Living in safety, think of danger—what stage of this cycle are we in?

TechFlow Selected TechFlow Selected

Living in safety, think of danger—what stage of this cycle are we in?

We are still in the early stages of this cycle.

Written by: 0xsmac

Translation: TechFlow

Introduction

The author, 0xsmac, delves into the current cyclical position of the crypto market and questions the effectiveness of "wisdom of the crowd" in financial market decision-making. The article reviews market changes since the FTX collapse in November 2022 and uses a comparison between Bitcoin and Ethereum price trends to forecast future market movements. Additionally, the author discusses the potential impacts of ETF approvals, institutional capital inflows, and structural changes within the cryptocurrency market, offering a deep understanding of the crypto market landscape.

Main Content

I tend to think that the wisdom of the crowd is mostly a joke. Of course, collective sentiment matters in certain contexts, but there are far too many examples where human behavior is irrational—especially when money is involved—or fails to recognize the cognitive biases they’re experiencing. More specifically, I’m referring to crowds with tendencies toward overconfidence and irrationality.

For instance, participants in financial markets.

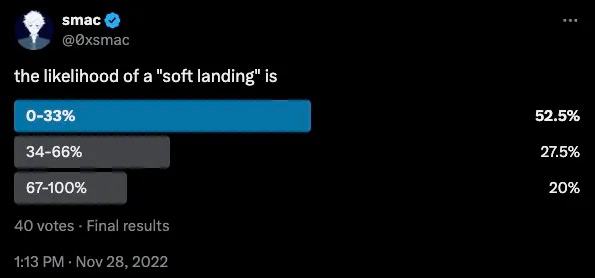

After the FTX collapse in November 2022 and the Nasdaq-100 (QQQ) dropping roughly 30% from its all-time high, I was curious about people’s views on a possible “soft landing.” Unsurprisingly, only one in five respondents was fairly confident we’d achieve it.

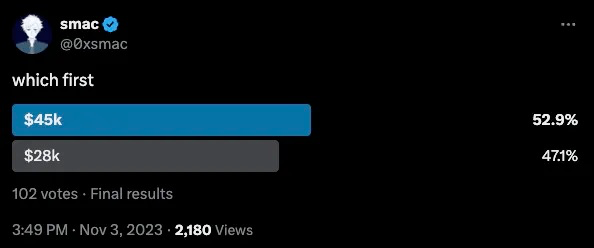

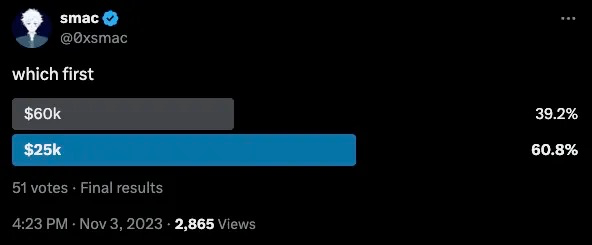

A year later, with Bitcoin having doubled in price (around $35,000) and clearly in an uptrend, I became curious again about sentiment. I often use polls like this to gauge positioning. It’s just one data point, but I’ve found most people answer based on what they wish would happen—especially on Twitter. So it’s no surprise that only half believed a ~30% upside was more likely than a 20% downside.

Even fewer expect prices to continue rising.

For various reasons, I was very confident at the time that targets of $45,000 and $60,000 would be reached. Now, my confidence in short-term price action is lower, and I'm somewhat uncertain about what might happen over the next six months or so. But many keep asking, “Where are we in the cycle?” This is a somewhat complicated question that already assumes things I’m not sure are necessarily true. Nevertheless, I’ll share my thoughts here so that the next time I inevitably get asked this, I can simply refer back to this piece.

The prevailing view seems to be that we're in the middle of the cycle. Interestingly, the most common answer I hear is “round five or six.” Even if true, that feels a bit like an evasive response—the kind of thing you say when you don’t have an opinion and want to stay neutral. It could be right, but if I thought so, I wouldn't be writing this article.

So where exactly are we in the cycle? Are we in the early innings, late stage, past the peak, or just getting started? Let me begin with another tweet from November 2022.

I mention this to highlight that in “this cycle,” price and time are two very different concepts. Looking at them separately, from a timing perspective, we’re around week 70 of the bull run. That said, I’d argue this actually overstates the true duration of this cycle. I could count on one hand the number of genuinely bullish people in November and December 2022. If I’m being generous, I’d say ~most~ people didn’t start realizing what was happening until sometime in Q1 or early Q2 last year. So we’re barely over 12 months in.

From a price perspective, Bitcoin has tripled from its lows, while Ethereum is up roughly 2.5x. Many who’ve lived through multiple crypto cycles feel we’re closer to the end than the beginning. This is largely because this cycle hasn’t followed the script they’re used to.

We wrote about this dynamic in our annual letter...

In previous crypto cycles, capital moved along a risk and speculation curve, following a logical flow: BTC → ETH → long tail of crypto assets (for risk and token investments). Market participants embraced new narratives, often centered around fundamental shifts enabled by crypto, creating waves of new believers—some lifelong converts, others exiting once prices retreated.

