

- Recent data show no clear signs of inflationary pressure receding.

- Analysis: Easing geopolitical risks may alleviate upward pressure on energy prices, granting the Fed greater policy flexibility. However, robust AI-related demand could bolster economic resilience, limiting expectations for aggressive monetary easing.

Commodities & FX: Trump Says U.S.-Iran Deal Could Be Reached Within a Week—Oil and Metals React to De-escalating Geopolitics

- Trump stated negotiations are progressing smoothly, with expectations of an extended ceasefire and the reopening of the Strait of Hormuz.

- Copper prices rose amid looming U.S. tariff reviews; Goldman Sachs and Citigroup have raised their copper price forecasts.

- Analysis: If implemented, the agreement would ease energy supply concerns, exerting short-term downward pressure on oil prices. Long-term demand from AI and energy transition trends, however, continues to support industrial metals such as copper.

Memory Market Enters “Super Cycle”; Google Raises $80 Billion to Accelerate AI Infrastructure Buildout

- JPMorgan forecasts the global memory market will reach $1.7 trillion by 2028, with HBM supply-demand gaps persisting through that year.

- Alphabet announced an $80 billion financing plan dedicated to AI infrastructure development; Berkshire Hathaway will contribute $10 billion. Meanwhile, Anthropic—a key Alphabet investment—has confidentially filed its IPO Form S-1 with the SEC and could go public as early as this fall, with a current valuation approaching $96.5 billion.

- Analysis: AI demand is expanding beyond GPUs into CPUs and memory. Combined with heavy capital commitments from tech giants and Anthropic’s IPO progress, investor confidence in long-term AI infrastructure growth has strengthened significantly. Further easing of geopolitical risks reduces macro uncertainty, creating a favorable environment for technology capital expenditures.

II. Market Recap

Commodities & FX Performance

- Spot Gold: Down ~1.3%, trading around $4,480–$4,500/oz, continuing its recent sideways-to-weaker trend amid easing geopolitical risk.

- Spot Silver: Down ~0.3–0.6%, near $75/oz, holding up relatively well supported by industrial demand.

- WTI Crude Oil: Up ~5%, near $92/barrel, driven by short-term geopolitical supply concerns and deal expectations.

- Brent Crude Oil: Up ~4.2%, near $95/barrel, with geopolitical factors dominating short-term sentiment.

- U.S. Dollar Index: Up ~0.25%, trading near 99.15–99.18, influenced by shifting risk sentiment and Fed policy expectations.

Cryptocurrency Performance

- BTC: –3.58%, currently ~$71,260.

- ETH: –0.79%, currently ~$1,990.

- Total Crypto Market Cap: –2.6%, ~$2.52 trillion.

- 24-Hour Liquidations: ~$632 million total; long positions accounted for $504 million.

