Deconstructing the "Colossal Scam" Claim About Bitcoin: A Deep Dive from Allegations to Rebuttals

TechFlow Selected TechFlow Selected

Deconstructing the "Colossal Scam" Claim About Bitcoin: A Deep Dive from Allegations to Rebuttals

The article uses rational analysis to refute these arguments, emphasizing market complexity, improved transparency, and the multifactorial drivers of Bitcoin's value.

Author: Luke, Mars Finance

In the world of finance—especially in the emerging and uncertain realm of cryptocurrency—interpretations and speculations abound. Among them, "conspiracy theories" often attract massive attention due to their dramatic and inflammatory nature. When markets experience sharp volatility or when certain narratives contradict intuitive perceptions, stories about "hidden hands" or "carefully orchestrated scams" find fertile ground. Recently, a narrative portraying the Bitcoin market as a "house of cards" built by insiders relying on fabricated demand and endless money printing has reignited widespread debate, directly targeting industry players such as Tether and Bitfinex.

These claims typically take real doubts or controversies within the market and amplify or link them into a seemingly coherent but logically flawed and evidentially weak storyline. As rational observers and responsible media, we must look beyond these sensational surfaces, critically examine the core arguments of such so-called "conspiracy theories," clearly identify their specific allegations, and evaluate them based on facts and logic—not rush to judgment.

Argument One: Tether Is an “Infinite Money Printer” That Artificially Inflates Bitcoin Prices with USDT

Core Conspiracy Claim: This theory asserts that Tether Ltd., issuer of the stablecoin USDT, can "create something from nothing" and "print out of thin air" vast amounts of USDT, then use this fiat-unbacked USDT to massively buy Bitcoin. This artificially inflates Bitcoin's price, creating a false sense of prosperity. Once the price is pumped, the manipulators allegedly sell part of their Bitcoin holdings for real dollars or other fiat currencies, thereby profiting through a "nothing-to-something" scheme. Some of these real fiat proceeds are then used as purported "reserves" to pass audits, forming a self-reinforcing cycle of fraud. In short, Tether is depicted as the biggest "insider casino operator" in the Bitcoin market, manipulating price movements through unlimited printing.

Rational Rebuttal and Factual Analysis: Portraying Tether’s operations as simply "infinite printing to pump Bitcoin" is an oversimplification that ignores the inherent complexity of markets and the actual mechanisms and demand dynamics behind stablecoins.

First, USDT issuance is fundamentally driven by market demand. Theoretically, when authorized market makers, major exchanges, or institutional investors need USDT—for trading, providing liquidity, or arbitrage—they deposit equivalent fiat currency (mainly USD) with Tether at the official 1:1 exchange rate. Only after receiving the fiat does Tether mint and issue an equal amount of USDT to those entities. Conversely, when institutions wish to redeem USDT for fiat, Tether destroys the corresponding USDT and returns the fiat. Thus, the growth in USDT supply largely reflects genuine demand for stablecoin liquidity across the crypto ecosystem—especially during periods of high market activity or significant price moves, when stablecoins serve as key transactional and hedging tools.

Second, while Tether’s reserve composition has historically been controversial, transparency has gradually improved. In the past, Tether faced scrutiny from regulators (e.g., the New York Attorney General's Office, NYAG) and broad skepticism over the transparency and adequacy of its audits. Critics questioned whether it always held reserves fully backed by high-quality assets matching its total USDT supply. Although these cases often ended in settlements (e.g., Tether and Bitfinex paying fines without admitting wrongdoing), they did not fully eliminate concerns. However, in recent years, Tether has begun publishing regular attestation reports prepared by third-party accounting firms (though not among the top-tier “Big Four”). While these attestations fall short of full financial audits, they do provide snapshots of its reserve composition—including cash, cash equivalents, commercial paper, corporate bonds, precious metals, and digital assets. Critics may still question the liquidity and risk profile of these assets, but this is categorically different from accusing Tether of "printing money out of nothing."

