Once Secretly Backed by a16z with $100 Million, Why Kickstarter's Crypto Dream Struggles to Become Reality?

TechFlow Selected TechFlow Selected

Once Secretly Backed by a16z with $100 Million, Why Kickstarter's Crypto Dream Struggles to Become Reality?

An investment's return should not solely depend on whether the project itself succeeds.

By Leo Schwartz, Jessica Mathews, Fortune Magazine

Translation: Luffy, Foresight News

In early December 2021, employees at crowdfunding startup Kickstarter received news of an unexpected windfall: an investment firm wanted to buy a portion of their shares. The announcement caused quite a stir within the company. Although employees had been accumulating equity for years, many had long since given up hope of ever being able to sell it.

The Kickstarter they now worked for was vastly different from the hot startup of 2009 that launched viral projects like Cards Against Humanity and Peloton. At the time, Kickstarter earned widespread acclaim from entrepreneurs and the public alike, even achieving the coveted startup milestone of becoming a verb—“Kickstarter” became synonymous with online crowdfunding campaigns.

Back then, the company’s anti-corporate ethos and grassroots spirit attracted celebrity investors and helped shape the early New York tech scene. Its events—from film premieres to rooftop festivals—and viral fundraising drives demonstrated that creative business ideas could find funding outside Silicon Valley, and that artists could gain direct support from fans.

But more than a decade after its launch, Kickstarter had lost much of its luster, cycling through CEOs. By 2021, the startup offered little to potential investors beyond headaches. Growth had plateaued; the company made money by taking a small cut when projects on its platform met funding goals. After a bitter unionization campaign, its once-positive culture had eroded into one perceived as hostile to progress. Many believed new shareholders would inherit ownership of a brand already past its prime.

For Kickstarter employees and early investors, this unexpected investment felt like a chance for redemption. After all, this wasn’t a modest round to keep the lights on—it was a staggering $100 million investment valuing the startup at $400 million. But there was a catch: the investment came with the expectation that Kickstarter would pivot toward blockchain, as its new backer—the crypto fund of venture capital giant Andreessen Horowitz—sought to ride the latest hype cycle.

This windfall could have provided the push the company needed to reinvent itself and regain relevance. Instead, the move into blockchain sparked sharp backlash from the community of creators and fans upon which Kickstarter depended, leading to high-profile project losses and reputational damage. The turmoil illustrates how even the most promising startups can lose their way, while highlighting the challenges of pursuing a do-good mission built on venture capital.

Trouble in Paradise

When Kickstarter launched in 2009, it was a pioneer among a group of New York startups—including Etsy and Foursquare—that challenged West Coast counterparts by focusing on art and culture, diverging from the engineer-first ethos of Bay Area projects like Google and Facebook.

The idea for Kickstarter—artists or creators seeking public funding for new albums, board games, or comic books—came from Perry Chen, a former DJ who started the company after struggling to raise funds to host a concert during the New Orleans Jazz Festival. Its most notable early investor was Fred Wilson, an early backer of companies like Tumblr and Twitter, whose Union Square Ventures is perhaps the most iconic New York-based venture firm.

Kickstarter began in a stylish loft in Manhattan’s Lower East Side, its front door covered in graffiti and bearing a sticker that read “Eat Shit.” The company built user engagement through events, hosting its first annual film festival in 2010 on the roof of the Gowanus Old American Can Factory in Brooklyn. Clips of projects funded via the platform played on screens—including intricate dances mimicking endangered plants and animals—while a brass band backed by Kickstarter performed for guests lining up to buy pies and craft sodas from crowdfunded food ventures.

Early employees recall a company that prioritized creativity and social consciousness over the typical Silicon Valley obsession with growth at all costs. Unlike typical venture-backed startups pursuing hockey-stick growth through losses, the Brooklyn-based company charged a 5% fee on successfully funded projects, a model that allowed Kickstarter to turn a profit as early as its second year.

