Powell: Now is the time to adjust policy

TechFlow Selected TechFlow Selected

Powell: Now is the time to adjust policy

Here is the full text of Powell's speech, regarding interest rate cuts!

On Friday local time, Federal Reserve Chair Jerome Powell delivered a speech at the annual Jackson Hole symposium. As a moment eagerly awaited by global markets, the Fed chair publicly declared that the U.S. central bank is about to officially enter a rate-cutting cycle.

Full text of the speech:

Today, more than four and a half years after the onset of the pandemic, economy-wide distortions related to the pandemic are gradually receding from their most extreme levels. Inflation has come down substantially, the labor market is no longer overheated, and overall financial conditions are now considerably looser than they were before the pandemic. Supply constraints have normalized, and the risk balance facing our dual mandate has shifted. Our goal is to restore price stability while maintaining a strong labor market—avoiding the kind of sharp rise in unemployment seen in past episodes when inflation expectations were less well anchored. We have made considerable progress toward this objective. While the job is not yet complete, we have clearly made significant headway.

Today, I will first discuss the current economic situation and the path ahead for monetary policy. Then, I will reflect on the economic events since the start of the pandemic—why inflation rose to levels unseen in generations, and why it has declined so much even as unemployment remained low.

Short-Term Policy Outlook

Let me begin with the current situation and the short-term outlook for policy.

For most of the past three years, inflation ran well above our 2% target, and labor market conditions were extremely tight. The primary focus of the Federal Open Market Committee (FOMC) was rightly on bringing down inflation. Prior to this episode, most living Americans had never experienced the pain of sustained high inflation. Inflation imposed substantial hardship, especially on those least able to cope with rising costs for essentials like food, housing, and transportation. High inflation created stress and a sense of inequity that persists today.