This cycle has been (so far) very different, and many who relied on past heuristics have been slow or unwilling to adapt. Frankly, this resistance has led to self-deception. We’re all human, so we naturally look around and evaluate ourselves (and our holdings) relatively—when our assets are up 3–5x, we aren’t satisfied because the ones we don’t own have surged 10–20x. Especially if those surging 10–20x are things we dislike. To me, this is precisely why many feel we’re either mid-cycle or in the latter half. They watch Solana go from under $10 to over $200. They see memecoins explode 100–1000x and scream internally.

"That's not the right order!"

"Why isn’t my asset doing that?"

"That shouldn’t be happening now!"

Things simply aren’t unfolding the way they wanted. So instead of questioning whether they might be wrong, they label the market as irrational. Or claim the cycle is compressed, or that financial nihilism has gone extreme. I don’t rule out these possibilities, but there’s little introspection.

For context, I know junior analysts at other funds recommended SOL below $30, only to be repeatedly dismissed. Months later, it’s almost comical how many scrambled to buy locked FTX tokens at much higher prices.

All this shows that the collective experience of the market rally shapes perceptions of where we stand in the cycle. Entering this cycle, most were overly focused on the Ethereum ecosystem and neglected everything else. This skewed the overall perception of crypto and distracted many from assessing our actual position.

So let’s weigh the arguments: are we closer to the early or late stages of this cycle?