The model gained widespread attention and achieved breakout success with projects such as Phoebe Waller-Bridge’s BBC comedy Fleabag (which later won Emmys), and the VR headset Oculus Rift (later sold to Facebook for $2 billion). In 2013, after the popular TV series Veronica Mars was canceled by Hulu, showrunner Rob Thomas turned to Kickstarter to raise $5.7 million for a movie. It became the most-funded project in Kickstarter history at the time, proving its mission of returning power to creators.

“Art for art’s sake really mattered,” a former Kickstarter employee told Fortune. “Whether a project could deliver returns to investors shouldn’t be the sole measure of its value.”

Kickstarter made it clear early on that it wasn’t chasing wealth, yet investors still poured in significant capital, including a $10 million round in 2011. Early backers included Meetup co-founder Scott Heiferman, Vimeo co-founder Zach Klein, and Arrested Development actor David Cross. Chris Dixon—now founding partner at a16z crypto—also joined as an angel investor.

Everyone seemed to understand that Kickstarter wasn’t built for massive financial returns. In a 2013 blog post, Wilson notably pointed out that Kickstarter didn’t need help from venture firms (even though they still contributed): “It never needed outside money, nor did it do much to optimize for profitability.” Another early investor told Fortune they invested because they “just liked the idea,” never expecting economic returns.

Yet, those early good vibes at Kickstarter would soon give way to another sentiment: a pervasive sense of chaos. When co-founder Yancey Strickler took over as CEO in 2014, the company began a rotating leadership model, although Chen remained involved in management roles in the years that followed.

Then in 2015, Kickstarter took the rare step of becoming a public benefit corporation—a for-profit entity legally required to meet social and environmental standards. Employees described the benefit corporation structure in a podcast as a legal safeguard protecting Kickstarter from investors attempting to force an exit or sale. “Reorganizing as a public benefit corporation blurred the line between personal values and corporate values,” one employee said on the podcast. “Our founders often described it as a structure enabling the company to operate like an organization driven by more than just profit.”

Chen reaffirmed this message when he returned as CEO in 2017, reiterating earlier claims that Kickstarter would never go public or be acquired. This performative commitment to ideals began to frustrate employees. “I definitely felt extreme exhaustion and burnout, and I don’t think employees had much confidence in Perry,” one employee said.