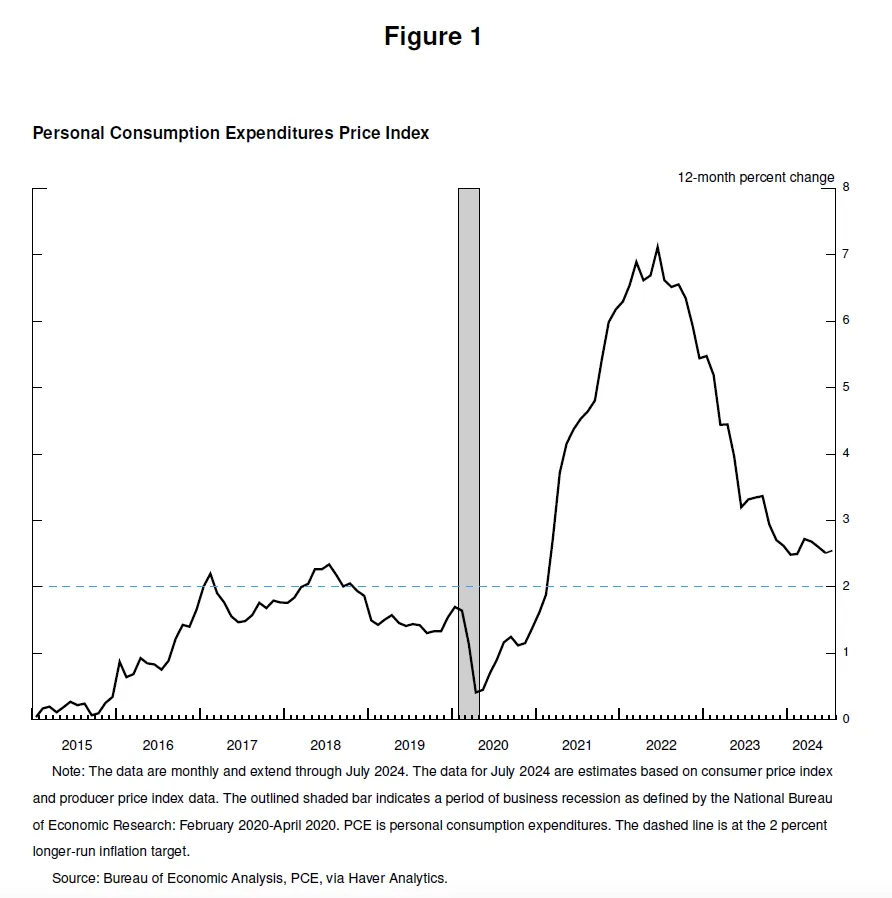

Our restrictive monetary policy helped restore balance between aggregate supply and demand, alleviated inflationary pressures, and kept inflation expectations well anchored. Inflation is now moving closer to our policy goal, with prices up 2.5% over the past 12 months. After pausing earlier this year, progress toward our 2% objective has resumed. I am increasingly confident that inflation is sustainably on a path back to 2%.

Turning to employment, in the years before the pandemic, we witnessed the clear benefits of a strong labor market: low unemployment, high labor force participation, historically narrow racial gaps in employment, and healthy real wage growth concentrated increasingly among lower-income workers—all amid low and stable inflation.

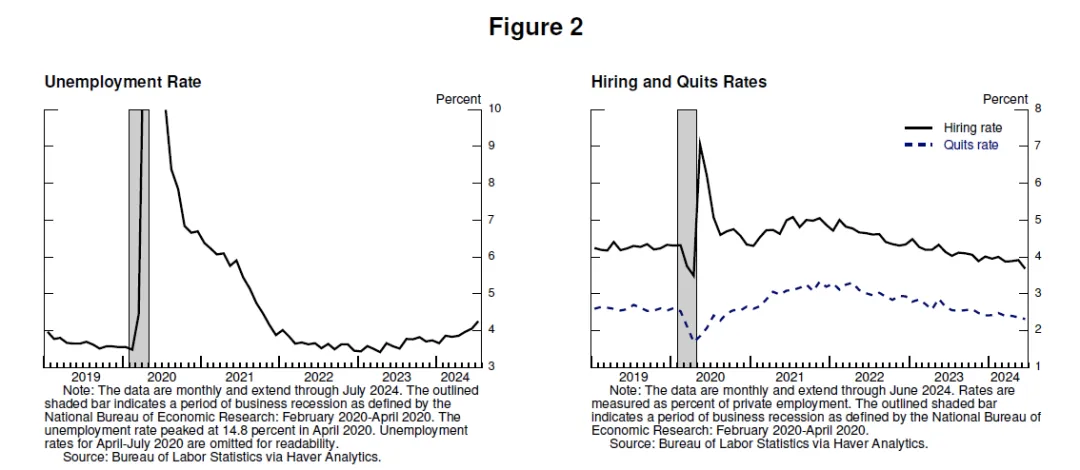

Today, the labor market has clearly cooled and is no longer overheated. Unemployment began rising over a year ago and now stands at 4.3%, still historically low but nearly one percentage point higher than at the beginning of 2023. Most of the increase occurred within the past six months.