Third, attributing Bitcoin’s long-term price trajectory solely to manipulation by Tether is untenable. Bitcoin prices are influenced by a complex mix of global macroeconomic conditions (like inflation expectations and interest rate policies), technological developments (such as Lightning Network and Taproot upgrades), shifts in market participant structures (including institutional adoption), regulatory trends, investor sentiment, and geopolitical factors. While large capital injections—whether via USDT or other sources—could theoretically influence short-term prices, especially in earlier, less-regulated markets, proving that Bitcoin’s entire decade-long bull-bear cycle was orchestrated by Tether as a single "scam" requires far more direct and comprehensive evidence than merely observing correlations between USDT issuance and Bitcoin price fluctuations at certain times. Academic studies and market analyses have yet to establish conclusive proof of systemic, long-term price manipulation by Tether.

Finally, if Tether were truly a pure "money printer" without underlying demand, its stablecoin USDT would have collapsed long ago due to failure to maintain its dollar peg. Despite occasional brief de-pegging events, USDT has generally remained relatively stable—a fact that indirectly confirms the existence of substantial real-world usage and demand.

Argument Two: “National Adoption” Is a Staged Illusion, With Key Figures Engaged in Insider Trading

Core Conspiracy Claim: This argument alleges that announcements by countries (like El Salvador) declaring Bitcoin legal tender, or major investments in Bitcoin by prominent entrepreneurs (such as Jack Mallers and Michael Saylor), are not genuine national strategies or business decisions—but rather carefully planned and funded "performances" orchestrated by insiders like Tether and Bitfinex. The goal? To create the illusion that "even nations and big institutions are buying," triggering FOMO among retail investors so insiders can offload their holdings or further inflate prices. Specific allegations include:

- El Salvador didn’t actually purchase Bitcoin with real money—it received direct transfers from Bitfinex and Tether;

- Tether played a deep role in drafting El Salvador’s Bitcoin legislation;

- Jack Mallers’ company funds came directly from Tether’s reserves;

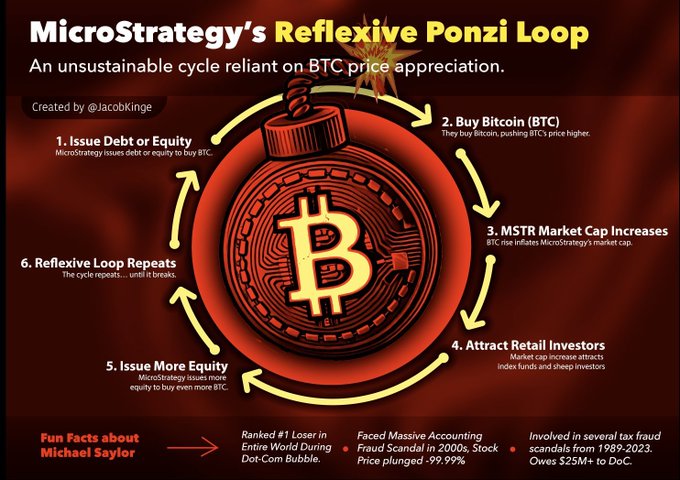

- Michael Saylor’s MicroStrategy engages in a "reflexive Ponzi scheme" through continuous high-leverage financing to buy Bitcoin.

Rational Rebuttal and Factual Analysis: Reducing national policy or corporate strategy to mere components of a conspiracy often overlooks the complex contexts and standard market practices involved.

About El Salvador’s Bitcoin Experiment:

- Standard Practice for Large Transactions: The claim that El Salvador received Bitcoin directly from Bitfinex and Tether wallets as evidence of "non-cash purchase" or "insider handout" misses standard market procedures. For sovereign states or large institutions making major purchases in crypto, using over-the-counter (OTC) desks instead of placing orders on public exchanges is standard practice. This avoids disrupting market prices with massive buy orders and allows for smoother execution. It is entirely normal for Bitcoin to be transferred directly from a seller’s wallet (which could belong to an exchange’s OTC desk, mining pool, or large holder such as Bitfinex or Tether affiliates) to the buyer’s wallet (e.g., El Salvador’s treasury). Therefore, citing blockchain transfer paths alone as proof of impropriety fails to account for routine institutional acquisition methods.

