Binance Research: Are We Entering a Bull Market? The 10 Most Important Narratives to Watch

TechFlow Selected TechFlow Selected

Binance Research: Are We Entering a Bull Market? The 10 Most Important Narratives to Watch

The crypto market saw significant growth at the end of the year, with NFT trading volume surging and DeFi and Bitcoin regaining spotlight, while global interest rate trends sparked market expectations.

Author: Binance Research

Translation: Baicai Blockchain

I. Introduction

Following the highs of 2021, the crypto market has largely been a build-focused environment over the past few years. As the frenzy around celebrity-endorsed NFTs, $69,000 Bitcoin, Dogecoin on SNL, and other narratives faded, some left the industry while others doubled down, broadening their horizons. In recent weeks, we’ve seen increasing market excitement—evident in both crypto events and asset prices—beginning to show some signs of a bull market.

While it’s still too early to claim we’ve entered a bull market, conditions are certainly better than they have been for some time. It is precisely for this reason that Binance Research has prepared this report, offering readers key narratives and indicators to monitor in the coming months.

So far this year, the total market capitalization of the crypto market has increased by approximately 110%, equivalent to over $870 billion. In Q4 alone, the market has grown by 55% (approximately $596 billion).

II. Key Narratives

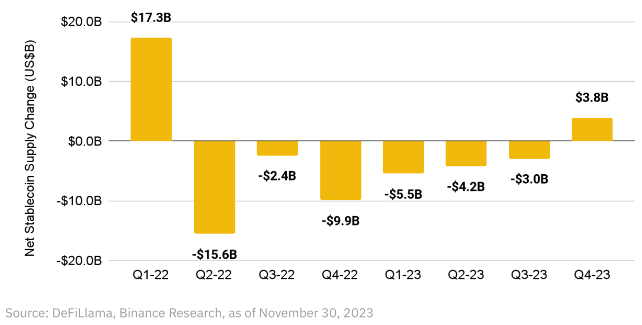

1. Stabilization of Stablecoin Supply Returns

Stablecoin supply serves as an indicator of the amount of capital ready and available for investment in crypto assets at any given point. Recent data shows that for the first time since Q1 2022, the net quarterly supply change among the top five stablecoins by market cap has turned positive.

Given that rising stablecoin supply indicates capital inflows into the crypto market and reflects growing underlying buying pressure, this recent shift can be viewed as a positive signal. Over the coming months, it will be important to closely track whether this trend is temporary or marks the beginning of a more sustained upward trajectory.

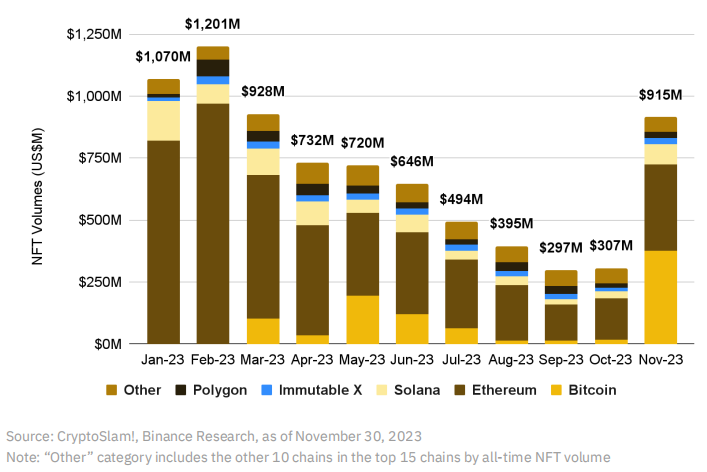

2. Rising NFT Trading Volume

NFT trading volume can serve as a leading indicator of market sentiment, as NFTs are considered highly volatile investments within the crypto space. For example, if we view Bitcoin as the benchmark asset, alternative tokens such as Ethereum tend to be more volatile—exhibiting higher price swings compared to Bitcoin.

If we continue along the risk spectrum, we eventually arrive at NFTs. The fact that NFT trading volume has broken its prolonged downtrend and shown significant month-on-month growth suggests positive market sentiment and a revival of speculative activity in the NFT sector after months of depressed prices and pessimism.

NFT trading volume broke its annual downward trend, showing notable month-on-month growth in November.

We should also highlight the remarkable rise of Bitcoin NFTs (discussed in greater detail in the “Bitcoin” section). Their growth has been extraordinary—as illustrated above—especially considering they were effectively invented in late 2022 and only began gaining traction in March 2023.

Bitcoin NFTs had almost no trading volume in January but became the most traded NFT category in November, with over $375 million in volume—surpassing Ethereum NFTs ($348 million). This is a significant achievement for a chain long thought to be unsuitable for applications and NFTs, and it will be fascinating to monitor developments over the coming months.

