Crypto VC Tells a $2 Trillion Story to Wall Street

TechFlow Selected TechFlow Selected

Crypto VC Tells a $2 Trillion Story to Wall Street

Wall Street looks toward cryptocurrencies; crypto VCs who haven't thrown in the towel are ready to double down.

By:律动 BlockBeats

Suddenly, what's drawing the most attention in the U.S. stock market seems no longer to be AI, but rather a pile of junk companies on the verge of delisting. Over the past several months, reverse mergers with ever-increasing amounts have been occurring at an unprecedented pace across the U.S. capital markets.

Publicly listed companies are completely abandoning their original core businesses and turning cryptocurrencies into their fundamentals, causing their stock prices to surge multiple times—sometimes even tens of times—within short periods. Now, the U.S. stock market has effectively become a playground for crypto圈 financial experiments. This time, crypto VCs have truly brought their narratives directly into Wall Street’s ears.

In the U.S. stock market, “igniters” are setting off DAT fireworks

Three months ago when investing in Sharplink, Primitive Ventures never expected this new crypto niche within the U.S. stock market to become so crowded in such a short period. "Back then, not many people were discussing these investment cases; it was incomparable to today's market heat—but we're really only talking about a span of one or two months," said Yetta, partner at Primitive.

In June this year, Sharplink Gaming announced it had completed a $425 million financing round, becoming the first U.S.-listed Ethereum reserve company. After the news broke, the company's stock price skyrocketed, surging over tenfold at one point. As the only Chinese-speaking fund involved in this deal, Primitive attracted significant attention within the industry.

"We realized that liquidity in the crypto market isn't great, yet institutional buying power is extremely strong. Bitcoin ETF volumes remain solid, and open interest (OI) for Bitcoin options on CME has even surpassed Binance," said Yetta. In April last year, Primitive held an internal meeting for a major review, after which they established a new investment direction focused on the convergence of CeFi (Centralized Finance) and DeFi (Decentralized Finance). Today, they’ve become among the busiest VCs in the crypto space.

Nowadays, Primitive receives emails daily from investment banks inviting them to participate in investments in digital asset reserve companies. In this new wave of investing, investment banks act as intermediaries organizing deals, responsible for helping projects identify and coordinate all investors, while also assisting teams with investor roadshows.

In the past month alone, Primitive has spoken with no fewer than 20 cryptocurrency reserve projects. However, currently, they have publicly disclosed participation only in Sharplink and another Litecoin-reserve company, MEI Pharma. This cautious investment approach stems from concerns about market overheating. Since May this year, the team has begun closely monitoring various topping signals.

"We definitely feel that the current level of market frothiness is significantly higher than just a few months ago," Yetta told Beating. The team now produces daily market reports and continuously evaluates appropriate exit strategies based on evolving conditions. "Digital asset reserve companies represent financial innovation—you can maintain a long-term bullish view on their underlying assets, but there’s also significant risk of deleveraging and bubble bursting during market downturns."

Unlike Primitive, Pantera is rolling up its sleeves to go all-in. This 12-year-old veteran crypto VC has even coined a new term for this domain—DAT (Digital Asset Treasury). In early July, Pantera launched a new fund named the DAT Fund.

In the fundraising memo, Pantera partner Cosmo Jiang wrote: "As an investor, it's rare to find oneself at the beginning of a new investment category. Recognizing this moment and acting swiftly to seize early opportunities is crucial."

The story Pantera tells investors is very simple: If a company increases its per-share bitcoin holdings (Bitcoin Per Share) every year, owning shares in that company means you’ll end up holding more and more bitcoin over time.

Companies like MicroStrategy—the pioneer of Bitcoin treasury strategies—and other crypto reserve firms operate under a basic logic: when their market cap trades at a premium to the value of their on-balance-sheet crypto assets, they use financial instruments such as private placements, convertible bonds, and preferred stock to raise capital from the market and purchase additional crypto assets. Because of the stock premium, these companies can accumulate larger quantities of assets at lower effective costs.

Investors typically use the mNav metric (Market Cap to Net Asset Value) to measure this premium multiplier and assess a company’s fundraising capacity. "Clearly, stock markets are volatile—sometimes certain assets get overvalued. By activating financial tools during those times, you’re essentially selling volatility. From this perspective, premiums can potentially be sustained long-term," Cosmo told Beating.

