The Monthly "Options Storm": Why Do Crypto Stocks Always Experience Sharp Volatility Around Mid-Month?

TechFlow Selected TechFlow Selected

The Monthly "Options Storm": Why Do Crypto Stocks Always Experience Sharp Volatility Around Mid-Month?

When market makers sell out-of-the-money call options, they hedge their short delta risk by buying shares of the underlying stock.

Author: Jay

Translation: TechFlow

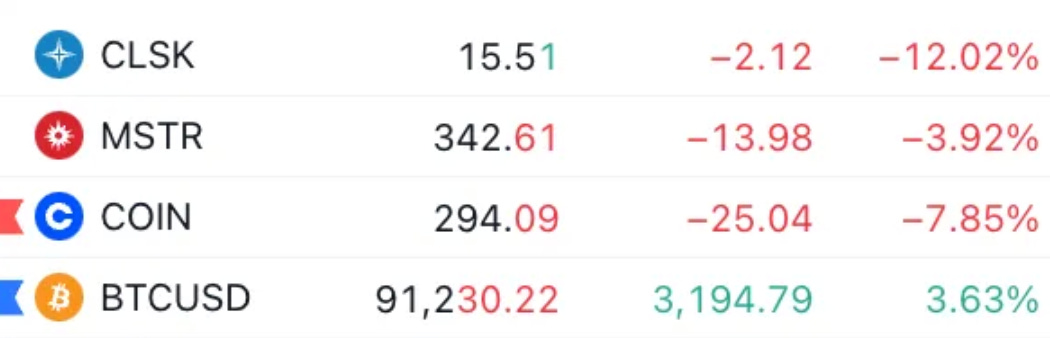

Kenny G wins again

So why are crypto stocks underperforming?

I’ll explain the basic dynamics of how options markets influence underlying stock prices.

A key factor is the upcoming monthly option expiration (mopex), which will occur this Friday, November 17 — with specific dynamics including:

-

Overly high expectations for price volatility

-

Market makers unwinding hedges

I'll use Coinbase as an example, but these factors apply to nearly all crypto-related stocks.

