MEV Value Breakdown: Technological Innovation, Market Scale, and Investment Insights

TechFlow Selected TechFlow Selected

MEV Value Breakdown: Technological Innovation, Market Scale, and Investment Insights

This article will provide a detailed introduction to the development of the MEV industry and potential opportunities.

Authors: Michael & Serein

Recently, Flashbots (MEV-Boost), an Ethereum infrastructure project, raised approximately $60 million at a $1 billion valuation. The funding round was backed by VCs, Layer 2 projects, angel investors, DEXs, and participants across the MEV supply chain.

MEV permeates the entire block production process. As a market derived from critical public blockchain infrastructure, the OP Crypto team has been closely tracking multiple projects in the MEV space. This article details our perspective on the development and potential opportunities within the MEV industry.

Origins of the MEV Market

MEV holds different value propositions for various stakeholders, but it is commonly understood as Maximum Extractable Value—the profit validators can extract by adding, removing, or reordering transactions within a block when proposing it to the chain. We can conclude that MEV inevitably exists due to the manipulatable nature of transaction ordering during block production. We will elaborate on these relationships later.

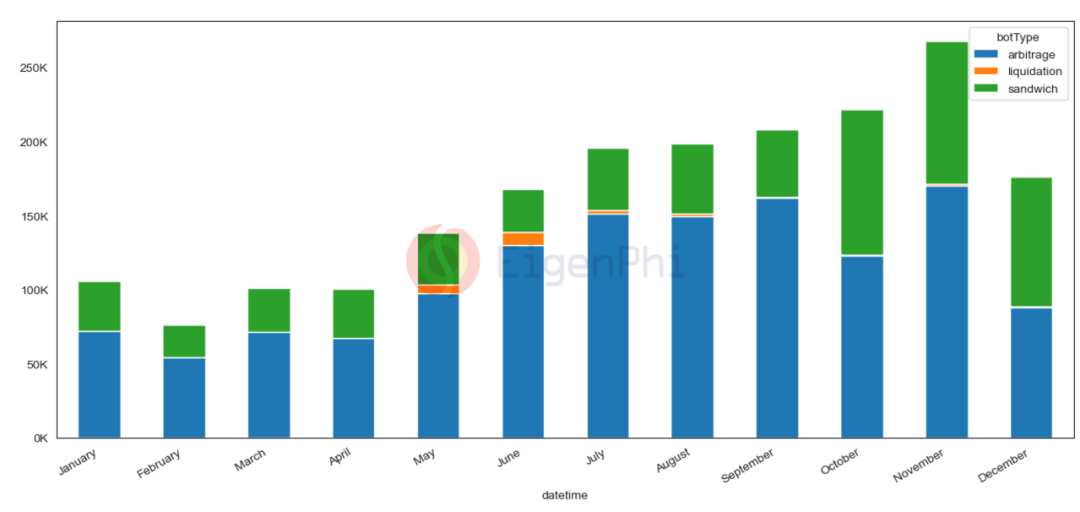

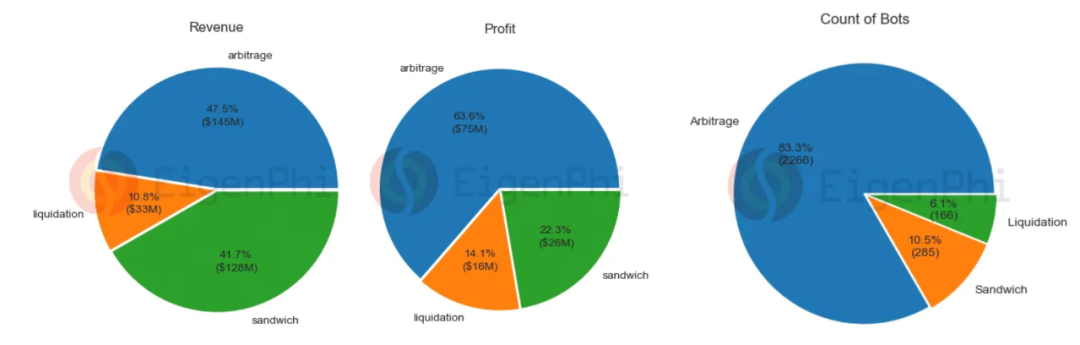

Consequently, MEV has given rise to several revenue-generating strategies, primarily arbitrage, sandwich attacks, and liquidations. According to Eigenphi’s data on MEV transaction frequency in 2022, arbitrage accounted for about 68% of transactions on average, while sandwich attacks made up around 30.6%.

