Citi: Dollar stablecoins "reflect rather than reinforce" the dollar's status, while non-dollar stablecoins are a key indicator of "de-dollarization"

TechFlow Selected TechFlow Selected

Citi: Dollar stablecoins "reflect rather than reinforce" the dollar's status, while non-dollar stablecoins are a key indicator of "de-dollarization"

U.S. Treasury demand will not increase significantly in the short term due to stablecoin growth, while the relative growth of non-U.S. stablecoins will become an important indicator for monitoring de-dollarization trends.

Author: Xu Chao, Wall Street Insights

Will demand for U.S. Treasuries significantly increase in the short term due to stablecoin growth?

According to Wind Trading Desk, Citigroup stated in a report on June 20 that the rise of dollar-based stablecoins reflects rather than drives the U.S. dollar's reserve status. Demand for U.S. Treasuries will not substantially increase in the short term due to stablecoin expansion. Instead, the relative growth of non-U.S. dollar stablecoins will serve as an important indicator of de-dollarization trends.

Stablecoin Growth Unlikely to Materially Boost Treasury Demand

The GENIUS Stablecoin Bill has passed the Senate, and the STABLE Act in the House has cleared committee. Citigroup views these developments as critical steps toward regulatory clarity for digital assets in the U.S., providing a positive catalyst for the industry. Legislative approval represents a key milestone in establishing a comprehensive regulatory framework, which could accelerate broader adoption of stablecoins.

Markets widely debate whether stablecoins could become a new source of demand for U.S. Treasuries—and thereby reinforce the dollar’s global standing.

Citigroup's analysis yields a conditional answer: "both yes and no." The crucial factor lies in the funding source. If newly issued stablecoins are backed by transfers from existing bank deposits or money market funds, there would be no net new demand for U.S. Treasuries.

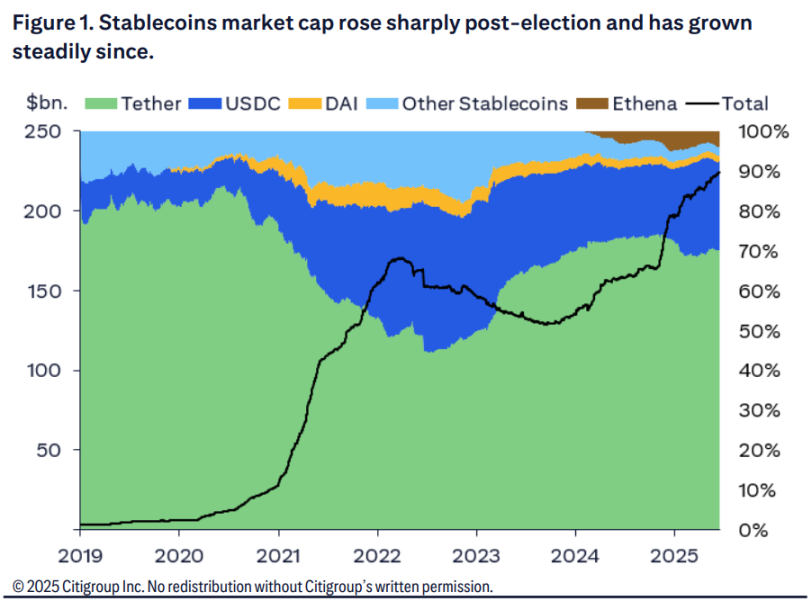

Currently, Tether and Circle primarily hold U.S. Treasuries and use repurchase agreements to collateralize their assets.

Citigroup believes that in the near term, before stablecoins achieve wider adoption, their growth will not significantly increase demand for U.S. Treasuries. Current stablecoin expansion may divert funds from bank deposits (reducing banks’ demand for Treasuries) and/or money market funds (directly reducing Treasury demand). If stablecoins begin offering interest, they could see larger-scale growth—but this too would likely come at the expense of existing holders’ allocations.

The source of stablecoin growth is critical. If growth stems from fund flows out of other Treasury-holding instruments such as money market funds (MMFs), it does not represent net incremental demand.

Citigroup estimates that under a base-case scenario, the potential long-term size (by 2030) of the stablecoin market could reach $1.6 trillion. Only portions originating from reallocations of physical U.S. cash ($240 billion), global M0 currency reallocations ($109 billion), and shifts from foreign-held deposits ($273 billion) would constitute genuine incremental demand for U.S. Treasuries.

Non-Dollar Stablecoins Emerge as Key Indicator of De-Dollarization

Citigroup maintains that the U.S. dollar’s dominant reserve role will persist—with or without stablecoins. In terms of reserve diversification, the euro stands as the only plausible long-term competitor.

Based on current trends, Citigroup projects the dollar will remain the dominant reserve currency through 2070. Even under aggressive assumptions—dollar share declining by 12.5% annually and euro share rising by 5% annually—this dominance would endure until 2046.

Citigroup emphasizes that relative issuance trends in stablecoins will provide an interesting lens through which to track shifts in dollar dominance. Since the launch of euro-denominated stablecoins under Europe’s MiCA regulation, their market capitalization has increased—coinciding with a weakening dollar and cracks in the “American exceptionalism” narrative.

Currently, euro stablecoins represent only a tiny fraction of dollar stablecoins, despite the dollar accounting for about 50% of global reserves and nearly 80% of foreign exchange transactions. This suggests stablecoin adoption may present both opportunities and risks to dollar dominance.

Analysts expect the dollar’s leading position to remain intact in the foreseeable future. The dollar’s entrenched reserve status and network effects mean dollar-based stablecoins are likely to continue dominating the market. However, the relative popularity and issuance volume of non-dollar stablecoins will serve as an intriguing barometer for monitoring de-dollarization trends.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News