Huobi Research: With the completion of the Cancun upgrade, will LRT (Liquid Restaking) catalyze the Ethereum ecosystem?

TechFlow Selected TechFlow Selected

Huobi Research: With the completion of the Cancun upgrade, will LRT (Liquid Restaking) catalyze the Ethereum ecosystem?

Overall, the LRT sector is a rapidly growing niche market.

With the completion of the Cancun upgrade, Ethereum and its related ecosystem tokens have performed strongly recently. Meanwhile, modular concept projects and Ethereum Layer 2 projects are successively launching mainnets, further driving market optimism toward the Ethereum ecosystem. The liquid restaking narrative has also begun attracting capital attention due to the explosive popularity of EigenLayer.

But is the progression from ETH → LST → LRT an actual catalyst for the Ethereum ecosystem, or merely a "matryoshka doll" scheme as many claim?

This research report provides a detailed analysis of the current state, opportunities, and future outlook of the LRT sector. Currently, many LRT protocols have not issued tokens and suffer from severe homogenization. However, KelpDAO, Puffer Finance, and Ion Protocol stand out with clearly differentiated development paths compared to other LRT protocols. The LRT sector remains a rapidly growing niche market. Huobi Research predicts that only a few leading projects will ultimately emerge dominant.

This report was written by the Research team under HTX Ventures. HTX Ventures is the global investment arm of HTX, integrating investment, incubation, and research to identify the world’s most outstanding and promising teams.