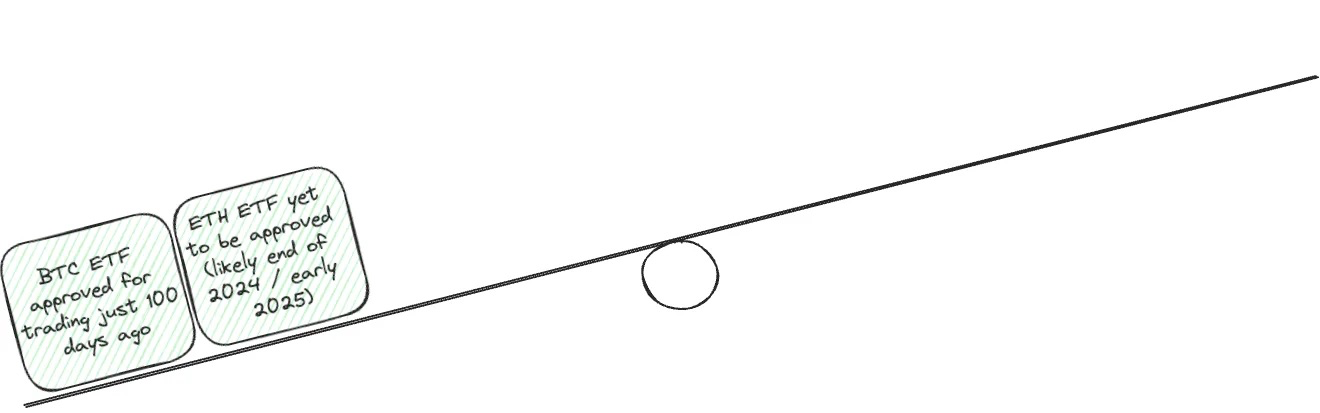

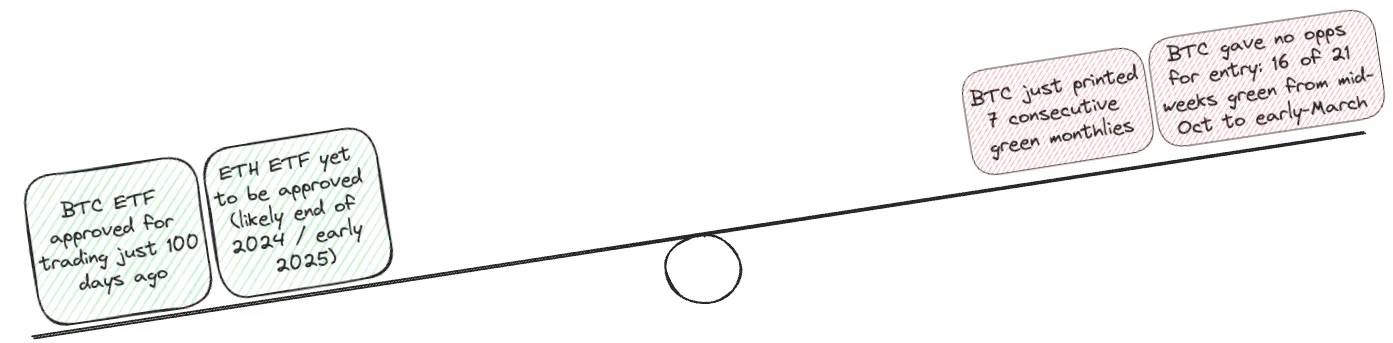

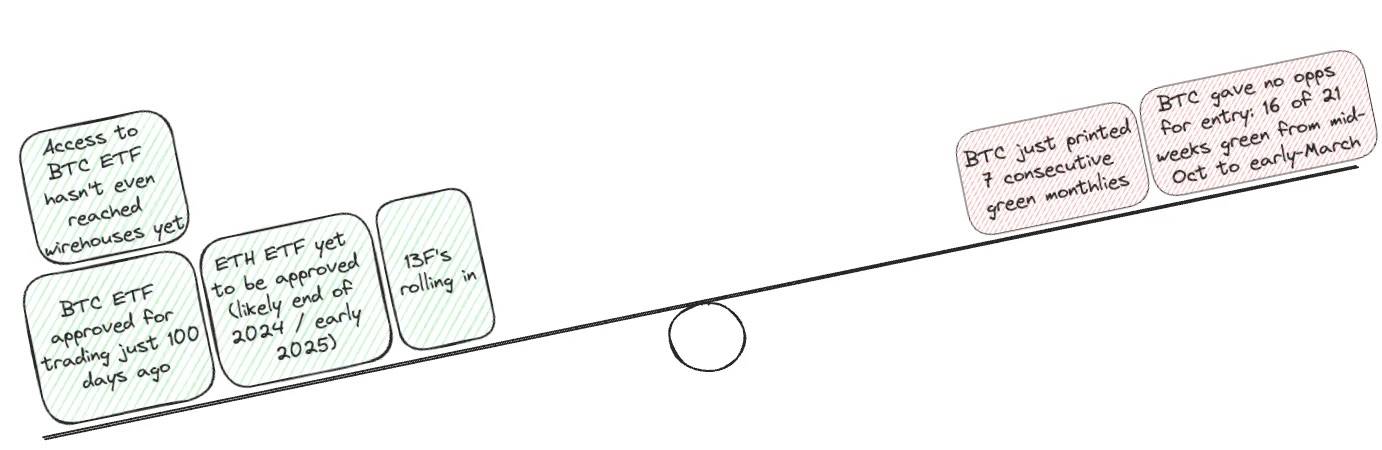

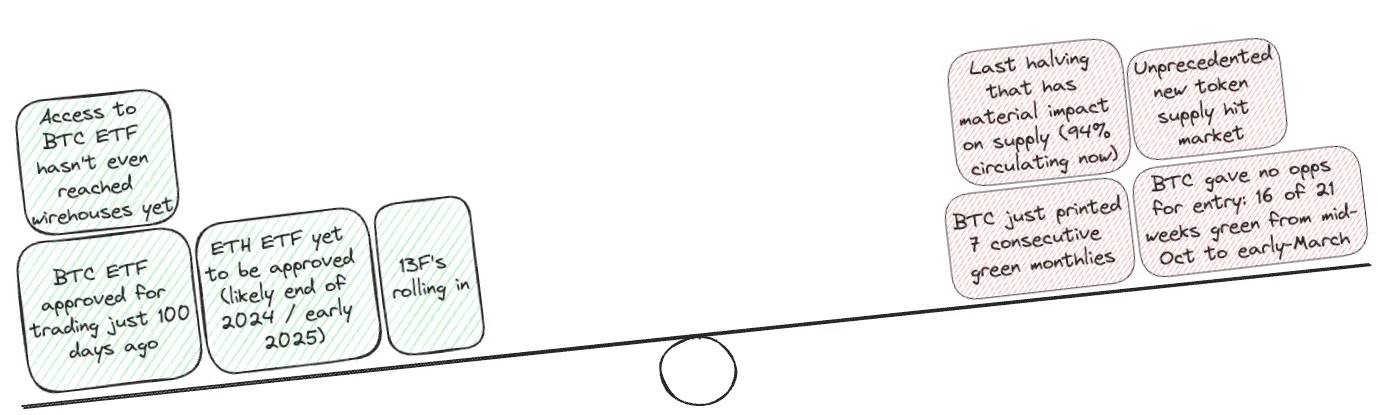

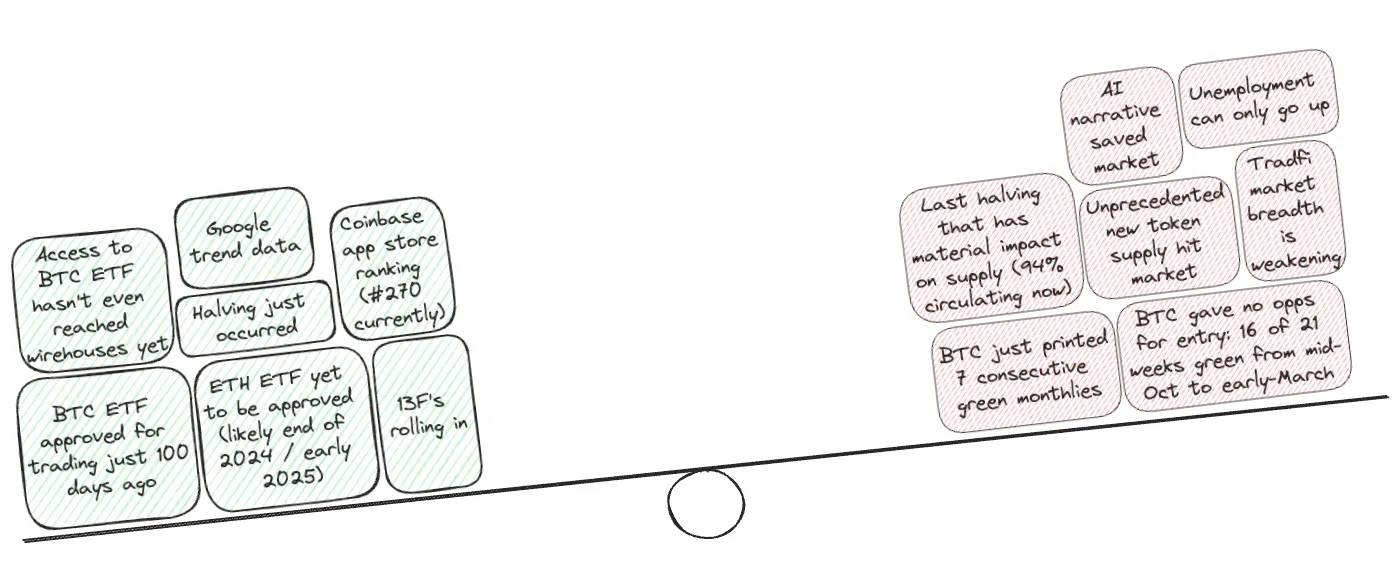

Only 100 days since Bitcoin ETF approval

Ethereum ETF not yet approved (likely late 2024 / early 2025)

I’ve written and tweeted extensively about crypto market structure and its significance—even though it sounds boring, it has massive implications. It’s a bit dramatic, but I liken it to tectonic plates—vast, slowly shifting parts of the market. In real time, it’s hard to sense how transformative these shifts will be or what aftershocks they’ll cause. But imagine being in crypto for 8, 9, or 10 years and witnessing the moment Bitcoin ETFs are approved.

Vast pools of new institutional capital now have a legitimate entry path into this asset class. Initial inflows have far exceeded broad market expectations, yet some declare the top just 100 days after ETF approval. But markets are forward-looking! Now that ETFs are approved, the flows are already priced in!

Yes, markets are forward-looking—but they’re not omniscient. Their assumptions about ETF inflows were actually wrong. People familiar with crypto don’t understand traditional market mechanics, and those familiar with traditional finance rarely spend time studying crypto. An ETH ETF is inevitable. In my view, the gap between BTC and ETH approvals is actually healthy—it allows time for digestion, education, and post-election clarity. The structural shift in crypto markets cannot be overstated.

Bitcoin has just posted seven consecutive months of gains

Bitcoin offered no entry points: 16 green weeks out of 21 from mid-October last year to early March

