Crypto has its own江湖; mapping the "Coinbase mafia" power landscape

TechFlow Selected TechFlow Selected

Crypto has its own江湖; mapping the "Coinbase mafia" power landscape

This crypto giant holds a key advantage: a vast network of former employees.

Author: Yueqi Yang

Translation: TechFlow

For years, Coinbase has dominated Bitcoin trading in the U.S. market, becoming the go-to exchange for users to buy and sell Bitcoin. Today, the cryptocurrency exchange is trying to reposition itself as a pillar of the broader financial system by leveraging its Base blockchain, launched last year.

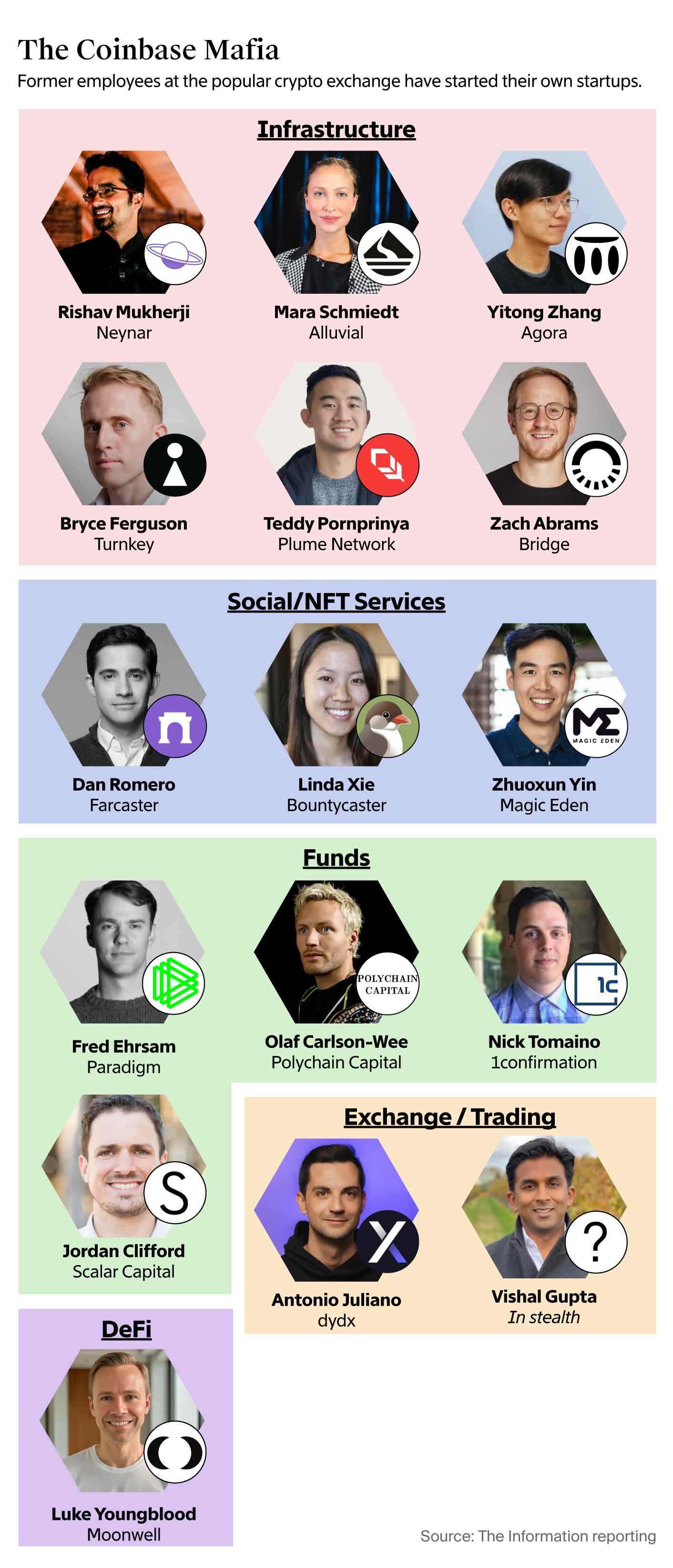

To attract users and generate revenue, Coinbase needs external applications built on its blockchain to offer services such as lending, international payments, and other financial products. The crypto giant holds one key advantage: a vast network of former employees who have gone on to launch their own crypto startups—about 40 of which have received investments from Coinbase.

