Galaxy: A Detailed Look at the Risks and Rewards of Ethereum Staking Economics

TechFlow Selected TechFlow Selected

Galaxy: A Detailed Look at the Risks and Rewards of Ethereum Staking Economics

To reduce the ETH staking rate, Ethereum's monetary policy may be adjusted.

Author: Christine Kim, Vice President at Galaxy Research

Translation: Luffy, Foresight News

This report provides a comprehensive overview of staking, how staking works on Ethereum, and key considerations for stakeholders participating in staking. It is the first part (of three) in a series exploring the risks and returns associated with various staking activities, including restaking and liquid restaking. The second report will outline restaking, its mechanisms on Ethereum and Cosmos, and the key risks involved.

Introduction

Ethereum is the largest proof-of-stake (PoS) blockchain by total value staked. As of July 15, 2024, ETH holders have staked over $111 billion worth of ETH, representing 28% of the total ETH supply. The amount of staked ETH, also known as Ethereum’s “security budget,” reflects the collateral at risk for validators who may be penalized by the network in the event of double-spending attacks or other protocol violations. In return for securing Ethereum, stakers are rewarded through protocol issuance, priority fees, and maximum extractable value (MEV). Users can easily stake ETH via liquid staking pools without sacrificing asset liquidity, driving demand for staking beyond developers’ initial expectations. Based on current staking trends, developers anticipate further increases in ETH staking rates over the coming years. To mitigate this trend, developers are considering significant changes to the protocol's issuance policy.

This report outlines staking on Ethereum, covering types of stakers, associated risks and rewards, and projections for staking rates. It also offers insights into developer proposals aimed at curbing staking demand through adjustments to network issuance.

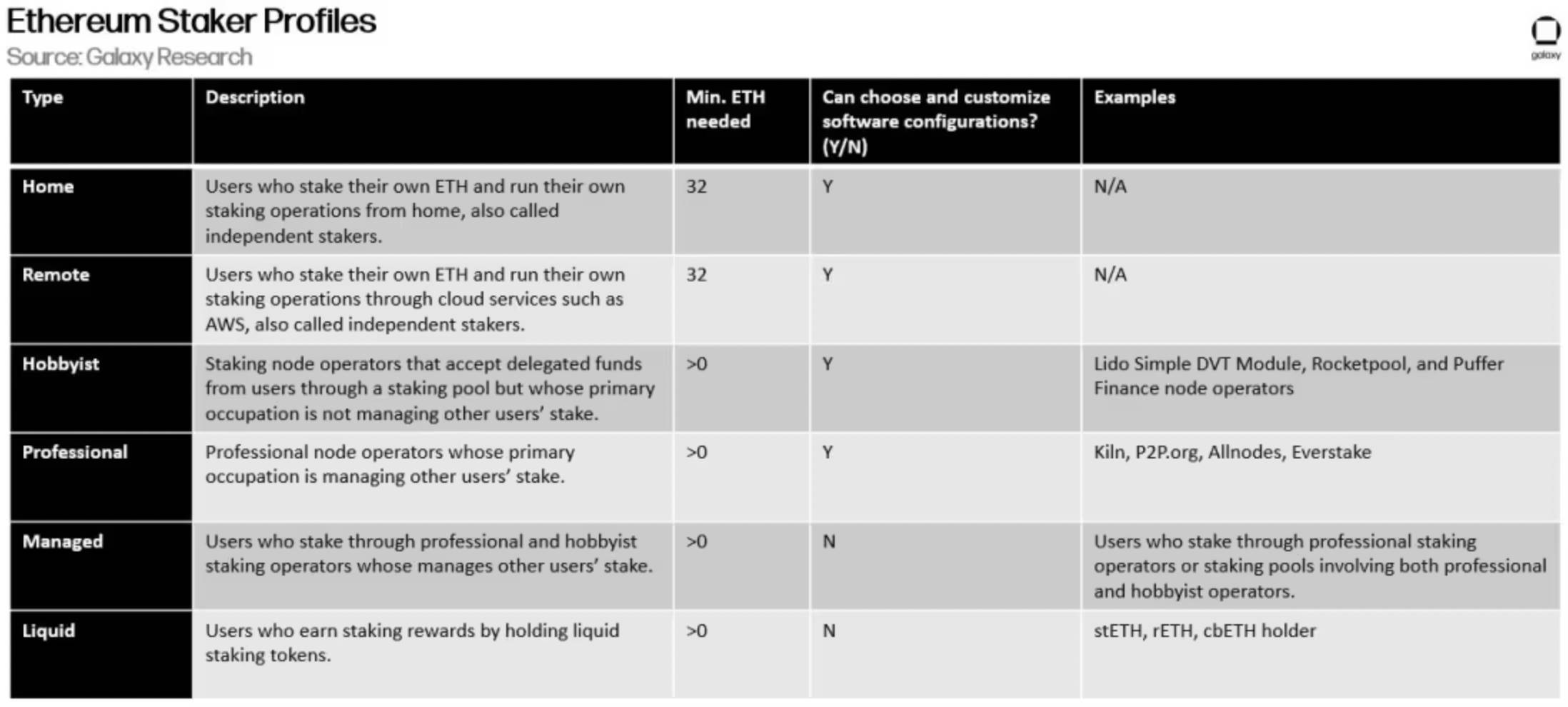

Types of Stakers

There are six main types of Ethereum users who can earn rewards through staking. The table below details their respective profiles:

Among these stakers, custodial stakers—those who delegate ETH to professional node operators—are the most numerous. While professional operators are fewer in number, they manage the largest share of staked ETH among all staker entity types.