Bitcoin has actually been rising for about a year and a half. Prior to April, 12 out of the past 15 months were positive. From mid-October last year to early March this year, 16 out of 21 weeks were green. That’s relentless. Still, few were prepared for what we saw in the first half of 2023. Would a period of consolidation shock us? No, I don’t think so. But judging by market momentum, there still seems to be PTSD from the last washout.

I also increasingly feel like I’m having the same conversations I had at the end of 2022 or early 2023—except now Bitcoin is around $60,000 instead of $18,000. Of course, they’re not identical, but skepticism centers on: we’ve already risen a lot, there’s no new narrative pushing us further, and memes have gone crazy.

But to me, none of these are valid reasons to believe we should decline.

BTC ETFs not yet available in offline broker channels

13Fs continue to emerge

Alright, now we’re diving into some banking-sector technicalities. When I say ETF access isn’t in offline broker channels yet, I mean advisors currently have no incentive to recommend the product to clients.

Advised trades fall into “solicited” and “unsolicited” categories. Solicited trades are those recommended by brokers (“you should buy ABC”), while unsolicited trades are initiated by clients (“I want to buy XYZ”). The key difference: commissions are paid only on solicited trades.

Currently, no brokerage firm allows BTC ETFs in client portfolios. This means advisors have zero incentive to recommend them. But that’s just a matter of time—all firms are in a wait-and-see mode, and once one moves, others will follow quickly.