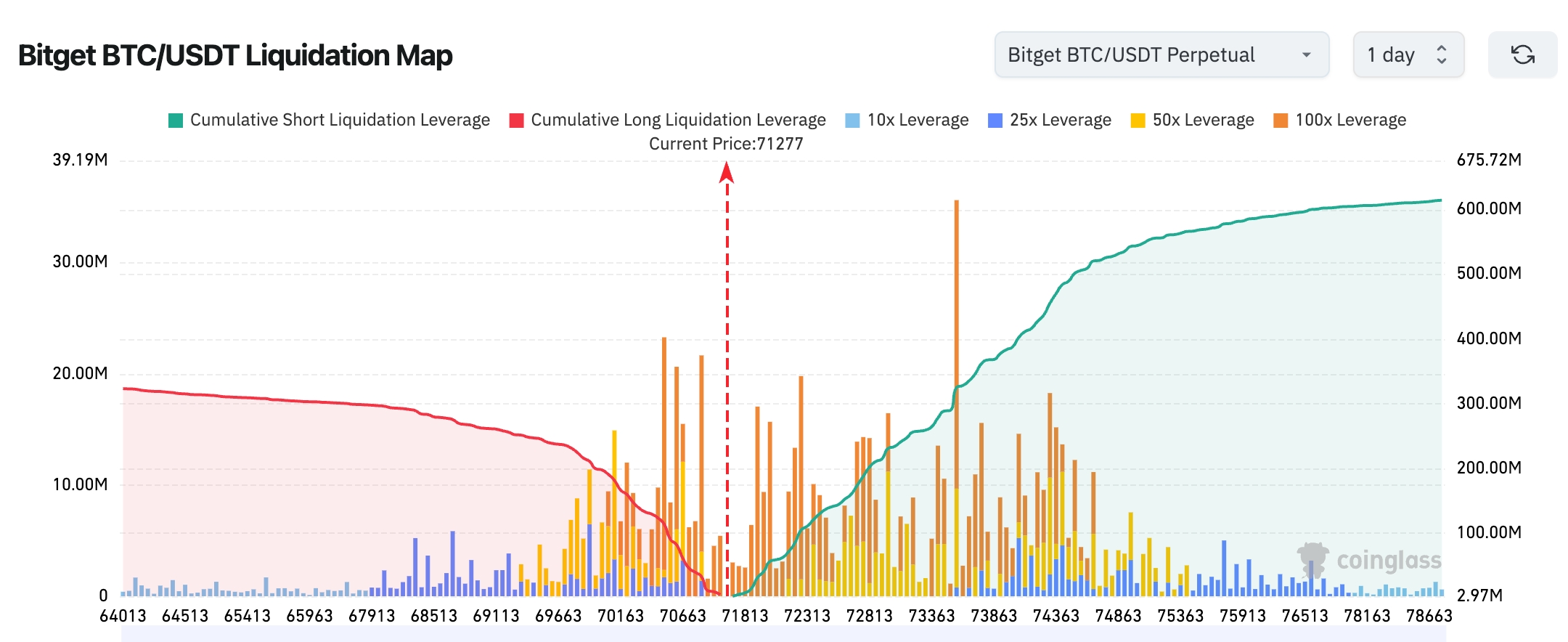

- Bitget BTC/USDT Liquidation Map: Current price (~$71,277) sits at the edge of a dense liquidation zone. A stronger rally above $72,000 could trigger cascading short liquidations, as the $73,000–$74,500 range holds significantly more short liquidation volume (green zone ~$600 million). Below $70,000–$70,600 lies a concentration of long leverage positions, but cumulative long liquidation volume remains markedly smaller than short-side exposure. Thus, structurally, the map suggests a near-term bias toward “sweeping short liquidity first.” Key watch level: whether a short squeeze emerges near $73,500.

- Spot ETF Net Flows: BTC spot ETFs saw modest net outflows yesterday; ETH spot ETFs remained relatively stable.

- BTC Spot Flows: Overall net outflow yesterday, reflecting partial profit-taking.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +0.09%, closing at 51,078.88—new all-time high, consecutive days.

- S&P 500: +0.26%, closing at 7,599.97—robust, steady advance to new highs.

- Nasdaq Composite: +0.42%, closing at 27,086.81—AI-related tech stocks led gains.

Tech Giants’ Performance

- NVDA: +6.29%, $224.43—driven by strong AI chip demand.

- MSFT: +2.28%, $460.52—cloud and AI businesses delivering steady growth.

- GOOGL: –1.07%, $372.34—Alphabet’s financing plan provides support, though market sentiment remains mixed.

- AMZN: –3.47%, $261.26—partial profit-taking.

- META: –5.07%, $600.47—short-term market correction.

- TSLA: –4.57%, $415.88—clear market divergence.

- AAPL: –1.84%, $306.31—monitor upcoming developments. Core driver: AI infrastructure capex expectations and memory cycle upswing underpin most mega-cap performance, while some stocks experienced profit-taking.

Sector Rotation Observations

AI Application Software Sector Shows Strong Gains

- Key Stocks: MongoDB up >10%; ServiceNow up 9–10%; Salesforce up >9%.

- Drivers: AI demand is rapidly spreading from foundational compute layers to application layers. Coupled with massive infrastructure investments by giants like Alphabet, market expectations for storage and enterprise AI software growth have surged significantly. Enterprises are accelerating adoption of AI-powered databases, automation platforms, and CRM solutions—driving sector-wide valuation recovery and capital inflows.

III. Deep Dives: U.S. Equity Analysis

1. Hewlett Packard Enterprise (HPE.US) – Earnings Beat Sparks Sharp Rally

Event Summary: HPE reported Q2 revenue of $10.7 billion, up 40% YoY—significantly exceeding consensus estimates. Network business revenue surged 148%. Adjusted EPS came in at $0.79—well above forecasts. The company also raised full-year guidance, sending after-hours shares up over 36%. This exceptional performance stems primarily from explosive demand for AI servers and related infrastructure. Market Interpretation: Multiple institutions highlight surging AI server demand as the core catalyst behind HPE’s earnings inflection point—the magnitude of the beat is rare in recent years. Analysts note HPE’s positioning in AI hardware is shifting from the periphery to center stage, with high order visibility ahead. Supply chain volatility remains a key watchpoint. Investment Takeaway: Hardware infrastructure providers offer significant earnings elasticity across the long-cycle AI capex wave. Investors should closely monitor subsequent order execution and gross margin trends to assess sustainability.

2. Alphabet (GOOGL) – $80 Billion Financing Plan

Event Summary: Alphabet announced an $80 billion financing initiative focused on AI infrastructure buildout; Berkshire Hathaway will invest $10 billion. Concurrently, Anthropic confidentially filed its IPO Form S-1 and may go public as early as this fall. These moves underscore tech giants’ deepening commitment to AI. Market Interpretation: Institutions broadly view long-term returns from AI infrastructure as highly attractive. Berkshire’s participation serves as powerful validation of the sector’s promise. Analysts believe this initiative will accelerate Alphabet’s cloud business growth and reinforce its leadership position in the generative AI ecosystem. Investment Takeaway: Mega-cap capital deployment will significantly raise barriers to entry across the AI ecosystem. Companies across the value chain stand to benefit continuously; investors should focus on tangible capex execution and resulting order flow opportunities.