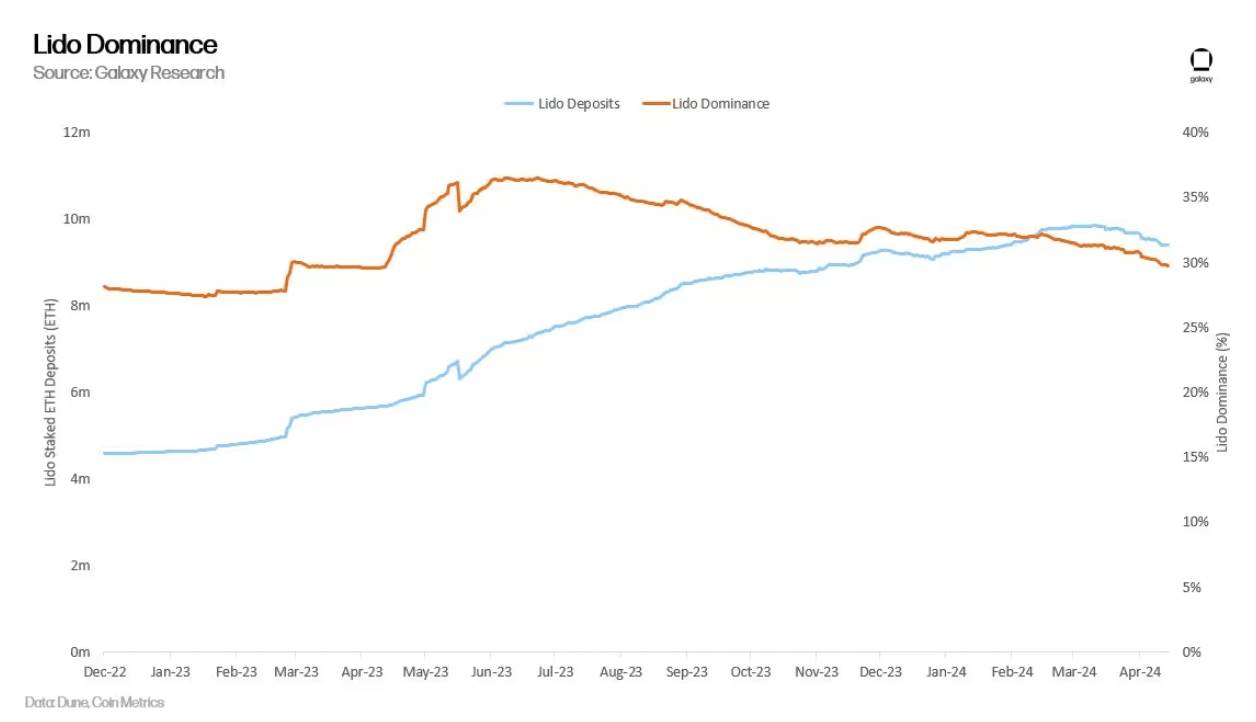

Liquid staking, restaking, and liquid restaking pool protocols are not considered in this analysis, as these entities do not directly operate staking infrastructure or fund its use. However, they do receive a portion of staking rewards from users leveraging their platforms and act as intermediaries connecting custodial stakers with professional (or amateur) stakers, making them important participants in Ethereum’s staking ecosystem. Lido, a liquid staking protocol, is currently the largest staking pool operator on Ethereum, accounting for 29% of staked ETH. Given the widespread adoption and critical role of liquid staking pools on Ethereum, understanding their risks is essential.

The next section of this report will delve deeper into staking risks based on the technologies and entities used to earn staking rewards.