Is LRT Just a Matryoshka Doll? Exploring the Evolutionary Path of LRT

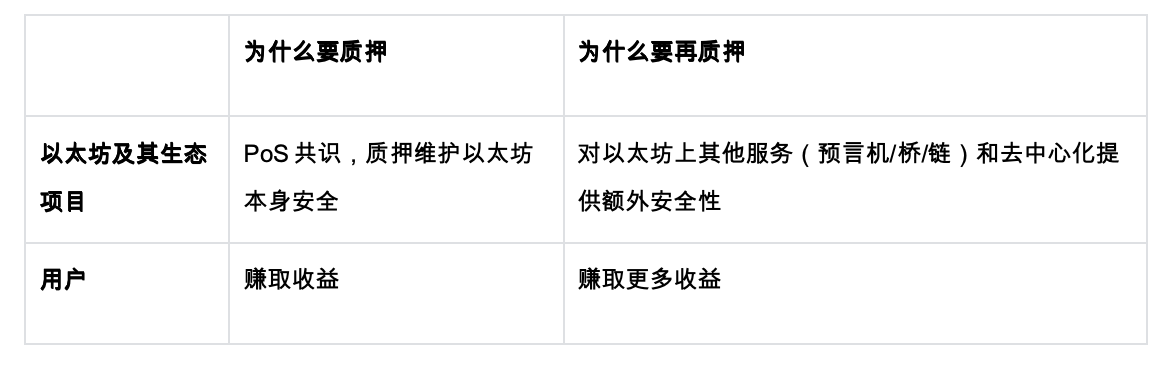

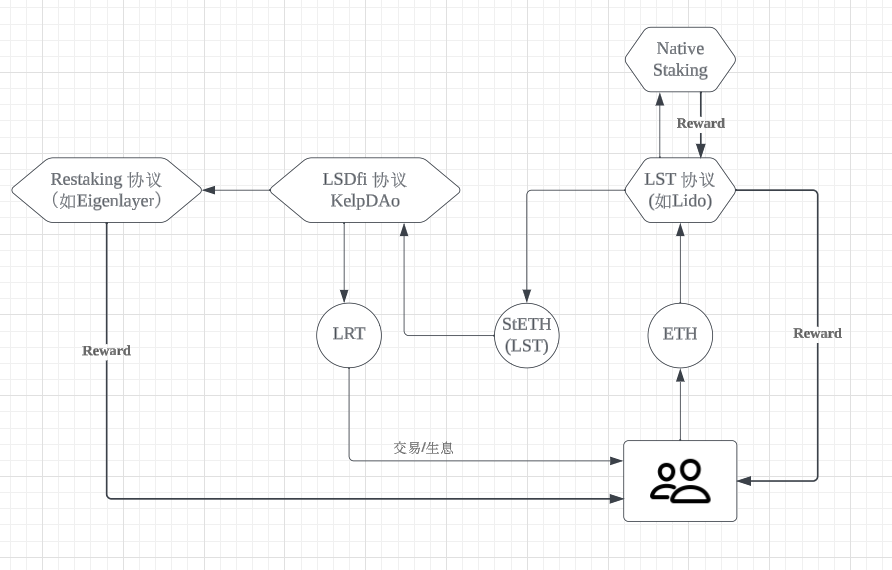

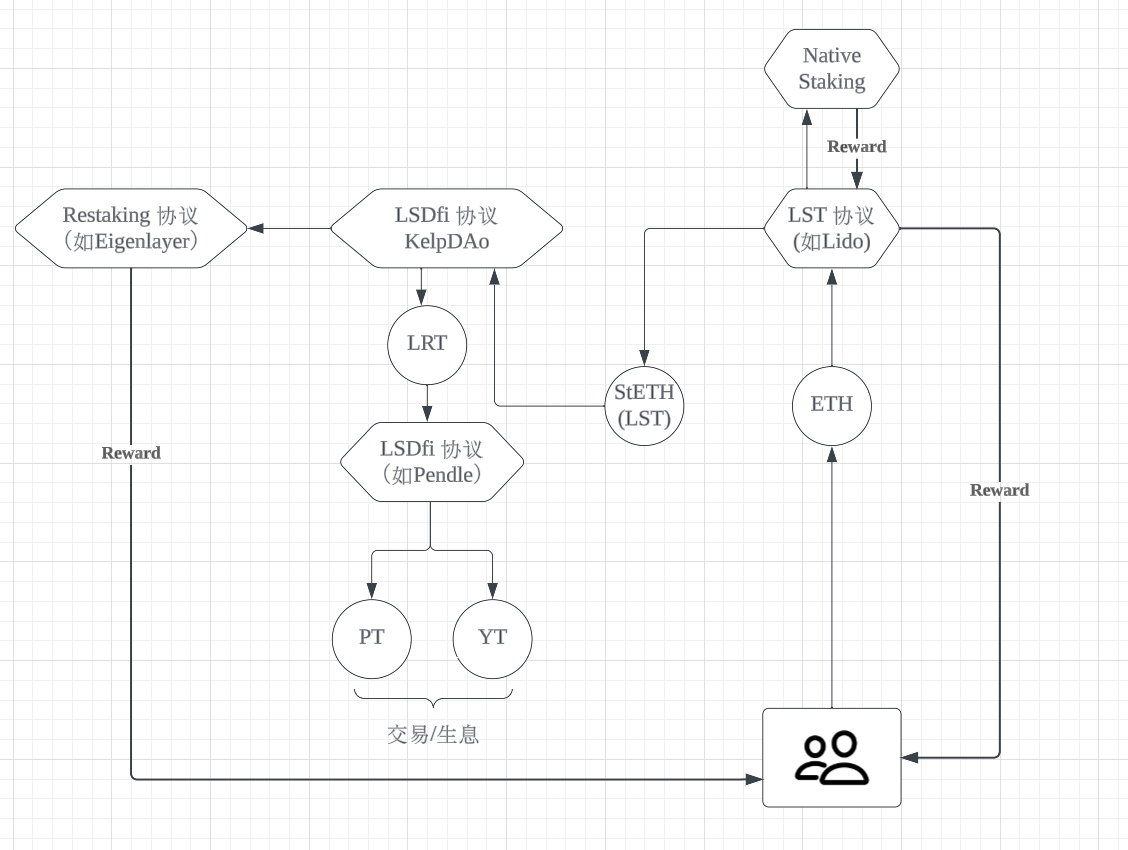

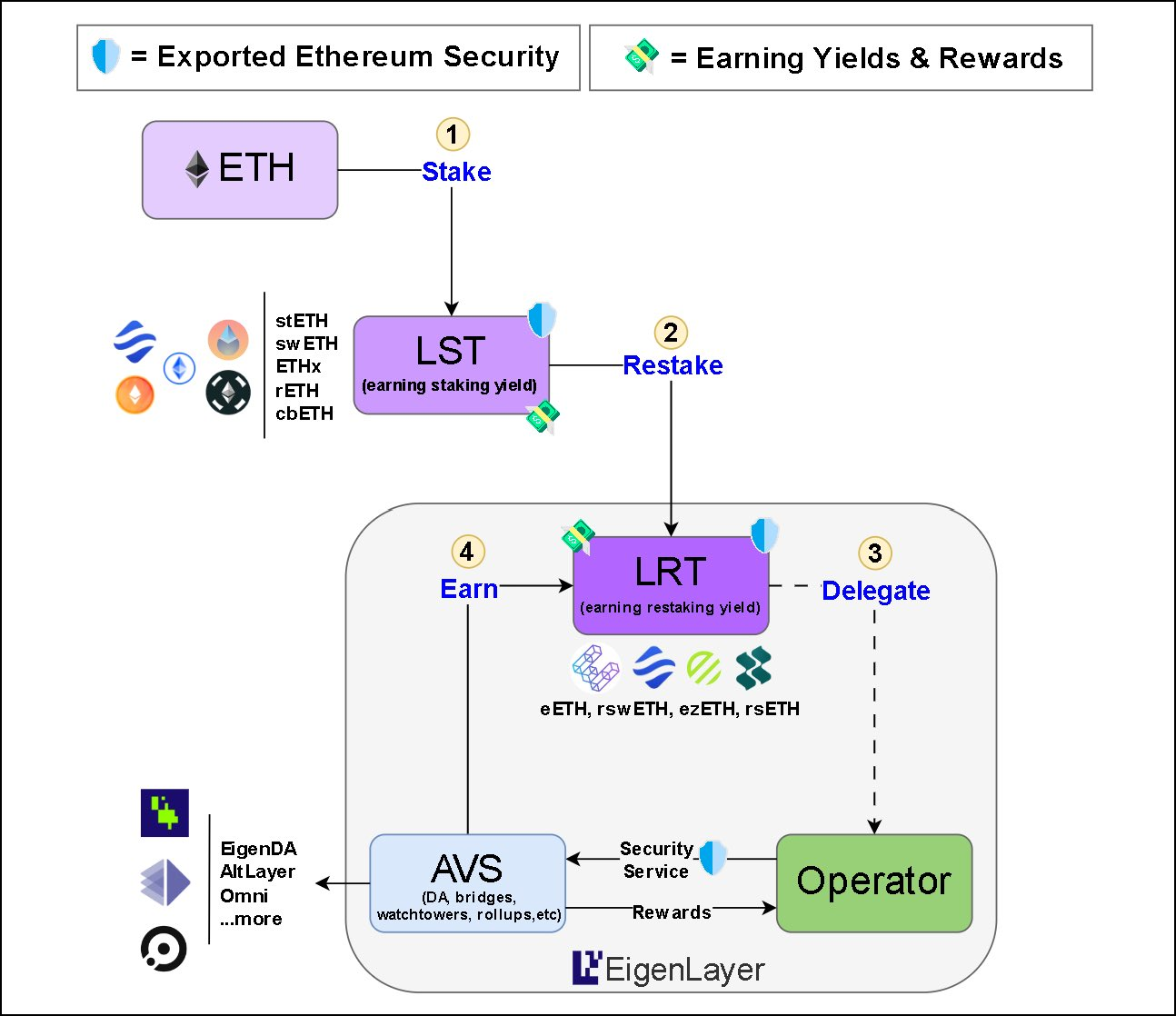

The concept of "restaking" was first introduced by EigenLayer in June 2023. It allows users to restake already-staked ETH or liquid staked tokens (LSTs), providing additional security for various decentralized services on Ethereum while earning extra rewards. Based on EigenLayer’s restaking service, liquidity restaking token (LRT) projects have emerged.

An LRT (Liquidity Restaking Token) refers to a "restaking receipt" obtained after depositing an LST into a restaking protocol.

So,

1. How exactly is this LRT "restaking receipt" created?

2. Is the path from ETH → LST → LRT truly just a "matryoshka doll" scheme, as many claim?

To answer these questions, we need to trace the evolutionary path of LRT.

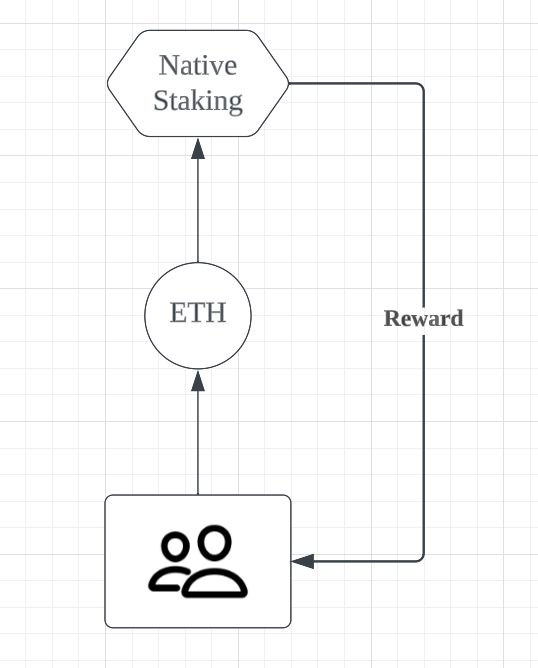

Phase 1: Native Ethereum Staking

After Ethereum's transition to PoS, validators—formerly miners—secure the network by storing data, processing transactions, and adding new blocks, earning rewards in return. Becoming a validator requires staking at least 32 ETH and running a dedicated computer connected to the internet year-round.