- Transparency and Real-World Impact: That said, El Salvador’s Bitcoin experiment is not without valid criticisms. Questions remain about the transparency of decision-making, the actual cost basis of acquired Bitcoin, the low post-launch usage of the Chivo wallet, and the real economic impact of Bitcoin legalization—all legitimate topics for ongoing evaluation. These issues require objective assessment based on facts, not dismissal under a blanket label of "fraud."

- Tether’s Role in Legislation: Whether Tether had substantial involvement in drafting El Salvador’s Bitcoin law is a serious concern worth investigating. If true, the extent, method, and potential conflict of interest must be evaluated. But this does not automatically prove the entire "national adoption" initiative is a sham; rather, it should be examined through the lens of lobbying, regulatory influence, and governance ethics.

About Jack Mallers and Michael Saylor:

- Business Relationships and Funding Sources: Allegations that Jack Mallers’ Strike or related companies sourced significant Bitcoin investment from Tether’s reserves require concrete evidence of fund flows and relationships. Investments, partnerships, or funding arrangements between crypto companies are common. What matters is whether such transactions are compliant, transparent, and free of undisclosed conflicts that might harm other investors.

- MicroStrategy’s High-Leverage Strategy: Michael Saylor’s MicroStrategy has publicly pursued an aggressive, high-leverage strategy of borrowing heavily to acquire and hold Bitcoin as a core treasury asset. This is an open, risky financial bet rooted in a strong conviction about Bitcoin’s future value. Unlike a Ponzi scheme—which pays early investors with funds from later ones—MicroStrategy uses raised capital to buy a real, tradable asset (Bitcoin). Its success depends entirely on Bitcoin’s future price performance and debt management. Labeling this a "reflexive Ponzi loop" misrepresents its mechanics. Nevertheless, the extreme risk of this approach cannot be ignored.

Argument Three: “Institutional Demand” Was Just Hype That Has Now Faded—ETF Outflows Are a Warning Sign

Core Conspiracy Claim: This view holds that the narrative of "mass institutional entry into Bitcoin" was merely a fleeting wave of hype and FOMO, lacking real or sustained demand. Net outflows from spot Bitcoin ETFs after initial inflows—or weaker-than-expected interest from some institutions—are interpreted as signs that "institutions are collectively fleeing" and "smart money has quietly exited," suggesting Bitcoin lacks long-term support.

Rational Rebuttal and Factual Analysis: Interpreting short-term institutional behavior as definitive evidence of a fundamental trend reversal often reflects a narrow understanding of financial market dynamics.

- Normal Volatility in ETF Flows: Fund flows in and out of ETFs are inherently volatile. Short-term net outflows do not necessarily signal a reversal of long-term trends or a collapse in institutional interest. Numerous factors affect ETF flows: cyclical changes in investor sentiment, macroeconomic shifts (interest rates, inflation data), profit-taking, portfolio rebalancing, tax considerations, and changing attractiveness of alternative assets. To assess true institutional sentiment and long-term allocation trends, one must analyze longer-term data, review public filings, track institutional holdings, conduct market research, and study industry fundamentals—not draw hasty conclusions from transient flow patterns.

- Gradual and Diverse Institutional Adoption: Institutional adoption of novel assets like Bitcoin tends to be gradual and cautious. Different types of institutions—pension funds, endowments, family offices, hedge funds, public corporations—have varying risk profiles, investment horizons, regulatory constraints, and decision-making processes. While spot Bitcoin ETFs offer a convenient and compliant access point for some, they represent just one pathway. Others may invest directly (self-custody), buy shares in Bitcoin miners, trade derivatives, or allocate via private funds. Judging overall institutional demand based solely on ETF performance risks drawing overly broad conclusions from limited data.