Mechanisms behind the three types of MEV:

It's evident that arbitrage and liquidation are forms of MEV that help maintain on-chain market equilibrium, whereas sandwich attacks represent unfair trading practices that exploit users’ transactions.

MEV presents both benefits and drawbacks. For example, arbitrage enhances DeFi efficiency by enabling searchers to quickly eliminate price discrepancies. However, sandwich attacks degrade user experience through increased slippage and network congestion, as attackers often raise gas fees to secure priority transaction inclusion.

The Relationship Between Ethereum Block Production and MEV

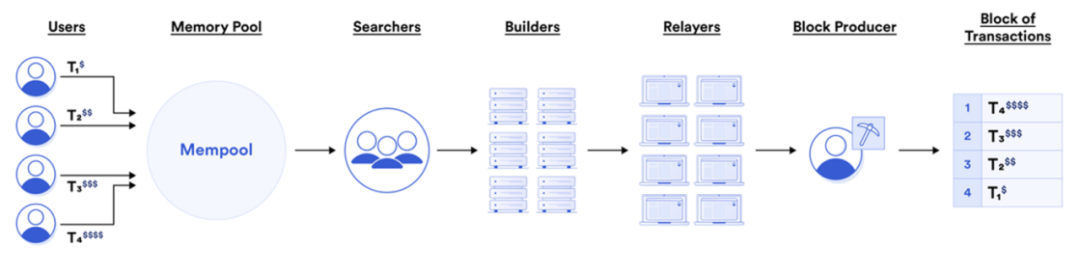

In Ethereum’s PoW era, key MEV participants were searchers and miners, with miners capturing the majority of MEV revenue—many of whom also acted as searchers. Since The Merge, changes in block production (separation of execution and consensus layers) and validator diversity (e.g., liquid staking) have reshaped Ethereum’s MEV ecosystem under PoS. Post-Merge Ethereum block production works as follows:

Even so, the transaction ordering process remains insufficiently decentralized: although transaction sequencing appears jointly determined by the execution and consensus layers, the same entity constructs and validates the block—and thus controls transaction order.

MEV Market Size

Revenue Perspective

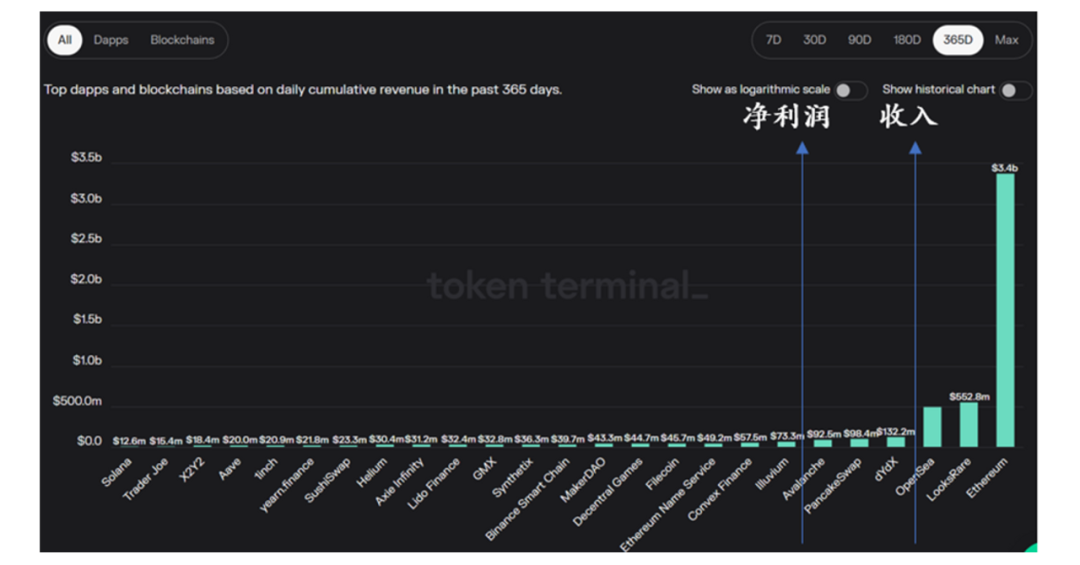

In 2022, 2,717 MEV bots generated approximately $300 million in revenue for the MEV market, with arbitrage gross margins reaching as high as 52%. In terms of revenue scale, this ranks just behind leading platforms like OpenSea and LooksRare.