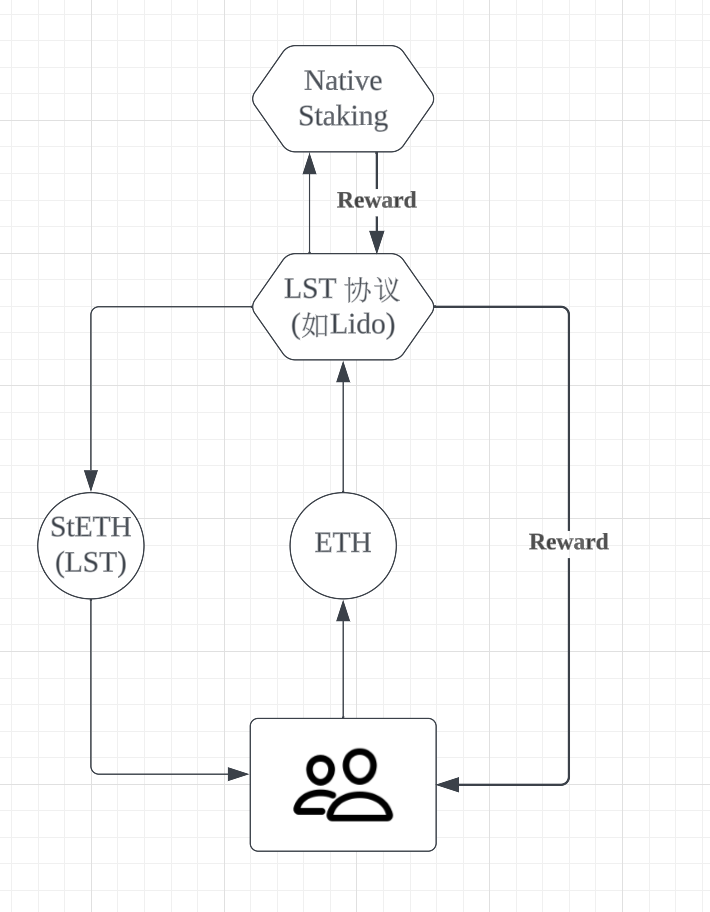

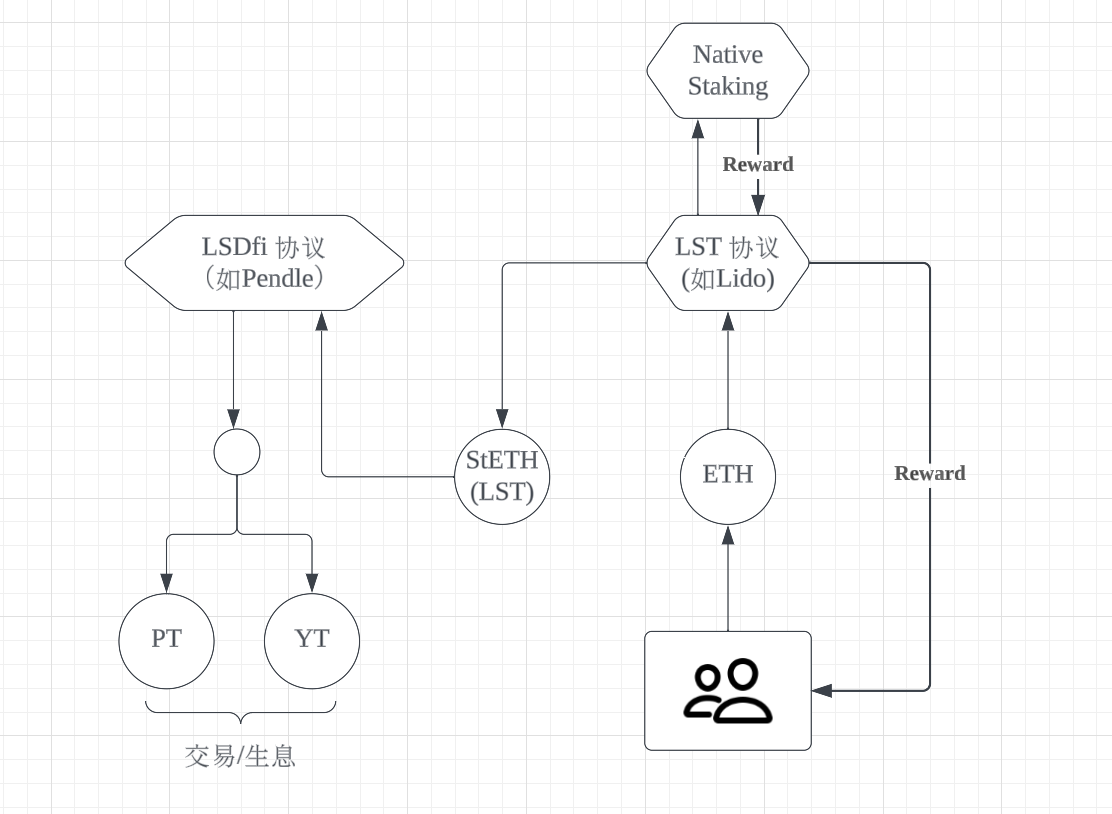

Phase 2: Emergence of LST Protocols

Due to the 32 ETH minimum requirement and long withdrawal delays, staking platforms emerged to solve two key problems:

1. Lowering barriers: For example, Lido allows staking any amount of ETH without technical expertise.

2. Unlocking liquidity: For instance, staking ETH on Lido yields stETH, which can be used in DeFi or nearly equivalently swapped for ETH.

In simple terms, it's like a “group purchase.”

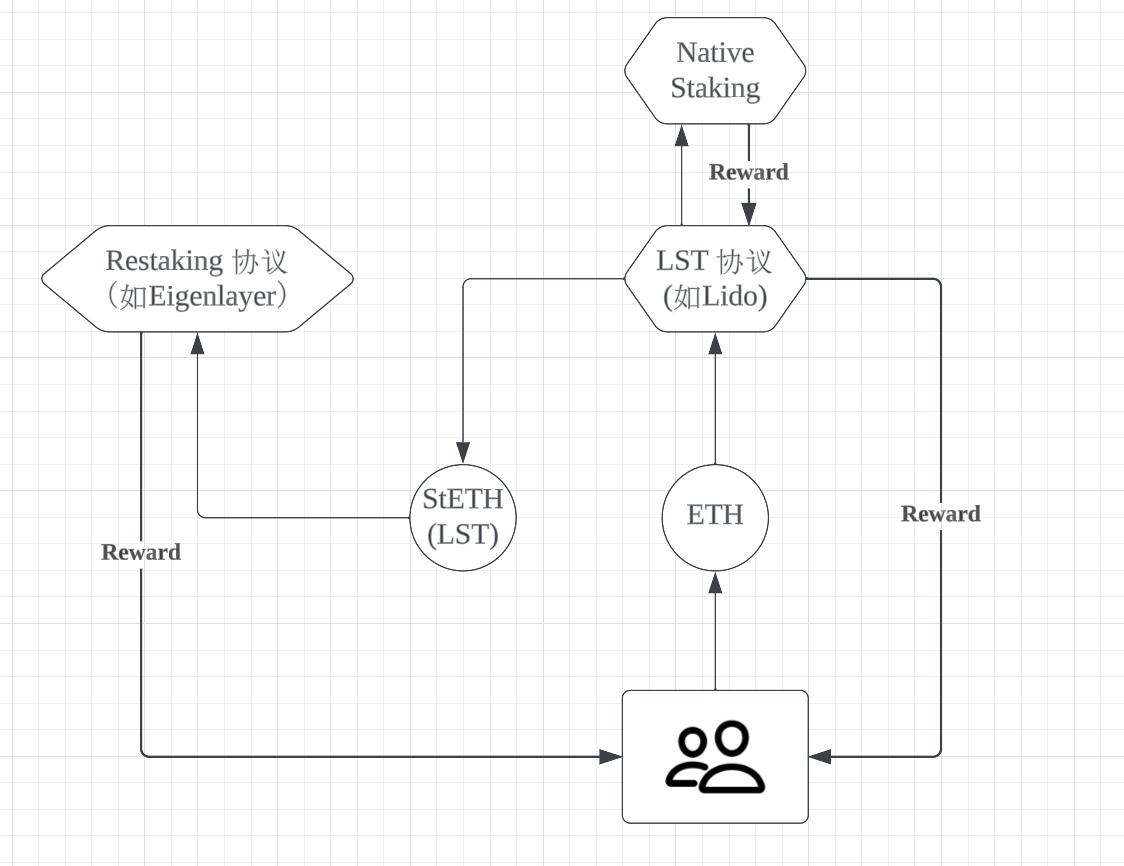

Phase 3: Emergence of Restaking Protocols

As the Ethereum ecosystem evolved, users realized that liquid staked tokens (LSTs) could be restaked across other networks and blockchains to earn additional yield while enhancing the security and decentralization of new networks.

EigenLayer is the most representative project here. Its restaking logic revolves around two core ideas: shared security within the Ethereum ecosystem and higher user returns.

● Restaking enables shared security between sidechains and middleware layers (e.g., DA layers, bridges, oracles), thereby strengthening Ethereum’s own security. Security sharing allows a blockchain to leverage another chain’s validator set value to enhance its own security.

● From the user perspective, it’s about seeking yield through staking—and even more yield through restaking.

Phase 4: Birth of LRT

After restaking protocols emerged, users found they could earn yield by restaking LSTs—but once deposited, their LSTs became illiquid. This gap presented an opportunity: certain protocols began helping users deposit LSTs into restaking protocols to earn yield while issuing a "restaking receipt" (i.e., LRT). Users could then use this LRT for further financial operations such as collateralization and borrowing, solving the liquidity lock-up issue. This "restaking receipt" is the LRT.

Phase 5: Pendle Fuels the LRT Explosion

Once users obtain LRTs, where can they go and what financial activities can they perform? Pendle offers an elegant solution.

Pendle is a decentralized interest rate trading market that enables trading of PT (Principal Token) and YT (Yield Token).

With the rise of yield-bearing stablecoins and, more recently, liquidity restaking tokens (LRTs), the variety of yield-bearing tokens has expanded significantly. Pendle has iterated continuously to support trading of these crypto yields. Pendle’s LRT markets have been particularly successful, essentially allowing users to pre-sell or position for long-term airdrop opportunities (including EigenLayer). These markets have quickly become Pendle’s largest and most dominant segments:

● Through custom integration with LRTs, Pendle allows Principal Tokens to lock in base ETH yield, EigenLayer airdrops, and any airdrops tied to the issuing restaking protocol. This creates annualized yields exceeding 30% for PT buyers.