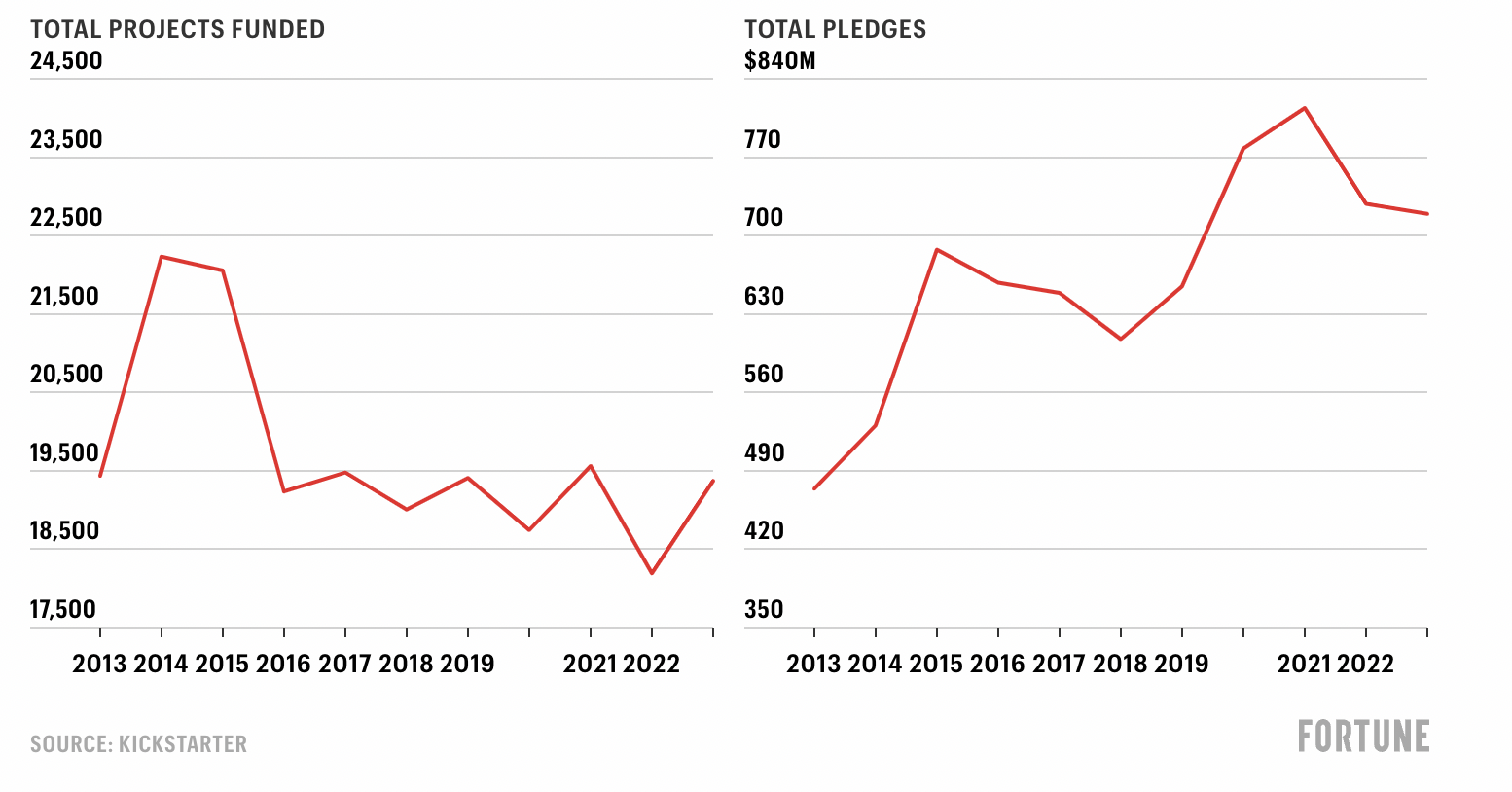

Although Kickstarter figured out how to make money early on, the company seemed perpetually unable to scale. By 2016, the number of crowdfunding projects on the platform stabilized at around 19,000 per year, showing no signs of growth. The amount of funding it took a cut from fluctuated annually, peaking near $814 million during the pandemic.

Number and funding amounts of projects funded on Kickstarter over the past decade

One early investor told Fortune that Kickstarter consistently failed to balance growth with adherence to its new charter, which required it to take on socially valuable but costly obligations. Despite its noble mission, internal dysfunction stemming from competing priorities left employees struggling to find career advancement paths.

In 2012, Kickstarter spent $7.5 million to purchase a building owned by a pencil company in Brooklyn’s trendy Greenpoint neighborhood. The space quickly became a template for mid-2010s tech offices, complete with a rooftop garden, sunroom, and cinema. Employees would drop by late on Saturday nights and still find others hanging around. On the flip side, the laid-back work culture led to stagnation, with some employees working only a few hours a day.

Meanwhile, the company continued to struggle with growth strategy. In 2016, it acquired a startup called Drip in response to the fast-growing subscription crowdfunding platform Patreon, but the move failed, and plans to counter its rising competitor were scrapped.

“Coming up with something that doesn’t conflict with some part of their mission isn’t the easiest task,” one investor said. “It feels like this has been going on for years.”

Dissatisfaction began brewing among employees, many of whom joined because of the company’s mission, which one described as a “dreamlike, lofty atmosphere.” They knew that due to Chen’s promise never to sell the company, their equity stakes would never increase in value.

In March 2019, tensions in Kickstarter’s workplace culture erupted in the form of a unionization drive—an unprecedented move for full-time tech workers at the time. New CEO Aziz Hasan, another leader stepping in after Chen, responded by calling an all-hands meeting and stating the company would not voluntarily recognize the union. Kickstarter fired two employees leading the union effort. Both immediately sued, accusing the startup of illegal retaliation.

