Why don't you have Bitcoin yet?

TechFlow Selected TechFlow Selected

Why don't you have Bitcoin yet?

Bitcoin should become our "mirror of thought."

Author: Daii

It's not that you're not smart enough, or poorly informed—it's simply that we’re all too accustomed to viewing today’s world through yesterday’s lens.

In 2011, when Nobel Prize-winning economist Paul Krugman reminded everyone that "at least so far, buying Bitcoin has been a good investment," the price was just $7. By 2013, Zhihu user @Busch echoed this view, earning over ten thousand upvotes. Yet, unfortunately, we still didn’t act.

Revisiting my old article from 2020, I suddenly realized the real reason we missed Bitcoin: we disguised fear as “rationality,” and masked the unknown with “arrogance.”

This article, already read 34,000 times and liked by 400 people, might serve as a mirror for us—a reminder that when the next “Bitcoin-level” opportunity arrives, we should impose fewer limits on ourselves and summon more courage.

Perhaps the past cannot be changed, but the future is still in our hands. After reading, don’t forget to share it with friends who, like us, are still hesitating.

Bitcoin Should Be a Mirror for Us!

I can't recall exactly when I first heard about Bitcoin—definitely late. Much later than Wu Gang, who knew about it as early as June 2009. Back then, life seemed carefree and everything was flourishing. My first Bitcoin trade was on November 9, 2017, at around $7,250. Just over a month later, on December 17, Bitcoin hit its historical high of over $19,000—more than doubling from my purchase price. You must feel sorry for me—why didn’t I buy more? But looking back now, buying Bitcoin then wasn’t the best timing, just as buying now isn’t either. For reasons, see my previous article: "Be Careful! Don’t Fall for It! Bitcoin Has Never Had a Bull Market!"

Screenshot of my first trade

What I regret even more now is why I didn’t buy Bitcoin earlier. This isn’t wishful thinking—it was genuinely possible. As early as September 11, 2011, a Nobel Prize-winning economist recommended buying Bitcoin. At that time, Bitcoin’s price peaked at only $7.025.

An Economist Recommending Bitcoin?

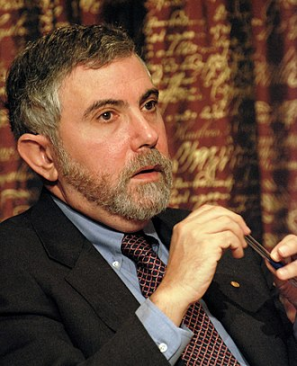

He is the very economist who recommended Bitcoin: Paul Krugman, winner of the 2008 Nobel Memorial Prize in Economic Sciences and columnist for The New York Times. He won the prize for his research on "international trade" and "the geographic distribution of economic activity." Krugman is an advocate of globalization, though his theories on international trade are now facing real-world challenges. That’s a topic for another day.

Krugman in 2008

Now, let’s examine his article recommending Bitcoin. This was Krugman’s earliest piece on Bitcoin, titled "Golden Cyberfetters," published as a blog post on September 7, 2011. Please bear with me—this date will keep reappearing throughout this article. I want to emphasize that opportunity is essentially about timing.

September 7, 2011: Krugman's first article on Bitcoin, "Golden Cyberfetters"

"Golden Cyberfetters"—when you first see this name, you’re probably confused. Don’t blame yourself; it’s a term coined by Krugman, derived from "Golden Fetters," which critiques the gold standard between 1919 and 1939. Many economists believe the gold standard contributed to the Great Depression of the 1930s—the era when milk was poured into sewers, as often cited in textbooks. The situation is complex overall, but all you need to remember is that the gold standard led to the Depression, and that was terrible. Here, Bitcoin is likened to digital gold. Since Bitcoin has a fixed supply of only 21 million coins, it similarly risks deflation and economic depression. Simply put, its limited issuance encourages hoarding. Bitcoin represents a new, internet-era gold standard, ultimately leading to "hoarding, deflation, and depression."

So to the extent that the experiment tells us anything about monetary regimes, it reinforces the case against anything like a new gold standard – because it shows just how vulnerable such a standard would be to money-hoarding, deflation, and depression.