● On the other hand, Yield Tokens enable a form of “leveraged point farming.” Via Pendle’s swap function, one can exchange 1 eETH for 9.6 YT eETH, accumulating EigenLayer and Ether.fi points as if holding 9.6 eETH.

● In fact, for eETH, YT buyers receive double points from Ether.fi—a true case of “leveraged airdrop farming.”

By leveraging Pendle, users can lock in ETH-denominated airdrop yields (based on market expectations around EigenLayer and LRT airdrops) and engage in leveraged liquidity mining. Given speculation around potential AVS airdrops to LRT holders this year, Pendle is likely to continue dominating this market segment. In this sense, $PENDLE offers strong exposure to the success of the LRT and EigenLayer verticals.

Summary:

The above explains how LRTs came into existence. So,

Is ETH → LST → LRT really just a matryoshka doll scheme, as many claim?

The answer depends on context.

If within a single DeFi ecosystem, an LST is staked to generate a restaking receipt, which is then itself staked—issuing a governance token in the name of locking liquidity, fueling secondary market speculation to prop up restaking expectations—then yes, it is a matryoshka doll. This model uses inflows from lower tiers to subsidize upper-tier assets, drawing on market expectations for a token without generating real underlying value.

Now consider the classic restaking model centered on EigenLayer + Pendle:

Through EigenLayer,

● Users restake LSDs into EigenLayer.

● The restaked assets are provided to AVS (Actively Validated Services) for protection.

● AVS provides validation services for appchains.

● Appchains pay service fees, which are split into three parts: staking rewards, service revenue, and protocol income distributed to stakers, AVS operators, and EigenLayer respectively.

Through Pendle,

● Users can lock in ETH-denominated airdrop yields (based on market expectations for EigenLayer and LRT airdrops)

● Leverage liquidity mining

● LRTs as yield-generating assets gain excellent utility

At its core, this model enables sharing of Ethereum’s security. Projects using this shared security must pay fees—creating positive cash flow into the ecosystem. This is absolutely not a matryoshka doll, but rather a sound economic model.

Simply put, the key drivers behind the current LRT narrative are two critical factors:

1. The yield-generating capability of LRT’s underlying assets

2. Use cases for LRT

First, the yield-generation ability of LRT’s underlying assets comes from EigenLayer—including EigenLayer airdrops and utility service revenues (detailed further below)

Second, Pendle provides an excellent example of LRT application scenarios

Next, we’ll focus on EigenLayer—the core restaking project—and provide a comprehensive review of other LRT projects

LRT Ecosystem Overview (In-Depth Focus)

EigenLayer – Restaking Middleware

EigenLayer Overview

EigenLayer is a re-staking pool on Ethereum, consisting of a suite of smart contract middleware enabling consensus-layer ETH stakers to opt into validating new software modules built atop the Ethereum ecosystem.

EigenLayer provides an economic security platform allowing any stakeholder to contribute to any PoS network. By reducing cost and complexity, EigenLayer effectively paves the way for L2s to access expressive innovation from the Cosmos stack. Protocols using EigenLayer are essentially “renting” economic security from existing Ethereum stakers, reusing ETH’s security across multiple applications.

In summary: EigenLayer uses a set of smart contracts to allow restakers to validate different networks and services, saving costs for third-party protocols while letting them benefit from Ethereum’s security, and offering restakers multiple yields and flexibility.

Product Mechanism

For middleware projects, EigenLayer helps achieve rapid cold starts—even if they later launch their own tokens, they can eventually transition to a native-token-driven model. EigenLayer acts like a security-as-a-service provider. For DeFi, developers can build various derivatives on top of EigenLayer.

● EigenLayer’s product logic within the broader LST/LRT landscape

● User flow via EigenLayer

Understanding EigenLayer AVS

Another key concept in EigenLayer is AVS (Actively Validated Services).

