Bitget UEX Daily Report | U.S.-Iran Negotiations Remain Deadlocked, but Ceasefire Expectations Boost U.S. Stocks; Google’s New Cache Compression Technology Disrupts Storage Sector

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S.-Iran Negotiations Remain Deadlocked, but Ceasefire Expectations Boost U.S. Stocks; Google’s New Cache Compression Technology Disrupts Storage Sector

Investors are advised to closely monitor U.S. employment data, the latest developments in the Middle East situation, and actual corporate earnings performance during the earnings season to seize structural opportunities—such as those in AI, aerospace, and CPUs—amid market volatility.

Author: Bitget

I. Key Market Highlights

Federal Reserve Updates

No major monetary policy adjustments for now; focus shifts to geopolitical risks

- White House Press Secretary Leavitt revealed that the U.S. and Iran have engaged in “productive contacts” over the past three days. Trump instructed the Department of Defense to pause strikes against Iran’s power and energy infrastructure—but emphasized that stronger measures would follow if Iran refuses to accept reality.

- Negotiations remain centered on uranium controls, with an action timeline expected within four to six weeks and no formal congressional authorization required. Meanwhile, Israel continues striking Iranian military targets without scaling back operations. Market impact: While the ceasefire expectation briefly eased risk premiums, no substantive de-escalation has occurred on the military front. Combined with the U.S. military’s troop buildup in the Middle East, oil prices and inflation uncertainty continue to constrain the Fed’s future policy space.

International Commodities

Hormuz Strait shipping disrupted; Saudi Arabia accelerates Red Sea export rerouting

- Since late February, when the Strait effectively halted operations, Saudi Arabia doubled crude exports from Yanbu Port within two weeks. Daily average loading volume this Friday reached 4.4 million barrels—approaching its 5-million-barrel target.

- COSCO Shipping has resumed booking services for Gulf countries, though vessels are temporarily avoiding the Strait of Hormuz. Market impact: Rapid supply-chain restructuring has temporarily alleviated global crude shortage concerns—but also exposed energy logistics’ vulnerability to geopolitical conflict. Oil price direction remains highly dependent on negotiation progress.

Macroeconomic Policy

Morgan Stanley CIO issues optimistic S&P earnings forecast

- Mike Wilson forecasts a 20% earnings growth for S&P 500 constituents over the next 12 months—a pace historically seen only during post-recession recoveries.

- Q1 earnings expectations have been revised upward to 11.9%, but JPMorgan warns that sustained $110/barrel oil prices could trigger a 5-percentage-point downward revision. Market impact: Upward earnings revisions support U.S. equity valuation resilience. The upcoming earnings season will serve as a critical validation window—geopolitics and oil prices remain key disruptors.

II. Market Recap

Commodities & FX Performance

- Spot gold: +0.72%, at $4,539/oz.

- Spot silver: +0.66%, at $71.73/oz.

- WTI crude: +1.13%, at $91.37/barrel.

- Brent crude: +1.13%, at $103/barrel.

- U.S. Dollar Index: +0.01%, at 99.637. Risk sentiment improved amid easing geopolitical tensions, leaving the dollar directionally neutral in the short term—though inflation expectations and Fed policy path still provide underlying support.

Core drivers: Markets rapidly priced in “a temporary easing of geopolitical risk,” triggering sharp declines in energy prices and easing prior stagflation concerns linked to high oil costs. Precious metals initially lost some safe-haven appeal before surging strongly late in the session. Institutions widely agree that gold’s long-term bull market fundamentals—central bank buying, persistent geopolitical uncertainty—remain intact; they recommend accumulating on dips. Crude faces near-term correction pressure, yet energy logic may reassert itself should U.S.-Iran negotiations fail to yield a substantive agreement. Investors should closely monitor developments in U.S.-Iran talks, the G7 foreign ministers’ meeting, and forthcoming EIA crude inventory data for directional guidance.

Cryptocurrency Performance

- BTC: +0.68% over 24H, at $71,176—rebounding for two consecutive days, driven by geopolitical relief and short-covering.

- ETH: +0.28% over 24H, at $2,165—relatively stable, supported by broad risk-sentiment improvement.