Kickstarter’s clumsy handling of the union push shattered the illusion that it was a different kind of startup. The move drew condemnation from Kickstarter creators, including David Cross, who used Twitter to urge fans to support the union. Supporters of progressive projects funded through the platform, such as the magazine Current Affairs, threatened to withdraw their backing. Shortly after recognizing the union, the company laid off 18 of its 140 employees, with Hasan citing a decline in new projects on the platform.

In early 2020, the pandemic forced Kickstarter employees to leave their Greenpoint headquarters and begin working remotely. During this period, the platform saw a brief surge as people stuck at home sought ways to support creators. Meanwhile, venture capital flooded into other startups at record levels and valuations, and cryptocurrency prices soared to all-time highs, with Bitcoin reaching $69,000 in November 2021. Just one month later, Kickstarter announced its blockchain plans—and a $100 million acquisition offer.

The Blockchain Gamble

Kickstarter was exactly the kind of company that appealed to rising venture capitalist Chris Dixon. Dixon ran Hunch, a recommendation startup in the early 2010s, and regularly wrote on his widely-read blog about longing for a more egalitarian era of the internet. He and colleagues at Founder Collective—a small VC fund founded by New York tech entrepreneurs—had already invested in another company called 20×200, aimed at “democratizing art” by sharing revenue with artists.

Dixon and his Hunch co-founder Caterina Fake both invested in Kickstarter in 2011, helping make the startup a darling of the New York tech scene. Soon after, Dixon joined Andreessen Horowitz, where he became enamored with blockchain, viewing the technology as a way to return the internet to its open-source roots. The firm would launch a dedicated unit called “a16z crypto” in 2018 focused exclusively on blockchain investments.

In his new role leading a16z crypto, Dixon raised up to $2.2 billion for his third fund and maintained contact with Chen. According to a person familiar with the matter, Kickstarter board members, including Chen, approached Dixon in the summer of 2021 to discuss a new investment, proposing the blockchain pivot as the driving force behind the deal. For Dixon, the prospect of bringing a familiar name like Kickstarter into the Web3 promised land was too enticing to pass up.

The deal wasn’t an injection of capital into Kickstarter in exchange for new equity; instead, it was structured as a tender offer, meaning all new cash would be used to buy existing shares held by other shareholders, with no money flowing directly to Kickstarter. Instead, it allowed employees and early investors to cash out.

According to sources, the secretive funding round totaled $100 million, led by a16z crypto and including several smaller investors, such as Yes VC, an early-stage fund led by Dixon’s former co-founder Fake, who also co-founded photo-sharing site Flickr.

While this was a massive check for a company with minimal revenue, it wasn’t unusual for a16z crypto. Dixon had made other bold bets to realize his vision for crypto networks, such as co-leading two rounds totaling over $160 million in 2018 for startup Dfinity. (Dfinity later became embroiled in controversy, with its token crashing 95% shortly after launch.)

In return for a16z’s generous backing, Kickstarter would attempt to become a Web3 company. This ambitious but unlikely plan required migrating its entire platform onto Celo, a blockchain developed by another a16z portfolio company. Kickstarter would operate as an open-source protocol rather than a tech company.

Meanwhile, users would be able to create their own niche mini-platforms around interests like anime, drawing in more participants and sharing profits through Kickstarter. This structure echoed models like Farcaster—users wouldn’t need to pay in cryptocurrency, but Kickstarter would need to build an entirely new open-source version of its software atop a blockchain that had never been tested with large-scale consumer applications.

Few in the crypto industry considered Celo a top-tier blockchain project, but it did boast a “carbon-negative” footprint, allowing Kickstarter to align with its environmental mission. Sepandar David Kamvar, Celo’s co-founder, joined Kickstarter’s board in August 2022.