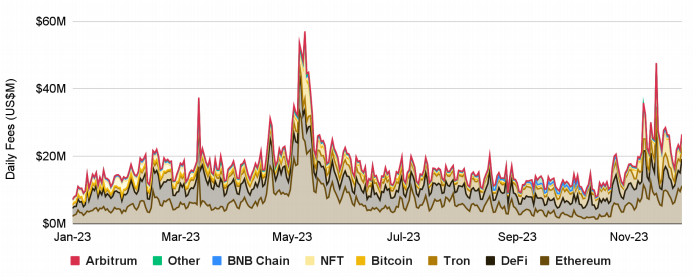

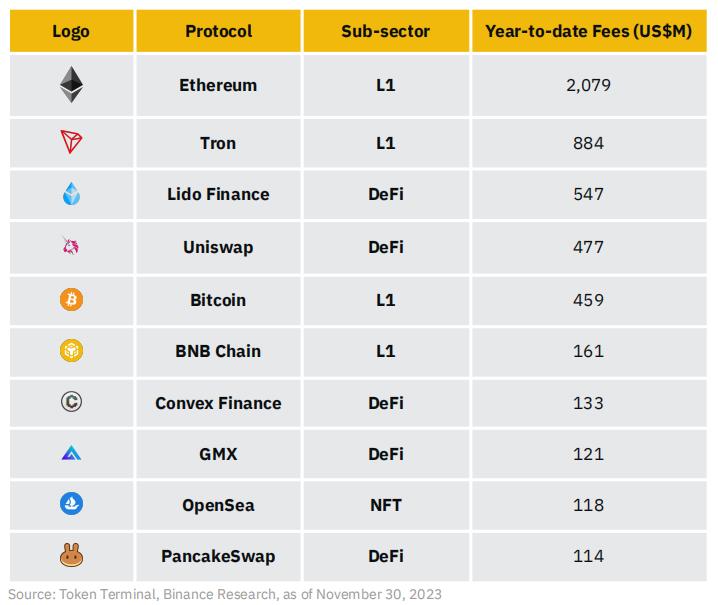

3. Protocol Fee Growth

As the industry continues maturing and protocols increasingly adopt revenue-generating business models, fees generated by top crypto projects have become a crucial metric to track. Over the past year, these fees have risen steadily, increasing by over 88% from January to November.

Note: "DeFi" includes Lido, Uniswap, Convex, GMX, PancakeSwap, MakerDAO, Aave, dYdX, Venus, and Curve. "NFT" includes OpenSea, Manifold.xyz, and Blur. "Others" include Flashbots and friend.tech.

In terms of cumulative fees, Ethereum has generated more than double the fees of any other single protocol year-to-date, exceeding $2 billion in total fees. Tron follows with approximately $880 million. Ethereum generates fees primarily by selling block space. Users paying these fees range from retail traders swapping memecoins on Uniswap to Layer 2 protocols like Arbitrum, which pay Ethereum to settle their transactions.

DeFi ranks second in fee generation after Ethereum, led by Lido and Uniswap. Convex, GMX, PancakeSwap, and MakerDAO have each generated over $100 million in fees year-to-date, with Aave close behind.

In the NFT space, OpenSea clearly leads, generating nearly twice the fees of Manifold and more than double those of Blur. Over the past year, competition between these two major NFT platforms has been intense. While Blur successfully increased its share of Ethereum NFT trading volume from about 40% to around 80%, OpenSea’s share declined from roughly 43% to about 20%. Nevertheless, OpenSea remains ahead in terms of fee generation.

The top 10 fee generators this year are dominated by Layer 1 networks and DeFi projects.

Notably, friend.tech, launched only in summer, has entered the top 20 protocols by fees (generating over $50 million). This highlights the opportunities available for projects capable of generating buzz and momentum, particularly in the emerging social finance (SocialFi) sub-sector.

Interestingly, Arbitrum is the only Layer 2 in the top 20, having generated over $50 million in fees. This is significant given the ongoing discussions around Layer 2s and their growing importance. Yet only Arbitrum appears on the list—a potentially telling sign, especially considering newly announced or launched L2s.

Overall, fee generation is a hallmark of truly sustainable businesses. Clearly, certain segments of the crypto market are capable of generating meaningful revenue, and seeing these numbers grow consistently throughout 2023 is encouraging. Monitoring which protocols and sub-sectors demonstrate the strongest fee growth will be a critical focus as we move into the next phase of the market cycle.