Staking Risks

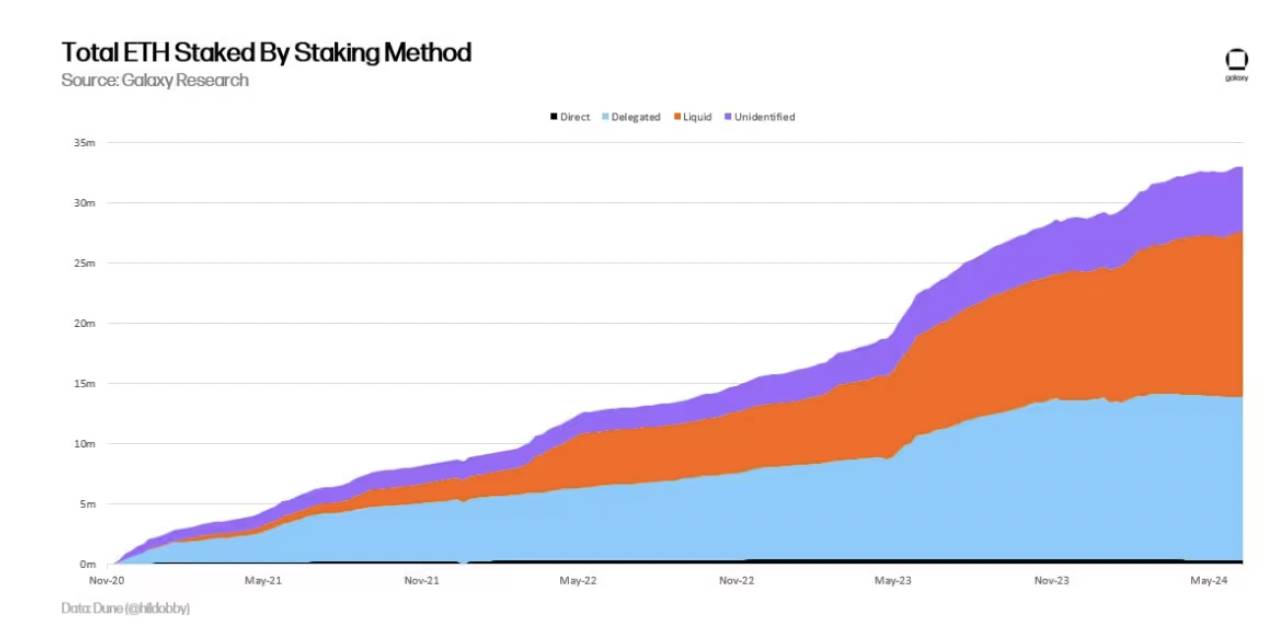

Staking-related risks largely depend on the method and technology used. Below are three major categories defining staking methods and their associated risks:

Direct Staking: Users or entities directly operate their own dedicated staking hardware and software. Risks include penalties and slashing. Downtime-related penalties may result in partial loss of staking rewards; misconfigured validator software or similar errors leading to slashing events could result in partial loss of staked ETH balance, up to 1 ETH.

Delegated Staking: Users or entities delegate their ETH to professional or amateur stakers for staking. Delegated staking carries all risks of direct staking, plus counterparty risk, as the entity receiving delegation may fail to fulfill responsibilities. ETH holders can delegate to minimally trusted staking providers—such as those governed by smart contract code—but this introduces additional technical risks, including potential code vulnerabilities or system hacks.

Liquid Staking: Users or entities delegate staking to professionals or amateurs and receive liquid tokens representing their staked ETH. Liquid staking includes all risks of direct and delegated staking. Additionally, due to market volatility and delays in validator entry/exit queues, liquidity risk may lead to depegging events where the value of liquid staking tokens significantly diverges from the underlying staked assets.

Total ETH staked across three different methods

Another notable risk across these three staking methods is regulatory risk. The further ETH holders are from direct control over their staked assets, the greater the regulatory exposure. Delegated and liquid staking require ETH holders to rely on various intermediary entities, which regulators and lawmakers may subject to specific rules and frameworks depending on their structure and business models.

Beyond regulatory risks, it is important to detail the protocol-level risks associated with these three staking types. Protocol risks arise when the network penalizes users—intentionally or unintentionally—for failing to meet standards and rules defined in Ethereum’s consensus protocol. There are three primary types of penalties, ranked from least to most severe:

-

Downtime Penalties: Applied when a node is offline and fails to perform duties such as proposing blocks or signing attestations. Typically, validators lose only a few dollars per day.

-

Initial Slashing Penalties: Imposed when a validator’s rule violation is detected by others. The most common cases involve proposing two blocks for the same slot or signing two attestations for the same block. Penalties range from 0.5 ETH to 1 ETH, depending on the validator’s effective balance—currently capped at 32 ETH. Developers are considering increasing the maximum effective balance to 2048 ETH and reducing initial slashing penalties in the upcoming Pectra network upgrade.

-

Correlation Slashing Penalties: A secondary penalty applied after an initial slashing, based on the total amount of staked ETH slashed within an 18-day window around the event. This penalty aims to scale punishment relative to the amount managed by malicious validators. It is calculated using the offending validator’s effective balance, total balance, and proportional slashing multiplier.

In addition to the above, if the network fails to achieve finality, validators may face special penalties. (For a detailed overview of Ethereum finality, see this Galaxy Research report.) When finality is not reached, offline validators face increasingly severe penalties. By gradually burning the stakes of validators not contributing to consensus, the network rebalances the validator set to restore finality. The longer finality is delayed, the harsher the penalties become.