However, Krugman separates theory from practice. Although he remains skeptical about Bitcoin’s long-term future, he doesn’t outright condemn it. He acknowledges Bitcoin’s extreme volatility and states, "buying into Bitcoin has, at least so far, been a good investment."

So how's it going? The dollar value of that cybercurrency has fluctuated sharply, but overall it has soared. So buying into Bitcoin has, at least so far, been a good investment.

Incidentally, in that blog post, Krugman also made another point: our monetary system shouldn’t enrich those merely holding money. Instead, it should facilitate transactions and make the entire economy richer. He argues that Bitcoin enriches holders simply by holding it—which defies natural order. Is that really true? It’s unrelated to this article, but interesting. We’ll discuss it another time.

What we want from a monetary system isn't to make people holding money rich; we want it to facilitate transactions and make the economy as a whole rich.

Back to the main point. You might say, "Wait, you couldn’t have seized this opportunity anyway—you don’t speak English well." No problem—we have Zhihu. On November 22, 2013, @Busch brought news of Nobel laureate Krugman recommending Bitcoin into the Chinese-speaking world via a Zhihu Q&A. See? Our Zhihu is impressive. And @Busch even shared a story. Even more remarkably, this answer received 12,000 likes.

Answer about Bitcoin receiving 12,000 upvotes

This is the Zhihu question: How does the economics community view Bitcoin? Answered by @Busch, it has now earned 12,805 upvotes. Twelve thousand likes—that’s truly impressive.

The 12,000 likes owe much to the story told. Let’s temporarily set aside our pragmatism and appreciate this excellent narrative.

The story is real—it’s about the "Capitol Hill Babysitting Co-op." A group of young parents working on Capitol Hill formed this mutual aid organization to solve childcare issues during social events. Upon joining, each member received 20 hours of babysitting coupons. Each coupon entitled them to a certain amount of childcare service. Parents providing services earned coupons, which they could use later when others watched their children. Of course, there were many management details—all thoughtfully considered.

The Capitol Hill Babysitting Co-op in 2000

Half-hour babysitting coupons issued by the co-op

But reality is harsh—in the end, problems emerged. Soon after launching, the co-op teetered on collapse. People were reluctant to spend coupons hiring others; instead, they preferred earning more coupons for personal emergencies.

@Busch argues the recession stemmed from insufficient output, caused by an inadequate number of babysitting coupons.

If we treat this co-op as an economy and babysitting services as its output (GDP), this perfectly defines a recession. The root cause lies in internal deflation—i.e., too few coupons in circulation.

Using this story, @Busch first criticizes Bitcoin’s anti-inflation nature. Its design incentivizes hoarding, potentially causing deflation and eventually a great depression. This echoes Krugman’s core message in "Golden Cyberfetters." Now you understand: the hard cap of 21 million is both Bitcoin’s most vulnerable and earliest attacked feature.

If it truly becomes the "currency of the future," the "global currency" as some fervent speculators claim, the global economy would suffer the same fate as the Capitol Hill co-op.

In fact, the conclusion is precisely the opposite. The recession wasn’t due to too few coupons or insufficient output, but rather lack of demand—a point clearly articulated in academic papers. @Busch draws an analogy between the certainty of coupon supply and Bitcoin’s finite quantity, making complex economic concepts easy to grasp. The conclusion is simple: if Bitcoin became international currency, it would suffer the same fate as the coupons—deflation, co-op failure, i.e., economic depression. Indeed, the explanation is concise, vivid, and illustrative—earning 12,000 likes was well deserved.

But the story was misused. Critiques of @Busch’s answer are beyond this article’s scope—we’ll cover them separately. You can search for them in our WeChat official account.