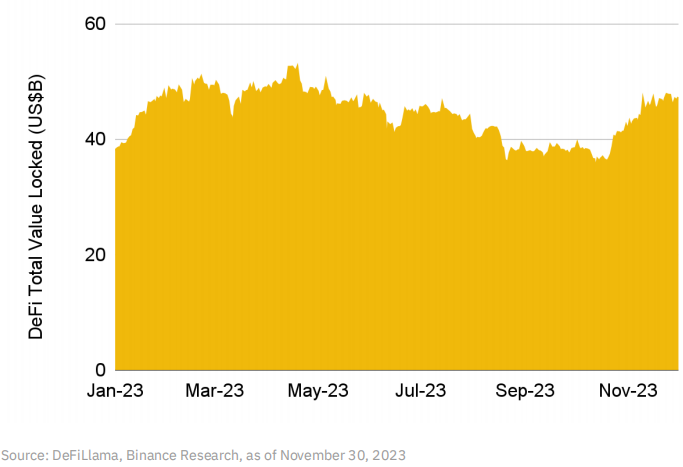

4. Return of DeFi

After months of relatively limited activity in the DeFi space, we are beginning to see signs of renewed engagement. Total Value Locked (TVL) in DeFi has increased by nearly 25% since the beginning of the year, with a 14% month-on-month increase in November. Since December last year, TVL has fluctuated between $45 billion and $50 billion. It will be important to observe whether this latest uptick is sustained and whether TVL can comfortably break above the $50 billion threshold in the coming weeks and months.

By blockchain, Ethereum remains the dominant player, accounting for over 56% of total TVL. Tron holds about 16%, BNB Chain slightly over 6%, with Arbitrum (~4.5%) and Polygon (~1.8%) making up the rest of the top five. Notably, four of the top ten blockchains by DeFi TVL are Ethereum Layer 2 networks (in addition to OP Mainnet and Base mentioned earlier).

By category, liquid staking (with $27 billion in TVL) has been one of the biggest winners this year, led by Lido, which commands over $20 billion in TVL. The Shanghai upgrade, which enabled withdrawals of staked ETH, significantly benefited Lido, helping it grow from ~$12 billion in TVL to over $20 billion today. Lending ($19 billion), decentralized exchanges ($13 billion), and bridges ($13 billion) follow as the next most popular categories.

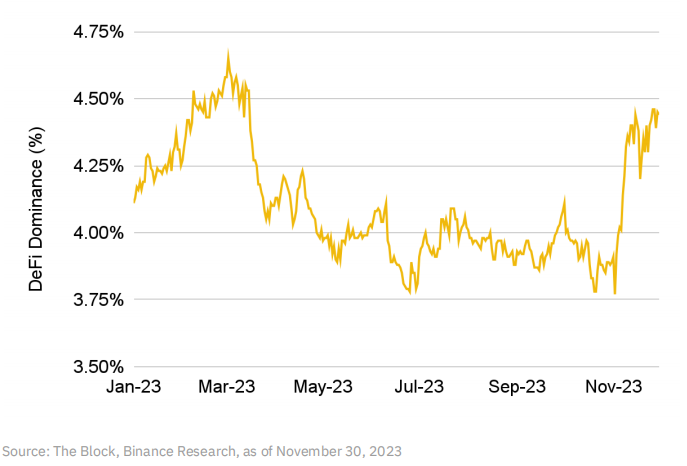

Another noteworthy chart is DeFi’s dominance—measured by calculating the combined market cap of top DeFi tokens as a percentage of the overall crypto market cap. After hovering between 3.8% and 4.1% since April, this figure began rising rapidly, increasing by 18% in November to reach 4.44% by month-end. Tokens such as Thorchain, PancakeSwap, Uniswap, and Synthetix were key drivers of this shift.

Key developments to watch:

-

MakerDAO will continue advancing toward its ultimate vision, with Stage 1 of its planned five-stage rollout expected in early 2024.

-

PancakeSwap recently launched its gaming marketplace and a new governance system featuring a novel vote-escrowed (ve) token, veCAKE.

-

Synthetix’s new product, Infinex—an upcoming decentralized perpetuals exchange—is set to launch soon.

-

Fluid, a high-capital-efficiency multi-layer DeFi protocol developed by the Instadapp team, is launching.

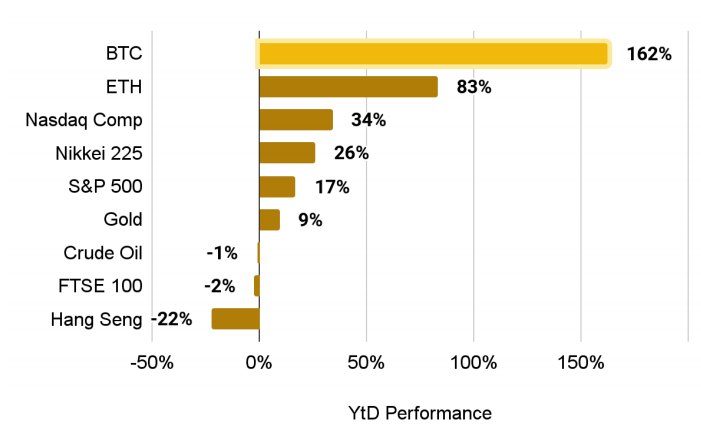

5. Bitcoin

It has been an eventful year for Bitcoin, attracting interest ranging from extreme crypto-native Ordinals (Bitcoin NFT) collectors to more traditional institutional investors approaching Bitcoin ETFs. So far, this has driven a substantial 162% increase in Bitcoin’s market cap in 2023—outperforming many other crypto assets and broader markets.