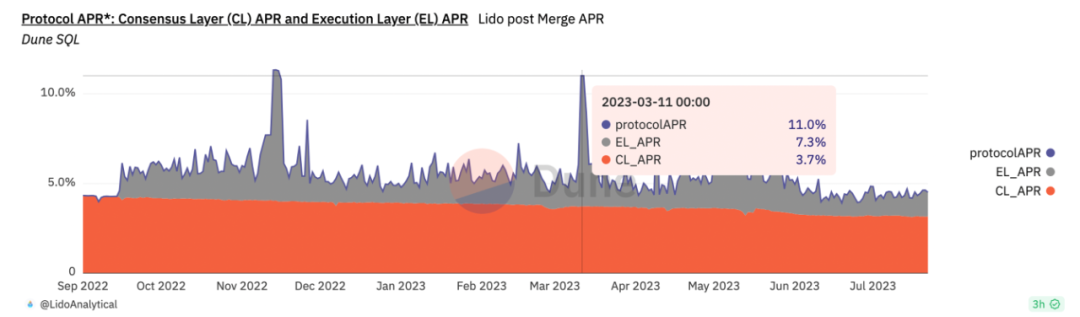

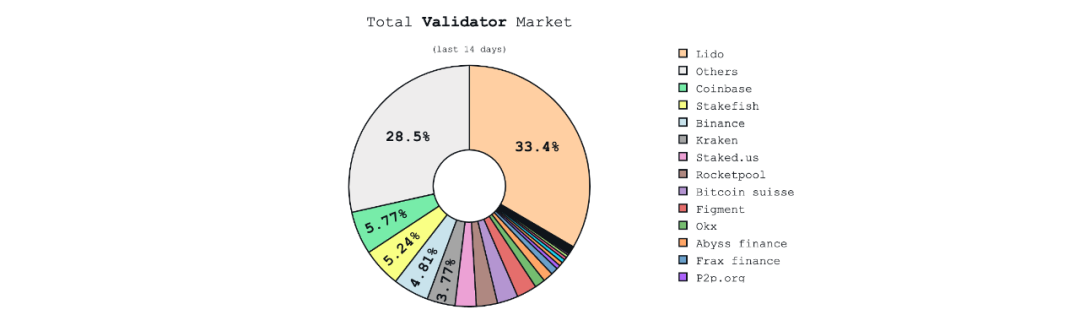

Take Lido DAO’s execution layer APR as an example: MEV income constitutes the main component, accounting for roughly one-third of stETH’s total revenue. During periods of high on-chain activity, MEV has contributed nearly 70% (as of March 11, 2023).

Therefore, we can infer that during bull markets, MEV income could continue to account for up to 70% of staking revenue. At such times, the MEV market’s income level becomes comparable to that of the LSD market.

Volume Perspective

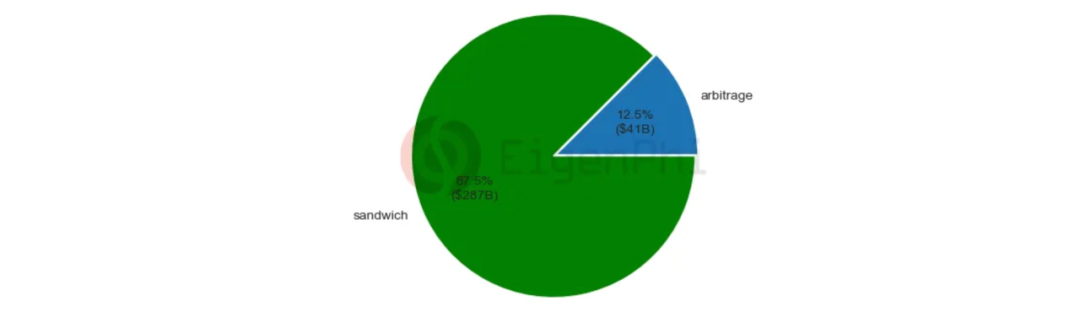

From a volume standpoint, sandwich attacks generated $287 billion in trading volume in 2022, significantly surpassing arbitrage’s $41 billion and representing 87.5% of total MEV volume—rivaling the annual trading volumes of top-tier DeFi protocols.