In April this year, Pantera invested in Defi Development Corps (DFDV), a company reserving Solana’s native token SOL. It became the first U.S.-listed firm to use a cryptocurrency other than Bitcoin as a reserve asset. Its share price has since surged over 20-fold in the past six months.

However, for Pantera, this was absolutely a contrarian bet—initially, virtually no one else wanted to invest. Nearly the entire $24 million financing came from Pantera itself.

Most DFDV members come from senior roles at Kraken, and the CFO previously operated a Solana validator node. Their deep understanding of Solana and professional competence in traditional finance were key factors convincing Pantera. "Even so, we did build in some downside protection mechanisms into the deal structure, but DFDV’s astonishing success was something we never anticipated."

"I believe the real catalyst was Coinbase’s inclusion in the S&P 500 index—it forced every fund manager around the world to start considering crypto." Since Trump’s re-election, the crypto industry has made rapid advances in traditional capital markets. Circle’s IPO drew global attention to stablecoins, while Robinhood’s move into RWA pushed security tokenization into the spotlight. Now, DAT has emerged as the next接力 concept.

Less than a month after investing in DFDV, Cantor Equity Partners (CEP) came knocking. DFDV’s success accelerated SoftBank and Tether’s plans for a Bitcoin reserve company, ultimately enabling CEP to privately raise approximately $300 million in external funding—with Pantera again becoming its largest outside investor.

The capital for Pantera’s investments in both DFDV and CEP came from its flagship Venture Fund and Liquid Token Fund. Initially, the team assumed these would be the only two investments they’d make in this space.

But market developments quickly exceeded Pantera’s expectations. Due to limitations in portfolio concentration and framework constraints within these two funds, Pantera soon decided to launch a dedicated new fund.

On July 1st, the DAT Fund began fundraising with a target of $100 million. On July 7th, it officially announced completion. Due to overwhelming LP enthusiasm, Pantera subsequently launched a second DAT Fund. By mid-month, when interviewed by Beating, the first DAT Fund had already fully deployed all its capital.

In publicly disclosed cases, Pantera often plays the role of “Anchor”—the largest contributor. Since DAT companies initially suffer from poor liquidity, leading to potential discounts, the team needs to first bring in heavyweight investors off-market to establish a foundational base, ensuring improved liquidity and narrower spreads.

On the other hand, being an “Anchor Investor” is also part of Pantera’s market strategy. "Over the past two months, we've received nearly a hundred proposals from DAT companies. Pantera is usually the first call they make because we entered early and gained cognitive leadership in this field. And they see that when we commit, we do so meaningfully—we’re willing to write big checks."

Of course, Pantera doesn’t invest in every single opportunity. For DAT companies, the fund equally values their ability to create “cognitive leadership” through marketing. Their investments in Sharplink and Bitmine were largely driven by such considerations. Among them, Bitmine was the first investment of the DAT Fund, where Pantera again played the “Anchor” role.

On June 2nd, Joseph Lubin, a core figure in the Ethereum community, led the reverse acquisition of Sharplink, giving birth to the first Ethereum reserve company. On June 12th, Lubin and other Ethereum leaders released an Ethereum fundamentals report via Etherealize, introducing Ethereum’s investment value to institutional investors.

On June 30th, the second Ethereum reserve company, Bitmine, was born. “Wall Street crypto expert” Thomas Lee publicly endorsed it and began making frequent appearances in mainstream media, explaining Ethereum’s investment potential. Around the same time, Sharplink’s stock price started climbing, and the “Ethereum arms race” rapidly became the hottest topic in the industry.

"To truly unlock financial leverage, a DAT company’s market cap needs to reach at least $1–2 billion," Cosmo told Beating. Only at this scale can a company achieve sustainable valuation premiums and open another door to institutional capital through instruments like convertible notes or preferred shares.

But before that, DAT companies must first tell their story effectively—not just to native crypto investors, but to a broader base of mainstream retail investors in the stock market. "You need them to understand the narrative and want to participate. The market must first ‘believe it will happen’ for the entire model to work."

Another critical factor for DAT success is building sustained trust with the market. Traditional finance demands “transparency + discipline.” Teams must be deeply crypto-native while also possessing sharp instincts in traditional finance, managing disclosures properly, understanding SEC rules and procedures, to ensure efficient and professional access to U.S. capital markets.

