After researching 100 yield-generating stablecoins, we identified 5 with promising potential

TechFlow Selected TechFlow Selected

After researching 100 yield-generating stablecoins, we identified 5 with promising potential

Stablecoins are becoming a market consensus.

By: Zuoye

Stripe's acquisition of Bridge is just the beginning. Huma using stablecoins to replace banking intermediaries, and Circle rising as the new crypto darling after Coinbase with USDC—these are all clumsy imitations of USDT.

Ethena has leapfrogged ahead; MakerDAO rebranded to Sky and pivoted to yield-bearing stablecoins; Pendle, Aave, and others are rapidly undergoing USDC → PT/YT → USDe transformations. This summarizes recent developments in on-chain stablecoins.

At least for now, YBS (Yield-Bearing Stablecoin) still falls under the broader stablecoin category. It’s hard for most people to grasp the fundamental difference between USDe and USDT. In my view, projects like USDe use yield incentives to attract users, distributing part of asset returns to depositors, then reinvesting those deposits to generate further yield.

Previously, issuing USDT was an act of creating a new asset. Tether’s reserves are managed by regulators or the issuer itself, with no involvement from users. Users could only passively accept that 1 USDT equals 1 USD and hope others would too.

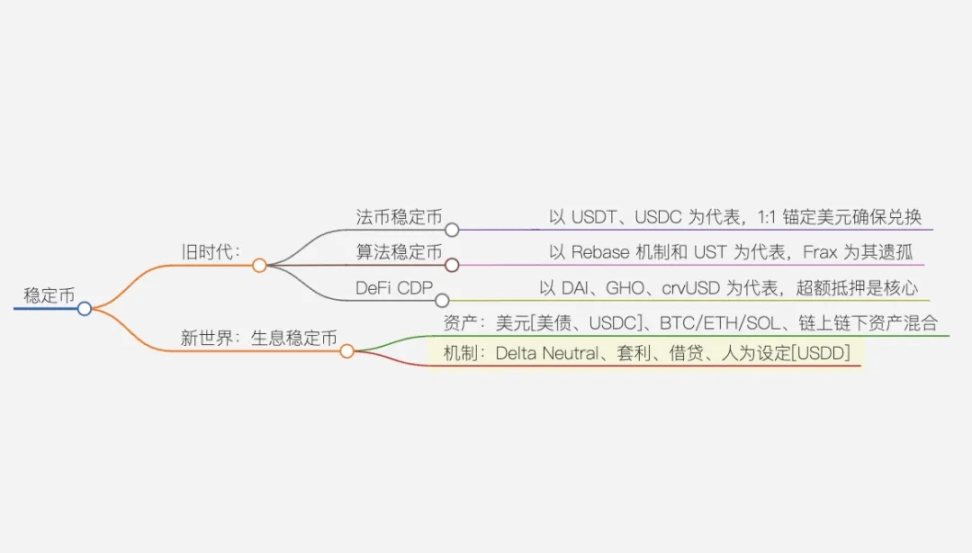

Caption: Stablecoin Classification

Image Source: @zuoyeweb3

YBS follows the on-chain bank model of deposit-taking and lending, decentralizing the power of asset issuance. Creating USDC requires political-commercial cooperation and exchange support, but YBS projects are exploding in number.

Let me reiterate: the history of crypto is the history of innovation in asset issuance models. This time it’s done under the banner of “stability,” making it seem milder than previous waves like ERC-20, NFTs (ERC-721), or Meme Coin on-chain PvP.