Bitcoin has performed very strongly year-to-date.

Key Bitcoin narratives:

A. Approval of Spot Bitcoin ETFs More Likely Than Ever

While the potential for a U.S.-regulated spot Bitcoin ETF has long existed, 2023 saw significant positive progress. Notably, the dispute between the SEC and Grayscale concluded largely in Grayscale’s favor. This prompted other players—including BlackRock, Fidelity, and Invesco—to submit applications for spot Bitcoin ETFs.

Currently, 13 spot Bitcoin ETF applications are under review by the SEC, with decision deadlines ranging from January 2024 to August 2024. Market expectations are high that approvals could come in the coming weeks or months, especially given the outcome of the Grayscale case and applicants’ ongoing efforts to revise their filings to improve approval odds.

Many final decision deadlines for SEC rulings on spot Bitcoin ETFs fall in Q1 2024, starting in January.

If approved, spot Bitcoin ETFs would address two major barriers to Bitcoin adoption: convenience/accessibility and mainstream acceptance.

With such ETFs, many institutional investors could easily, compliantly, and widely include Bitcoin in portfolios—improving distribution. Endorsement by global asset management giants like BlackRock, Fidelity, and Invesco would enhance Bitcoin’s legitimacy and help alleviate regulatory/compliance concerns among new investors. This is expected to trigger substantial inflows into Bitcoin from institutions previously on the sidelines and retail investors who may have had reservations.

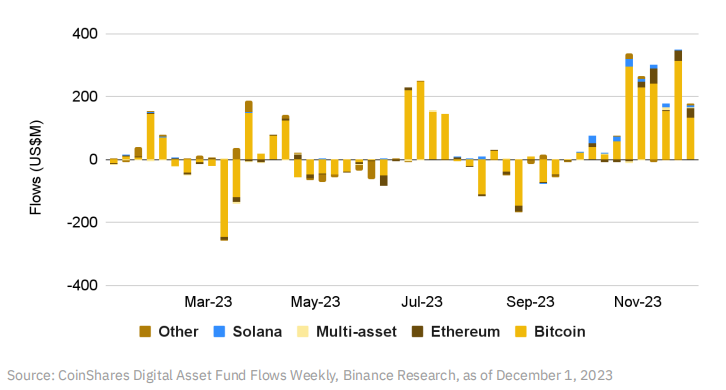

Recent data from CoinShares shows Bitcoin ETPs attracted over $1.6 billion in inflows, making them one of the most popular assets. Total assets under management have grown over 100% since the start of the year, reaching $46.2 billion—the highest level since May 2022. This reflects growing investor interest in regulated crypto exposure through traditional financial channels.

Global inflows into crypto ETPs showed significant increases in October and November, with Bitcoin being the dominant asset.

B. Upcoming Bitcoin Halving

Bitcoin miners are incentivized through two mechanisms: block rewards and transaction fees.

Block rewards have traditionally made up the bulk of miner income, while transaction fees have only recently seen volume increases following the launch of Ordinals. Block rewards are issued for every newly mined block—approximately one every 10 minutes—and are cut in half roughly every four years. Block rewards started at 50 BTC per block when the Bitcoin blockchain launched in 2009.

After halvings in 2012, 2016, and 2020, the current block reward is 6.25 BTC. This will halve again in April 2024 to 3.125 BTC per block.

Bitcoin’s mining reward halves approximately every four years, with the next halving expected in April 2024.

Considering Bitcoin is an asset with a fixed maximum supply (21 million) and the halving reduces the rate of new Bitcoin creation by 50%, basic economic principles suggest rising prices are a natural consequence. The halving inherently creates scarcity for Bitcoin, reinforcing its narrative as digital gold. Historically, this event correlates with increased market volatility, though overall, crypto markets tend to perform well in the year following a halving.

C. Continued Growth of 'Ordinals' and 'Inscriptions'

One of the most significant developments for Bitcoin in 2023 has been the emergence of Ordinals and Inscriptions. Casey Rodarmor’s “Ordinal Theory” enables tracking of each smallest unit of Bitcoin—satoshis—and assigns a unique identifier to each satoshi.

These individual satoshis can then be “inscribed” with arbitrary content—such as text, images, or videos—creating what is known as an “inscription,” or quickly dubbed Bitcoin NFTs. For a deeper dive, see our report “A New Era for Bitcoin?”