- Regulatory Caution ≠ Industry Rejection: Regulators like the U.S. SEC maintaining caution toward crypto-related products (e.g., new ETF applications) and emphasizing investor protection and anti-manipulation measures is a normal part of their mandate. This reflects the ongoing maturation of the crypto market, which still needs progress in transparency, compliance, risk controls, and infrastructure. Equating regulatory prudence with rejection of Bitcoin’s long-term value—or framing it as part of a "conspiracy"—is a clear overreach and misreading.

Argument Four: Tether and Bitcoin Have Entered a “Death Spiral”—Imbalance Could Trigger Collapse

Core Conspiracy Claim: This apocalyptic narrative posits that Tether and Bitcoin are locked in a fragile, interdependent "vicious cycle" or "death spiral." Specifically, Tether supposedly buys Bitcoin to prop up its own value (or fabricate reserve strength), while Bitcoin’s price relies on perpetual liquidity from Tether’s "printing press." If any link breaks—say, a massive run on Tether leading to redemption failures, or a catastrophic Bitcoin crash severely eroding Tether’s BTC-backed reserves—the entire system collapses like dominoes, triggering a historic financial disaster. Saifedean Ammous’ comments about Tether potentially holding more Bitcoin than USD in reserves are often cited to highlight structural instability.

Rational Rebuttal and Factual Analysis: While interconnected financial systems can transmit risks, depicting the Tether-Bitcoin relationship as a hair-trigger "death spiral" exaggerates fragility and misunderstands the foundations of both systems.

- Tether’s Value Foundation: Tether (USDT) derives its value primarily from its promise to maintain a stable 1:1 peg with the U.S. dollar. Its backing comes from declared reserves intended to match outstanding USDT supply. According to Tether’s periodic attestations, these reserves consist mainly of cash and cash equivalents (e.g., short-term Treasuries, money market funds), corporate bonds, secured loans, and other investments—including Bitcoin. While Bitcoin is part of Tether’s reserves, it is neither the entirety nor the dominant component. USDT’s stability hinges on the overall quality, liquidity, and sufficiency of its reserve portfolio, along with market confidence in its ability to honor redemptions.

- Bitcoin’s Multifaceted Value Drivers: Bitcoin’s value is not monolithically dependent on Tether’s liquidity. As previously discussed, Bitcoin’s price and perceived value stem from multiple forces: technical attributes (decentralization, scarcity, security), network effects, supply-demand dynamics, macroeconomic trends, regulation, and adoption levels. While Tether, as a major stablecoin provider, contributes significantly to Bitcoin’s trading depth and liquidity, this does not mean Bitcoin’s intrinsic value rests solely on Tether’s shoulders.

- Complexity of Risk Transmission: A severe crisis of confidence or reserve shortfall at Tether could indeed trigger broader market stress, affecting Bitcoin through reduced liquidity and increased risk aversion. Similarly, an extreme and prolonged Bitcoin price collapse could pressure Tether’s balance sheet if it holds significant BTC reserves. However, whether such shocks inevitably escalate into uncontrollable "death spirals" depends on many variables: shock magnitude, responses from other market participants, regulatory capacity, and the resilience of each system. Interpreting speculative or forward-looking statements (e.g., hypothetical scenarios about future reserve compositions) as imminent threats or established realities lacks grounding in current conditions and dynamic equilibria.

- Focus Should Be on Transparency and Risk Management: A more constructive approach is to monitor the transparency of Tether’s reserve disclosures, the quality and liquidity of its assets, the independence and credibility of audit/attestation processes, and the robustness of its internal risk management and contingency plans. These are the real indicators of systemic stability and risk exposure.

Why Do Conspiracy Theories Flourish and Spread?