Staking Rewards

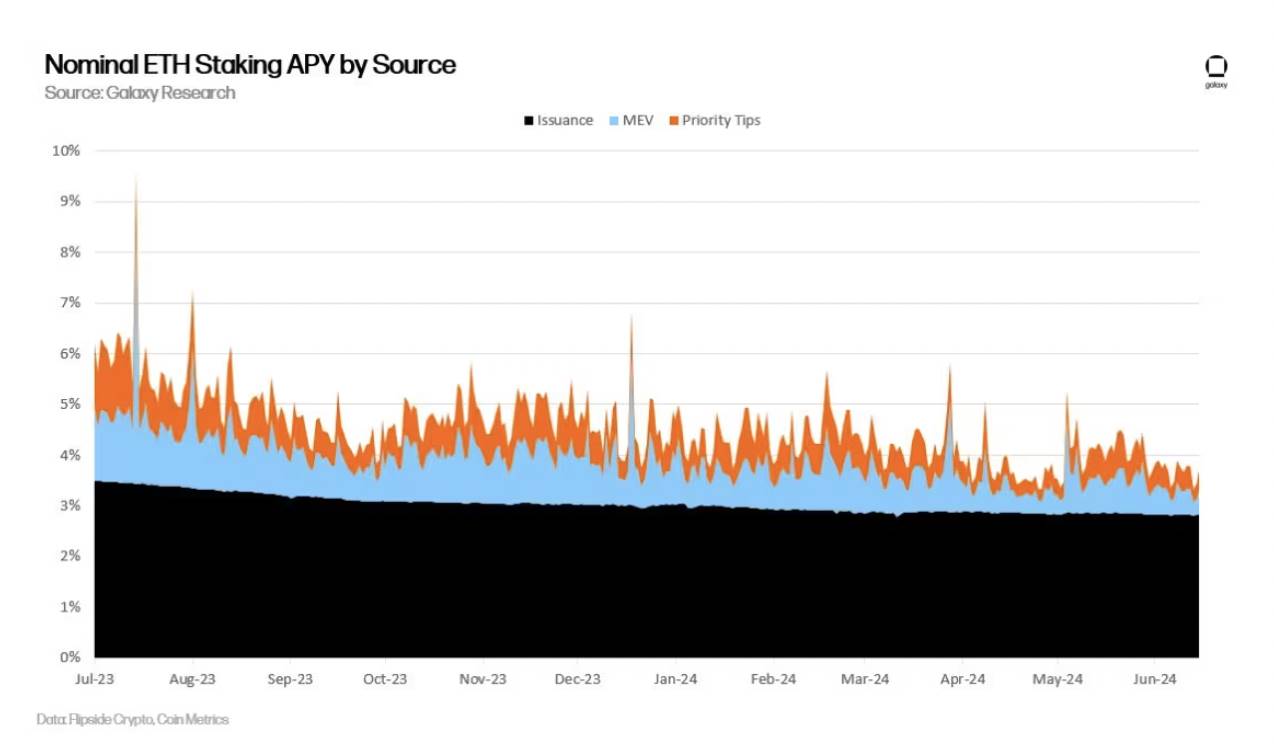

Of course, stakers earn approximately 4% annualized yield on staked ETH while assuming risk. These rewards come from new ETH issuance, priority fees attached by users to transactions, and MEV.

Nominal staking yield of ETH

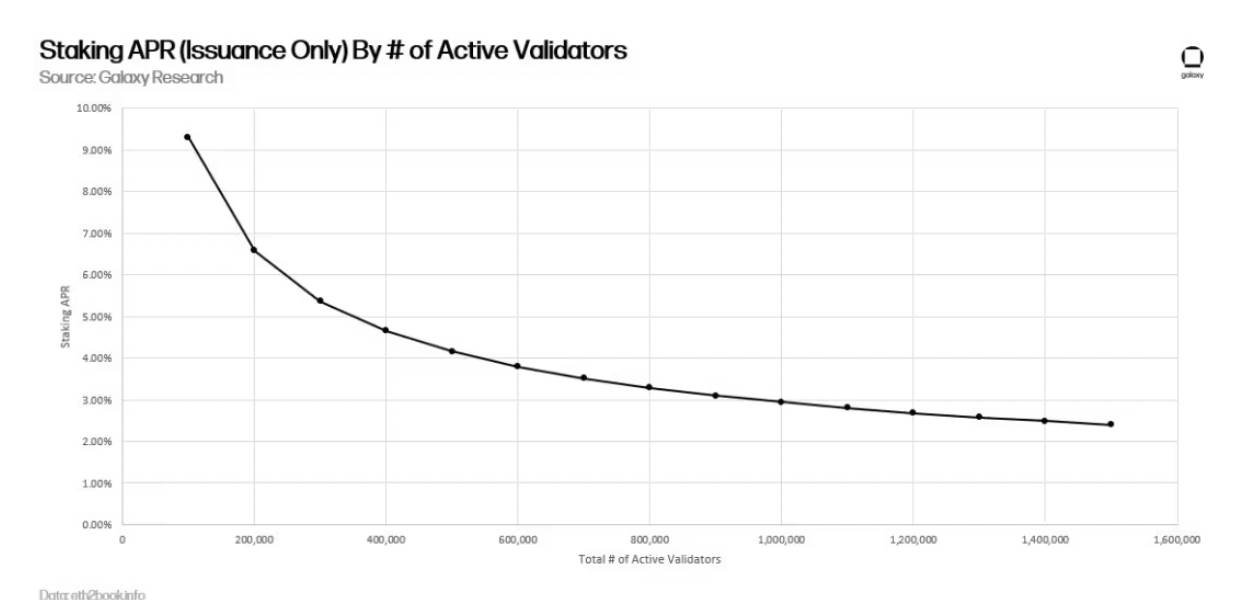

Note that over the past two years, staking rewards have steadily declined for two main reasons. First, both the total amount of staked ETH and the number of validators have increased. As more value is staked, issuance rewards are diluted for each validator, as illustrated below:

Staking yield paid solely by ETH issuance

While issuance rewards can be calculated based on the total number of active validators and the amount of ETH staked on Ethereum, the other two sources of validator income are harder to predict, as they depend on network transaction activity.