In terms of on-chain transaction scenarios, MEV contributes significantly to trading volume on leading DeFi platforms:

MEV Value Chain and Industry Landscape

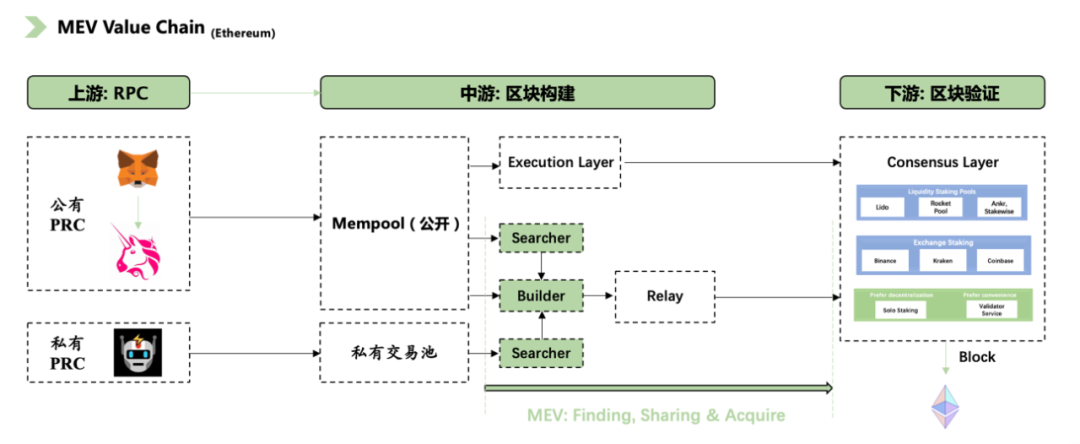

Based on Ethereum’s current block production framework, we outline the MEV value chain as shown below:

1. Upstream

Primarily consists of RPC providers who handle signing and broadcast transactions from local nodes to the network.

2. Midstream

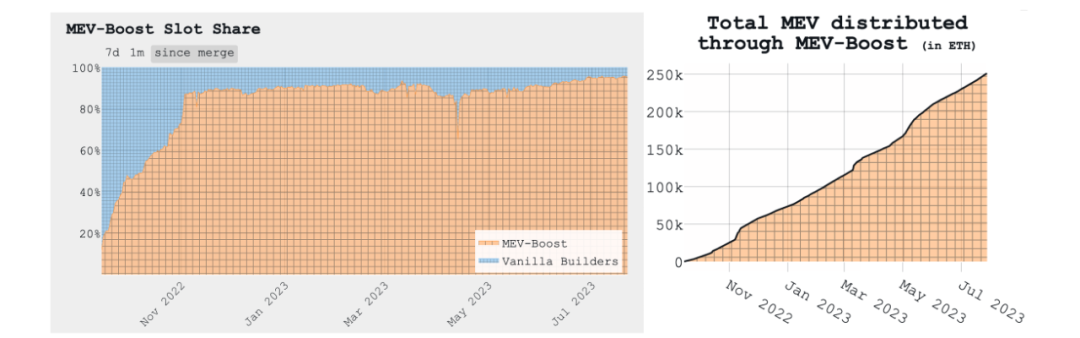

This stage involves block building (transaction ordering) in either public or private environments, identifying MEV opportunities, and determining MEV revenue distribution. The dominant solution remains Flashbots MEV-Boost, which commands around 90% of Ethereum slot share. Since its launch less than a year ago, MEV-Boost has captured over 250k ETH (~$469 million at current prices) in total MEV revenue.