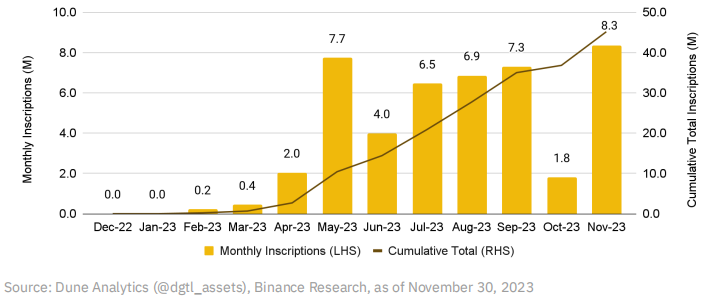

Following a resurgence in minting volume in November, total Bitcoin inscriptions are approaching 50 million.

Inscriptions led to the creation of BRC-20 tokens, enabling the deployment, minting, and transfer of fungible tokens on Bitcoin for the first time. See our full report, “BRC-20 Tokens: A Primer.” While initial excitement followed the launch of inscriptions and BRC-20s, the market cooled briefly. However, activity in these markets saw a significant revival in November. Total inscription volume rose 362% from October’s low, marking the highest monthly volume ever, exceeding 8.3 million. To date, inscriptions have generated over $140 million in fees—a welcome boost for miners, especially given Bitcoin’s historically low transaction fees and the upcoming halving, which will further reduce miner revenues.

Perhaps one of the most important impacts has been the surge of excitement and innovation sparked by inscriptions—both within and beyond the Bitcoin ecosystem. Many new builders have flocked to Bitcoin, existing projects are releasing updates faster, and a wave of new ideas is circulating within the Bitcoin community.

A recent example is Taproot Wizards raising $7.5 million in funding—an Ordinals project based on the famous “Bitcoin Wizard” meme. The impact of inscriptions and BRC-20s on transaction fees and Bitcoin network congestion has also reignited discussions around Bitcoin Layer 2 solutions (“L2s”).

Stacks and its upcoming sBTC solution—which aims to create a decentralized, non-custodial Bitcoin L2—are also interesting developments worth watching.

Overall, between the prospect of a spot Bitcoin ETF, the upcoming halving, and the innovation driven by Ordinals, it’s clear that Bitcoin is entering an exciting period in its history—one that deserves close attention.

6. Growth Among Alternative Layer 1 Protocols

Although Ethereum remains the dominant smart contract Layer 1 (L1) by most conventional metrics, alternative L1s have shown promise over the past year.

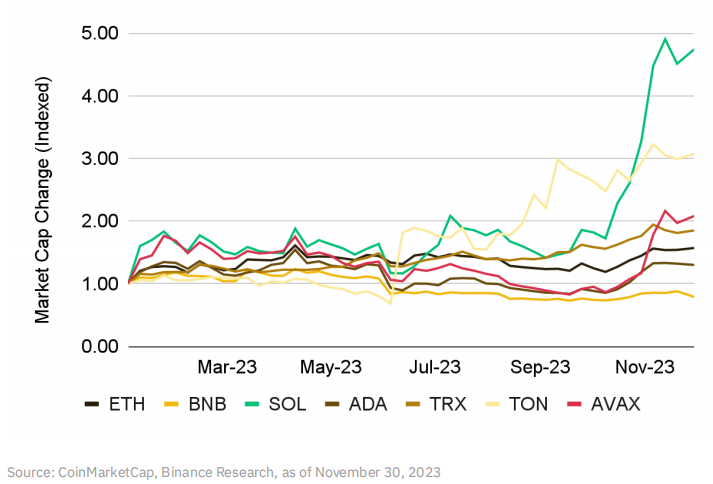

Solana has recently performed exceptionally well, with $SOL’s market cap increasing by approximately 56% in November.

After being impacted by the FTX collapse in 2022, Solana successfully navigated the crisis and continued releasing new products and improvements, fostering renewed optimism. Despite network outages in 2022, only one occurred in 2023 (in February). With the upcoming release of Firedancer—a new independent validator client—such incidents are expected to decrease further.

Solana has also performed well in DeFi, with TVL growing 57% from $418 million to over $650 million. This was driven by activity and attention from airdrops on Pyth Network, Jupiter Exchange, and Jito Network. Additionally, several other major DeFi projects introduced points systems, where user activity earns points that may factor into future potential airdrops.

Toncoin has also performed strongly, with its partnership announcement with Telegram being a recent highlight.

Announced in September, this collaboration means Telegram will fully rely on TON as its Web3 blockchain infrastructure, and TON Space—a self-custodial Web3 wallet—has already been integrated into all 800 million of Telegram’s monthly active users. Furthermore, TON projects and ecosystem partners will benefit from in-app promotion within Telegram and priority placement on its advertising platform.

Recently, Animoca Brands, a major gaming/metaverse VC firm, announced an investment in the TON Foundation and became one of the largest validators on the TON chain.

Other major L1s have also seen numerous announcements and developments. Ethereum successfully implemented post-Shanghai withdrawals of staked ETH, becoming a largely deflationary asset and fostering a large DeFi market in areas like liquid staking and LSDfi.