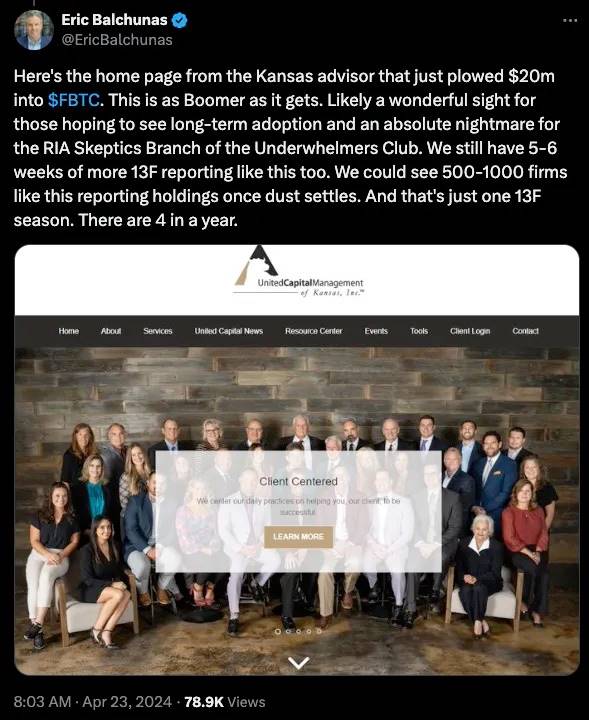

13Fs are also steadily filing in. A key insight Eric Balchunas pointed out a week or two ago: IBIT reported about 60 holders (more to come), but they account for only ~0.4% of total shares. Meaning, “mostly small fish, but lots of them.” So far, one advisor in Kansas allocated $20 million into Fidelity’s BTC ETF, representing 5% of their portfolio.

Final halving meaningfully impacts supply (currently 94% circulating)

Unprecedented new token supply entering the market

Honestly, these two clichés seem to repeat every cycle. Still, they’re worth noting—about 94% of Bitcoin’s supply is now circulating, and the latest halving may be the last materially significant one. On the flip side, the market continues to drown in new token supply—new L2s, Solana ecosystem tokens, bridges, LRTs, SocialFi, yield arbitrage plays. The list goes on, and the total FDV across these projects is both staggering and speculative. As always, most tokens will trend toward zero as insiders unlock and dump. Though plenty has already been written about that.

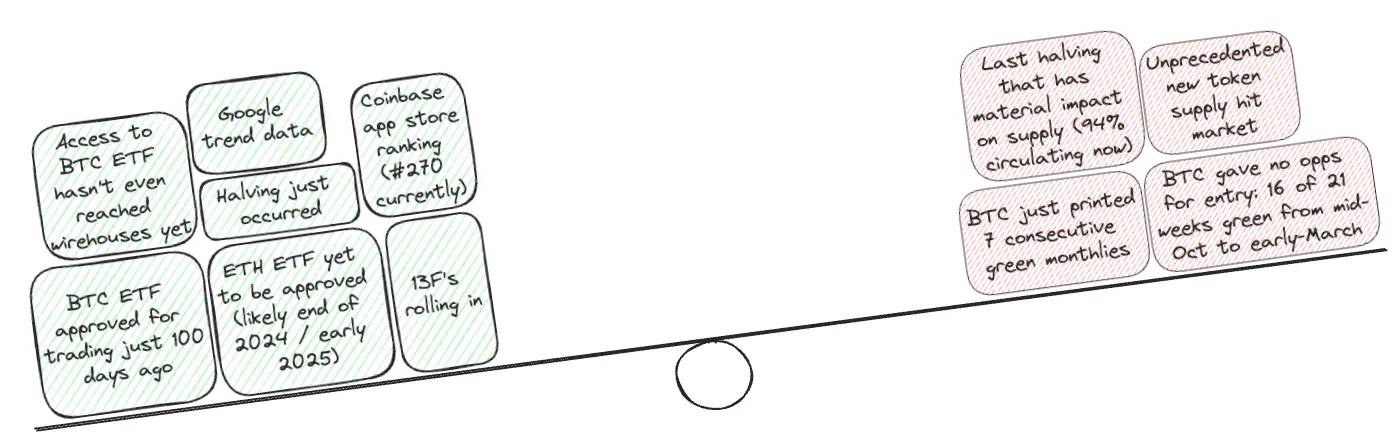

Halving just occurred

Google Trends data

Coinbase app store ranking (currently #270)

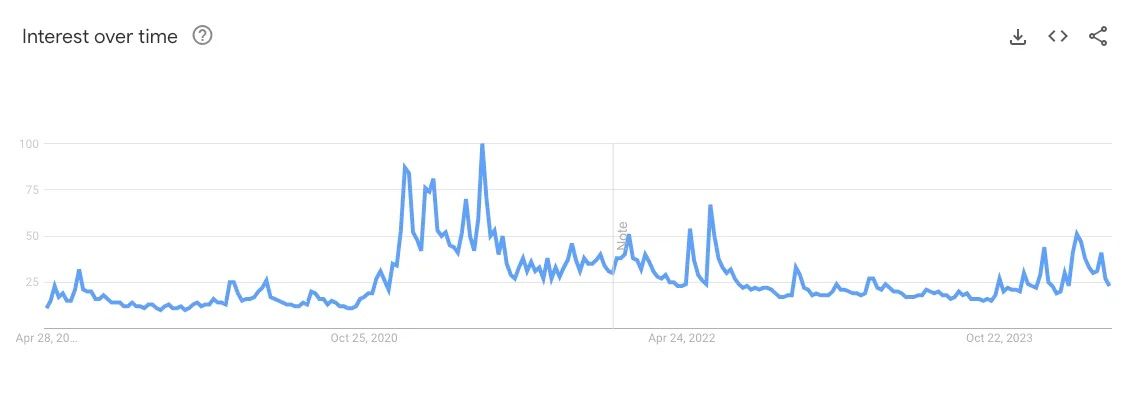

The halving did just happen—supply reduced, plain and simple. Personally, I don’t find these last two arguments compelling on their own, but they contrast sharply with popular perceptions of our cycle stage, which makes them interesting. If we examine Google Trends for widely recognized terms like BTC, ETH, SOL, and NFTs, there’s a clear pattern.

