Bitget UEX Daily Report | U.S.-Iran De-escalation Remarks Boost Market Sentiment; U.S. Stocks, Cryptocurrencies, and Gold All Rally; NVIDIA Invests $2 Billion in Marvell Technology

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S.-Iran De-escalation Remarks Boost Market Sentiment; U.S. Stocks, Cryptocurrencies, and Gold All Rally; NVIDIA Invests $2 Billion in Marvell Technology

Investors should maintain flexible positioning and closely monitor the progress of subsequent negotiations, as well as today’s ADP and ISM data for validation.

Author: Bitget

I. Top News Highlights

Federal Reserve Updates

Fed Officials Warn Iran Conflict Could Intensify Persistent Inflationary Pressures

- Jeff Schmid, President of the Kansas City Fed, noted that rising energy prices triggered by U.S.-Israel-Iran tensions could keep U.S. inflation elevated near 3% for longer—especially given that inflation is already high and has persisted for an extended period.

- He emphasized that energy-driven inflation should not be simplistically dismissed as transitory.

- Market impact: This statement reinforced investor caution regarding the Fed’s policy path. Short-term optimism from de-escalation signals is partially offsetting expectations, potentially delaying rate cuts.

International Commodities

De-escalation Signals Between U.S. and Iran Boost Energy & Precious Metals Markets

- Trump stated the U.S.-Iran conflict could conclude within two to three weeks, possibly enabling an early agreement; Iranian President Pezeshkian expressed willingness to end the war—but only if guaranteed against future aggression.

- Iran’s core steel plant was struck; the EU is considering reactivating its 2022 energy crisis response measures to manage market disruption.

- Market impact: Risk sentiment rebounded swiftly, lifting safe-haven assets like gold while easing upward pressure on oil prices—though infrastructure damage still poses long-term supply uncertainty.

Macroeconomic Policy

ECB President Challenges U.S. Optimism on War’s Economic Impact at G7 Meeting

- ECB President Christine Lagarde clashed with U.S. Treasury Secretary Bessent, arguing that war impacts will persist significantly longer—not briefly—due to widespread infrastructure destruction.

- Iran named 18 major U.S. tech firms—including industry giants—as “targets”; its Foreign Minister confirmed ongoing information exchanges with the U.S., but no formal negotiations have begun.

- Market impact: Transatlantic policy divergence highlights global economic uncertainty. While short-term risk assets benefit, long-term inflation and supply-chain pressures warrant continued attention.

Key Events

SpaceX Partners with 21 Banks to Prepare for IPO

According to sources cited Tuesday, SpaceX is collaborating with at least 21 banks to prepare its landmark IPO—the largest underwriting syndicate in recent years. Internally codenamed “Apex,” the offering is expected in June, with a projected valuation of $1.75 trillion, positioning it as one of Wall Street’s most anticipated stock market debuts. Sources said Morgan Stanley, Goldman Sachs, JPMorgan Chase, Bank of America, and Citigroup serve as active bookrunners—the lead banks managing the transaction. They added that another 16 banks have signed on for smaller roles. Roughly half of these banks had not previously been publicly reported as involved. The syndicate’s scale underscores both the magnitude and complexity of this proposed offering.

II. Market Recap

Commodities & FX Performance

- Spot Gold: +0.72%, ~$4,700; trend: surged sharply amid de-escalation signals, peaking near $4,700 before stabilizing.

- Spot Silver: +0.13%, ~$75; key feature: rebounded strongly alongside gold, reflecting restored safe-haven sentiment.

- WTI Crude: +0.66%, $102.19; driver: retreated on de-escalation expectations, easing short-term upside pressure on energy prices.

- Brent Crude: +0.31%, $104.37; driver: adjusted downward following war-ending signals.

- U.S. Dollar Index: −0.07%, 99.81; driver: improved risk sentiment weakened the dollar.

Cryptocurrency Performance

- BTC: +1.55% over 24H, ~$68,245; trend analysis: rallied strongly on U.S.-Iran de-escalation rhetoric, reclaiming the $68,000 level.

- ETH: +3.4% over 24H, ~$2,107; trend or key feature: recovered in line with broader markets, signaling rapid improvement in market sentiment.

- Total Crypto Market Cap: +0.5% over 24H, $2.43 trillion; driver: BTC and ETH leadership boosted overall risk appetite.

- Liquidations: ~$325 million liquidated over 24H—$136 million longs, $189 million shorts.