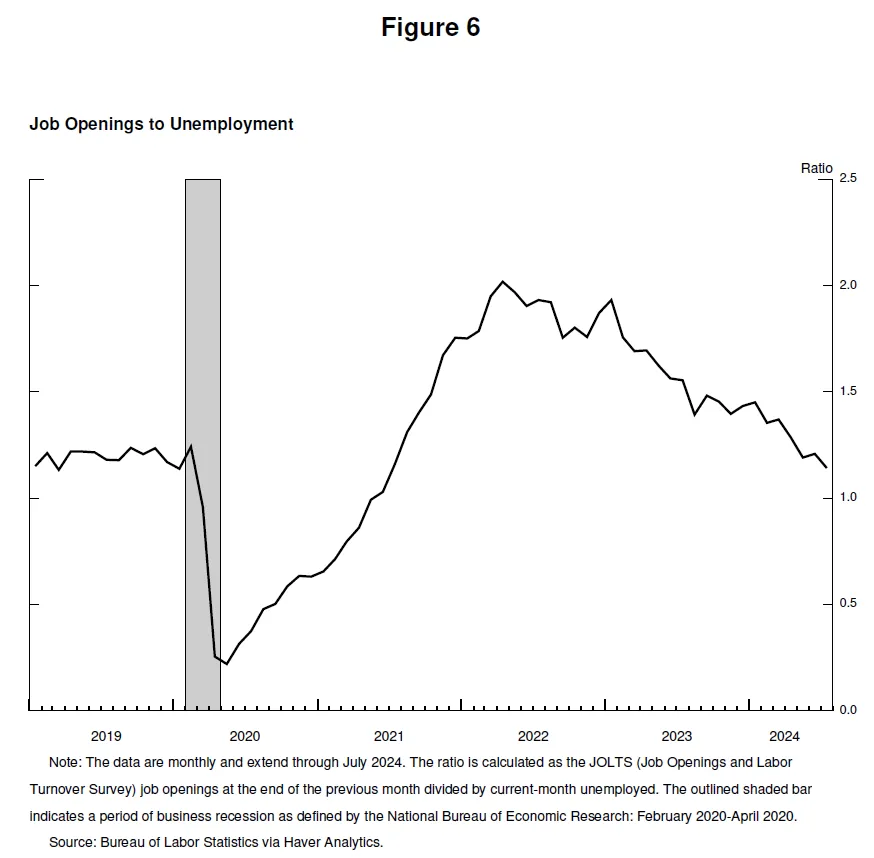

To date, the rise in unemployment has not been driven by the kind of mass layoffs typically seen during recessions. Instead, it primarily reflects a notable increase in labor supply and a slowing pace of hiring. Even so, the cooling in the labor market is evident. Job growth remains solid but has slowed this year. Job openings have declined, and the ratio of vacancies to unemployment has returned to pre-pandemic ranges. Hiring and quit rates are now below levels seen in 2018 and 2019. Nominal wage growth has moderated. Overall, the labor market is significantly looser than it was in 2019—the year before the pandemic, when inflation was below 2%. The labor market does not appear likely to be a source of inflationary pressure in the near term. We do not seek or welcome further cooling in labor market conditions.

Overall, the economy continues to grow at a solid pace. But data on inflation and the labor market indicate that conditions are evolving. Upward risks to inflation have diminished. Downside risks to employment have increased. As we emphasized in our most recent FOMC statement, we are attentive to risks on both sides of our dual mandate.

It is time to adjust policy. The direction is clear; the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.

We will do what is necessary to support a strong labor market while continuing to make progress toward price stability. With an appropriate reduction in the degree of policy restraint, there is good reason to believe the economy can achieve a return to 2% inflation while sustaining a strong labor market. Our current level of the policy rate provides ample room to respond to any risks, including the risk of further deterioration in labor market conditions.

The Rise and Fall of Inflation

Now let us turn to why inflation rose and why it declined significantly even as unemployment remained low. Research into these questions is growing rapidly, and now is a good time to discuss them. Of course, definitive assessments are premature. This period will be analyzed and debated for many years to come.

The arrival of the pandemic quickly led to a global economic shutdown—a time of great uncertainty and severe downside risks. In times of crisis, Americans have consistently demonstrated adaptability and innovation. The government responded with unprecedented strength, particularly in the United States, where Congress passed the CARES Act with broad bipartisan support. At the Federal Reserve, we used our tools forcefully and in novel ways to stabilize the financial system and help avoid a depression.

After a historic but brief recession, the economy began recovering in mid-2020. As the risk of a prolonged, deep downturn receded and economies reopened, we faced the prospect of a slow recovery similar to that following the global financial crisis.

Congress provided substantial additional fiscal support at the end of 2020 and early 2021. In the first half of 2021, spending rebounded strongly. The ongoing pandemic shaped the pattern of recovery. Persistent health concerns limited face-to-face services. But pent-up demand, stimulus policies, changes in work and leisure patterns due to the pandemic, and accumulated savings from constrained service consumption together fueled a historic surge in consumer goods spending.