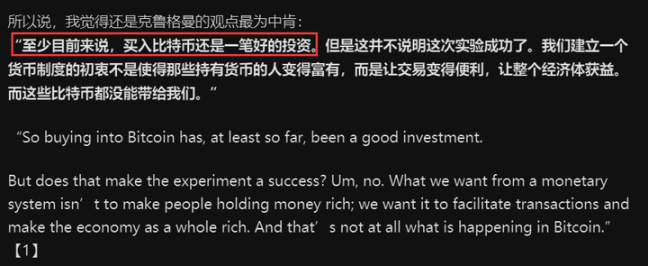

Here comes the key point—what you care about most. Don’t assume @Busch intended his Q&A to discourage Bitcoin purchases. Quite the contrary—he deliberately quoted Krugman’s full sentence: "at least so far, buying into Bitcoin has been a good investment," even bolding it to emphasize the message.

Screenshot from the 12,000-upvote Zhihu answer, quoting Krugman's recommendation to buy Bitcoin

Now pay attention: two key dates represent potential opportunities to buy Bitcoin. One is when Krugman published his article—September 7, 2011. The other is when @Busch referenced it on Zhihu—around November 22, 2013.

A Nobel Prize-winning economist recommending Bitcoin is an extremely rare signal. Yet even if you saw it, you still wouldn’t buy. Why? That’s what this article aims to reveal. Let’s analyze each case.

Why Wouldn’t You Buy?

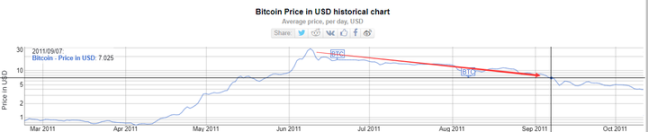

Suppose you were lucky enough to see Krugman’s Bitcoin recommendation on September 7, 2011. You still wouldn’t necessarily buy. Looking at the price trend then makes it clear. Bitcoin was priced at $7.025, having just dropped from a historical high of $29 one month prior. Note: the chart below doesn’t show a cliff-like drop because it uses a logarithmic scale—one that emphasizes trends. To learn more about logarithmic scales, please refer to my earlier article "Be Careful! Don’t Fall for It! Bitcoin Has Never Had a Bull Market!" Don’t fault me for repeatedly promoting it—many now believe we’re in a bull market, and I don’t want my readers deceived.

Bitcoin price trend before September 2011 (logarithmic scale)

Look at the linear-scale chart below, and you’d be even less inclined to buy. The decline appears far steeper than on the logarithmic chart—more intuitive, more frightening. This is a classic "bear market." As the saying goes, "Don’t try to catch a falling knife in a bear market." You decide to wait. Sure enough, prices keep dropping. By November 11, 2011, Bitcoin was down to $2.10. At this point, you’d feel even more confident in Krugman’s prediction that Bitcoin would fail. You’d feel lucky you didn’t listen—hearing him would’ve cost you dearly.

Yet from today’s perspective, you actually missed an opportunity.

From September 2011 to January 2020, Bitcoin prices remained in a downtrend

Now consider the second moment—November 22, 2013. This is the most likely time Chinese readers could have learned of Krugman’s Bitcoin endorsement via Zhihu. Would you buy? Probably not. As shown below, two years later, Bitcoin had surged nearly 100-fold—from $7 to $675. Such gains were unprecedented. Isn’t that a bubble? Even scarier, prices kept rising—just 20 days later, on November 30, it hit $1,052, a new all-time high. Such extreme volatility made you doubt Krugman’s words. The risk seemed too great. More likely, you gave up—thinking, "Opportunities abound; why stress over Bitcoin?"

And so, the second chance to buy Bitcoin slipped away.

On November 22, 2013, when Krugman’s idea reached China, Bitcoin was priced at $675

To help you appreciate how rare it is for an economist—let alone a Nobel laureate—to recommend Bitcoin, you should understand mainstream views on Bitcoin. This context will further highlight how precious these two opportunities were.

Is Bitcoin a Bubble?

Economists are common; recommendations are not. A Nobel-winning economist endorsing Bitcoin is exceptionally rare. That single endorsement was a fluke—never repeated since. On the contrary, Krugman began denouncing Bitcoin.