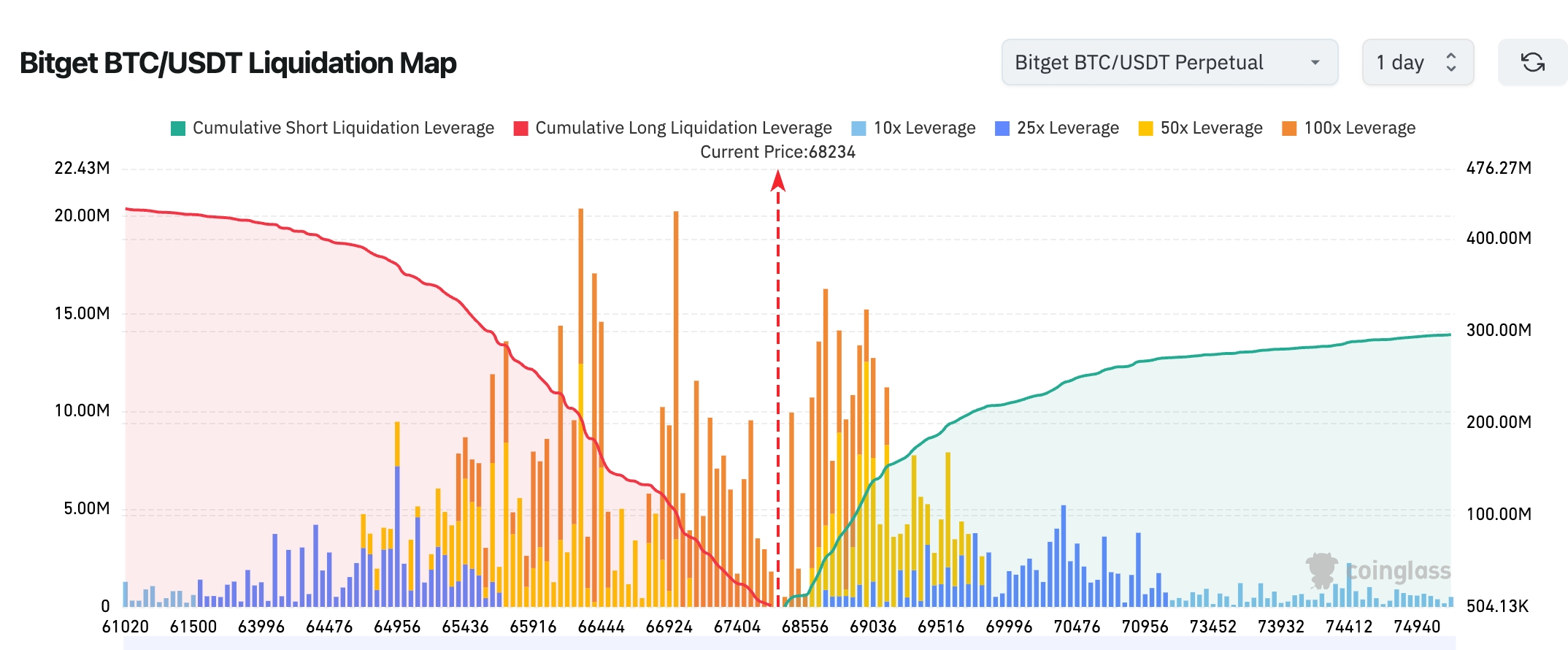

- Bitget BTC/USDT Liquidation Map: Current price ~$68,234—approaching the dense long-liquidation zone above $68,500–$69,000. High-leverage positions (50x–100x) are notably concentrated here; further upside may trigger cascading long liquidations. Strong support forms around $67,000–$67,500, while resistance intensifies above. Near-term consolidation near $68,000 is likely before direction emerges—key watch: whether volume-backed breakout above $69,000 occurs.

- Spot ETF Net Flows: BTC spot ETFs saw ~$19.1M net inflow yesterday; ETH spot ETFs saw ~$5.4M net inflow.

- BTC Spot Flows: $2.64B inflow, $2.672B outflow—net outflow of $32M.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +1,125.19 points, 46,341.33 (+2.49%)—largest single-day gain since May last year.

- S&P 500: +184.80 points, 6,528.52 (+2.91%)—boosted by swift digestion of geopolitical risk.

- Nasdaq Composite: +795.99 points, 21,590.63 (+3.83%)—driven significantly by tech stocks.