The deal didn’t require Kickstarter to follow through. Nevertheless, one employee who worked at Kickstarter during the tender offer said the company clearly communicated internally that a16z was involved and that the venture giant was investing because Kickstarter was willing to enter Web3.

The tender offer landed in employees’ inboxes on December 8, 2021—the same day Kickstarter revealed its blockchain plans. They could sell up to 32.49% of their shares at $7.41 per share, a significant markup from their purchase price, and could choose to sell even more if others opted out. Kickstarter would even cover related fees.

For some employees, the buyout was a welcome surprise after years of turbulence. “It felt like a once-in-a-lifetime opportunity,” one employee recalled thinking upon receiving the offer.

Taylor Moore, one of the fired union organizers, reacted to the news with alarm.

“Kickstarter’s leadership talks about Perry Chen and his sycophants like characters in the classic tale of the Emperor’s New Clothes—completely detached from reality,” he told Fortune. “Meanwhile, the people actually doing the work know it’s a stupid idea.”

Despite Chen’s newfound enthusiasm for blockchain, the announcement offered few concrete details and set a timeline of less than a year for the transition. This raised concerns among the Kickstarter community, who feared the plan would turn their beloved project platform into a get-rich-quick scheme amid crypto market hype. Some users expressed concern about the environmental impact of shifting to blockchain, which could generate massive carbon emissions—even though Kickstarter chose Celo for its climate-friendly profile.

Isaac Childres, founder of a popular tabletop game company, wrote in a June 2022 newsletter: “What we’ve seen in crypto is almost rampant fraud, theft, and financial loss,” announcing that future projects would move to other crowdfunding platforms.

Much of the community’s anger was directed at employees, who voiced skepticism in group chats. Meanwhile, the company decided to hire external consultants to announce the blockchain move, leaving many employees unprepared for the wave of sharp criticism from users. Given Kickstarter’s track record of stumbling through new initiatives, doubts emerged about its ability to pull off a major technical transformation. “It was just unbelievable,” one employee said.

The blockchain plan seemed doomed from the start—and soon proved to be. Within months, executives stopped mentioning it, and no part of the platform migrated to run on blockchain. “It felt like Drip,” said a former employee, referring to the ill-fated Patreon rival. “They announced it, and then nothing happened.”

In 2022, Kickstarter hired another CEO, Everette Taylor—its fifth leadership change in a decade—taking over after a series of events including union organizing, the failed blockchain rollout, and the departure of about 40% of staff. According to a Kickstarter spokesperson, Chen quietly stepped down as board chair and began a transition plan last year to fully leave the board.

New CEO Taylor made it clear immediately that blockchain was no longer a priority. On October 4, 2022—one week after taking office—he told TechCrunch: “We are not committed to moving Kickstarter onto the blockchain.”

Although Dixon and a16z crypto declined to comment on this article, Dixon recently stated at a book launch event for his new title Read Write Own that despite public aversion to blockchain, it remains a long-term game. Meanwhile, Kickstarter hasn’t completely ruled it out. After announcing the initiative in 2021, it formed an independent public benefit corporation called Creative Crowdfunding Protocol, staffing it with two employees, including a former Kickstarter operations manager. Today, its website lists two software engineering job openings in Bangladesh, and Celo still lists Kickstarter as an “ecosystem partner.”

The shift hasn’t damaged Kickstarter outright, and a16z’s funding undoubtedly helped rebuild goodwill with employees and investors. But employees say it was yet another distraction hindering the company from emerging from its slump. The blockchain collapse ultimately alienated both users and staff, reinforcing the perception that Kickstarter’s glory days are behind it.

In a late 2022 interview hosted by Celo, Kickstarter COO Sean Leow insisted the company still believed in the protocol. When asked whether he saw gaps in the vision, Leow replied: “I’d say currently 95% of it is gap.”

Kickstarter declined to make Leow, Taylor, or other executives available for interviews.