We’re still far from the peaks seen during prior genuine bull markets.

Same goes for Coinbase’s app store ranking (currently #270). I’ll touch shortly on the controversial topic of retail participation, but it’s safe to say there’s significant room for growth in native crypto app usage.

AI narrative saved the market

Unemployment can only rise

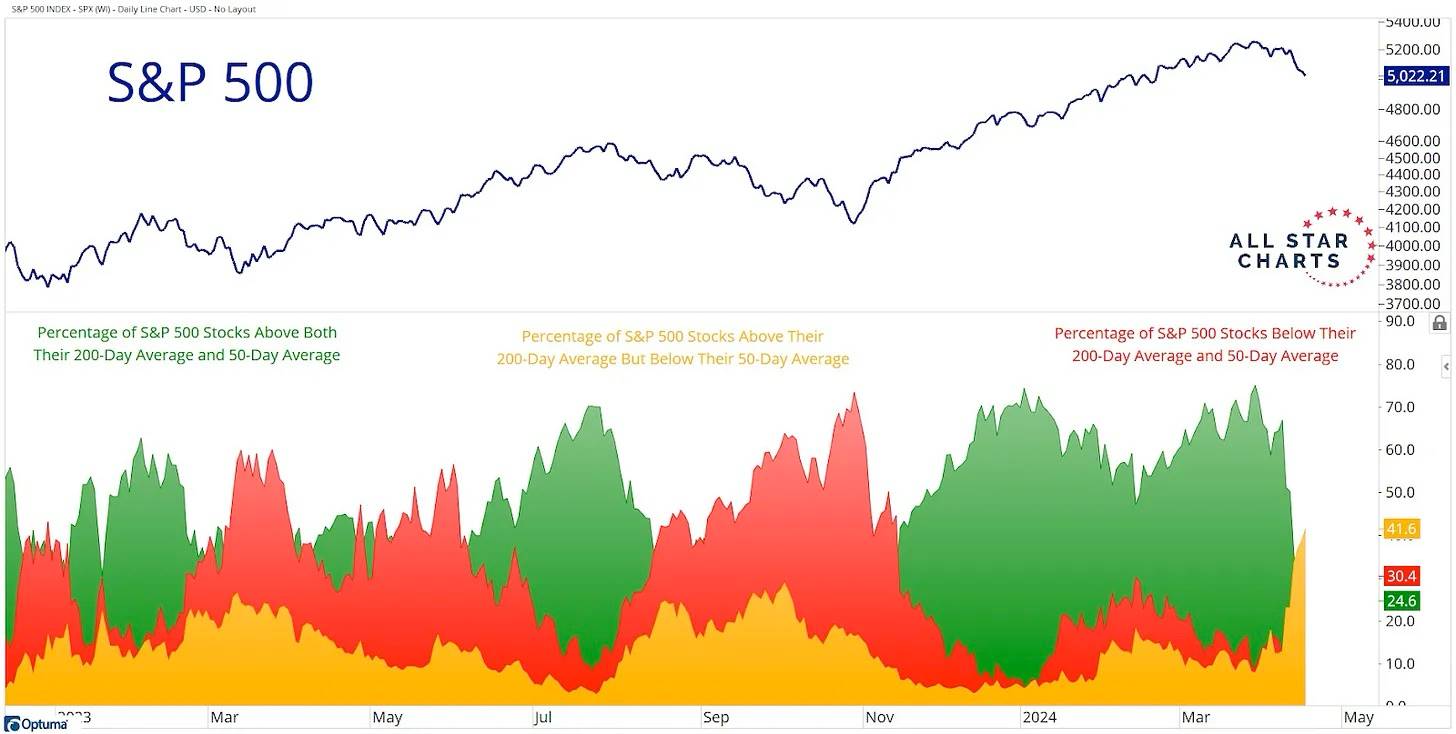

Traditional market breadth weakening

I’m willing to believe the AI narrative rescued traditional markets in Q4 2022 and Q1 2023. Had ChatGPT not launched then, traditional markets might have struggled rather than finding solace in a new innovation paradigm. But you can’t prove a counterfactual, so we must work with today’s reality. Indeed, labor markets remain incredibly strong, though unemployment can only rise from here. It’s also true that traditional markets are seeing declining breadth.

The key takeaway: the percentage of stocks above their 200-day MA but below their 50-day MA has surged (now over 40%).

I believe we haven’t yet seen the jaw-dropping surge that typically follows breakout highs. I was publicly bullish for a long time while others insisted repairing 2022’s damage would take ages. Now, those same people tell me we can’t go higher. That doesn’t mean they’re right this time—I see ample evidence suggesting we still have significant upside.