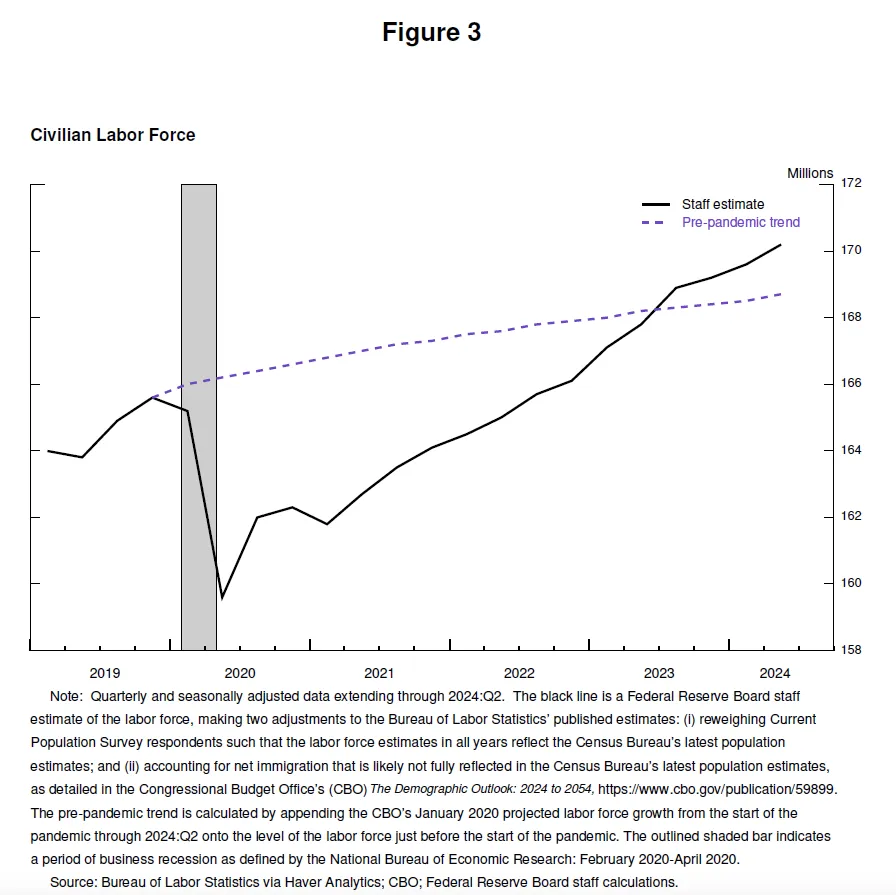

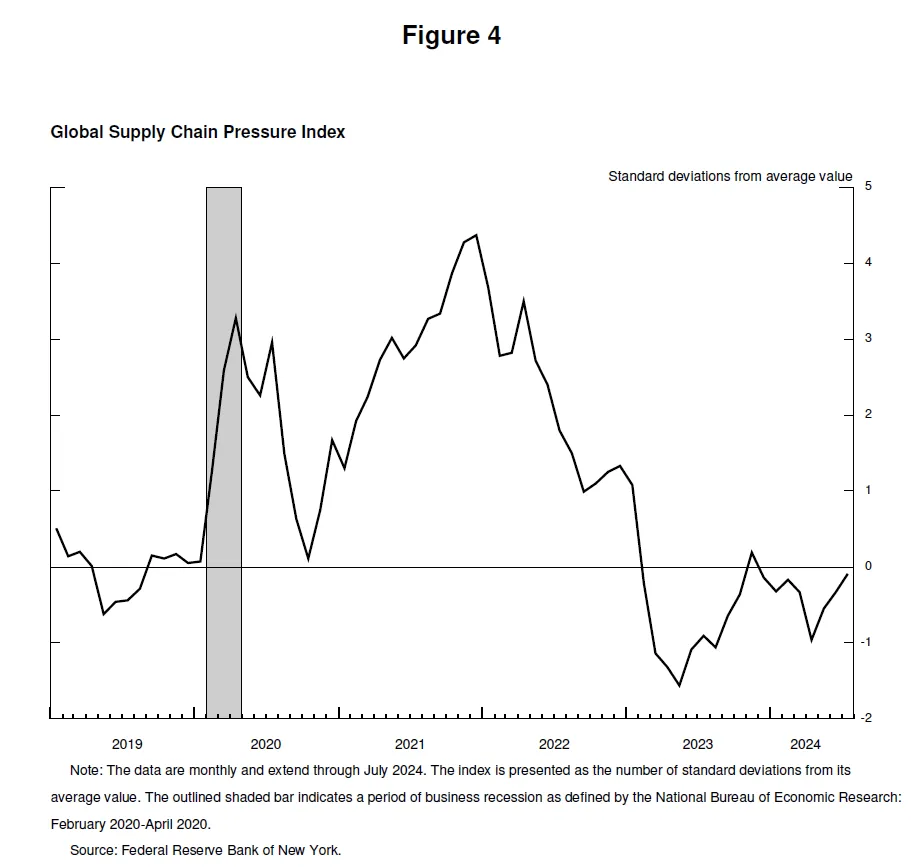

The pandemic also severely disrupted supply conditions. At its onset, 8 million people left the labor force; by early 2021, the workforce remained 4 million smaller than pre-pandemic trends. Labor force size did not return to its pre-pandemic trend until mid-2023.

Supply chains were thrown into disarray by worker absences, broken international trade links, and dramatic shifts in the structure and level of demand. This situation was clearly very different from the sluggish recovery after the global financial crisis.

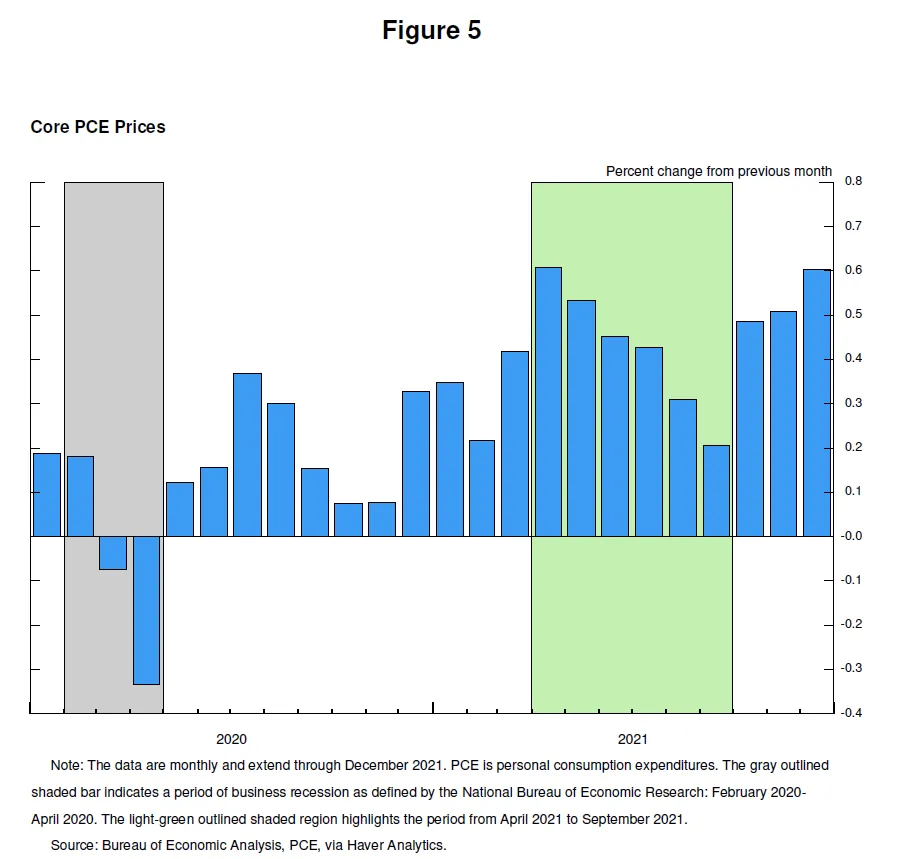

Inflation followed. After running below target in 2020, inflation surged in March and April of 2021. The initial spike was concentrated in goods experiencing supply shortages, such as motor vehicles, which saw very large price increases. My colleagues and I initially judged these pandemic-related factors to be transitory and expected the rise in inflation to pass quickly without requiring monetary policy action—in short, that inflation was “transitory.” The conventional wisdom had long been that central banks could look through temporary inflation spikes as long as inflation expectations remained well anchored.