"We spend a lot of time on due diligence. What matters isn’t just the static mNav number. Does the team have a clear management structure? Can they raise capital consistently? Do they have the capability to build new business models? These are the traits of a truly outstanding ‘DAT founding team.’"

Beyond Bitcoin, Ethereum, and Solana reserves, Pantera has recently invested in several other large-cap altcoin reserve companies. From Bitcoin to major coins, then to altcoins, the narrative evolves progressively: while Bitcoin DAT relies entirely on financial engineering for growth, major coin DATs can generate yield through staking and DeFi activities, and altcoin protocols offer mature applications and revenue streams on-chain as fundamentals—allowing stock market investors to gain exposure to their growth via DAT.

Different from Bitcoin and major coin DATs, many altcoin DATs receive their initial reserves directly from protocol foundations or their token investors.

Sonnet BioTherapeutics (SONN), the strategic reserve company for Hyperliquid, received its initial reserve when top crypto VC Paradigm directly injected over 10 million HYPE tokens purchased late last year. According to Beating, StablecoinX—the strategic reserve company for Ethena—was also initiated by the Ethena Foundation, allowing PIPE round investors to contribute using either their ENA tokens or USDC.

Due to weaker liquidity, altcoin DATs often experience massive price spikes immediately after funding announcements—creating insider trading opportunities for those with advance knowledge. In the case of SONN, the official announcement came on July 14th, but the stock began rising sharply from July 1st, quadrupling in price before the public reveal.

Recently, CEA—a BNB reserve company backed by YZi Labs—faced a similar issue. To prevent participants from learning the company name prematurely, the team reportedly purchased several U.S. shell companies in advance and randomly selected one at the last moment. Even so, front-running occurred hours before the official July 28th announcement.

On the other hand, many investors worry about potential “self-dealing” risks in altcoin DATs. Given weak liquidity in crypto markets, large-cap, high-priced tokens are difficult to exit without steep discounts. But by injecting these assets into a DAT company, artificial on-chain liquidity becomes real liquidity in the U.S. stock market.

Therefore, whether this represents “providing growth exposure” or merely “seeking exit liquidity” requires careful discernment by investors. "Many DATs operate in regulatory gray zones, such as listing on low-barrier exchanges. But such short-term operations struggle to establish stable disclosure and compliance frameworks. Without genuine capital premiums, it’s just musical chairs."

Regulatory risk is another challenge for DAT companies. If the SEC classifies altcoins or other on-chain assets as securities, DAT structures would require major adjustments. Still, both Primitive and Pantera believe this remains a superior battlefield. "Because U.S. equity markets offer far better liquidity, and public company investors enjoy greater protections, doing DAT investments now offers better odds and payoffs compared to pure crypto investing," said Yetta.