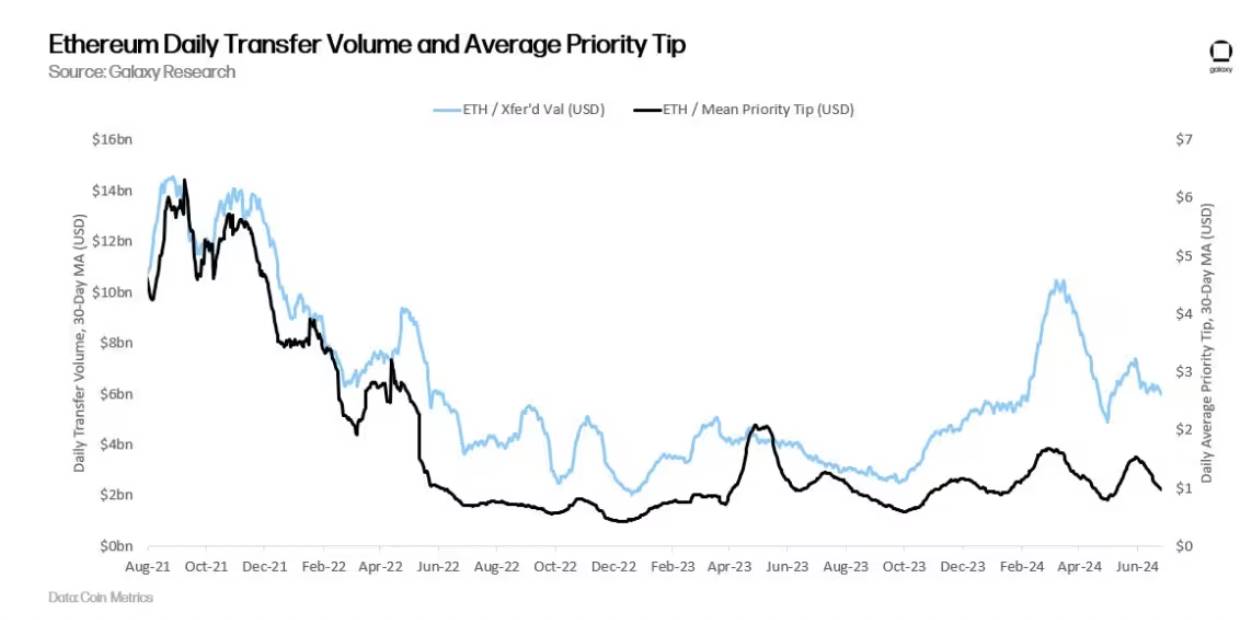

Over the past two years, reduced transaction activity has led to lower base fees, priority fees, and MEV for validators. Generally, the higher the value of assets transferred on-chain, the more willing users are to pay tips for priority transaction inclusion, and the higher the MEV profits for searchers reordering transactions within blocks. As shown below, daily dollar value transferred on Ethereum correlates with transaction priority fees:

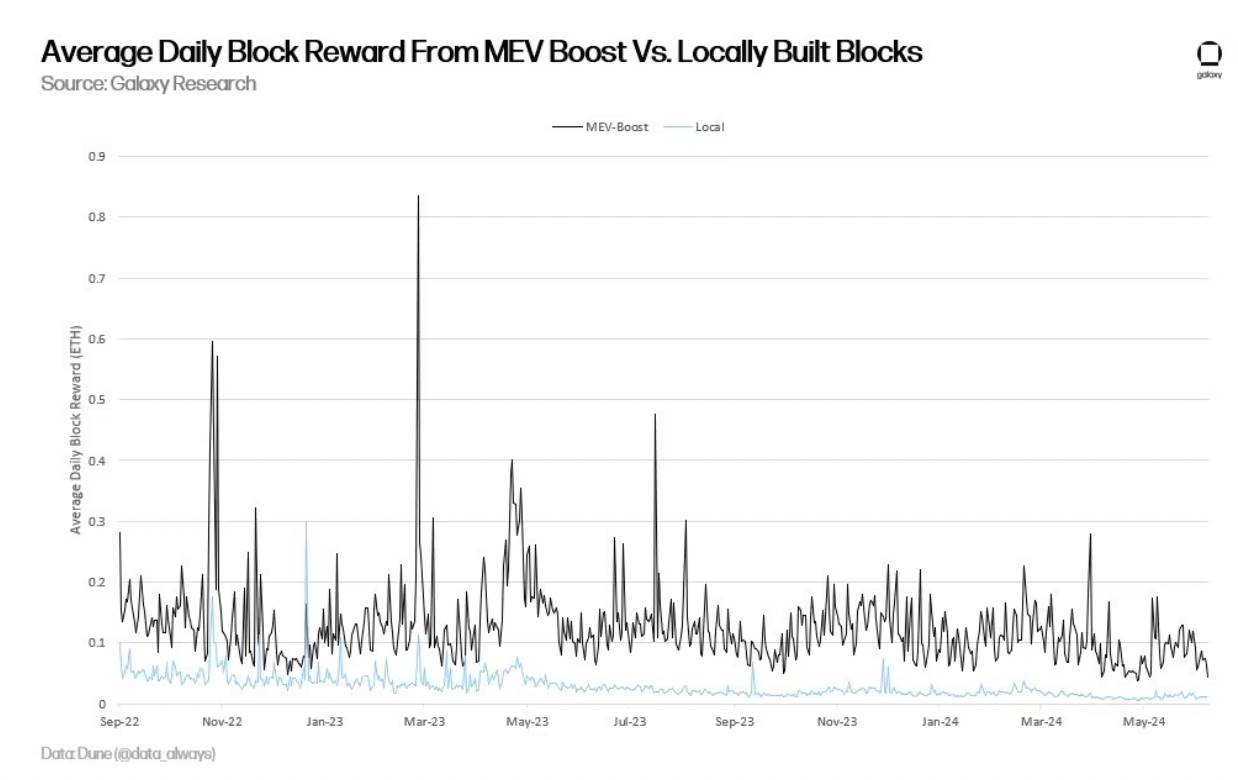

According to Galaxy’s calculations, MEV can boost validator yields by approximately 1.2%. Compared to other forms of validator income—including new ETH issuance and priority fees—MEV accounts for about 20% of validator rewards. Some view MEV as extra value given to block proposers beyond priority fees or ETH issuance. Others argue that priority fees themselves can represent MEV profits if funded through successful frontrunning or backrunning trades. To account for the fact that priority fees may inherently contain MEV, alternative methods compare the value of blocks built with MEV-Boost software versus those built without it.

The chart above suggests MEV may be significantly larger than 20% of validator rewards. According to analysis by Ethereum Foundation researcher Toni Wahrstätter in October 2023, median block rewards increase by 400% when validators receive blocks via MEV-Boost instead of building blocks locally.