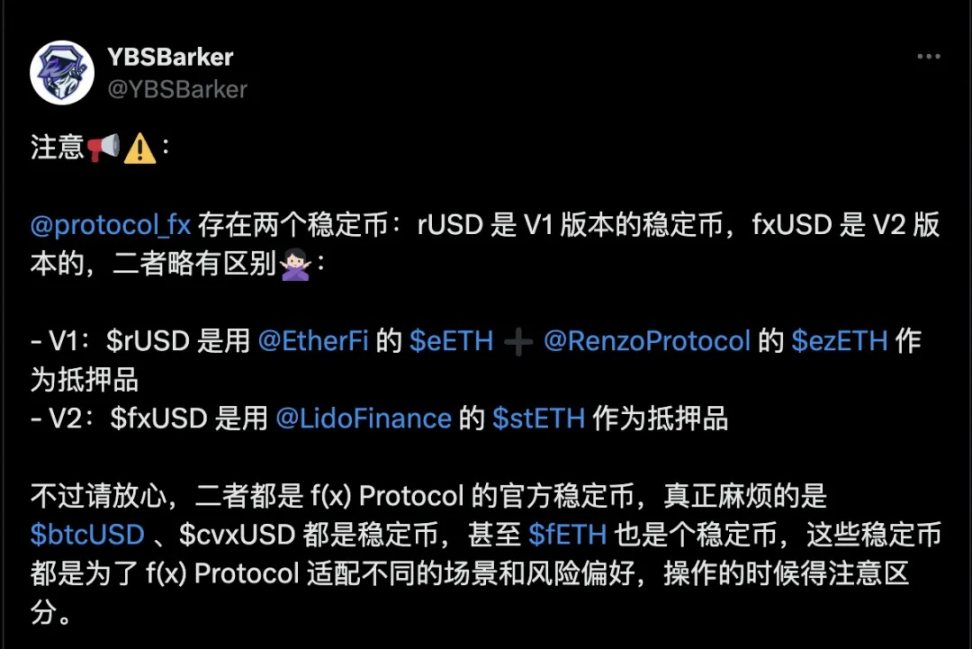

Take f(x) Protocol as an example—it has at least five stablecoins: rUSD and fxUSD from V1 and V2 respectively, plus $btcUSD, $cvxUSD, and even fETH is considered a stablecoin because it captures only part of ETH’s volatility to maintain price pegging, while the residual volatility is absorbed by xToken.

Caption: Multiple Stablecoins in f(x) Protocol

Image Source: @YBSBarker

Stability arises from volatility—volatility creates stablecoins.

Sailing from the Old World to the New Continent

Whether called yield-bearing stablecoins or StableFi, these are new expressions of stablecoins. Let’s briefly trace their origins.

Stablecoins originated within Bitcoin—the peer-to-peer electronic cash payment system. But Bitcoin isn’t stable. That’s not due to design flaws; Bitcoin is fundamentally an unpegged monetary system whose fair value continues fluctuating, unable to stabilize in the short term.

The earliest attempt at USDT occurred in the Bitcoin ecosystem before shifting into exchange pricing domains. The golden combo of Bitfinex and Tether gave stablecoins their first home—much like today’s Coinbase and Circle partnership.

Fiat-backed stablecoins were thus born. Their mechanism is simple: you just need to trust Tether Inc., and everyone must agree on USDT’s market stability. First-mover advantage allowed Tether to achieve profit margins higher than BlackRock.

Closely following was DAI issued by MakerDAO. For years, the over-collateralized mechanism (CDP) remained the sole option for on-chain stablecoin issuance. A 1.5x collateral ratio limits capital efficiency but grants greater credibility to market participants.

From an on-chain perspective, much of crypto’s subsequent history has been about reducing collateral ratios. Financial alchemy works both ways—Hyperliquid can amplify trading leverage, but there hasn’t been a good way to leverage asset creation.

Caption: Main Algorithmic Stables in 2022

Image Source: stablecoins.wtf

UST marks a tragic chapter in algorithmic stablecoins—the classic model collapsed. Frax is at best semi-algorithmic, more accurately described as hybrid—and effectively just a USDC wrapper now.

In terms of mechanisms, yield-bearing stablecoins require both yield generation and price stabilization. Any of the three existing approaches work: DeFi giants’ CDP systems, Ethena’s delta-neutral strategy, or even USDD stabilized by SBFG’s promise—as long as the market accepts it.