BNB Chain continues expanding its ecosystem, notably with the announcement of BNB Greenfield—a next-generation data storage platform—and opBNB, an optimistic Layer 2 built on OP Stack.

Avalanche continues announcing partnerships in gaming and RWA sectors. Its collaboration with J.P. Morgan Onyx and Apollo Global is a recent noteworthy initiative.

Cardano continues working on scaling efforts, including Hydra development and its upcoming privacy-focused sidechain Midnight.

Tron remains the largest chain for $USDT issuance and continues serving as an efficient method for users and enterprises to send $USDT payments.

7. Emergence of SocialFi

Social media apps have long been seen as natural candidates for integration with blockchain technology and cryptocurrencies. In 2023, product-driven growth in this corner of the crypto economy drew attention—particularly friend.tech.

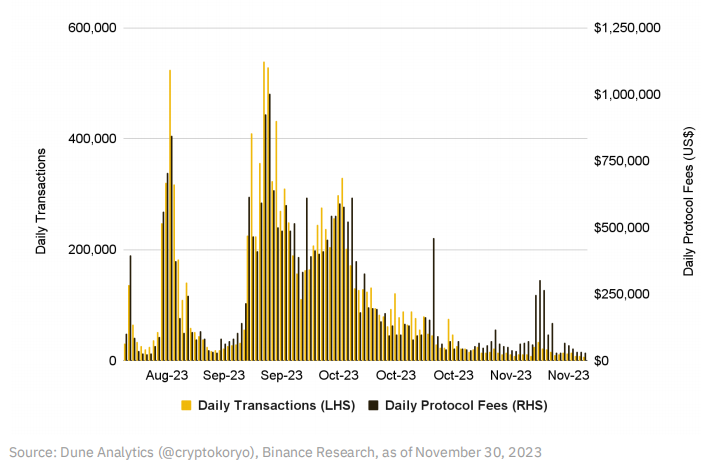

friend.tech is a SocialFi dApp that first launched in early August on Base, an Ethereum L2. It allows users to trade tokenized shares of Twitter profiles (called “Keys”). Holding a Key grants access to exclusive content and private chat rooms with the profile owner (referred to as “Subjects”). Users pay transaction fees, part of which go to the protocol and part to the Subjects.

Since launch, friend.tech has generated over $25 million in total protocol fees. It also runs an activity-based points system, rumored to be linked to a potential future airdrop. Although it generated considerable hype during August and September, daily activity has slowed over the past two months.

Nonetheless, the product remains in testing phase with a full launch upcoming. Perhaps most importantly, friend.tech managed to attract widespread attention—even from non-crypto influencers—demonstrating the potential reach of Web3 social applications.

friend.tech daily trading volume (LHS) and daily protocol fees (RHS)

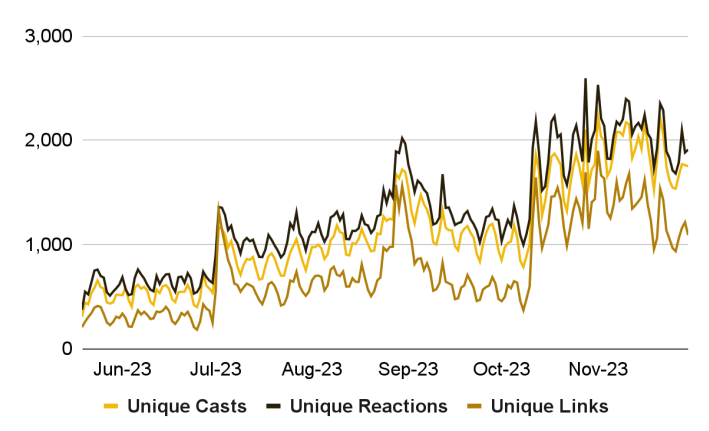

Another notable Web3 social app is Farcaster. Farcaster is a decentralized social protocol running on the Ethereum L2 OP Mainnet.

In October, the protocol opened registration without requiring invitations (moving beyond invite-only access), since when daily engagement has surged. Farcaster aims to foster a community-oriented platform with high-quality discussions. To that end, it recently hosted an AMA series featuring prominent guests including Balaji and Vitalik Buterin.

Farcaster's unique daily interactions have steadily increased since opening permissionless registration in October.

Another noteworthy Web3 social platform is Lens Protocol, which continues evolving. Built by the Aave team and deployed on Polygon, Lens shows strong interest in NFTs and caters largely to creators and artists.

After its initial launch in 2022, it announced its v2 version earlier this year. New features include “Open Actions,” enabling external smart contracts to be embedded in Lens posts, improving value-sharing opportunities, and a suite of new profile-related upgrades (“Profiles V2”). The launch of BN Square is another notable event, providing crypto users a new platform to exchange views and track breaking news.