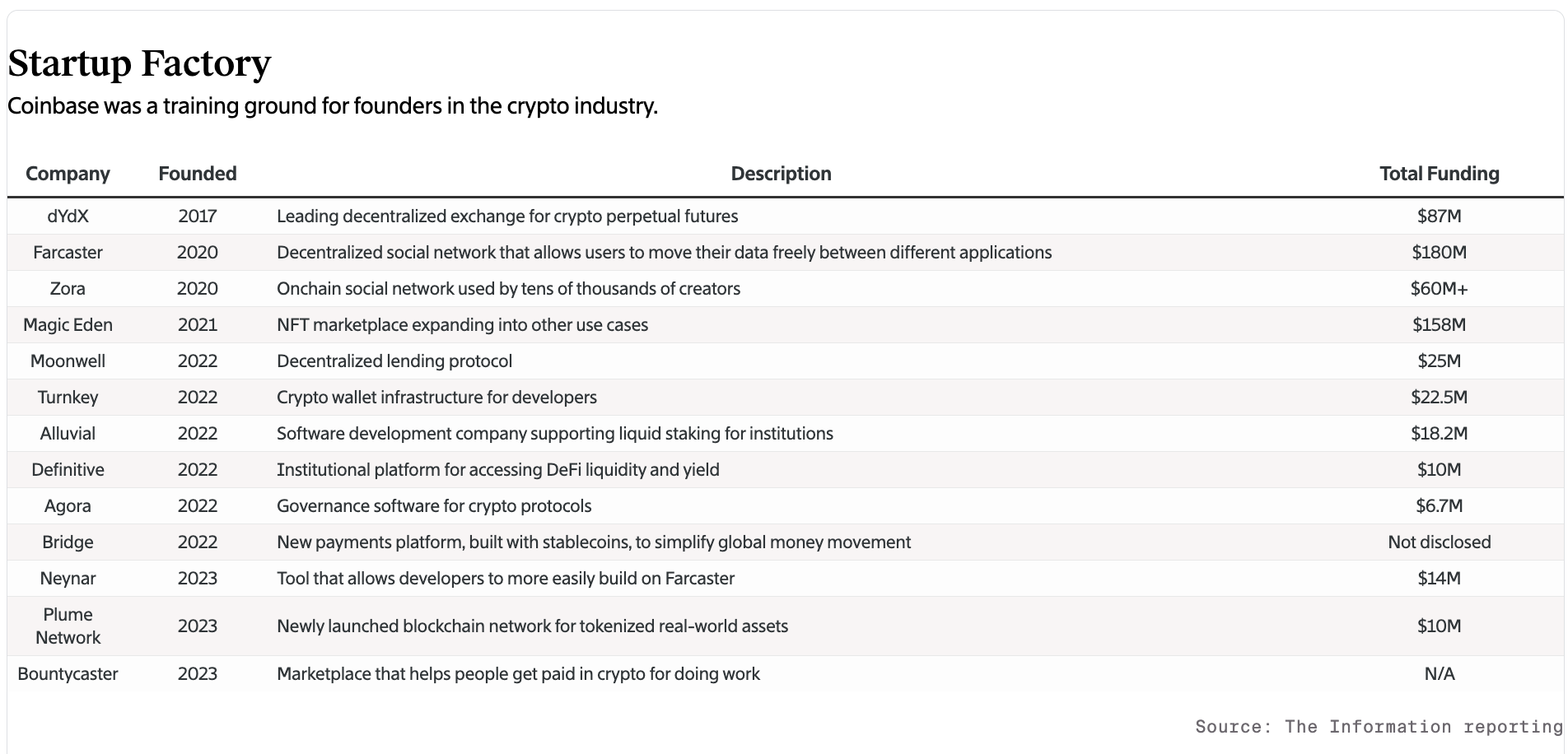

One example is Moonwell, a decentralized finance (DeFi) application that allows users to lend and borrow cryptocurrencies across blockchains, including Coinbase’s Base. Moonwell launched on Base the day the blockchain went live in August 2023 and has since become one of the network’s most popular apps, securing over $145 million worth of crypto assets on the chain.

Moonwell founder Luke Youngblood left Coinbase in spring 2022 after working at the crypto giant for three years. He wanted to build decentralized protocols—leaderless organizations governed by token holders—but said this was difficult to achieve at Coinbase due to increasing regulatory risks and traditional corporate structures.

Shortly after Youngblood submitted his resignation, he received a message on Slack from Shan Aggarwal, who leads Coinbase’s venture investing and corporate development. “He just said, ‘Whatever you’re doing, we want to invest in you,’” Youngblood recalled. “‘Let us know, because we want to be able to back you.’”

Coinbase Ventures eventually became an early investor in Youngblood’s new company. According to internal figures, over the years, Coinbase employees have founded around 100 venture-backed startups spanning industries from non-fungible token (NFT) marketplaces to DeFi and social media networks.

More startups founded by former Coinbase employees are on the way. Vishal Gupta, the company’s former head of trading who left last year, said his startup will launch publicly in the coming weeks. Drawing on his experience, he plans to start a company in the field of crypto trading.