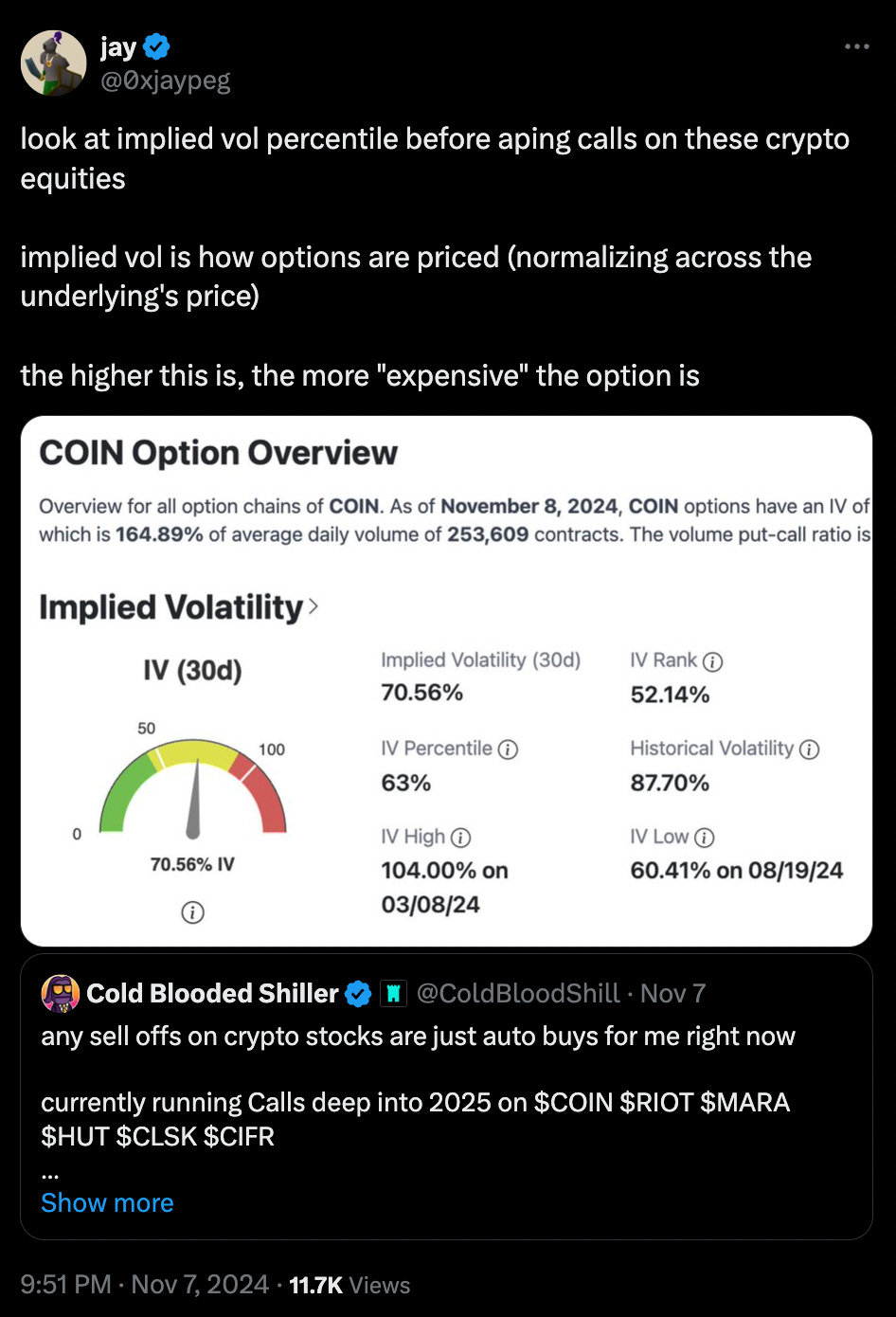

I previously mentioned that after Trump’s victory, due to the dynamic I'm about to describe, you should check implied volatility before considering buying call options.

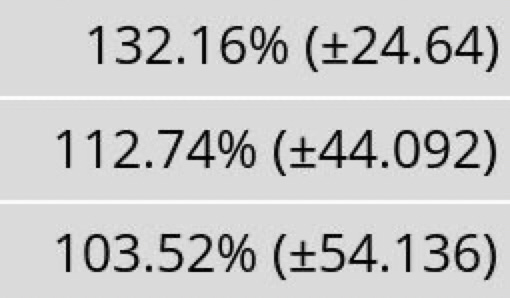

Here is the implied volatility data for Coinbase options expiring on November 15, 22, and 29.

A 132% volatility implies a 95% probability that the underlying asset will move up or down by approximately 16.62% per day. This level of expectation is extremely high.

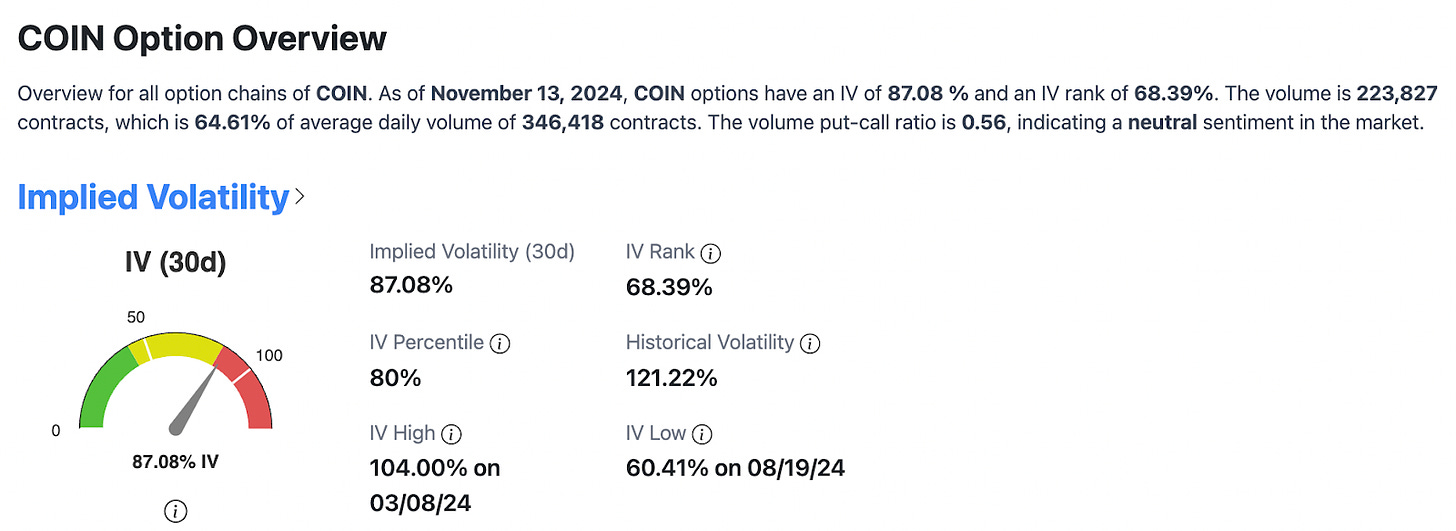

The 30-day historical percentile for implied volatility stands at 80%. This means that over the next 30 days, this level of implied volatility (or expectations for Coinbase upside) is higher than 80% of historical periods. This is unusually high in the absence of a quarterly earnings call.

So what happens when market expectations are this elevated? What do market makers do?

When market makers sell out-of-the-money call options, they hedge their short delta risk by buying shares.

As expiration approaches, the delta of these out-of-the-money calls declines, so market makers sell shares to avoid directional exposure.

Near November 15, the rate at which out-of-the-money calls lose delta accelerates (assuming all else equal).