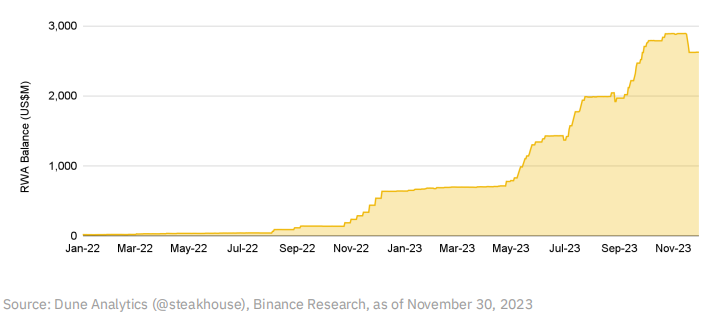

8. RWAs Enter the System

Real World Assets (RWAs) refer broadly to physical-world assets that are tokenized and purchased on-chain. Examples include real estate, bonds, commodities, stocks, etc. While the idea of tokenizing assets and bringing them on-chain has been discussed for a long time, 2023 has seen some particularly compelling moves.

MakerDAO

Maker, the protocol behind the DAI stablecoin, has been involved with Real World Assets (RWAs) since at least 2020 and saw significant expansion in 2023.

In brief, Maker allows users to deposit collateral into vaults and draw debt denominated in DAI. While initially only ETH was accepted as collateral, this has expanded to include stablecoins, wrapped BTC, liquid staking derivatives (LSDs), and more.

Maker also provides DAI loans backed by RWA collateral to borrowers approved via MakerDAO governance. Borrowers include institutions like Huntingdon Valley Bank, which has a $100 million RWA-backed lending vault with Maker.

Now, RWAs account for over 49% of Maker’s balance sheet—up from just ~12% at the start of the year. A significant portion of these RWAs consists of U.S. Treasuries, which have yielded high returns in the rising interest rate environment over the past 18 months. This means RWAs now contribute to over 60% of Maker’s income, and Maker’s own revenue reached an all-time high of over $200 million annually by early November.

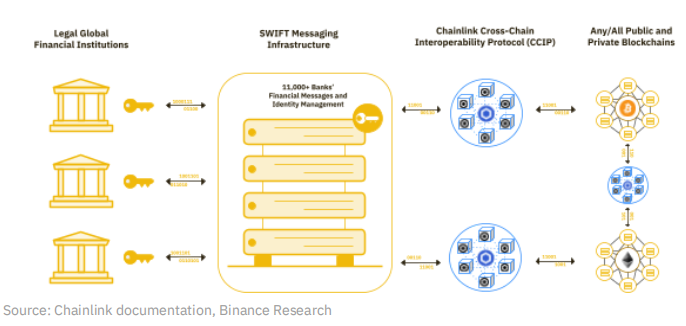

Chainlink and CCIP

Chainlink, best known for its oracle network, is a web3 infrastructure company offering a suite of solutions including Data Streams, Functions (for connecting smart contracts to APIs), Automation (smart contract automation), and more.

The Cross-Chain Interoperability Protocol (CCIP) is a notable new development. CCIP is a decentralized cross-chain messaging/data transfer protocol designed to create a shared global liquidity layer, enabling all chains—public or private legacy financial networks—to interconnect. Chainlink envisions CCIP as a bridge between traditional finance and crypto, enhancing interoperability between these worlds. Closer integration of RWAs into blockchains is a natural part of this process.

A key advantage of CCIP is that it allows users to define their targets using existing APIs and messaging services, connect via CCIP, and execute on-chain transactions. A significant integration already established is with Swift, the messaging service used by over 11,000 traditional financial institutions globally. With Swift able to communicate via CCIP, friction for traditional finance connecting to blockchains is reduced, potentially accelerating RWA integration.

We’ve already seen the early-access mainnet launch of CCIP (version 17), with further developments expected in the coming weeks. Notable case studies include ANZ Bank, with more major banks like Citi and BNY Mellon also exploring CCIP. Which institutions adopt CCIP in the coming months will be a key development to watch.

9. ZK-Everything

Growth in zero-knowledge ("zk" or "ZK") technology has long been a persistent theme in crypto. However, 2023 saw compelling ZK-related momentum, including the launch of multiple ZK rollups.

Key developments:

In short, there are two types of L2 rollup solutions: optimistic and ZK. While optimistic rollups currently dominate most of the L2 market share, ZK rollups are growing rapidly and widely seen as the future of scaling due to their reliance on zero-knowledge proofs (ZKPs)—an extremely efficient method of proving transaction validity with diverse applications across crypto.

Until this year, one reason ZK rollups were less popular than OP rollups was their poor compatibility with the Ethereum Virtual Machine (EVM). Given EVM is the dominant smart contract engine in the market, early ZK rollups lacked easy EVM support, giving optimistic rollups an edge (due to EVM compatibility). However, zkEVMs changed this. zkEVMs are special ZK rollups that allow smart contracts to be easily deployed on EVM-compatible environments, enabling developers to migrate EVM dApps seamlessly onto zkEVMs.