- Total crypto market cap: +0.5% over 24H, at ~$2.52 trillion. BTC-driven sentiment recovery is gradually taking hold.

- Liquidations: $157M total over 24H—$54M longs, $103M shorts.

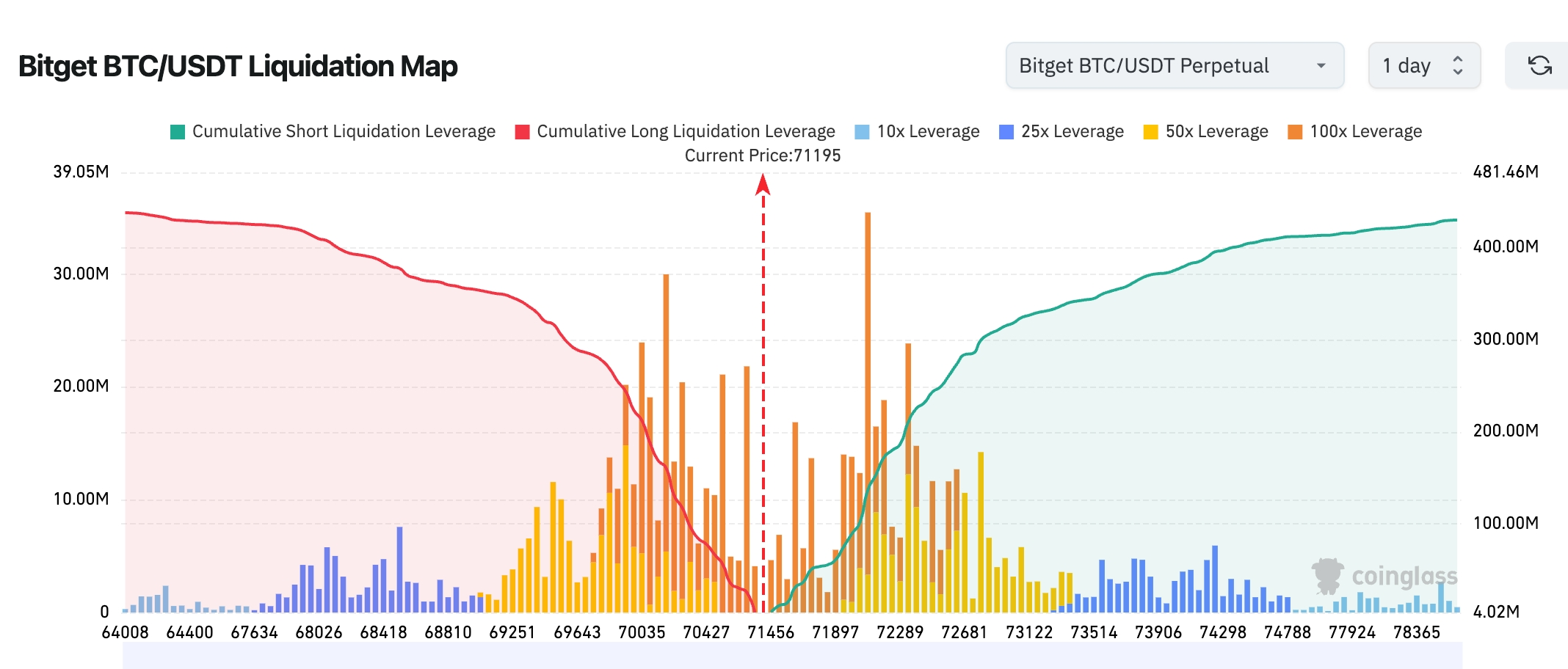

- Bitget BTC/USDT liquidation heatmap: Current price ~$71,195. Downside long liquidation zones have notably shrunk, while a dense cluster of high-leverage short positions remains concentrated between $71,800–$73,000—making upward short squeezes more likely in the near term. Overall structure shows significantly stronger liquidity above than support below; price consolidation would likely test upper liquidation density first.

- Spot ETF net inflows/outflows: BTC spot ETFs saw $78.5M net inflow yesterday; ETH spot ETFs saw $23.8M net inflow.