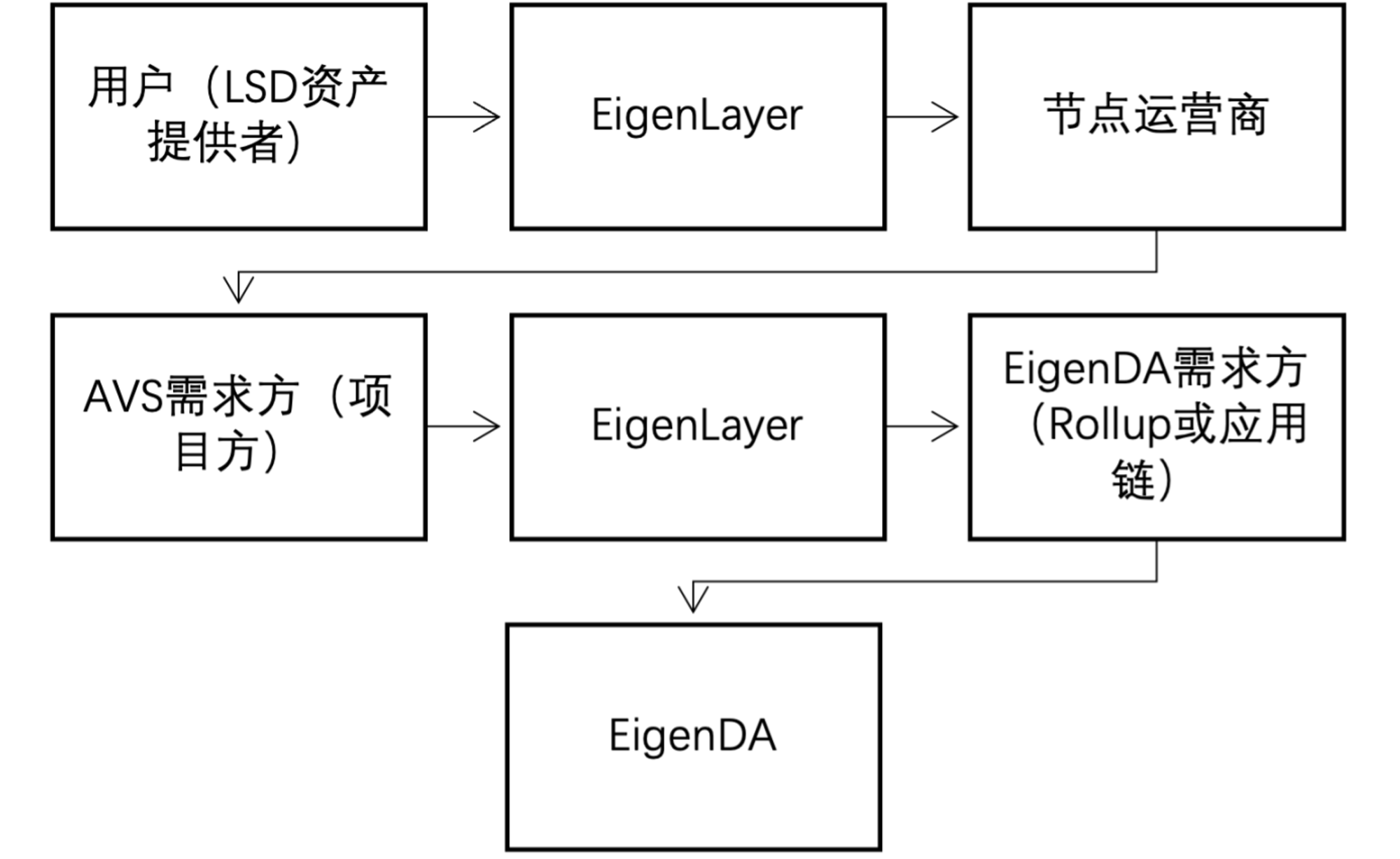

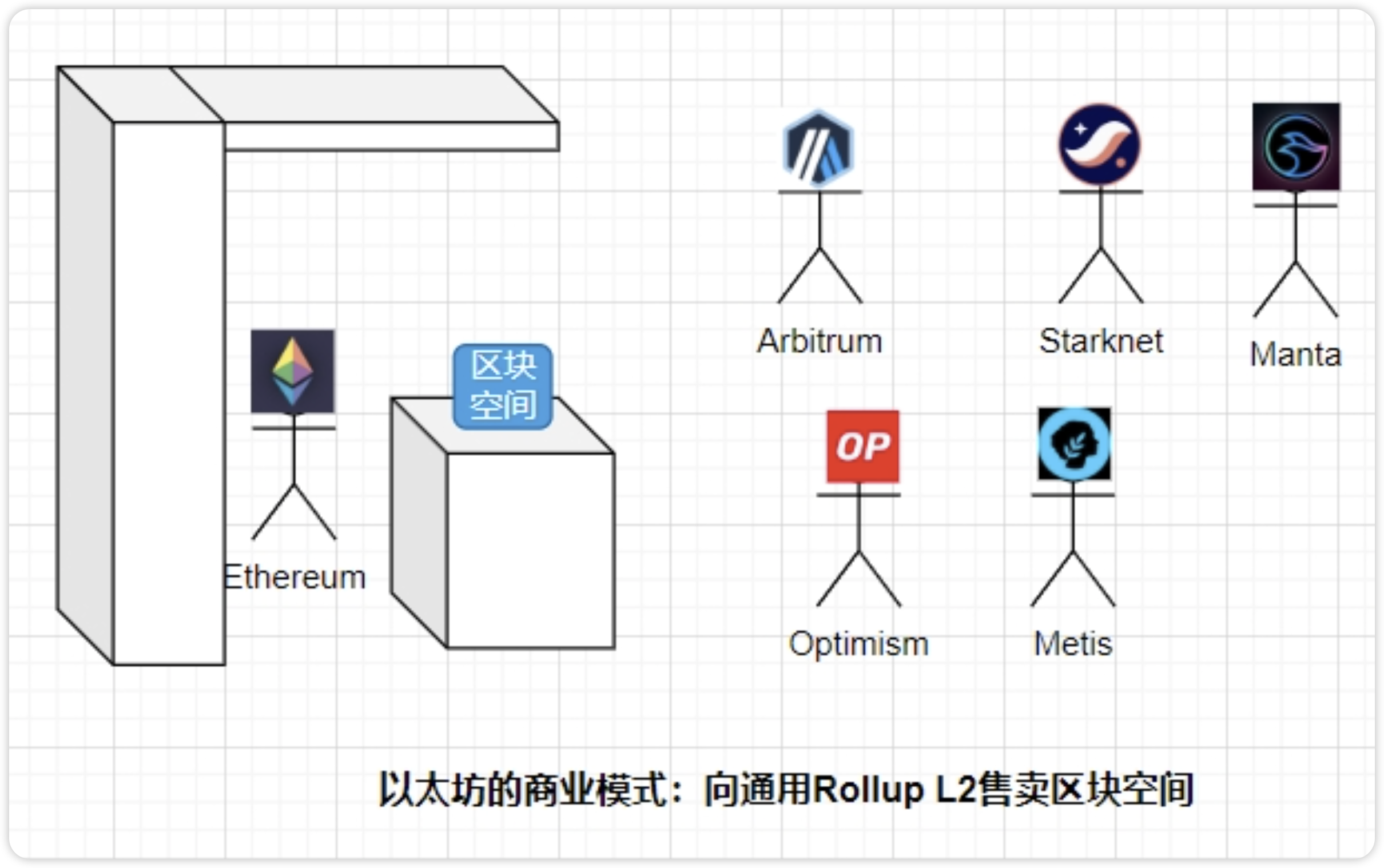

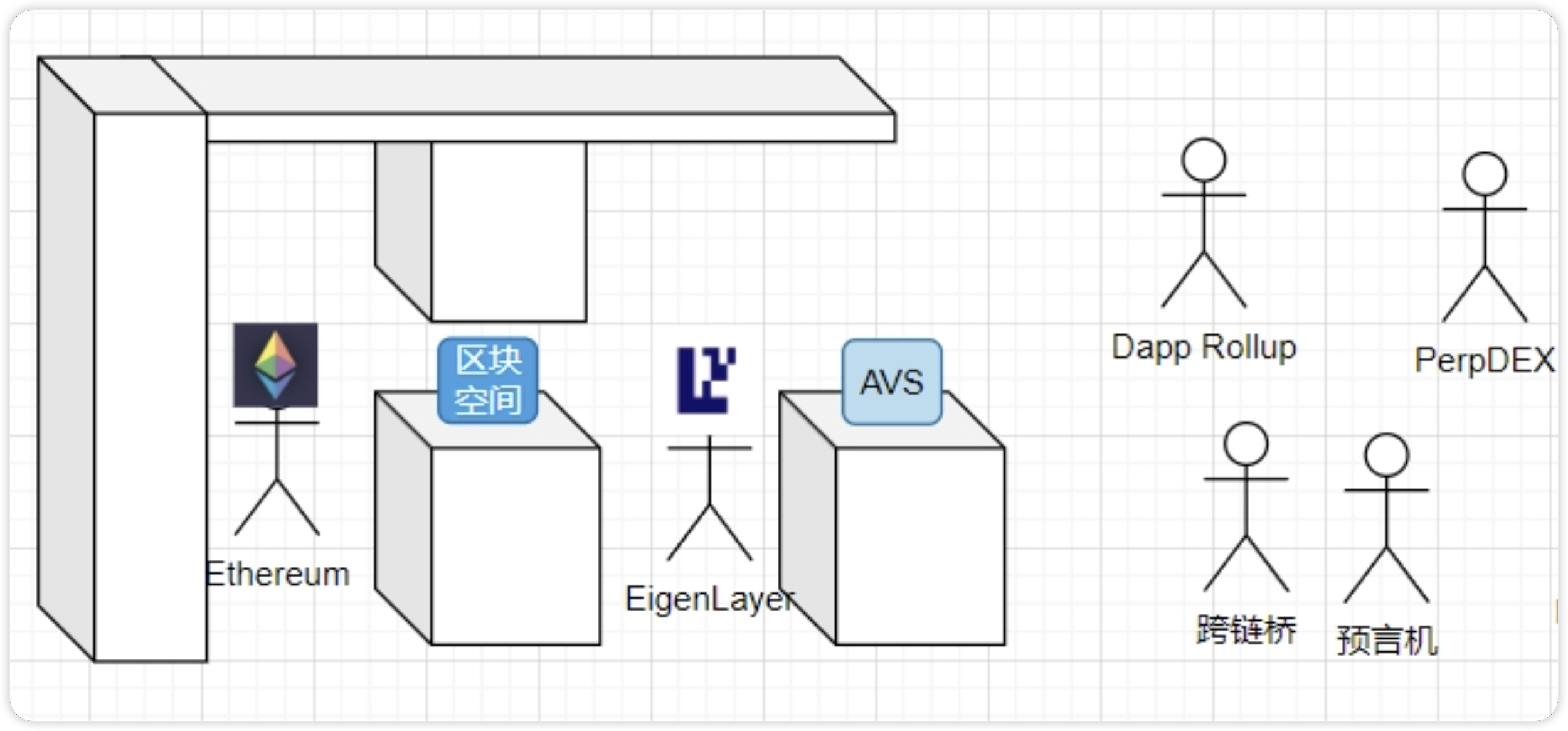

Restaking is easy to understand; AVS is trickier. To grasp EigenLayer’s AVS, we must first understand Ethereum’s business model. From a business perspective, Ethereum currently sells blockspace to general-purpose Rollup L2s.

Image source: Twitter @0xNing0x

General Rollup L2s pay gas fees to package their state data and transactions into smart contracts deployed on Ethereum, storing them as calldata. Ethereum’s consensus layer then orders and includes this data in blocks. This process essentially involves Ethereum actively verifying the consistency of Rollup L2 state data.

EigenLayer’s AVS abstracts this specific process into a new concept—AVS.

Now consider EigenLayer’s business model: it packages Ethereum’s PoS consensus security into a “budget version” (lower specs), weakening consensus security slightly but making it much cheaper.

Because it’s a budget AVS, its target market isn’t high-security-demand general Rollup L2s, but rather dApp Rollups, oracle networks, cross-chain bridges, MPC multisig networks, trusted execution environments—projects with lower consensus security needs. Isn’t that product-market fit (PMF)?