“The culture at Coinbase is: do big things, finish your work, and then move on to do your own thing,” said Breck Stodghill, a partner at crypto investment firm Haun Ventures and a former early engineer at Coinbase.

This practice dates back to Coinbase’s early days, when some employees received executive support upon deciding to start their own ventures. Linda Xie, who joined as employee #30 in 2014, decided to leave three years later to launch a crypto fund.

When she informed Coinbase co-founder and CEO Brian Armstrong of her decision, “he gave me a high five and said, ‘Welcome to being a founder,’” Xie recalled. She added that Armstrong subsequently offered to invest in her new fund and volunteered to serve as a reference whenever needed.

The philosophy behind this approach is that a growing crypto ecosystem creates more opportunities for Coinbase—even if it means losing a talented employee in the short term.

“We often talk with them before they leave Coinbase, and well before they officially launch their companies, we decide to invest in and support these founders because we know they plan to leave and start their own ventures,” said Aggarwal. Coinbase Ventures typically invests between $1 million and $5 million, and currently backs approximately 450 companies.

A Broad Support Platform

Successful founders emerging from Coinbase can expand their influence and market share within the crypto ecosystem while also benefiting Coinbase. Most startups backed by Coinbase do not compete directly with its core business of crypto trading. Instead, they aim to build services that leverage Coinbase’s infrastructure or integrate with Coinbase products.

“When Coinbase Ventures invests, you gain the support of Coinbase as a larger platform positioned at the center of the crypto ecosystem,” said Aggarwal, noting that this facilitates collaboration with the company.

Early backing from Coinbase Ventures can also attract investors like a16z, which invested in Coinbase when it was still a startup, and Haun Ventures, whose founder Katie Haun previously served on Coinbase’s board. Many prominent crypto VCs are former Coinbase employees who are familiar with founders’ backgrounds, helping to draw additional funding.

Olaf Carlson-Wee, Coinbase’s first employee, founded Polychain Capital in 2016 at age 26—one of the earliest crypto hedge funds. Fred Ehrsam, who co-founded Coinbase with Armstrong, later launched Paradigm, a venture firm focused on crypto. (Ehrsam stepped down as managing partner of Paradigm last year but remains a partner.)

Stodghill of Haun Ventures said he reconnected with Rishav Mukherji, a former Coinbase product manager, after leaving the company. Mukherji founded Neynar, a crypto infrastructure startup, in 2023, and Haun led its $11 million funding round in May.

A Strong Desire for Change

While Coinbase’s role as a launchpad for founders and a talent pipeline for the broader industry reflects its deep Silicon Valley ties and extensive crypto expertise, it also highlights how some founders feel the need to break away from the industry giant to innovate at the cutting edge of crypto technology.

Many founders supported by Coinbase recount experiences similar to Youngblood’s—they say they wanted to build at the frontier of crypto, such as in advanced DeFi or launching a token. Others feel Coinbase has lost the entrepreneurial spirit that once attracted builders who saw themselves as owners of small teams willing to take on ambitious projects.

Dan Romero, who later founded the decentralized social platform Farcaster, played a key role in tackling major challenges during his time at Coinbase starting in 2014. For instance, after Silicon Valley Bank abruptly exited, he flew to Europe to secure a new banking partner to keep operations running, Armstrong recalled on a recent podcast.

By 2019, when Romero decided to leave, Coinbase had evolved into a much more mature company. “I joined when there were only 20 people. Now there are 800, and I felt a strong desire to go do my own thing,” Romero recalled telling his managers. “Brian [Armstrong] understood.”

During the recent crypto bull market, Coinbase continued to grow rapidly—from 1,717 employees in early 2021 to about 5,000 by early 2022. Founders who left during this phase said they were partly motivated by a desire to avoid increased bureaucracy and cumbersome processes. Armstrong acknowledged that Coinbase had hired too quickly, leading to declining efficiency. After several rounds of layoffs, the workforce was reduced to around 3,500.

In some cases, Coinbase fell behind in developing popular products. For example, Coinbase announced plans in October 2021 to launch an NFT marketplace at the peak of the NFT craze, but the platform didn’t go live until six months later—by which time the market had already cooled significantly.

With the launch of the Base blockchain, Coinbase has regained some favor among crypto purists. According to DefiLlama, Base is now the sixth-largest blockchain and has become a small but growing source of revenue for Coinbase. The company earns transaction fees from activity occurring on the blockchain.

Base contributed the majority of Coinbase’s $108.6 million in “other transaction revenue” in the first half of this year. While this remains a tiny fraction of its $3 billion total revenue during the same period, it has already surpassed the fees Coinbase earns from its custody services.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News