Tech Giants’ Moves

- Meta: +6.67%, $572.13

- NVIDIA: +5.59%, $174.40

- Google A: +5.14%, $287.56

- Tesla: +4.64%, $371.75

- Amazon: +3.64%, $208.27

- Microsoft: +3.12%, $370.17

- Apple: +2.9%, $253.79

Core reason: Fresh de-escalation signals between the U.S. and Iran significantly reduced the global geopolitical risk premium, rapidly restoring investor risk appetite. As quintessential high-beta growth assets, tech giants benefited most—these companies rely heavily on stable global supply chains and robust capital expenditure plans. De-escalation directly eased those concerns. Meanwhile, AI infrastructure demand remains red-hot, and Fed officials’ warnings about persistent inflation haven’t dented market expectations for eventual monetary easing—jointly propelling the “Magnificent 7” rally. Market sentiment shifted from risk-off to chasing growth stocks.

Sector Rotation Highlights

Memory Stocks rose >6.49%

- Representative names: SanDisk +10%+, Micron Technology +~5%, Seagate Technology +8%+

- Driver: Rising AI data center demand expectations, combined with broad tech rebound.

Optical Communications Stocks mostly rose

- Representative name: POET +~17%

- Driver: Continued momentum in AI infrastructure investment expectations.

Crypto Mining Companies rebounded sharply

- Representative names: Applied Digital +15%+, Hut 8 +~10%

- Driver: Direct boost from BTC’s price recovery.

Gold Stocks posted top gains

- Representative name: Coeur Mining +~14%

- Driver: Lingering safe-haven sentiment during early-stage de-escalation.

Popular U.S.-Listed Chinese Stocks rallied collectively

- Representative name: NIO +9%+

- Driver: Anticipated EV delivery data improvements coupled with improved risk sentiment.

III. In-Depth Stock Analysis

1. NVIDIA – Strategic $2 Billion Investment in Marvell Technology

Event Summary: NVIDIA announced a $2 billion strategic investment in Marvell Technology on Tuesday—a major follow-up to their existing AI chip collaboration. The move aims to deepen synergy between AI chips and optical communications, reinforcing NVIDIA’s leadership in high-performance computing and data center network infrastructure. As a global leader in semiconductors, Marvell’s products serve widely across AI accelerators and networking equipment. This equity investment helps NVIDIA secure critical supply chain resources, while providing Marvell capital to expand production capacity—jointly meeting surging hardware demand driven by explosive AI compute growth. Market Interpretation: Analysts broadly view this deal as strengthening NVIDIA’s AI ecosystem. It consolidates its dominance in the semiconductor value chain and sends a strong signal that the AI capex cycle remains intact. NVIDIA’s stock rose over 5%; Marvell surged nearly 13%—reflecting robust market confidence in AI’s long-term growth trajectory and growing acceptance of supply-chain integration trends. Investment Insight: Deepening AI supply-chain integration is accelerating. Investors should closely monitor long-term growth potential across semiconductor and optical communications sectors—and track progress on joint initiatives for sustained catalysts.

2. Tesla – Q1 Delivery Data Imminent

Event Summary: Tesla and several other new-energy vehicle (NEV) makers are set to release their Q1 2026 global delivery figures imminently. Prior concerns emerged due to potential supply-chain disruptions from U.S.-Iran geopolitical tensions. These reports will serve as a critical test of EV demand resilience and corporate capacity to navigate geopolitical risks. As the industry leader, Tesla’s delivery performance reflects not only its own production-sales dynamics but also serves as a key barometer for the entire NEV sector. Market Interpretation: Analysts widely believe that Q1 delivery data exceeding consensus would strongly bolster investor confidence in NEV demand. Though geopolitical factors introduce short-term uncertainty, Tesla’s 4.64% rally yesterday suggests the market has already priced in potential positives—and reaffirms continued faith in the company’s long-term growth narrative. Investment Insight: Investors should closely monitor the short-term catalytic effect of delivery data on share price, while simultaneously evaluating long-term benefits to global supply-chain recovery signaled by de-escalation—seizing valuation-recovery opportunities across the NEV sector.

3. Meta – Leading Gains Among Tech Giants

Event Summary: Meta Platforms’ stock jumped 6.67% yesterday—the highest among the Magnificent 7—directly benefiting from improved risk sentiment following U.S.-Iran de-escalation and sustained market expectations for AI application rollout. As a leader in social media and the metaverse, Meta’s AI-powered content recommendation and advertising business are increasingly delivering tangible results. Market Interpretation: Multiple institutions note Meta’s strategic execution in social platforms and the metaverse ecosystem is steadily materializing. De-escalation signals effectively eased macroeconomic headwinds, expanding room for valuation recovery. Yesterday’s leadership reflects strong investor confidence in Meta’s resilient, high-margin ad business—and in AI’s platform-level applications. Investment Insight: Tech-giant valuation recovery could extend amid improving risk sentiment. Investors should focus on earnings delivery and alignment with capex commitments—capitalizing on structural opportunities within sector rotation.