Image source: Twitter @0xNing0x

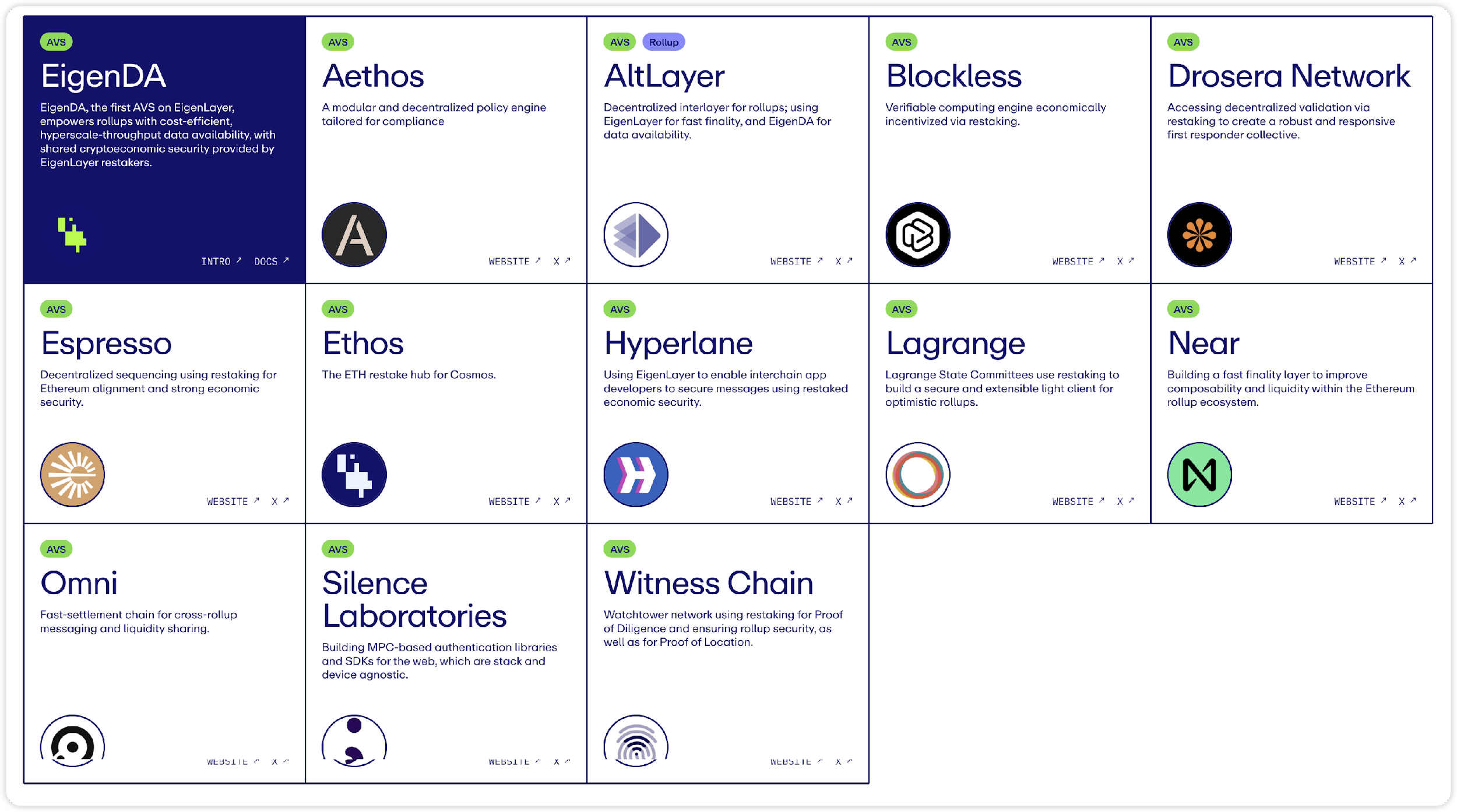

AVS (Actively Validated Service) Projects

Currently, around 13 AVS projects are integrated with EigenLayer, with more joining via EigenLayer’s developer documentation. These projects are highly aligned with the RaaS concept, primarily serving rollups’ needs for security, scalability, interoperability, and decentralization—with some extending into the Cosmos ecosystem.

Well-known examples include EigenDA, AltLayer, and Near. Below we outline key characteristics of selected AVS projects:

● Ethos: Ethos primarily bridges Ethereum’s economic security and liquidity to Cosmos. While Cosmos consumer chains typically rely on native staking of their own tokens for security, Ethos links Ethereum’s economic security and liquidity to Cosmos. Inspired by Mesh Security (which allows using one chain’s staked tokens on another), Ethos enhances economic security without requiring additional nodes. A key benefit: ETHOS may receive token airdrops (and revenue) from partner chains. Simultaneously, the ETHOS token itself will be airdropped to ETH restakers on EigenLayer.

● AltLayer: A new project launched in collaboration with EigenLayer, introducing Restaked Rollups featuring three AVS components: 1) fast finality, 2) decentralized sequencing, and 3) decentralized validation. ALT’s tokenomics are clever—ALT must be staked alongside restaked ETH to secure these three AVS components.

● Espresso: Focused on decentralized L2 sequencers. AltLayer actually integrates Espresso, allowing developers deploying on the AltLayer stack to choose either AltLayer’s decentralized validation solution or the Espresso Sequencer.

● Omni: Aims to unify all Ethereum Rollups. Omni introduces a “unified global state layer” secured via EigenLayer restaking, integrating cross-domain management of applications.

● Hyperlane: Aims to connect all Layer 1s and Layer 2s. With Hyperlane, developers can build interchain applications. Its permissionless interoperability allows Rollups to self-connect to Hyperlane without cumbersome governance approvals.

● Blockless: Adopts a network-neutral application (nnApp) model, allowing users to run a node while using an app, contributing resources to the network. Blockless will provide infrastructure for EigenLayer-based apps to minimize slashing risks.

Other Notable AVS Projects:

● Lagrange: A competitor to LayerZero, Omni, and Hyperlane, building cross-chain infrastructure capable of generating universal state proofs across major blockchains;

● Drosera: An “incident response protocol” designed to contain vulnerabilities—when hacks occur, Drosera’s Trap detects and mitigates damage;

● Witness Chain: Uses restaking for Proof of Diligence to secure Rollups, and Proof of Location to establish physical node decentralization.

EigenLayer Product Summary

EigenLayer’s key product features can be summarized as follows:

● EigenLayer acts as a “super connector,” linking staking, infrastructure middleware, and DeFi.

● EigenLayer plays a bridging role in Ethereum restaking, extending Ethereum’s cryptoeconomic security. Its market demand and supply fundamentals are solid.

● EigenDA serves as an early implementation of Danksharding, part of Ethereum’s rollup-centric roadmap. In short, it’s a “lite version of sharded storage.”