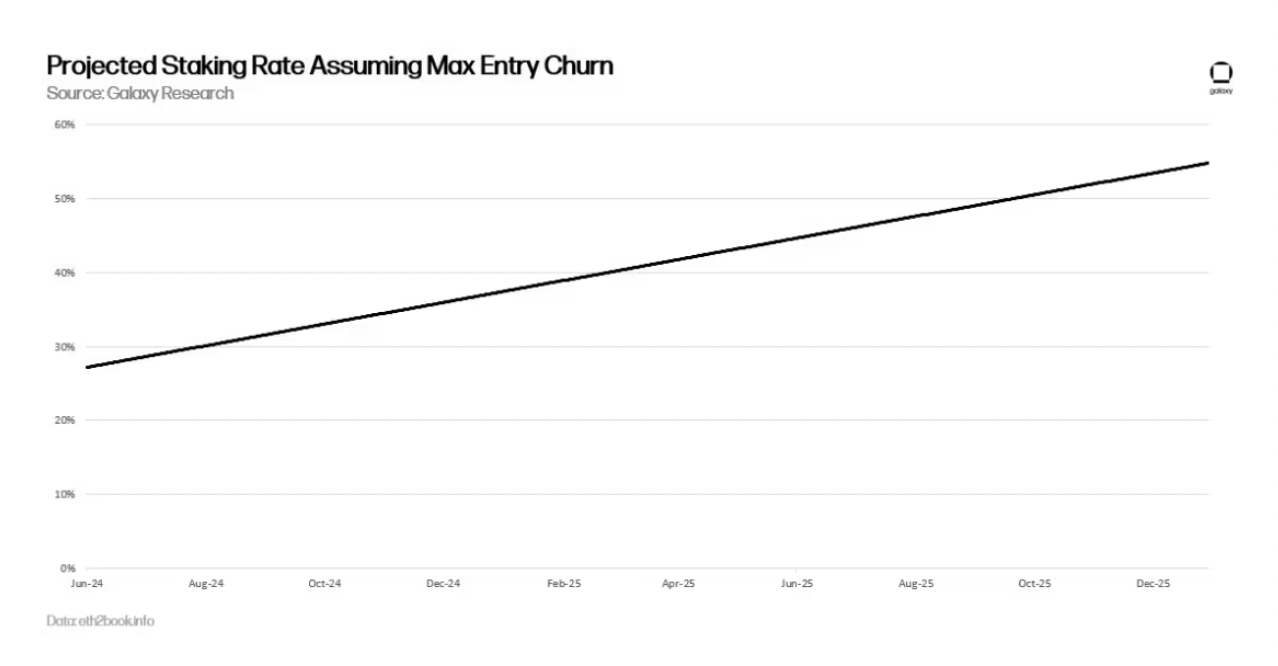

Staking Rate Projections

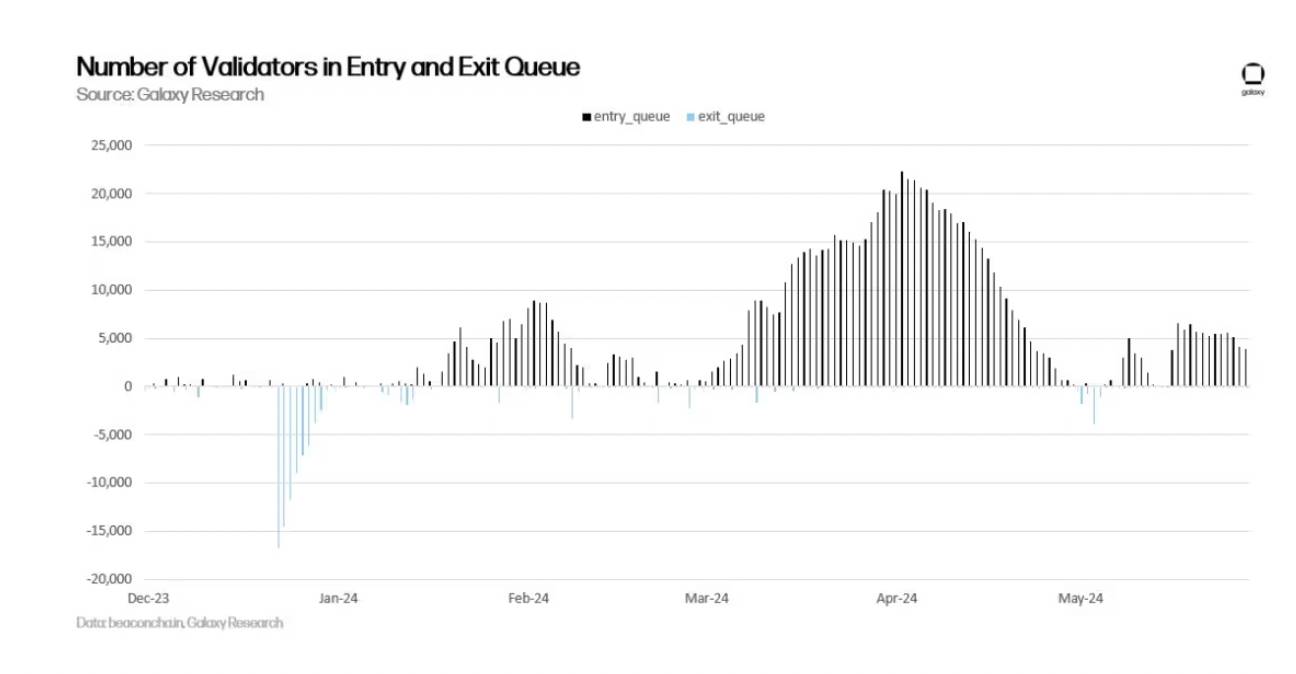

Assuming staking demand on Ethereum continues growing linearly as it has over the past two years, the staking rate is expected to exceed 30% in 2024. As noted earlier, higher staking rates reduce returns from new ETH issuance. Liquid staking services on Ethereum make it easy for users to stake while bypassing entry queues and other barriers. Users can simply buy stETH to gain exposure to staking rewards. Heavy buying of stETH can cause its market value to deviate from the underlying staked asset value, creating an stETH premium until more ETH is staked on Ethereum. In contrast, actual staking on Ethereum is delayed. Only 8 new validators—or up to 256 ETH in effective balance—can be added per epoch (6.4 minutes). Therefore, even if the maximum number of validators were added every epoch until the end of 2025, it would take over a year (specifically 466 days) for Ethereum to reach a 50% staking rate.

Historically, demand to join the Ethereum staking queue has exceeded withdrawal demand. Although recent days have seen reduced queue entry activity, staking demand is expected to surge again due to several factors, including additional yield opportunities via restaking, increased MEV from a revival in DeFi activity, and regulatory shifts enabling staking in traditional financial products like ETFs.

Validators in entry and exit queues

Developers recognize that rising staking rates and declining staker yields are inevitable, prompting consideration of several network issuance changes to curb staking demand.

Discussion on Changes to New ETH Issuance

ETH holders should be aware that future staking yields may undergo significant changes. Ethereum developers are evaluating multiple options to guide the staking rate toward a target threshold, such as 25% or 12.5%. Ethereum Foundation researcher Caspar Schwarz Schilling explains the main reasons for maintaining a low staking rate:

-

Dominance of Liquid Staking Tokens (LSTs): Higher staking rates could concentrate more ETH within a single staking pool (e.g., Lido), increasing centralization risks and the influence of a single entity or smart contract on Ethereum’s security.