The “transitory inflation” view was widely held at the time; most mainstream analysts and central bank leaders in advanced economies shared it. The prevailing expectation was that supply conditions would improve quickly, the rapid rebound in demand would run its course, and demand would shift from goods back to services, bringing inflation down.

For a time, the data were consistent with the transitory hypothesis. From April to September 2021, monthly readings of core inflation declined each month, though progress was slower than expected.

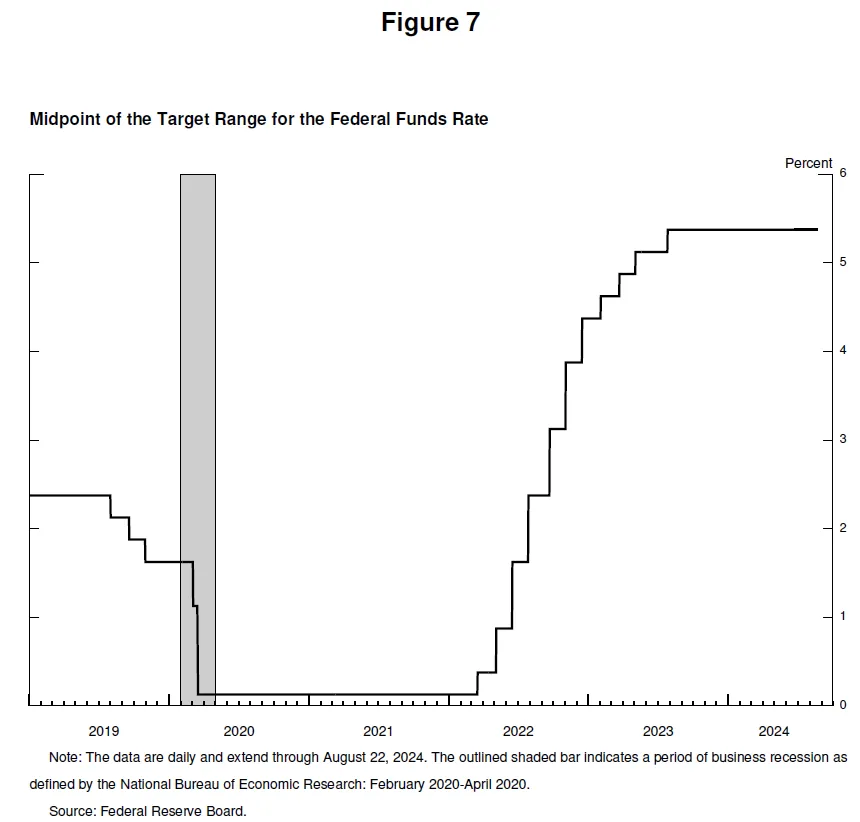

By midyear, support for the transitory narrative began to weaken, and our communications reflected this shift. Starting in October, the data clearly diverged from the transitory hypothesis. Inflation began spreading from goods into services. It became evident that high inflation was not temporary, and a strong policy response would be needed to keep inflation expectations anchored. We recognized this and began shifting policy in November. Financial conditions started tightening. After gradually ending asset purchases, we initiated interest rate hikes in March 2022.

By early 2022, headline inflation had exceeded 6%, and core inflation surpassed 5%. New supply shocks emerged. The war in Ukraine caused sharp increases in energy and commodity prices. Improvements in supply conditions, along with the shift in demand from goods to services, took longer than expected—partly due to continued developments in the U.S. pandemic. The pandemic also continued to disrupt production in major economies globally.