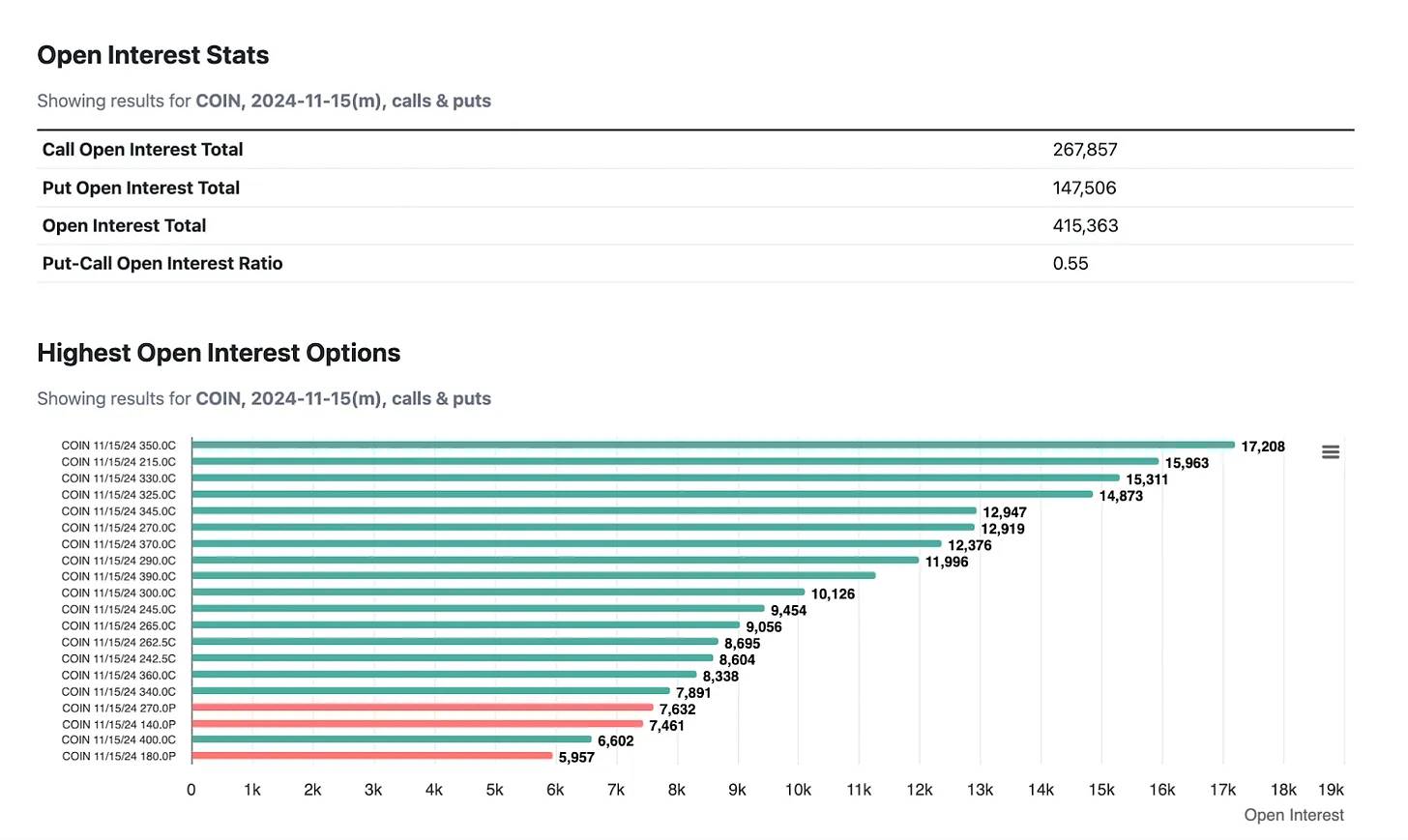

Looking at open interest in options, there's a clear skew toward out-of-the-money calls (puts are barely visible on the chart).

As expiration nears, the reflexivity of market maker hedging behavior amplifies directional volatility. As a result, market makers become more aggressive in selling shares (unless other entities are aggressively buying Coinbase).

Meanwhile, as investors take profits (closing long calls, prompting market makers to sell hedged long stock), this cycle reinforces itself. This creates a large reflexive loop.

How did we get here?

Last week, Coinbase options positioning was extremely bearish (visible from historical put/call ratios and 25-delta skew).

Trump’s victory triggered massive position unwinding (creating the opposite scenario of what I described earlier), causing market makers to buy back shares as they covered their short puts.

The market pendulum swung violently in the opposite direction, causing implied volatility (prices) of these options to spike sharply — along with it, the delta of out-of-the-money calls increased (leading to more aggressive hedging, and inevitably, its unwind).

Due to short covering, market maker hedge unwinds, and broad expectations for a "supercycle," volatility expectations shifted excessively to the upside. This phenomenon is reflected across the implied volatility of all crypto stocks.

This is also why I chose to sell a large amount of volatility at this moment — such extreme expectations rarely materialize, and it also serves as an excellent hedge against spot positions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News