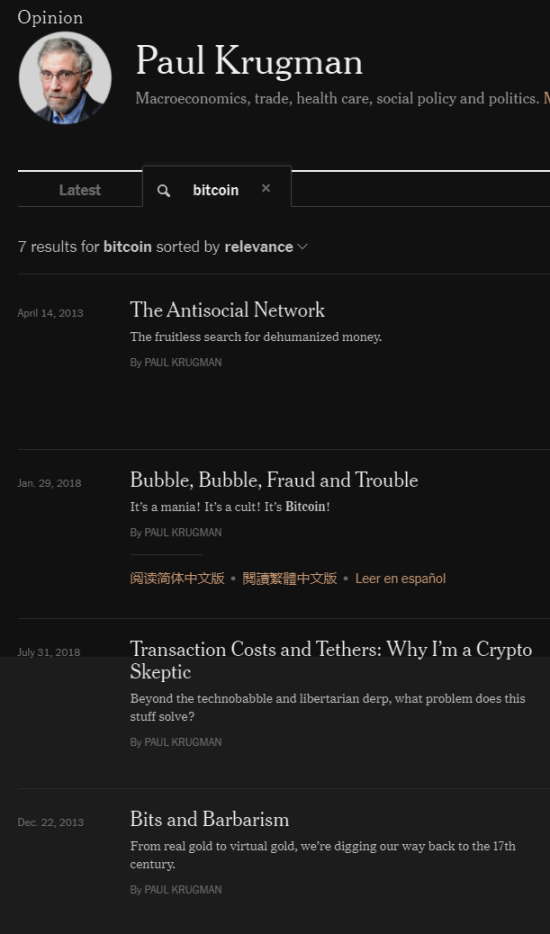

After September 7, 2011, Krugman’s stance on Bitcoin shifted from ambiguous to openly hostile. Below is a list of his Bitcoin-related articles in The New York Times. Judging from their titles, his opposition is unmistakable: April 14, 2013—"The Anti-Social Network"; January 29, 2018—"Bubble, Bubble, Fraud and Trouble"; July 31, 2018—"Why I Am a Cryptocurrency Skeptic."

Krugman's New York Times column—selected Bitcoin-related articles

Especially notable is his January 29, 2018 piece. He wrote it after a barber asked whether he should buy Bitcoin. He was furious—so much so that he titled it "Bubble, Bubble, Fraud and Trouble," using "bubble" twice. The article ends with a vivid expression of his anger toward Bitcoin: "No, my barber shouldn’t buy Bitcoin. This will end badly, and the sooner it does, the better."

So no, my barber shouldn't buy Bitcoin. This will end badly, and the sooner it does, the better.

I’m guessing here—but on January 29, 2018, Bitcoin was trading above $11,000, down over $8,000 from its one-month-earlier peak of over $19,000. Maybe Krugman himself was stuck holding bags—otherwise, why so angry? Just kidding, maybe not.

January 29, 2018: Bitcoin price above $11,000

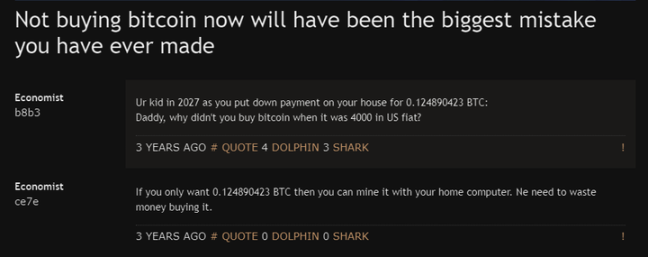

Bitcoin doesn’t exclude economists from ownership despite widespread criticism. There’s an anonymous forum frequented by American economics graduates, professors, and job seekers—because of anonymity, you might hear truth, or hearsay. It’s called "Economics Job Market Rumors" (EJMR), website: econjobrumors.com. Three years ago, a thread appeared there with a bold title: "Not Buying Bitcoin Now Is the Biggest Mistake of Your Life." Disclaimer: this is rumor, not evidence of economists buying Bitcoin—I’m just sharing gossip.