High inflation was a global phenomenon, reflecting common experiences: surging demand for goods, strained supply chains, tight labor markets, and sharp price increases for commodities. The global inflation surge differed from any period since the 1970s, when high inflation became entrenched—we are determined to avoid such an outcome.

By mid-2022, the labor market was extremely tight, with labor demand exceeding pre-pandemic trends by more than 6.5 million since mid-2021. Some of this demand was met as workers returned to the labor force after the pandemic eased. But labor supply remained constrained, and in summer 2022, labor force participation was still far below pre-pandemic levels. From March to December 2022, job openings were nearly twice the number of unemployed, signaling a severe labor shortage. Inflation peaked at 7.1% in June 2022.

Two years ago at this podium, I discussed some of the potential costs of fighting inflation, including rising unemployment and slower economic growth. Some argued that restoring price stability would require a recession and persistently high unemployment. I expressed our unwavering commitment to achieving a full return to price stability—and staying the course until the job was done.

The FOMC did not waver. We steadfastly fulfilled our duty, and our actions powerfully demonstrated our commitment to restoring price stability. We raised the policy rate by 425 basis points in 2022 and another 100 basis points in 2023. Since July 2023, we have maintained the policy rate at its current restrictive level.

Summer 2022 marked the peak of inflation. Over two years, inflation has declined 4.5 percentage points, with unemployment remaining low throughout—an outcome that is welcome and historically unusual.

Why Did Inflation Come Down Without a Significant Rise in Unemployment?

Pandemic-related imbalances in supply and demand, along with severe shocks in energy and commodity markets, were key drivers of high inflation, and their reversal played a crucial role in inflation’s decline. These factors took longer to dissipate than expected, but ultimately contributed importantly to the subsequent fall in inflation. Our restrictive monetary policy brought about a moderate decline in aggregate demand, which, combined with improving aggregate supply, reduced inflationary pressures while allowing the economy to continue expanding at a healthy pace. As labor demand slowed—with reductions in job openings—the historically elevated ratio of vacancies to unemployment normalized without widespread, disruptive layoffs, removing the labor market as a source of inflationary pressure.

It is also essential to highlight the critical importance of inflation expectations. Standard economic models have long held that inflation will return to target—without requiring an economic slowdown—as long as product and labor markets are balanced and inflation expectations remain firmly anchored at the target. That is what the models say. But since the 2000s, the stability of long-term inflation expectations had never been tested by sustained high inflation. Whether inflation expectations would remain anchored was far from certain. Concerns about de-anchoring reinforced the view that bringing inflation down would require an economic slowdown, particularly in the labor market. A key lesson from recent experience is that well-anchored inflation expectations, combined with strong central bank action, can bring inflation down without requiring an economic slowdown.

This narrative attributes the inflation surge primarily to an unusual collision between overheated, temporarily distorted demand and constrained supply. While researchers differ in their methods and conclusions, a consensus appears to be forming—one that I share—that places this collision at the center of the explanation for rising inflation. Overall, as markets recover from pandemic-induced distortions, our efforts to moderately restrain aggregate demand, and the anchoring of expectations, have collectively placed inflation clearly on a sustainable path toward our 2% objective.

Bringing inflation down while maintaining a strong labor market was possible only because inflation expectations remained anchored—reflecting public confidence that the central bank would achieve 2% inflation over time. This confidence was built over decades and reinforced by our actions.

This is my assessment of events. You may have a different view.

Conclusion

Finally, I want to emphasize that the pandemic economy proved unlike any previous period, and there is much more to learn from this extraordinary time. The Federal Reserve commits in its "Statement on Longer-Run Goals and Monetary Policy Strategy" to a comprehensive public review of our framework every five years, making appropriate adjustments. As we begin this process later this year, we will remain open to criticism and new ideas while preserving the strengths of our framework. The limits of our knowledge—so evident during the pandemic—require humility and intellectual curiosity, a focus on learning from past experience, and flexibility in applying those lessons to current challenges.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News