3. Intel (INTC) – CEO’s COMPUTEX Keynote Preview

Event Summary: Intel’s CEO will deliver a keynote address at COMPUTEX, drawing intense market attention to its latest AI chip roadmap and product updates. With shares recently under pressure, the speech represents a critical opportunity to restore investor confidence. Market Interpretation: Though facing stiff competition, analysts believe timely delivery of promised performance and ecosystem support could provide meaningful near-term sentiment lift. Progress on AI accelerators and open-platform strategy will be pivotal in determining Intel’s share in the increasingly diversified competitive landscape. Investment Takeaway: Investors should carefully assess how well the speech aligns with market expectations. Near-term volatility may present tactical entry points, but long-term success remains contingent upon execution quality and ecosystem development outcomes.

4. Micron Technology (MU.US) – AI Memory Demand Drives Record Highs

Event Summary: Micron’s stock continues its strong run, repeatedly hitting new all-time highs—peaking near $1,046—and now trading consistently above $1,000. Its entire 2026 HBM (High Bandwidth Memory) production capacity—including HBM4—is fully booked via long-term contracts. Q2 revenue and gross margins both hit record levels, with AI datacenter demand for advanced memory serving as the primary growth engine. Market Interpretation: Institutions widely see Micron transforming from a traditional cyclical memory vendor into a core AI infrastructure supplier. HBM shortages are expected to persist through 2028, supporting pricing power and elevated gross margins. Several major banks have raised their price targets—some to $1,000–$1,750—reflecting strong optimism about the AI memory supercycle. Investment Takeaway: MU benefits from solid fundamentals driven by AI compute expansion-induced memory bottlenecks, making it suitable for long-term thematic allocation within AI portfolios. However, investors must monitor validation of its Q3 earnings report (June 24) and manage exposure to cyclical volatility.

IV. Cryptocurrency Project Updates

1. According to OnchainLens monitoring, an Ethereum OG whale sold another 5,000 ETH (~$10 million). Cumulatively, the whale has sold 60,000 ETH (~$122.25 million) at an average price of $2,106 and 9,442 wsETH (~$23.99 million).

2. Strategy disclosed in an SEC filing on Monday that it sold 32 Bitcoin between May 26–31 to fund preferred stock dividends—the first reported Bitcoin sale since December 2022.

3. Per The Block, Telegram CEO Pavel Durov announced that The Open Network (TON)’s native cryptocurrency will revert to its original whitepaper name, “Gram,” as part of its “Make TON Great Again” initiative.

4. According to Cryptopolitan, Strive plans to expand its ATM equity offering for common stock and SATA preferred stock by $2.1 billion each—totaling $4.2 billion. Estimates suggest Strive acquired ~2,649 BTC (~$193 million) over four trading days last week, including 1,179 BTC purchased on Friday alone.

5. Ian De Bode, CEO of Ondo Finance, stated that Ondo Perps—the first perpetual futures platform built for real-world assets (RWA)—will launch in the coming weeks.

V. Today’s Market Calendar

Upcoming Data Releases

Key Event Schedule

Tuesday, June 2

- COMPUTEX 2026 officially opens (June 2–5): Premier AI hardware event featuring NVIDIA, AMD, Intel, and other industry leaders. ★★★★★

- U.S. May ADP Private Payrolls release.

- Microsoft Build 2026 developer conference opens, focusing on AI applications.

Wednesday, June 3

- Major U.S. earnings: Broadcom (AVGO) and CrowdStrike (CRWD) report after market close ★★★★★ (AI hardware & cybersecurity heavyweights).

- COMPUTEX continues + Microsoft Build ongoing—AI theme remains dominant.

Thursday, June 4

- SpaceX begins IPO roadshow: One of the most anticipated IPOs in history—likely to boost market sentiment.

- COMPUTEX continues—AI compute, PC, and supply chain developments remain top-of-mind.

- Earnings: Ciena (CIEN) pre-market; Planet Labs (PL) post-market.

- IPO: Quantinuum (QNT) officially lists on U.S. exchanges (quantum computing theme).

Friday, June 5

- U.S. May Nonfarm Payrolls (NFP): Market expects ~115K–130K jobs added, unemployment rate ~4.2%, and average hourly earnings growth—a key inflation indicator. ★★★★★

Institutional Views: Leading investment bank analysts broadly agree that a potential U.S.-Iran agreement removes short-term geopolitical risk premiums, supporting continued upside for risk assets. However, the AI capex supercycle remains the dominant narrative. JPMorgan has raised its memory market forecast to $1.7 trillion, underscoring infrastructure demand resilience. Tech giants’ financing initiatives and earnings beats further bolster market confidence. While crypto markets face near-term headwinds—with ETF outflows and liquidations signaling leveraged-position unwinding—accumulation signals among long-term holders are clearly emerging. Overall, the Fed’s enhanced policy flexibility combined with the AI theme suggests continued upside momentum for U.S. equities and related assets—though investors should remain vigilant against volatility risks stemming from rapid valuation expansion.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute any investment advice. Data herein may contain unavoidable discrepancies; please refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News