- BTC spot flows: $2.029B inflow vs. $2.004B outflow yesterday—net inflow of $25M.

U.S. Equity Index Performance

- Dow Jones: +0.66%, at 46,429.49—up for two straight sessions.

- S&P 500: +0.54%, at 6,591.9—defensive and growth sectors contributed evenly.

- Nasdaq: +0.77%, at 21,929.83—driven significantly by tech and aerospace themes.

Tech Giants’ Updates

- Apple (AAPL): +0.39%, at $252.62—robust consumer electronics demand, buoyed by improved risk sentiment.

- Amazon (AMZN): +2.16%, at $211.71—steady e-commerce growth and AWS cloud synergy.

- NVIDIA (NVDA): +1.99%, at $178.68—sustained AI compute demand, solid market confidence in AI narratives.

- Microsoft (MSFT): −0.46%, at $371.04—short-term profit-taking pressure emerged.

- Google (GOOG): +0.17%, at $290.93—release of new memory-optimization algorithms triggered ripple effects across the storage supply chain.

- Meta (META): +0.33%, at $594.89—stable performance in social platforms and advertising.

- Tesla (TSLA): +0.76%, at $385.95—EV sector rallied alongside broader risk sentiment.

Core rationale: Ceasefire expectations significantly boosted risk appetite, lifting growth stocks broadly. Google’s memory-optimization technology weighed on storage stocks short term—but the long-term AI thesis remains well-supported, resulting in partial sector rotation.

Sector Rotation Highlights

Commercial Space Sector: +10%+

- Key names: Rocket Lab (RKLB) +10%+, Planet Labs (PL) +10%+.

- Catalysts: Rising speculation that SpaceX will soon file its IPO prospectus, combined with Intuitive Machines securing a $180M NASA commercial lunar payload contract—accelerating commercialization and drawing capital into related equities.

CPU-Themed Sector: +7%+

- Key names: Intel (INTC) +7%+, AMD +7%+, Arm Holdings (ARM) +16.38%.

- Catalysts: AI-driven CPU supply tightness; Intel and AMD plan price hikes across their full CPU lines starting March–April; Arm’s self-developed AGI CPU outlook further heightened market expectations.

Memory/Storage-Themed Sector: Significant decline

- Key names: Micron (MU), Western Digital (WDC), SanDisk (SNDK) down 3%–5.7%.

- Catalysts: Google’s release of TurboQuant and similar algorithms drastically reduces memory requirements for LLMs and vector search engines—raising concerns about long-term memory chip demand.

Gold Mining Sector: +3%+

- Key names: Agnico Eagle Mines (AEM) +4.68%, Kinross Gold (KGC) +3%+.

- Catalysts: Precious metal price rebound, bolstered by geopolitical safe-haven demand.

III. In-Depth Stock Analysis

1. Google (GOOG) – TurboQuant and Related Algorithms Reduce AI Memory Footprint

Event Summary: Google launched several new algorithms—including TurboQuant and PolarQuant—to substantially compress memory requirements for large language models (LLMs) and vector search engines. It also unveiled Lyria 3 Pro, a music-generation model capable of producing full 3-minute songs in one go, embedded with SynthID watermarking. While these technological advances improve AI efficiency, they have sparked market concern over long-term memory chip demand—pressuring memory-related stocks across the board.

Market Interpretation: Institutions broadly agree that memory optimization may weaken near-term demand for DRAM, HBM, and HDDs—directly impacting companies like Micron and Western Digital. However, longer term, enhanced AI efficiency could expand overall compute deployment scale, keeping hyperscaler spending elevated—albeit along a structurally altered technical pathway. Some analysts note this reflects an early signal of AI’s shift from “training-centric” to “inference-optimized.”

Investment Implications: Memory-sector valuations face near-term pressure. Investors should differentiate between short-term technical headwinds and long-term AI demand trends—and closely track the real-world rollout of Google’s algorithms and actual hyperscaler memory procurement plans.