A three-year-old EJMR forum post: "Not buying Bitcoin now is the biggest mistake of your life"

Back in China, successful entrepreneur Jack Ma joined the chorus criticizing Bitcoin. He declared Bitcoin a bubble—seriously and earnestly. That was on May 16, 2018, at the Second World Intelligence Conference—an important event co-hosted by: National Development and Reform Commission, Ministry of Science and Technology, Ministry of Industry and Information Technology, Cyberspace Administration of China, Chinese Academy of Sciences, Chinese Academy of Engineering, China Association for Science and Technology, and Tianjin Municipal People’s Government.

May 16, 2018: Jack Ma speaks at the Second World Intelligence Conference, stating blockchain is not a bubble, but Bitcoin is

Ma’s exact words: "Blockchain is currently a hot term. First, blockchain is not a bubble, but today’s Bitcoin is. Bitcoin is merely a small application of blockchain."

The key point: Bitcoin had just fallen from its all-time high of over $19,000 to just over $8,200—another $3,000 drop since Krugman’s angry column "Bubble, Bubble, Fraud and Trouble." This seems to confirm Ma’s claim—Bitcoin is a bubble, and it’s bursting.

May 16, 2018: Bitcoin at $8,291—less than half its all-time high

Upon reflection, whether you didn’t buy Bitcoin, or Krugman and Ma called it a bubble—both positions were reasonable, rational decisions.

But 11 years later, our rationality hurts our eyes (watching it rise) and empties our pockets (missing out). We can’t keep fooling ourselves daily, claiming Bitcoin is still a bubble that will eventually vanish. Wouldn’t we become modern-day Xianglin Sao (brothers)? We must ask ourselves: Was rationality wrong? Should we have gambled wildly to capture Bitcoin’s rewards? No—the error lies not in rationality, but in ourselves.

What Exactly Did We Do Wrong?

Rationality itself isn’t wrong. The mistake lies in how we applied it. Our survival instinct prioritizes safety and discourages risk. We easily dismiss new things because novelty implies immaturity and danger.

In essence, we lack tolerance for novelty. Often, deep down, we’re afraid. Consider how terrifying it must have been to be the first person to eat crab—otherwise, we wouldn’t still use "first to eat crab" today to praise pioneers. Eating crab is a personal choice. Once elevated to societal level, the issue grows far more complex.

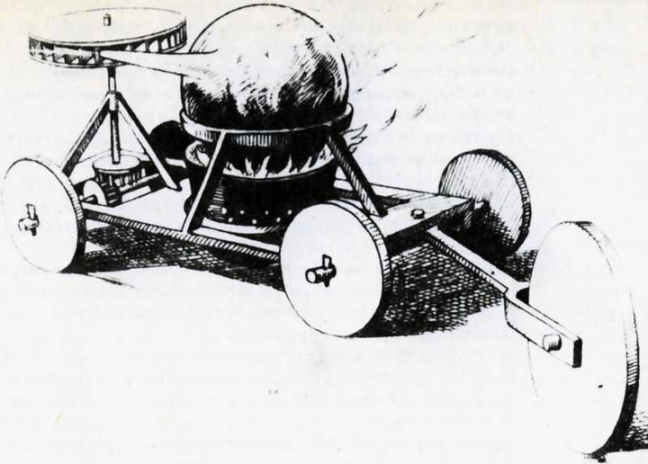

Look at Britain’s 19th-century "Red Flag Act," and you’ll see that early automobiles faced no less hostility than Bitcoin does today. When first invented, cars were generally inferior to horse-drawn carriages—or rather, carriages opposed them. Carriages themselves couldn’t speak—the opposition came from us humans. Early cars performed poorly in comfort and stability. The 1678 car prototype below looks downright monstrous. Worse, they were noisy—a car suddenly passing by could startle anyone. In 1865, Britain enacted the "Red Flag Act" to "regulate" automobile use. At the time, a car’s main advantage—and perhaps only remaining one—was speed.

Car from 1678

The 1865 Red Flag Act stipulated that self-propelled vehicles must be accompanied by a crew of three; if attached to two or more vehicles, an additional person was required; a man carrying a red flag must walk at least 60 yards (about 55 meters) ahead of the vehicle. His duties included directing traffic, warning pedestrians, and assisting horses and carriages. This flagman gave the law its name.