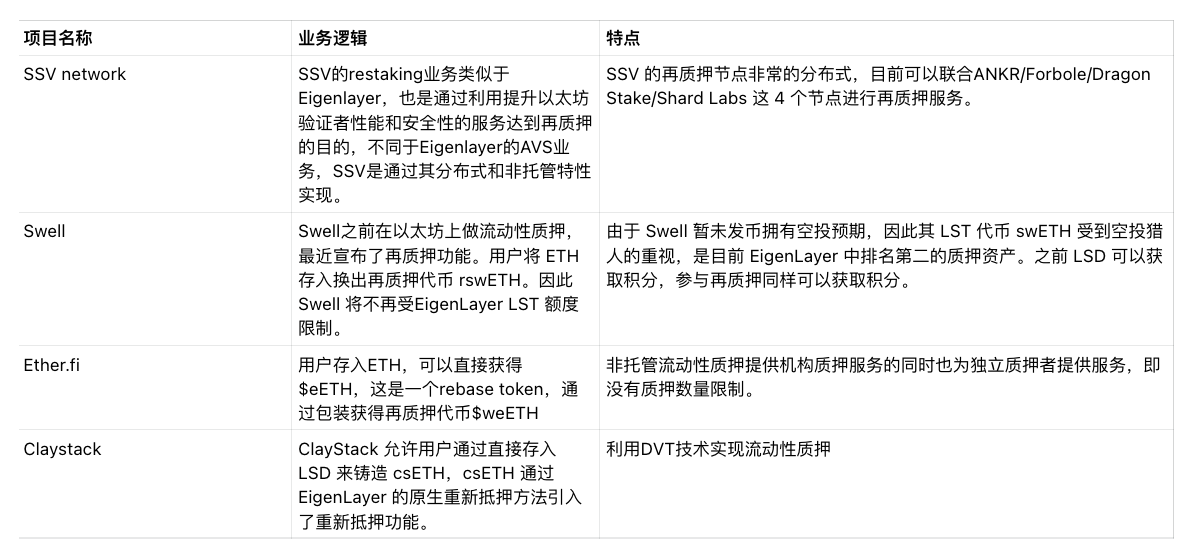

EigenLayer Ecosystem Projects

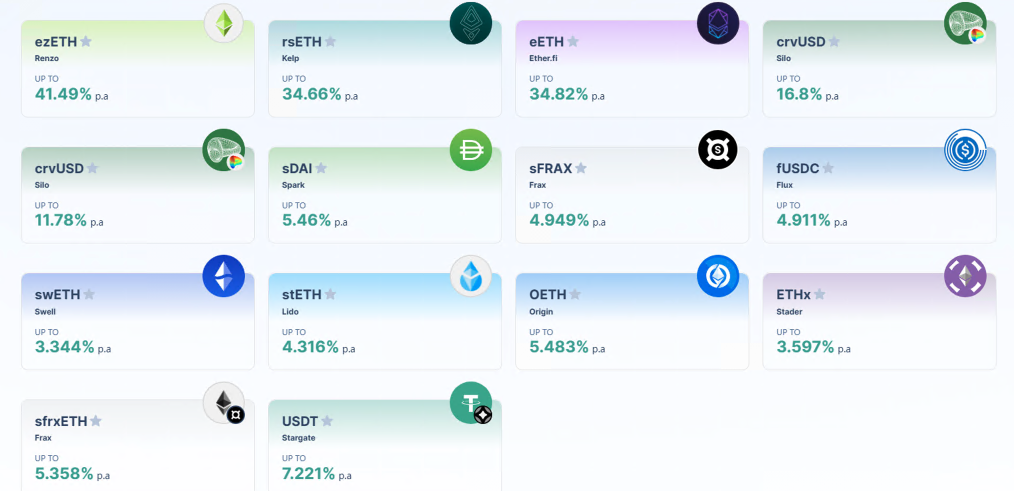

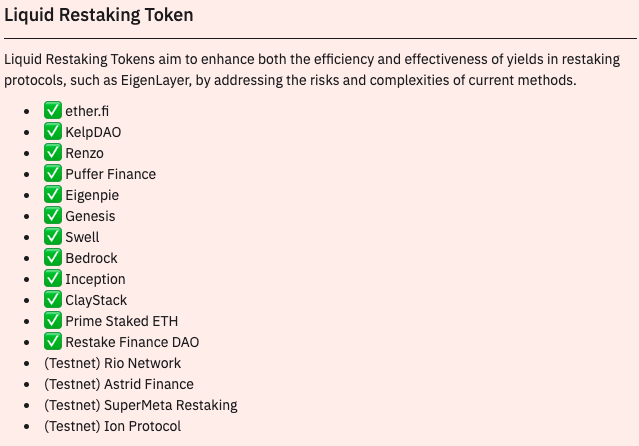

Overview of Ethereum LRT Projects

There are currently about 15 LRT protocols on Ethereum, with 9 live and 6 still in testnet. Most LRT protocols rely on EigenLayer for restaking yields and fall into three main categories:

● Liquid-LSD Restaking: Aggregates users’ LSTs and deposits them into external restaking protocols like EigenLayer, issuing a liquidity restaking token (LRT) as a receipt (examples: KelpDAO, Restake Finance, Renzo). These protocols are highly homogenized with limited innovation.

● Liquid Native Restaking: Native liquid restaking refers to projects like ether.fi or Puffer Finance that offer small-ETH-node services, supplying ETH from within nodes to EigenLayer for restaking.

● Protocols that optimize on top of EigenLayer, offering both security/validation services and LRT functionality (e.g., SSV). Their growth depends on differentiating from EigenLayer and finding competitive advantages to attract node operators.

Most LRT protocols innovate along three dimensions:

1. Offering stronger security than EigenLayer;

2. Addressing EigenLayer’s allocation challenges: As AVS count grows, restakers must actively manage operator allocation strategies—an increasingly complex task. LRT protocols offer optimized allocation solutions.

3. Bypassing deposit limits: EigenLayer caps LST deposits and requires 32 ETH plus operation of an EigenPod-integrated node for native ETH deposits—barriers most users cannot meet. Some LRT protocols remove these restrictions.

Specific projects and details follow:

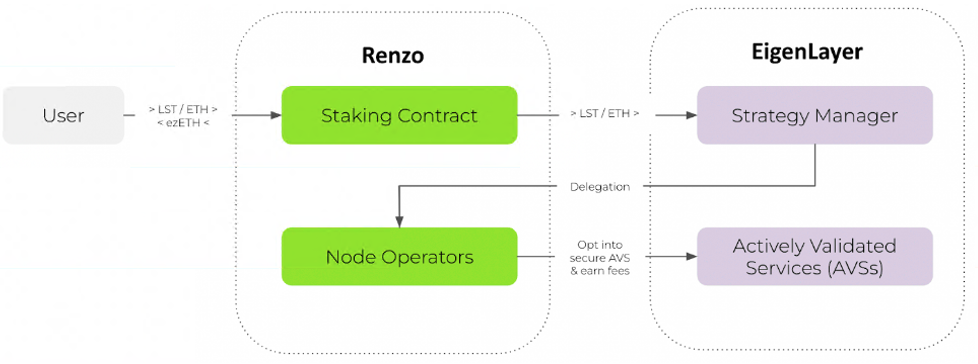

Renzo

Renzo optimizes on EigenLayer by abstracting away the complexity of restaking for end users. Restakers no longer need to manually select or manage operators and reward strategies. Renzo helps users build portfolios optimized for higher-yield AVS allocations. Additionally, Renzo imposes no deposit caps, a key factor behind its explosive TVL growth.

Funding: Announced a $3.2M seed round in January, led by Maven11, with participation from SevenX Ventures, IOSG Ventures, OKX Ventures, and others.

Business Logic:

● Users deposit ETH or LSTs into Renzo and receive equivalent $ezETH;

● Renzo stakes the LSTs into AVS nodes on EigenLayer, adjusting weightings to maximize yield.

Status: No token issued yet. $ezETH is its LRT token, priced above ETH due to accrued restaking yield. 217,817 ezETH minted, TVL $777.7M. Fees are adjusted based on restaking yield. Community: 51.7K Twitter followers.

KelpDAO

KelpDAO is an LRT project backed by Stader Labs, with a business model similar to Renzo. A key difference lies in rsETH withdrawal: Renzo requires over 7 days, whereas KelpDAO offers an AMM liquidity pool enabling instant redemption of $rsETH.

Business Logic:

● Deposit stETH or other LSTs into KelpDAO to receive rsETH. The Node Delegator contract stakes LSTs into EigenLayer’s Strategy Manager contract.

● Integrated with EigenLayer, users earn EigenLayer points while unlocking liquidity via LRTs and retaining LST yield benefits.

Status: No token issued. TVL $718.76M, outperforming Restake Finance. No fees charged—a current advantage. Community: 23.6K Twitter followers, low engagement.

Restake Finance ($RSTK)

RSTK is the first modular liquidity restaking protocol on EigenLayer, simply helping users deposit LSTs into EigenLayer. It lacks innovation or competitive edge. Its tokenomics offer little novelty. Token price surged temporarily due to restaking and EigenLayer hype but has since underperformed.

Business Logic:

● Users deposit LSTs generated from liquid staking into Restake Finance;

● The protocol deposits users’ LSTs into EigenLayer and issues rstETH as a restaking receipt;

● Users use rstETH in DeFi to earn yield and accumulate EigenLayer积分 (pending token launch).

Token Utility:

● Governance

● Staking for protocol revenue share

Status: TVL $15.5M, 4,090 rstETH in circulation, over 2,500 unique addresses, more than 750 users. Community: 12.8K Twitter followers, low engagement.