2. Micron (MU) / Western Digital (WDC) – Sector Correction Triggered by Google’s Memory Optimization

Event Summary: Micron fell ~3% and Western Digital ~4.7% following Google’s TurboQuant compression algorithms; SanDisk and other memory stocks declined similarly. Markets worry that sharply reduced AI model memory dependency could erode the strong demand tailwind previously generated by AI data center expansion.

Market Interpretation: Analysts point out that AI memory remains in short supply (HBM shortages are expected to persist through 2026–2028). Yet self-developed optimization technologies from tech giants like Google may accelerate a “memory efficiency revolution,” reshaping the entire supply chain. Institutions caution that current downside stems largely from sentiment contagion—not actual demand destruction.

Investment Implications: Exercise caution amid near-term memory-sector volatility. Consider opportunistic entries after technical validation, while diversifying exposure across other AI value-chain segments.

3. Rocket Lab (RKLB) / Planet Labs (PL) / Intuitive Machines (LUNR) – Commercial Space Sector Rally

Event Summary: Rumors of SpaceX’s imminent IPO filing propelled RKLB and PL up >10% each; Intuitive Machines surged 14.68% after winning a $180M NASA commercial lunar payload contract. Rocket Lab benefits from a record order backlog—including an $816M contract with the Space Development Agency—significantly boosting sector-wide enthusiasm.

Market Interpretation: Institutions believe SpaceX’s IPO anticipation could drive a broad re-rating of the commercial space ecosystem. As a leading small-to-medium launch vehicle provider, RKLB stands to benefit directly; PL leverages its Earth observation satellite network; and LUNR builds on lunar infrastructure development—all poised to gain from dual defense-and-commercial momentum. Analysts have upgraded growth forecasts for these firms, highlighting dual-demand drivers.

Investment Implications: Commercial space sector momentum is likely to persist. Focus on companies backed by tangible orders and meaningful technical moats—but remain alert to post-rumor volatility.

4. Intel (INTC) / AMD – CPU Supply Tightness Drives Price Hikes and Stock Gains

Event Summary: Surging AI demand continues diverting capacity, worsening CPU shortages for Intel and AMD. PC and server OEMs face acute scarcity, prompting both firms to raise prices across all CPU lines starting March–April. Their shares rose >7% Wednesday; Arm jumped 16.38% the prior day on its AGI CPU roadmap.

Market Interpretation: Multiple institutions note that CPU shortages—compounded by earlier memory constraints—have already pushed PC prices up 10–15%. The AI-first strategy is actively reshaping the semiconductor supply chain. While Intel and AMD gain pricing power, they also confront mounting capacity-expansion pressures and growing competition from Arm-based architectures.

Investment Implications: Short-term CPU-sector strength is validated. Monitor real-world margin improvements from price pass-through—and track how AI-chip capacity expansion impacts traditional CPU supply over time.

5. Circle (CRCL) – Shares Hit Record Single-Day Decline

Event Summary: Circle (CRCL) plunged 20.11%, marking its largest-ever single-day drop. Shares hit a low near $101 intraday and closed at $101.17; it rebounded slightly (+2.66%) the next day to close at $103.86. The primary catalyst was the unexpectedly stringent draft of the U.S. Clarity Act. Market rumors suggest the latest congressional compromise version may explicitly ban stablecoin platforms from paying any form of yield, interest, or rewards to holders (“yield ban”), directly undermining USDC’s short-term Treasury investment income model. If enacted, such a ban would severely diminish USDC’s attractiveness, reducing transaction volume and reserve size. Fox Business reporter Eleanor Terrett first disclosed draft details, triggering rapid negative repricing and capital flight. Secondary factors included profit-taking pressure from the ~10x post-IPO rally, compressed future interest margins due to Fed rate-cut expectations, and competitive dynamics with Tether plus broader regulatory uncertainty amplifying sentiment swings.

Market Interpretation: Institutions widely view the plunge as sentiment-driven overselling. Near-term volatility persists, but long-term fundamentals remain robust—USDC’s real-world circulation and on-chain usage continue rising (already meaningfully ahead of peers in 2026). Should the final legislation prove milder than feared (“less draconian than feared” is already circulating), share price recovery could be swift.