Stipulated that self-propelled vehicles should be accompanied by a crew of three; if the vehicle was attached to two or more vehicles an additional person was to accompany the vehicles; a man with a red flag was to walk at least 60 yd (55 m) ahead of each vehicle, who was also required to assist with the passage of horses and carriages. The vehicle was required to stop at the signal of the flagbearer. (Section 3) Additionally vehicles were also required to have functional lights, and not sound whistles or blow off steam whilst on the road. (Section 3) A speed limit of 4 mph (2 mph in towns) was imposed for road locomotives, with a fine of £10 for contravention. (Section 4)

Reading text alone, you might not grasp how severely the law restricted speed. But think carefully—it’s brutally harsh, almost malicious. The car moves, but just ahead of it, someone must walk on foot. Clearly, how fast could such a vehicle possibly go?

A man with a red flag walks ahead of the car—the origin of the "Red Flag Act"

This photo was taken in 1896—the very year the Red Flag Act was repealed after 31 years. Driving the car is Charles Rolls, later co-founder of Rolls-Royce. The photo was likely staged to memorialize the era—showing the standard configuration: three people, one walking ahead with a red flag. For more on this history, see "When Cars Appeared, Horse Carriages Opposed Them."

Science fiction writer Liu Cixin

Science fiction author Liu Cixin said in "The Three-Body Problem": "Weakness and ignorance aren’t barriers to survival, arrogance is." Our intolerance may appear as arrogance to other species. Arrogance is humanity’s social gene. Indeed, we possess intelligence superior to other Earth creatures. Arrogance isn’t something we actively pursue; sometimes it manifests as pettiness; more often, it expresses itself through our intolerance of new things.

The Red Flag Act is history; "Bitcoin is a bubble" continues...

Conclusion

Happily, The Economist—a venerable publication founded in 1843—has laid down its arrogance. On October 29, 2020, it published an article that earned praise. Titled "Getting down with the cool kids on bitcoin," with the subtitle "How investors might learn to stop worrying and love crypto," it even featured Bitcoin’s symbol in its illustration. The "cool kids" refer to the "Blitz Kids"—a group active at the Tuesday Club nights in London’s Covent Garden during 1979–80. They gained acclaim for launching the New Romantic subculture movement. Those familiar with British cultural history will understand their significance. All you need to know is: these cool kids were no ordinary group—they contributed greatly to British culture and produced many celebrities.

October 29, 2020: Illustration from The Economist's article "Getting down with the cool kids on bitcoin"

The article states: "Bitcoin is a pretty tiny club. Beside it, gold looks as capacious as Wembley Stadium. The market value of all bitcoin is just 1–2% of the value of all the gold above ground. Scarcity is a trait of many things that are perceived to have value."

Bitcoin is a pretty tiny club. Beside it, gold looks as capacious as Wembley Stadium. The market value of all bitcoin is just 1-2% of the value of all the gold above ground. Scarcity is a trait of many things that are perceived to have value.

At the end, the article quotes Steve Strange—the iconic representative of the "cool kids": "The best move I ever made was turning Mick Jagger away at the door."

Steve Strange, who sadly died in 2015, understood this fully. "The best move I ever made was turning Mick Jagger away at the door," he said.

Mick Jagger, whom he turned away, is a legendary British rock star. At the time, Steve Strange himself was young and unknown. The author subtly suggests: don’t let the current "cool kids" playing with Bitcoin leave you behind. We should proactively join. The Bitcoin club won’t disappear just because we refuse to enter.

Indeed. Cars are now our companions; horse carriages belong to history. We’re nearly forgetting the arrogance of the Red Flag Act. Now Bitcoin has arrived. Because of past arrogance, we’ve missed chances again and again to benefit from Bitcoin.

Profits are always temporary. If we fail to shed arrogance when facing new things, we’ll keep missing "Bitcoin-level" opportunities. In this sense, remembering the Bitcoin chances we missed will humble us, reduce our arrogance, and open doors to more new opportunities.

Bitcoin should rightly become our "mirror of thought."

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News