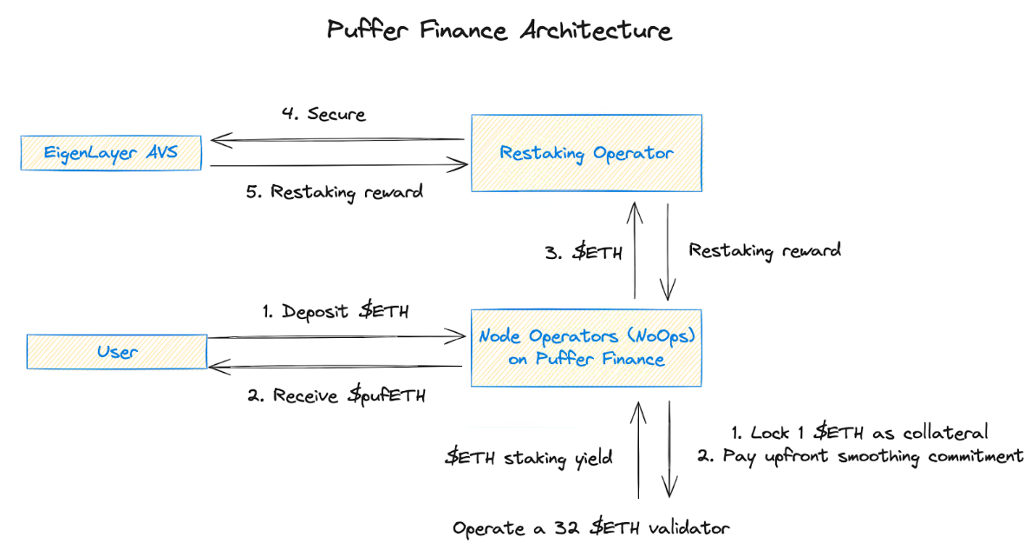

Puffer Finance

Backed by Binance Labs, Puffer has gained significant recent attention. Puffer Finance is a slashing-resistant liquid staking protocol falling under the Liquid Native Restaking category. It raised $6.15M in a seed round led by Jump Crypto. Puffer also plans to develop a Layer 2 network.

Advantages:

● While EigenLayer requires 32 ETH per node, Puffer lowers the threshold to 2 ETH, aiming to attract smaller node operators.

● Enhanced security via secure-signer & RAVe (Remote Attestation Verification on-chain).

Business Logic:

● Users stake $ETH to receive $pufETH. Puffer’s Node Operators split the $ETH—part goes to Ethereum validators, part to EigenLayer restaking.

Status: Staking live. 365,432 pufETH minted, TVL $1.40B. Community: Largest Twitter following among LRT projects—213.7K.

Liquid Staking + Restaking Services

These projects already held strong positions in liquid staking before entering restaking. Advantages include: 1) Already managing large ETH deposits, easily convertible to restaking tokens; 2) Existing user base—users don’t need to seek separate LRT protocols. Swell and Ether.fi have emerged as leaders in the EigenLayer ecosystem, leading by deposit volume.

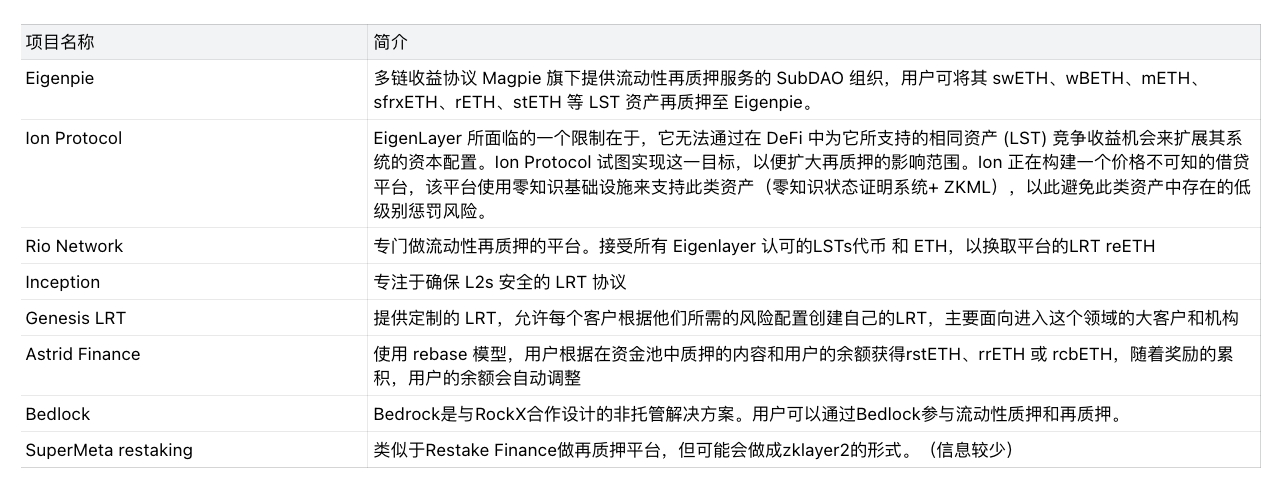

Other LRT Protocols

Conclusion

Currently, many LRT protocols have not issued tokens and suffer from high homogenization. However, KelpDAO, Puffer Finance, and Ion Protocol stand out with clearly differentiated development strategies.

Based on token issuance rankings among LRT protocols, ether.fi leads in quantity, followed by Puffer Finance and Renzo.

● From a practical standpoint, LRT resembles a speculative leverage tool for liquidity. “Leverage” means the original asset remains one, but through token mapping and locked权益, multiple derivative receipts can be layered on top of the same ETH.

● These derivative instruments greatly enhance liquidity during bullish cycles, favoring market speculation.

● However, because protocols are interconnected via liquidity—holding A allows borrowing B, borrowing B unlocks C—if a major protocol A fails, the risk cascades systemically.

Future Outlook for the LRT Sector

Overall, the LRT sector is a rapidly growing niche market. The LST sector offers ~5% stable yield, attractive during bear markets. LRT yields depend heavily on the capabilities of restaking providers like EigenLayer—only sustainable yields will ensure continued user interest and capital accumulation. The LRT space is still early, with severe homogenization and limited capital capacity. We predict only a few top-tier projects will ultimately succeed.

Risks:

● Slashing risk: Increased likelihood of losing staked ETH due to malicious activity.

● Centralization risk: If too many stakers migrate to EigenLayer or similar protocols, systemic risks to Ethereum could arise.

● Smart contract risk: Vulnerabilities may exist in protocol smart contracts.

● Multi-layered risk stacking: A core issue with restaking—compounding existing staking risks with additional ones, creating complex, multi-tiered exposure.

Future Opportunities:

● Multi-layer DeFi integration of LRTs, such as lending.

● Enhanced security: DVT technology can reduce node operation risks (e.g., SSV, Obol).

● Multi-chain expansion: Developing LRT protocols across multiple L2s or PoS chains (e.g., @RenzoProtocol, @Stake_Stone).

— — — — — — — — — — —

About Us

This report was authored by the Research team under HTX Ventures. HTX Ventures is the global investment division of HTX, integrating investment, incubation, and research to identify the world’s most outstanding and promising teams. As a pioneer in the blockchain industry for over a decade, HTX Ventures drives cutting-edge technological advancements and emerging business models, offering comprehensive support—including funding, resources, and strategic consulting—to foster long-term blockchain ecosystems. To date, HTX Ventures has supported over 200 projects across multiple blockchain sectors, with select high-quality projects listed on HTX. Additionally, HTX Ventures is one of the most active fund-of-funds (FOF) investors, partnering with top-tier global blockchain funds such as IVC, Shima Capital, and Animoca Brands to co-develop the blockchain ecosystem.

References

1. SevenX Ventures: The Landscape and Opportunities of LRT (Liquidity Restaking Tokens)

https://foresightnews.pro/article/detail/51837

Join TechFlow official community to stay tuned Telegram:https://t.me/TechFlowDaily X (Twitter):https://x.com/TechFlowPost X (Twitter) EN:https://x.com/BlockFlow_News