The real distinction lies in yield distribution mechanisms, which depend on the source of yield-generating assets. Two simplest methods exist: using staked assets like stETH on-chain, or off-chain instruments like U.S. Treasuries that inherently yield returns. These can also be combined.

Ethena’s USDe is special: it uses stETH for yield while relying on CEX hedging to maintain price stability. It also requires off-chain entities for compliance and partially backs reserves with USDC. As always, everything can be mixed—no strict boundaries between mechanisms or assets.

If Ethena used only ETH assets, hedged entirely on Hyperliquid, and distributed yields fully on-chain, it would represent the ideal native on-chain yield-bearing stablecoin.

Unfortunately, such a project doesn’t strictly exist yet.

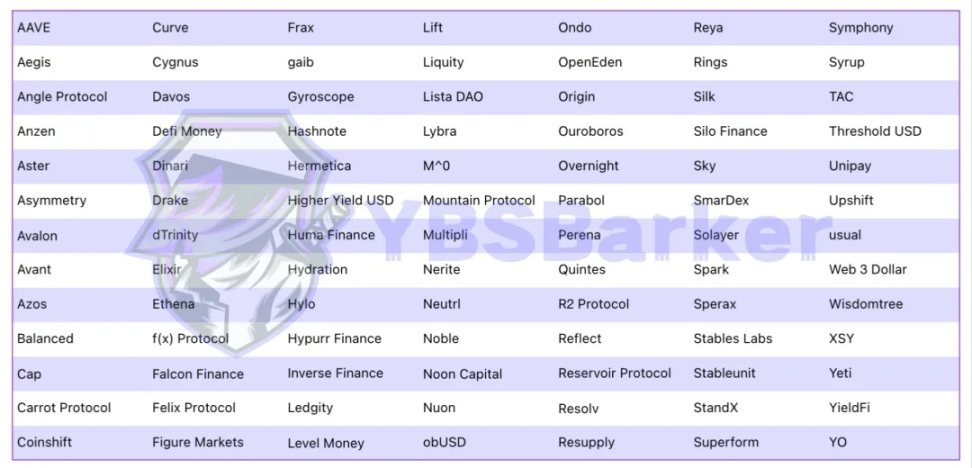

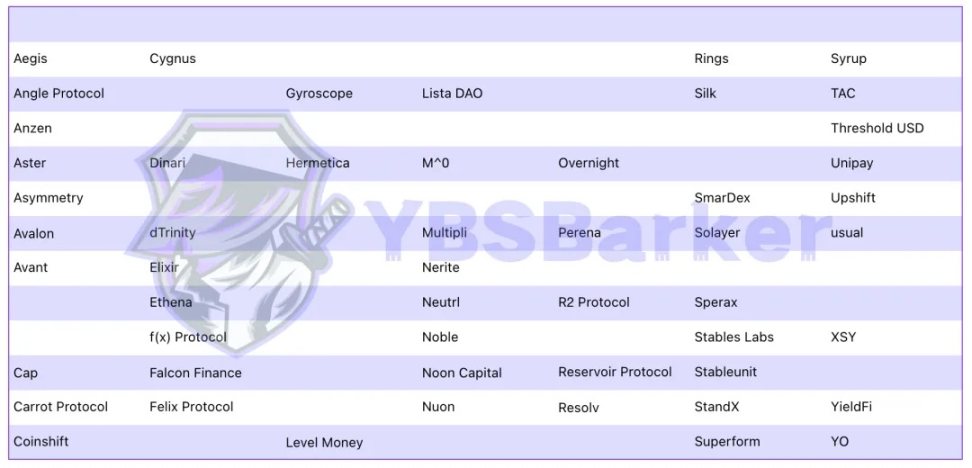

Caption: List of Yield-Bearing Stablecoin Projects

Image Source: @YBSBarker

We’ve compiled 91 such projects here. Adding USDT, USDT0, USDC, PYUSD, and USDD makes rounding up to 100 easy.