The world of Bitcoin and the broader crypto ecosystem—due to its disruptive technology, idealistic ethos, and early-stage regulatory gaps coupled with mixed actor quality—naturally fosters extreme narratives and speculation. Here are several reasons why such "conspiracy theories" thrive:

- Information Asymmetry and Limited Transparency: While blockchain offers on-chain data transparency, the internal operations, full financials, decision-making processes, and even ultimate control of key centralized entities (exchanges, stablecoin issuers, project foundations) often remain opaque or deliberately obscured to the public. This information gap fuels speculation, suspicion, and malicious interpretations.

- Historical Precedents of Fraud and Failure: From Mt. Gox’s theft to Celsius and Voyager’s bankruptcies, and the FTX exchange’s spectacular collapse, the crypto industry has seen repeated incidents of fraud, mismanagement, insider abuse, or hacking. These real disasters have eroded trust, making people more likely to believe in "conspiracies" or "scams" when faced with uncertainty or market anomalies.

- Price Volatility and the Psychological Need for Simple Explanations: Cryptocurrencies are known for wild price swings. After sharp rallies or crashes, especially for those who suffered losses, there’s a strong psychological urge to find a simple, direct cause. "Manipulation by whales or insiders" is easier to grasp and share than accepting that prices result from complex interactions of fundamentals, speculation, and sentiment—a common cognitive bias.

- Interest-Driven Narrative Construction: In any financial market, some actors may promote specific narratives for personal gain—profiting from short positions, discrediting competitors, promoting their own projects or views, or chasing clicks and attention. Social media’s anonymity and rapid dissemination amplify sensational, exaggerated, or distorted "conspiracy theories."

- High Technical Barriers and Emotional Interpretation: For the general public unfamiliar with cryptography, consensus algorithms, or token economics, understanding Bitcoin’s value proposition and ecosystem mechanics presents a steep learning curve. In such cases, simplistic, emotional, or demonizing narratives spread more easily than nuanced, rational analysis.

Conclusion: Upholding Rationality, Evidence, and Critical Thinking Amid the Fog

The world of Bitcoin is an arena where cutting-edge technological innovation, radical financial experimentation, and complex human behaviors intersect. It reveals both the immense potential and appeal of decentralized ideals and peer-to-peer value transfer, and exposes the inevitable irregularities, opacity, and risks of nascent markets. So-called "conspiracy theories" are often selective, one-sided, and subjective interpretations of this complex reality. They may correctly highlight genuine problems or latent risks in the industry, but their explanatory frameworks and final conclusions frequently lack solid evidence, rigorous logic, or comprehensive factual consideration.

We should not treat every critique or question as a threat or malicious attack. Constructive criticism, healthy skepticism, and persistent demands for transparency and accountability are essential external pressures—and internal drivers—that push any industry, especially emerging ones, toward maturity, standardization, and sustainable development. Continued scrutiny of Tether’s reserve composition, calls for independent audits, vigilance toward unusual on-chain activity, and strict examination and disclosure of related-party transactions reflect a maturing market.

Yet, when confronted with grand narratives claiming to expose "systemic manipulation," "colossal scams," or "doomsday predictions," maintaining clarity of thought, independent judgment, and strong critical thinking becomes paramount. We must carefully assess the source and reliability of information, distinguish factual reporting from opinion, recognize that correlation does not imply causation, and resist emotionally charged arguments that bypass reason.

Bitcoin’s future will not be determined by a few alleged "conspiracies" or a handful of accused "insiders." Instead, it resembles a vast, ongoing, globally participatory socioeconomic experiment. Its ultimate path and historical significance will be shaped by continued technological breakthroughs, the gradual clarification and coordination of global regulations, the maturation of market participants' understanding and behavior, and broader societal acceptance and interaction patterns.

In this uncharted digital frontier—full of unknowns, opportunities, and challenges—only by embracing lifelong learning, cultivating independent thinking, and grounding judgments in evidence can we avoid being blinded by temporary fog or misled by sensational stories. And for the crypto industry as a whole, the path to earning lasting public trust and broad recognition lies in proactively increasing transparency, strengthening self-regulation, welcoming oversight, and openly addressing legitimate market concerns. Only thus can the breeding ground for conspiracy theories be effectively minimized.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News