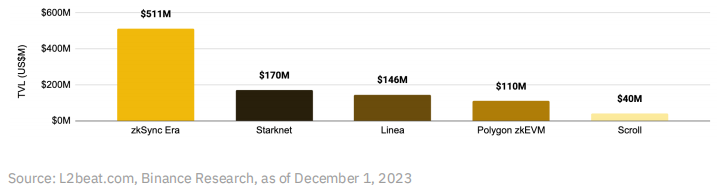

2023 saw the launch of many zkEVMs, starting with zkSync Era and Polygon zkEVM in March, followed by Linea and Scroll. StarkNet, another ZK pioneer, operates a production ZK rollup, and Kakarot zkEVM brings EVM compatibility to StarkNet tech. Taiko is another zkEVM expected to launch early next year.

In recent months, growth among Rollup-as-a-Service (RaaS) providers has also been strong. While many initially focused on optimistic rollups, the zkRaaS segment is growing, with companies like AltLayer, Gelato, and Lumoz emerging as key players to watch. This could lead to more ZK rollups entering the market over the next year.

TVL of the top ZK-rollups

Beyond rollups, there are many other applications of ZK technology. A significant upcoming example is the ZK coprocessor.

ZK coprocessors are tools that offload data-intensive and expensive computations off-chain. They reduce gas costs for dApp users while enabling more complex functions and computations, improving user experience. Even with some computation moved off-chain, dApps can still benefit from Ethereum’s full security.

In Web2, many apps shape user experiences by capturing behavioral data, whereas Web3 dApps are limited by the cost of storing data and running queries on-chain. ZK coprocessors unlock the potential for a new generation of Web3 dApps, with use cases including on-chain gaming, DeFi loyalty programs, dynamic incentive schemes, digital identity, and KYC.

The recent launch of Succinct, a new ZK protocol, is also an interesting development.

Succinct offers developers a platform to discover, collaborate, and build applications using ZK technology. As part of this platform, developers can leverage the Succinct Protocol—an infrastructure layer designed to make ZK development more coordinated and seamless.

A notable recent partnership is with Avail, a data availability solution. Other upcoming partners include Lido and Celestia.

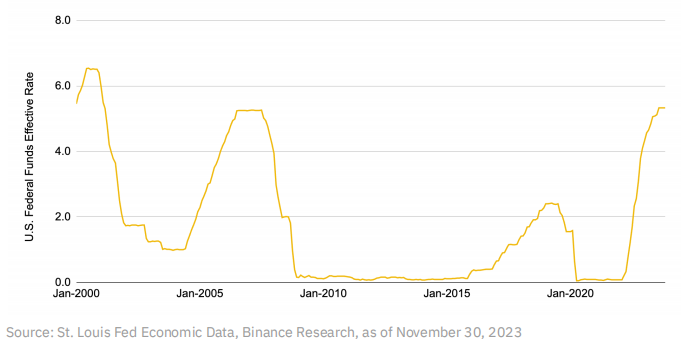

10. Are Interest Rates About to Fall?

From a macroeconomic perspective, interest rates are one of the most important factors affecting asset valuations. In the U.S., for instance, the higher the benchmark rate set by the Federal Reserve, the higher the risk-free return investors can earn simply by investing in ultra-safe government bonds. This naturally reduces interest in more volatile options like tech stocks and cryptocurrencies, as investors can achieve solid capital returns from government instruments.

U.S. interest rates are at their highest level in 22 years—one of the fastest hiking cycles in American history.

The Fed kept benchmark rates at 0–0.25% post-pandemic to stimulate spending, but with inflation rising rapidly, it conducted an unprecedented 11 rate hikes—from 0–0.25% in March 2022 to 5.25–5.5% by July 2023. However, in the last two Fed meetings, rates were held steady. Though inflation remains above the Fed’s 2% target (3.2% in October 2023), it’s a clear improvement from 2022’s 5–8% levels.

Latest Fed projections indicate declining rates in 2024 and 2025, suggesting rates may have peaked or are near peak. Other countries have already begun cutting rates—China’s central bank has lowered reserve requirements twice and reduced its one-year loan prime rate. Declining inflation in Europe has also led investors to expect earlier ECB rate cuts.

While only one piece of the macro puzzle, with global easing underway, investors will need to look beyond government bonds for yield. This will impact high-growth sectors like tech and crypto. At minimum, this presents a positive backdrop for crypto, alongside ongoing developments across Web3.

III. Conclusion

The past few weeks have been exciting—a welcome shift after months focused purely on building. As noise increases and new participants enter the market, things are getting wilder. It’s more important than ever to track the right metrics and focus on what truly matters. This report aims to serve as a starting point for the most important narratives and data points to watch in the months ahead.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News