I also believe the delay in Ethereum ETF approval benefits this cycle—both in duration and price. Again, a counterfactual, but had it been approved in May, it would’ve been too close to Bitcoin’s approval. Market attention spans are short; clustering approvals and product launches causes internal competition. Who knows how impactful that would’ve been. But as the sole crypto ETF, giving BTC inflows space to breathe is crucial. This is just the appetizer. ETH ETFs will have their moment—and BTC’s performance will be their best marketing tool. A new generation of fund managers is now forced to confront Bitcoin as an asset class. They can no longer dismiss it; if they underperform peers exposed to BTC, they’ll need answers. Calling BTC a scam is no longer a tenable stance.

This is what a healthy market looks like: an undervalued asset gradually rises as more people realize they can’t buy it cheaper anymore. After digestion, there’s a consolidation phase, then continued ascent. If you remain bullish, a blow-off top is the last thing you want.

This Time Is Different

A terrifying phrase. Sure, you might whisper it to yourself or confide in a close friend about your wildest dreams. But saying it aloud in public? Brace for backlash.

We’ve all been there. Someone mutters these words, and we mock them, act smug and sarcastic, dunk on them on Twitter, call them stupid, imply it must be their first bull run—as if that matters.

Unless you’re here, you subtly, quietly believe, deep down, that eventually, it will be different.

If you say it and turn out wrong, everyone laughs, calls you a fool for thinking it would be different. No big deal. Most of those people lack independent views anyway, so why expect anything else?

But if you see enough evidence it might be different and do nothing… then who’s the real fool?

Flows are growing—but where are they going?

My biggest open question is how much of these passive flows will eventually migrate on-chain. The less exciting version of crypto is BTC as a new asset class, held modestly in institutional portfolios, while everything else remains internet subculture. Undeniably, it’s hard today to determine what portion of ETF inflows will directly or indirectly reach on-chain activity. You might think—Smac, how dumb are you? No one buys IBIT and does anything with BTC on-chain. True—for now. But that’s not the point. We all know wealth effects in crypto are real. ETFs will be an appetizer for some. The question is scale, and frankly, we may not get a clear answer soon. But we can look for directional signals.

Looking at stablecoin activity reveals compelling data. As shown below, November last year marked the first positive stablecoin supply change in about 18 months. Sustained net inflows into stablecoins suggest we’re earlier in the cycle than many believe. This is especially stark given the dramatic drawdowns seen in the last cycle.

We can also track total stablecoin supply on exchanges, which dropped over 50% from peak to trough but has now clearly begun trending upward.

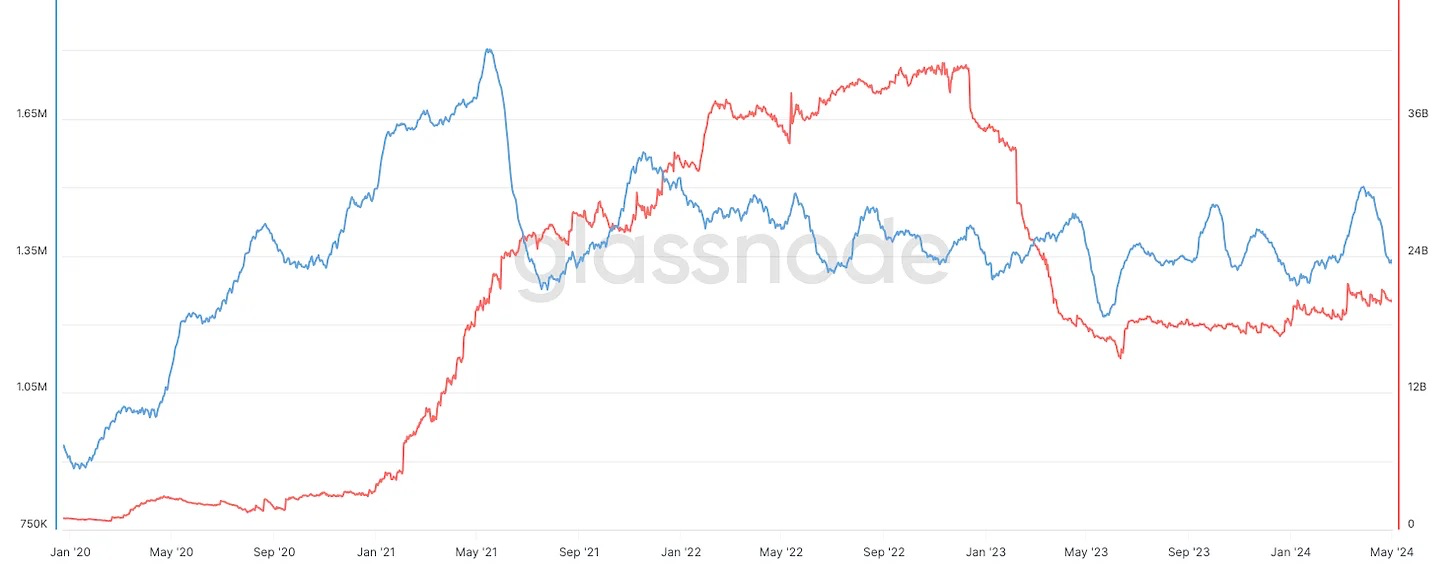

The hardest translation is whether and how this activity translates on-chain. Stay open-minded, but below is total active addresses (blue line) vs. stablecoins on exchanges. Depending on your interpretation, you might draw various conclusions, but my read is:

During the last bull run, we saw a massive spike in new active addresses, followed by a sharp drop as people exited, then relative stability since Q3 2021. We haven’t seen signs of a new wave—suggesting retail participation hasn’t returned.