Beyond the U.S. market: racing to become the next MicroStrategy

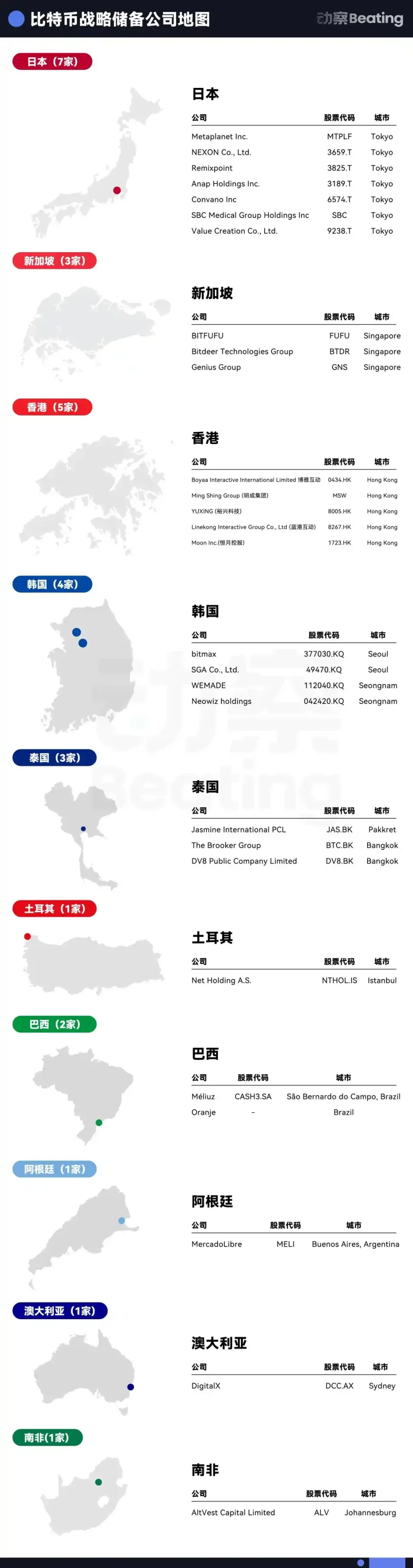

The U.S. stock market is widely recognized as the most efficient, inclusive, and liquid capital market—an accepted truth among investors. For replicating the next MicroStrategy, Nasdaq remains the optimal venue. But that doesn’t mean other markets lack opportunity. Outside the U.S., players aim to become the next Metaplanet.

Over the past year, Metaplanet’s stock premium has steadily climbed, delivering investors over 10x returns. This explosive “Asian miracle” has revealed regional arbitrage opportunities to more people.

Asia pioneered Bitcoin treasuries. Mid-2023, Waterdrop Capital partnered with China Pacific Investment Management (Hong Kong) Ltd. to establish the Pacific-Waterdrop Fund, later taking a stake in Boyaa Interactive, a Hong Kong-listed company that had just begun purchasing Bitcoin. In 2024, as MicroStrategy’s stock surged, Waterdrop grew even more confident in this trend. Currently, Waterdrop holds stakes in five Hong Kong-listed firms and plans to increase that to at least ten by year-end.

"Clearly, the U.S. market for Bitcoin and major coin reserve companies is now extremely crowded. The next wave of growth is more likely to come from capital markets outside the U.S.," said Nachi, a crypto trader who has now joined the reserve company investment wave. Earlier this year, he participated in the investment in Nakamoto Holdings, a Bitcoin reserve company, quickly earning a 10x return.

At the beginning of the year, Nachi joined Mythos Venture as an individual LP. The fund focuses exclusively on “Asian Bitcoin reserves,” with its latest deal being DV8, a Thai-listed company that recently raised 241 million Thai baht, becoming Southeast Asia’s first Bitcoin reserve company.

In addition, he has personally invested in several other regional Bitcoin reserve projects, mostly with seven-figure USD amounts. For example, Oranje, Latin America’s first Bitcoin reserve company acquired in April, received support from Brazil’s largest commercial bank, Itaú BBA, and raised nearly $400 million in its first round.

"We believe there’s room in Japan, South Korea, India, and Australia to build such Bitcoin reserve companies," said Nachi. After joining Mythos, his role gradually shifted from LP to “quasi-GP,” evaluating investment opportunities alongside other members. His task now is identifying public companies interested in takeovers—“shell owners” in Asia have become his most frequent meeting targets lately.

“Being first” is key to winning in non-U.S. capital markets. It allows teams to build first-mover advantages and capture greater market attention. But it also means that regional arbitrage in the Bitcoin reserve narrative is a race against time.

Shell companies vary greatly in acquisition cost—one might be bought for $5 million, while the DV8 deal in Thailand involved participating parties spending around $20 million.

From shell acquisition to listing and trading, the entire process generally takes one to three months, with regulatory approval efficiency being the main variable. However, going from spotting an opportunity to full execution typically takes at least six months—or even longer.

The DV8 acquisition took nearly a year from start to finish, only officially completing in July this year. The deal was led by UTXO Management and Sora Venture, the same entities behind Metaplanet’s transformation.

Recently, Sora also orchestrated the acquisition of SGA, a South Korean software services firm. "Asia, especially Southeast Asia, has relatively closed capital markets, but the volume here is actually huge—many foreign investors simply don’t understand how active these markets are," Luke, partner at Sora Ventures, told Beating.

"Everyone’s racing against time now, but in Asian markets, I believe few can compete with Sora." In Luke’s view, local regulations pose a major barrier for most overseas capital. Most VCs lack full experience in acquisitions and regulatory communications and fundamentally don’t understand Asian markets.

Sora Ventures’ strategy involves bringing in numerous local partners to facilitate connections with stock exchanges and regulators, accelerating project launches. In the SGA deal, the team went from initial talks to final agreement in under a month—setting the fastest acquisition record in the history of the Korean Stock Exchange.