IV. Cryptocurrency Project Updates

1. S&P Dow Jones Indices tokenized its iBoxx U.S. Treasury Index on the Canton Network—bringing this pivotal fixed-income benchmark onto-chain as a digital asset. This tokenized index is not an investment product, but enables financial institutions to integrate pricing and index-level benchmark data directly into blockchain systems.

2. NFT marketplace Magic Eden announced its native wallet will enter “export-only mode” on April 1 and fully cease operations on May 1. Users must export private keys or seed phrases before then—or permanently lose access to assets. The wallet has been removed from all app stores; new downloads or recoveries are impossible.

3. Will Peck, Head of Digital Assets at WisdomTree, stated the pending “Clarity Act” currently debated in Congress is not essential for digital asset innovation. Existing SEC rules, he argued, already sufficiently support tokenized securities and funds—and the SEC possesses all necessary tools to foster high-quality tokenized markets.

4. New Hampshire’s Bureau of Securities Regulation plans to issue a $100 million municipal bond backed by Bitcoin. Rated Ba2 by Moody’s—two notches below investment grade—the bond’s principal and interest will be paid from revenue generated by the Bitcoin collateral. If Bitcoin’s price falls below a specified threshold, the trust will be liquidated to fully repay bondholders.

5. CFTC Enforcement Director: Combating insider trading based on misappropriated information in prediction markets, energy market manipulation, retail fraud, and anti-money laundering violations remain enforcement priorities.

6. Ethereum Layer-2 network Base released its 2026 strategy, focusing on scaling onchain tokenized asset markets, stablecoin payment use cases, and developer ecosystems. Base plans to enable tokenized trading of equities and commodities, and optimize settlement efficiency and cost for existing perpetual contracts and prediction markets. For payments, Base will introduce privacy features, stablecoin-denominated fees, multi-stablecoin liquidity, and savings/lending functionality. On the developer side, Base will continue investing in projects like Base Batches, introducing new tools and incentives to enhance AI and onchain market interaction.

V. Today’s Market Calendar

Data Release Schedule

| 08:15 | U.S. | ADP Employment Change | ⭐⭐⭐ |

| 08:30 | U.S. | Retail Sales (MoM/YoY) | ⭐⭐⭐⭐ |

| 10:00 | U.S. | ISM Manufacturing PMI | ⭐⭐⭐⭐ |

Key Event Preview

April 1 (Wednesday)

- NEV makers—including Tesla—will release Q1 delivery data en masse; Tesla has revised its 2026 delivery forecast downward to 1.689 million units;

- St. Louis Fed President and 2028 FOMC voter James Bullard speaks on the U.S. economy and monetary policy at 21:05 Beijing time;

- U.S. March ADP employment numbers released at 20:15; February retail sales MoM at 20:30; March S&P Global Manufacturing PMI final reading at 21:45; March ISM Manufacturing PMI at 22:00.

April 2 (Thursday)

- Dallas Fed President and 2026 FOMC voter Lorie Logan speaks at 23:00;

- U.S. initial jobless claims for week ending March 28 released at 20:30.

April 3 (Friday)

- U.S. March unemployment rate and nonfarm payrolls released at 20:30; March S&P Global Services PMI final reading at 21:45;

- Hong Kong and U.S.-listed Chinese stocks closed for Good Friday.

*This week’s U.S. equity theme centers on Fed speeches, NFP & ADP data, and Tesla delivery figures. Overlapping labor data and policy signals suggest heightened volatility.

Institutional Views:

Top-tier investment bank analysts broadly agree that de-escalation signals between the U.S. and Iran injected strong momentum into markets. Yesterday’s record-breaking daily gains across the three major U.S. indices—and concurrent rebounds in tech and crypto assets—underscore investor optimism about rapid geopolitical risk digestion. Institutions including Morgan Stanley note that improved short-term risk sentiment is likely to persist, though Fed officials’ inflation persistence warnings remind markets that energy price volatility could still constrain policy easing space. Overall, current conditions favor growth assets—but investors should remain vigilant about Iran’s latent long-term threats and the EU’s energy measures’ spillover effects on commodities. Maintaining portfolio flexibility and closely tracking negotiation developments—as well as today’s ADP and ISM data—remains critical.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News