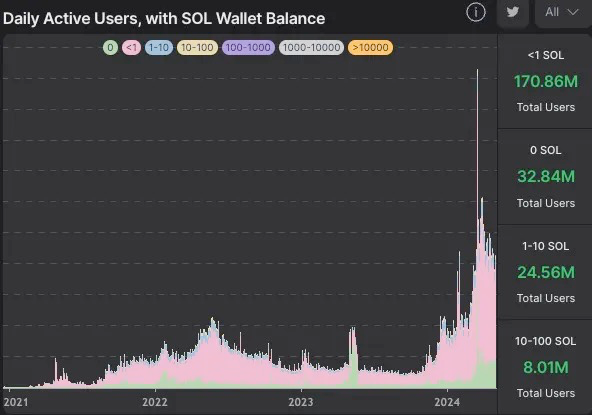

It’s also worth acknowledging that retail activity may be happening via Solana. Clearly, activity there has increased significantly over the past 6–9 months, and I personally expect this to continue.

Ignore SOL tokens with DAU of 0 or less than 1 (Source: hellomoon)

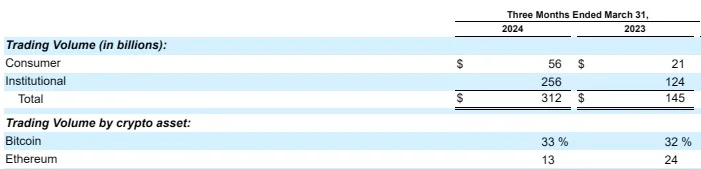

What about more off-chain data? From Coinbase’s recent 10-Q, we actually saw monthly transacting users (MTUs) decline from 8.4M to 8.0M. Yet trading volume more than doubled on both retail and institutional sides. Interestingly, while BTC’s share of trading volume remained flat, ETH’s share shrank significantly—possibly signaling rising demand for broader crypto assets (i.e., altcoins), which is very healthy long-term, as wider distribution across crypto assets is the ideal end state. Haters and losers will say everything in crypto is empty, that people are just arriving at the final stage of super-gambling. I say it means more interesting early-stage projects and protocols worth exploring.

Q1 2024

Q1 2024

How does this compare to what we’ve seen from Coinbase users in recent years? First, we’re still over 40% below the 2021 MTU peak (11.4M) and below late-2022 levels. Despite all the talk about memes and retail transformation, I simply don’t see a credible argument that this is happening at scale. Is it occurring in pockets among highly crypto-native users? Sure. But again, this shows people trapped in the crypto bubble, missing the bigger picture. If you live on Twitter consuming crypto content and treat it as gospel, you’ll do poorly.

End of 2021

End of 2023

My final point here concerns altcoins beyond BTC and ETH. As early crypto investors, we firmly believe this space will grow beyond just the majors. The simplest way to measure this activity is TOTAL3, tracking the top 150 altcoins outside BTC and ETH. I find it instructive to observe the previous high-to-low cycles. Comparing the 2017 cycle to the recent one, it’s clear the relative upside is compressing (though still astronomical)—something we’d expect as the space expands. The base is larger, so parabolic moves intuitively become harder. But even allowing for further compression, I don’t think enough people realize how much room remains. TOTAL3 is only $640 billion—sounds big, but it’s negligible in the macro financial scheme. If we believe this space could reach $10 trillion in the next 24 months, with BTC taking 40–50%, massive value creation remains ahead.

2017–18

2020–21

2024–25?

Personally, I don’t think this will be memecoin-dominated—a view some strongly disagree with. Memecoins serve a purpose and will remain important in crypto (even traditional finance), but I’m also optimistic about a new wave of mature founders. They’re deeply thinking about solving real problems and focusing on decade-long outcomes. We’re eager to work with founders like this.

I believe we’re still in the early stages of this cycle. I’d guess we’re about one-third through. Despite widespread belief that it’s all about memecoins, other meaningful developments are underway. SocialFi is seeing renewed innovation, ERC-404 remains underexplored, DePIN adoption is growing beyond crypto circles, RWAs are slowly moving on-chain, and we’re seeing more attempts to explore how distributed systems impact the “real” world. We continuously add new theses to our public database and are always excited to speak with builders working at strange, novel, and ambitious intersections.

Despite the industry’s many flaws, I remain very optimistic about its future.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News