In fact, according to RootData, 181 projects involving stablecoins have been cataloged so far, while DefiLlama lists 259. However, excluding non-yield-bearing ones, the active mainstream options are mostly covered here.

Sorted alphabetically by protocol rather than stablecoin, focusing on protocols gives better clarity. Strictly speaking, USDe isn't a yield-bearing stablecoin—sUSDe fits the definition. A complete yield-bearing stablecoin protocol tokenomics should look like this:

1. The stablecoin and its staked version, e.g., USDS and sUSDS

2. The protocol’s main token and its staked version, e.g., ENA and sENA

Additionally, focusing on protocols better reflects the distinction: "protocols distribute yield, stablecoins are yield receipts." Drawing from past asset issuance innovations, high-potential projects in any sector rarely exceed five—true for blockchains, DeFi, L2s, wallets, inscriptions, runes, meme coins, etc.

Yield-bearing stablecoins occupy a complex intersection where DeFi, RWA, and stablecoins pull against each other. Protocols like Aave’s GHO (ERC-20) and sGHO (ERC-4626), or Curve’s crvUSD and scrvUSD, mainly reinforce their own ecosystems without aggressively challenging USDe or USDS market share.

So the real question becomes: beyond USDS and USDe, how much space remains for emerging YBS protocols?

We applied preliminary filtering to the list of 91 protocols based on subjective criteria:

1. Established DeFi protocols not centered on YBS—like Aave, whose core remains lending;

2. Inactive projects—the most subjective criterion:

• Not yet launched on mainnet (will update later)

• Bandwagon projects—copying 2022 DeFi giants launching stables, 2023 Ethena-style delta hedging, or current trends

• Acquired or already ceased operations

3. No funding or backup—perhaps struggling to survive, but stablecoin projects need reserves. Lack of funding indicates lack of confidence from Tier 1 investors, making technical superiority or community-driven large TVL unlikely.

Note: Projects like Trump family-affiliated WLFI’s USD1 resemble USDT more closely and aren’t meaningfully related to yield-bearing stablecoins—excluded from discussion.

Caption: Post-Filter Projects

Image Source: @YBSBarker

These remaining 52 projects form the actual competition for the final spots in the YBS race—for instance, we directly excluded Polkadot’s Hydration. Surely no one still expects Polkadot to revive?

Another example: Figure Markets’ YLDS represents the opposite of on-chain yield-bearing stablecoins, yet holds legal registration and serves traditional finance clients with strict compliance needs. Detailed exclusion reasons are available in our Feishu document.

After rough filtering, we assess details across three dimensions: fundamentals, yield mechanism, and APY.

• Fundamentals: official website, Twitter, contract address (CA)

• Yield Mechanism: strategy & actions, yield sources, distribution method, rewards

• APY calculation method

A brief note: “strategy” refers to the financial strategy behind the YBS, “actions” are concrete operational steps, “yield sources” refer to where protocol revenue comes from, and “distribution” usually involves rewarding stakers—but specifics vary per case and won’t be elaborated here.

Take Avalon as an example: its stablecoin is USDa, and yield-bearing version is sUSDa. Details include:

• Yield Sources: interest income from USDa borrowing + revenue from USDa Lend service

• Strategy: stake USDa/sUSDa LP tokens in KodiakFi (Berachain ecosystem)

Avalon is particularly typical—it relies on Pendle. In today’s YBS ecosystem, the Pendle-Aave combo benefits more than Curve ever did at its peak. I’ll leave that hole for future exploration.

Naturally, this leads to assessing security and stability of emerging protocols. Sui’s Cetus serves as a cautionary tale—a two-hole disaster (Cetus compensation claims open today 😭).