A company’s fundraising rhythm and market strategy form another barrier. "mNav is a late-stage valuation model—it only makes sense once Bitcoin holdings reach a certain scale. Early-stage companies operate under completely different logic compared to MicroStrategy." Thanks to super-voting rights structures, U.S.-listed DAT companies can continuously dilute shares while maintaining control.

But most Asian public companies lack such mechanisms, limiting the team’s ability to dilute. This means teams must precisely time fundraising rounds and may need to repurchase shares using cash flow from core operations to achieve reverse dilution. DV8 in Thailand, for instance, has already obtained relevant local licenses and will soon launch a cryptocurrency exchange platform.

Currently, Sora is accelerating a planned acquisition in Taiwan’s market and advancing a second Bitcoin reserve company in Japan. In May, the team acquired a 90% stake in Top Win, a Hong Kong-based luxury distributor listed in the U.S., which will soon be renamed Asia Strategy. "Our goal is to create nine or ten ‘Metaplanets’ across Asia and consolidate them under a U.S.-listed parent company, allowing U.S. market investors to gain indirect exposure to Asian premium valuations."

Top Win participated in the acquisitions of Metaplanet, Evermoon Holdings, DV8, and SGA. It is expected to complete its initial fundraising round soon, with Sora Ventures continuing its “multi-player + small capital” model—total fundraising under $10 million and a six-month lock-up period.

Luke hopes Top Win will eventually adopt a capital structure consisting of 30% ownership in Asian companies and 60% Bitcoin reserves, crafting a distinct narrative for investors. Of course, all of this remains just vision and storytelling—the sustainability of Asian market premiums and whether U.S. investors will buy into the Asian narrative remain to be tested by time and the market.

"We must admit that in Asia, the floor is high but the ceiling is low. To truly reach scale, you ultimately need to be in the U.S. market, where you attract global investors and players," said Nachi. While investors chase Alpha through Bitcoin reserve narratives globally, there’s a shared consensus: the underlying Beta still hinges on favorable U.S. regulatory developments.

"If national Bitcoin reserve legislation actually passes, government purchases in the U.S. would trigger synchronized allocations by regional governments and sovereign funds worldwide—potentially driving Bitcoin prices upward indefinitely," Nachi added.

People saved by “crypto stocks”

Compared to the bleak state of the crypto market, the current DAT sector appears exceptionally vibrant. This new wave not only captures attention but also seems to offer trapped crypto capital an “escape route.” "Almost every top 100 market-cap crypto project is now considering launching a DAT," an investor told Beating.

From late 2024 to early 2025 marked a critical juncture when many crypto VC funds reached maturity and began new fundraising cycles—yet poor DPI figures deterred many LPs. Since the beginning of the year, numerous crypto funds have shut down.

Since 2022, valuations in crypto’s primary market have inflated continuously, with many projects raising millions in seed rounds despite having little actual innovation or real-world application. With the rise of crypto ETFs and FinTech+Crypto, VCs have become LPs’ last choice for crypto allocation.

Meanwhile, shrinking market liquidity has made exits increasingly difficult. Retail investors no longer buy into “VC coins,” while projects face high listing fees to get onto exchanges. "Now, getting listed on a top-tier exchange usually requires giving up at least 5% of your token supply—costing $5 million at a $100 million valuation. That’s roughly the same price as acquiring a U.S. shell company."

But the opening of the U.S. regulatory environment has brought new hope. Crypto reserve companies not only provide the best exit path for tokens but also offer a fresh narrative to attract institutional capital into the crypto ecosystem.

Beyond crypto VCs, mid-tier investment banks have also benefited from this boom. According to Bloomberg, DAT deals now occupy 80% of many mid-tier brokers’ workloads, with business in this area expected to grow 300% by year-end.

The industry now wishes to migrate the entire $2 trillion crypto market into U.S. equities. Within less than two months, dozens of DAT companies have emerged.

According to Pantera’s vision, the DAT sector will undergo major consolidation within three to five years. When downturns arrive, smaller DAT companies unable to achieve economies of scale will fall into negative premium territory and be acquired at rock-bottom prices by larger rivals. "DAT is an ‘experimental field for a new treasury model,’ not a center for technological innovation. Ultimately, only two or three companies will survive."

But for now, the music has just begun. Cosmo believes it will be at least another six months before the sector reaches peak intensity. "Who will ultimately win remains completely unknown. All we can do is back the teams we believe have a chance of becoming one of those final ‘two or three.’"

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News