Investment Implications: Maintain caution near term; monitor upcoming congressional hearings and the final bill text. For long-term investors, consider strategic accumulation on dips—leveraging Circle’s growth potential in payments, tokenization, and cross-border settlements.

IV. Crypto Project Updates

1. Asset manager Franklin Templeton partnered with Ondo Finance to launch an ETF tokenized version tradable 24/7 in crypto wallets—bypassing traditional brokerage accounts and fixed trading hours.

2. As the U.S. Securities and Exchange Commission (SEC) prepares to roll out an innovation exemption program for tokenized assets, the U.S. House Financial Services Committee held a hearing on March 25 titled “Tokenization and the Future of Securities: Modernizing Capital Markets.” SEC Chair Paul Atkins stated the agency will soon solicit public input on a range of rulemaking topics—including a proposed innovation exemption serving as a regulatory sandbox for on-chain assets.

3. Bloomberg Senior ETF Analyst Eric Balchunas noted Morgan Stanley’s spot Bitcoin ETF could launch imminently. The New York Stock Exchange has formally announced listing arrangements for the fund—a typical precursor to imminent listing. Morgan Stanley filed its application in January and submitted a revised S-1 registration statement last week, confirming the ETF will list on NYSE Arca under the ticker MSBT.

4. According to Onchain Lens monitoring, a whale withdrew 11,999 ETH (~$26M) from Coinbase after a one-month dormancy and immediately staked it.

5. Following a compromise on stablecoin yield provisions in the U.S. CLARITY Act, reactions across the crypto industry have been mixed. Insiders report Coinbase expressed dissatisfaction with the latest compromise—but has not publicly opposed it. The proposal was presented to the crypto industry on Monday and to banks on Tuesday. Some stakeholders “expressed pleasant surprise,” while others—including Coinbase—voiced concerns that the proposal may impose unintended, excessive constraints on stablecoin products and services.

V. Today’s Market Calendar

Data Release Schedule

| 20:30 | U.S. | Initial Jobless Claims (prior week) | ⭐⭐⭐⭐ |

| 22:00 | U.S. | Existing Home Sales (Feb) | ⭐⭐⭐ |

Key Event Preview

March 26 (Thursday)

- U.S. Initial Jobless Claims (20:30)—a high-frequency labor-market indicator;

- Multiple Fed officials’ speeches (Jefferson, Barr, etc.)—to clarify recent policy trajectory and inflation response;

- G7 Foreign Ministers’ Meeting (Mar 26–27)—watch for statements on the Middle East, Hormuz Strait, and energy supply.

March 27 (Friday)

- Final March University of Michigan Consumer Sentiment Index—assessing the impact of geopolitics and oil prices on consumer mood and inflation expectations.

In addition, ongoing U.S.-Iran negotiation updates remain critical: Monitor the latest statements from the White House and Iran. Any substantive progress—or reversal—could materially affect oil prices and global risk assets.

Institutional Views:

Morgan Stanley CIO Mike Wilson maintains his optimistic 20% 12-month S&P 500 earnings growth forecast, noting the current earnings upgrade trend closely mirrors historical post-recession recovery phases. Although U.S.-Iran negotiations remain fraught and military activity unchanged, signals of “productive contact” have already lifted U.S. equities for two straight days—and falling oil prices further ease inflationary pressure. Q1 earnings expectations have risen to 11.9%; the earnings season beginning in three weeks will be a crucial stress test. In crypto markets, BTC stabilized near $71,000, lifting total market cap; dominant short liquidations signal improving leverage sentiment. However, continued outflows from BTC/ETH spot ETFs warrant attention to institutional capital flows. Overall, institutions see the combination of temporary geopolitical relief and robust earnings expectations continuing to support risk assets—but warn that renewed oil spikes above $110/barrel, triggered by negotiation setbacks, could pressure both earnings and valuations. Investors are advised to closely track U.S. labor data, latest Middle East developments, and actual earnings-season results—and selectively capture structural opportunities in AI, aerospace, and CPUs amid volatility.

Disclaimer: The above content was compiled via AI search and verified manually for publication only. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News