From DeFi Lego to YBS Building Blocks

Reaching the new continent doesn’t mean victory—survival crises become even more urgent.

Still too many players. Let’s apply endgame thinking to narrow down. Referencing YBSBarker’s data and on-chain metrics, we select 12 protocols based on underlying assets, core mechanisms, and quantitative indicators like TVL.

Caption: Final 12 Selected Projects

Image Source: @YBSBarker

Important: this reflects current market conditions, not a guarantee these projects will win. Beyond DeFi giants and institutional adoption, these 12 primarily compete for retail use cases—interest accrual, pricing units, and payments—the hardest yet most rewarding battleground.

Ethena might envy Sky most: backed by Treasury yields and DAI’s established user base, combining yield and stability to instantly become Ethena’s strongest rival.

Caption: Parameters of Selected Projects

Image Source: @YBSBarker

Looking at the remaining 12 contenders, one thing is clear: yield really is a customer acquisition tool.

Like early DeFi Lego blocks, YBS protocols constantly compose with other protocols. Multi-chain, multi-protocol, multi-pool setups are standard. Every YBS structure and every yield farmer focused on YBS operates with transferable knowledge—all ultimately contributing TVL and revenue to Pendle.

Remember earlier talk about leverage in asset creation? In YBS, that role belongs to Pendle—not Ethena or other YBS protocols. Everyone’s working hard just to enrich Pendle.

There remain serious issues: given YBS is still in early stages, many flaws are tolerable. But sustainability of yields remains questionable. Sky allocated $5 million in profits to USDS holders, leaving almost no protocol profit—essentially losing money to gain attention.

Besides, most YBS protocols issue a native token—like ENA or Resolv, which recently went live. Their token prices rely on protocol revenue and yield-sharing capacity. If the token price drops, it drags down confidence in the yield-bearing stablecoin itself.

In other words, expanding YBS scale doesn’t necessarily boost the protocol token if net profits are low. Conversely, falling token prices trigger risk-off behavior, causing liquidity withdrawal from the stablecoin—potentially spiraling into a death loop akin to UST.

The takeaway: we must monitor protocols’ sustainable profitability. Since YBS projects function as crypto banks via deposit-taking and lending, principal safety is paramount. YBSBarker’s Protocol Revenue metric will keep tracking protocol safety, while Yield Sharing Ratio monitors payout levels.

Now entering hot takes—no objectivity here, purely subjective views.

Beyond Sky and Ethena, which emerging YBS protocols hold breakout potential?

I pick Resolv, Avalon, Falcon, Level, and Noon Capital. No scientific basis—just gut feel, call it “project vibes.”

Caption: Potential Leaders

Image Source: @YBSBarker

One common misconception: YBS projects rushing to launch tokens are bad. Not necessarily true. There are indeed scammers, but for YBS, secondary market liquidity for the protocol token is essential. Ethena secured top-tier exchange-affiliated VCs, forming de facto alliances—effectively ceding some USDe minting rights.

But minting power is tied to ENA. Institutional investors want returns, so they won’t dump USDe—that would sink their own investments. Stablecoins exist in binary states: 0 or 1. But ENA can be slowly sold or staked for yield. That’s Ethena’s master-level playbook.

Circle brute-forced money to Binance and Coinbase; Ethena adopted a more crypto-native “bribery mechanism”—just like Curve Wars. Game theory beautifully reused.

Conclusion

This was just an appetizer. After this broad overview, I hope readers now have a holistic sense of today’s YBS landscape—not thinking building a YBS is as distant as creating a USDT, nor mistaking YBS for the next Meme Coin.

The trust and capital reserves required for YBS far exceed what memes can offer. Always remember: YBS is a form of money. Especially true YBS not backed by Treasuries or dollars—they’re not far off in credibility from BTC/ETH themselves.

Next, I’ll dive deeper with a detailed guide on launching yield-bearing stablecoins. All mechanisms and nuances left out here will be thoroughly explained.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News