Feeling the Way Forward

Kickstarter may have achieved the rare startup honor of becoming a noun, but the company has lost its former shine. “When I say I worked at Kickstarter, everyone’s instinctive reaction is, ‘Oh, is that still a company?’” said a former employee who joined in 2022.

Today, Everette Taylor continues searching for new revenue streams, launching initiatives to help creators with logistics and tax planning. The CEO has also tried to reintroduce Kickstarter to the public through magazine interviews and conference appearances, emphasizing his role as a Black CEO and the company’s commitment to executive diversity.

A year after Taylor joined, Kickstarter appointed a new CFO to help boost revenue. According to company data and internal emails sent by the CFO, while total fundraising has grown, revenue has declined since 2019. “They’re always talking about it,” said a former employee. “It feels like every all-hands meeting is an emergency.” A spokesperson declined to provide Kickstarter’s revenue figures.

Ultimately, new products haven’t addressed Kickstarter’s core problem: over the past decade, the number of projects funded annually on the platform has stopped growing. Taylor’s more corporate approach to a company whose internal motto was once “Fuck the monoculture” has drawn criticism from five former employees interviewed by Fortune. In early 2023, Taylor became a spokesperson for a Chevrolet ad campaign and joined the board of a publicly traded online luxury marketplace in February.

“A lot of people were frustrated that the CEO was making sponsored content,” one employee said. “It felt like a betrayal of company values.”

Widespread fraud on the platform remains another persistent concern. Over the past three years, the Better Business Bureau has received over 100 complaints about the company, many involving scams or users never receiving the products they supported. Last year, the Ohio Attorney General reached a settlement with a Kickstarter scammer who claimed to raise funds for a turtle conservation charity but instead funneled the money into cryptocurrency. The scammer agreed to repay defrauded donors and refrain from crowdfunding in Ohio for five years.

Due to Kickstarter’s mechanics, projects can receive full funding without launching, and Kickstarter still takes a cut. According to Fortune’s understanding, an internal estimate suggested revenue from fraudulent projects could reach as high as 18%, echoing past actions by state attorneys general and the Federal Trade Commission investigating scams on Kickstarter. (Kickstarter itself has not been accused in these lawsuits or complaints.) A spokesperson denied the estimate and said the company has taken “extensive measures” to combat fraud, including new detection software and processes.

With prices soaring again, cryptocurrency is regaining popularity, and open-source protocols could still offer solutions to Kickstarter’s thorny problems. As Leow mentioned in the 2022 interview, blockchain’s immutable ledger with traceable addresses and transaction history could help address the platform’s struggles with fraud and trust.

Still, Kickstarter’s biggest challenge may simply be that time has passed. “I feel like they’re outdated,” a former employee told Fortune. “Why would people go to Kickstarter when there are so many other viable ways—like becoming a TikTok influencer—to raise money?”

Kickstarter does serve a niche market for independent creators wanting to produce, say, a board game with detailed instructions or a clock using AI to write a new poem every minute.

“Since its launch in 2009, creative projects on Kickstarter have secured $8 billion in pledges,” said the spokesperson in a statement. “Looking ahead, we will continue to center our work around community.”

The spokesperson said the company’s position in the creator economy differs from platforms like TikTok. They pointed to recent projects funded by social media influencers and a Kickstarter-backed film recently screened at the Sundance Film Festival.

However, competitors like BackerKit have attracted disgruntled users after the blockchain scandal, and Kickstarter continues to lose top creators. In February, fantasy author Brandon Sanderson, who launched the largest campaign in Kickstarter history, announced his next project would be on BackerKit.

Ultimately, Kickstarter failed to reinvent the rules of investor and community support. Instead, each time it tried to leap to a new level, it stumbled over its own idealism.

“People want it to become a marketplace again and regain household-name status,” said a recently departed employee. “I feel we’re stagnating because our reputation keeps getting worse.”

After the pandemic, Kickstarter never moved back into its 33,000-square-foot brick headquarters in Greenpoint, choosing instead to sell it for $29.5 million. After months of searching, Kickstarter is now in negotiations with a potential buyer.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News