-

Credibility of Slashing: Related to concerns about LST dominance, high issuance flowing into a single entity or application could undermine the credibility of large-scale slashing events. For example, if a slashing event affects most stakers, the protocol might face pressure from ETH holders to revert the state and restore penalized balances. Ethereum has only made one irregular state change before—the response to the infamous 2016 DAO hack. While unlikely, an irregular state change in response to mass slashing is not impossible. In fact, some researchers believe such an outcome becomes more likely under high issuance conditions.

-

ETH as Trustless Base Money: High staking rates could lead to insufficient circulating native ETH and a surge in third-party-issued liquid staking tokens. Ethereum researchers prefer promoting native ETH usage beyond staking rather than relying on less decentralized LSTs.

-

Minimum Viable Issuance (MVI): Although staking costs are negligible compared to mining, they are not zero. Professional staking providers must run required hardware and software, incurring operational expenses. Users must pay fees to these providers. Moreover, even if users obtain liquid staking tokens by staking native ETH, they assume additional risk if third-party operations fail. Keeping staking costs minimal serves the network’s interest, as higher costs necessitate higher issuance, leading to ETH supply inflation.

Ethereum developers and researchers are weighing various proposals to reduce the staking rate. These include:

-

Short-term: Reduce staking rewards. In February 2024, Ethereum Foundation researchers Ansgar Dietrichs and Caspar Schwarz-Schilling revived a proposal for a one-time reduction in staking yields—an idea originally introduced by Anders Elowsson. In their latest paper, they suggest cutting staking yields by 30%, though the exact figure depends on the current staking rate. Given rising staking rates since February, researchers believe the theoretical cut should now be higher. This proposal requires only minor code changes and aims to dampen economic incentives for staking by reducing short-term issuance. It is intended as a temporary measure paving the way for long-term solutions like target policies.

-

Long-term: Implement a staking ratio target. Introduce a new ETH issuance curve where the higher the staking rate exceeds a target threshold (e.g., 25% of total ETH supply staked), the more expensive it becomes for validators to stake and earn rewards. This concept builds on research by Elowsson, Dietrichs, and Schwartz-Schilling. Several mechanisms could implement such a target, differing in issuance schedule and the degree of issuance decline. For more details on issuance curves under a staking ratio target model, refer to this Ethereum Research article.

None of the above proposals are scheduled for inclusion in the next Ethereum hard fork, Pectra. However, developers are likely to push for issuance changes in subsequent upgrades. So far, discussions within the Ethereum community about issuance changes have been highly contentious, with no broad consensus. Key objections include concerns that reduced staking income could harm profitability for large staking providers and individual stakers; existing proposals lack sufficient research and data-driven analysis. It remains unclear what the ideal target staking rate for achieving MVI should be, and whether changing issuance would alleviate concerns about centralization of staking distribution—or worsen them by driving away independent stakers. To address concerns about long-term profitability for independent stakers, Ethereum co-founder Vitalik Buterin shared preliminary research in March 2024 on introducing anti-correlated rewards and penalties favoring node operators managing fewer validators.

Ethereum’s proof-of-stake beacon chain, launched in December 2020, has maintained unchanged monetary policy since inception. However, prior to the merge, Ethereum’s monetary policy underwent several revisions over its roughly seven-year history. The original block reward was set at 5 ETH/block. It dropped to 3 ETH during the Metropolis upgrade in September 2017, then to 2 ETH during the Constantinople upgrade in February 2019. Later, the London upgrade in August 2021 burned miner rewards from transaction fees, and the Merge upgrade in September 2022 completely eliminated mining rewards.

Under proof-of-stake, changes to Ethereum’s monetary policy may prove more controversial than previous issuance changes under proof-of-work, as they affect a much broader user base. Unlike miners, issuance changes now impact a growing number of ETH holders, staking service providers, liquid staking token issuers, and restaking token issuers. With a broader base of stakeholders securing Ethereum, developers are less likely to frequently alter monetary policy as they did in the past. The contentious nature of these debates may lead to increasingly rigid staking policies and rewards over time. Consequently, the window of opportunity to change Ethereum’s codebase is narrowing and unlikely to remain open for long.

Conclusion

The staking economy built on Ethereum is still in its infancy. When the beacon chain launched in 2020, users staking ETH had no guarantee of being able to withdraw or move funds back to Ethereum. When the beacon chain merged with Ethereum in 2022, users began earning additional rewards via transaction priority fees and MEV. In 2023, the ability to withdraw staked ETH was enabled, allowing users to exit validators and realize profits from staking operations. Several other changes are on Ethereum’s development roadmap that will impact staking businesses and individual stakers. While many of these changes—such as increasing the validator’s maximum effective balance in the Pectra upgrade—may not affect staking economics, some will.

Therefore, as Ethereum’s roadmap evolves and is implemented through hard forks, carefully assessing the risks and returns of staking on Ethereum is crucial. Since Ethereum’s staking economy involves far more stakeholders than during its PoW era, changes affecting staking dynamics may become increasingly difficult to execute over time. Nevertheless, Ethereum remains a relatively new PoS blockchain, and significant changes are expected in the coming months and years. The impact of altering staking dynamics on all relevant stakeholders must be carefully considered.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News