The relay model theoretically separates Builders from Validators. However, in practice, this means consensus-layer Validators do not participate in bundle bidding and struggle to capture MEV revenue. Yet, as noted in the “Market Size” section, Lido’s execution-layer returns are largely driven by MEV—indicating that PBS under Flashbots has not been effectively implemented.

Examining midstream stakeholders reveals that mining pools, LSD participants, and others are deeply embedded in MEV capture, with MEV income forming a significant portion of their total revenue. Conversely, as long as MEV opportunities exist, stakeholders will continue participating via low-cost methods.

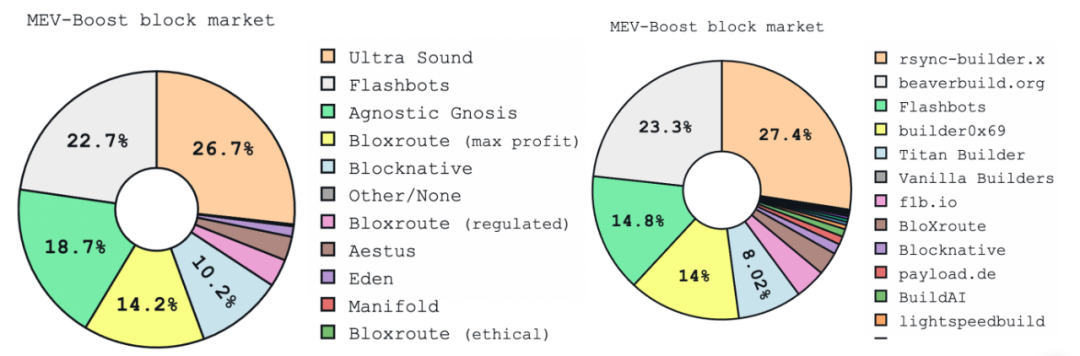

Left: Relay participant landscape; Right: Builder participant landscape

3. Downstream

Responsible for proposing (validating) new blocks, ensuring user transactions and MEV-extracting transactions gain network consensus and ultimately generate MEV revenue. Validators originate from CEXs, liquid staking providers, institutional stakers, or individual stakers. With emerging mechanisms in liquid staking—such as DVT-based staking pools—the downstream landscape may evolve, though we won’t delve into that here.

Solutions Overview

1. Flashbots

Flashbots is a research and development organization focused on mitigating negative externalities caused by MEV (e.g., network congestion). It has launched several products, including Flashbots Auction (with Flashbots Relay), Flashbots Protect RPC, MEV-Inspect, MEV-Explore, and MEV-Boost. Here, we focus on Auction (MEV-Geth) and MEV-Boost.

-

MEV Auction

MEV Auction emerged during Ethereum’s PoW era, when MEV participants included searchers and miners. Flashbots Auction established a private communication channel between searchers and miners, enabling transparent and fair negotiation over transaction ordering and pricing.

The MEV Auction process works as follows:

-

Submit auction: Searchers package transactions into Bundles and submit them to Flashbots Auction, specifying a minimum price;

-

Miner bidding: Miners bid on desired Bundles within the auction system, setting their own minimum prices;

-

Block construction: Miners select one or more highest-bidding Bundles and include them in the block;

-

Settlement and execution: Transactions and Bundles in the block are executed according to the agreed-upon order and price from the auction;

The core advantage of MEV Auction lies in enabling coordination on transaction ordering. For searchers, it avoids costly gas wars and failed transaction fees. For miners, it allows substantial MEV revenue capture without needing to actively search for MEV opportunities.

With Ethereum’s transition to PoS, Flashbots introduced MEV-Boost.

-

MEV-Boost

Its core logic is outsourcing block-building from validators. Builders assemble blocks and relay them via relays to block producers (i.e., Ethereum validators), resulting in finalized blocks—commonly referred to as PBS (Proposer-Builder Separation).

The process works as follows:

In MEV-Boost, Builders must commit to not front-running, or face slashing—but this relies on trust.

MEV-Boost offers similar benefits to MEV Auction: fair and efficient transaction ordering and a market mechanism for MEV revenue distribution between searchers and validators. The key difference is that validators fully outsource block building, and the presence of Builders accelerates block creation, improving blockchain efficiency.

2. Shutter Network

Shutter Network is an open-source project leveraging threshold encryption via a Distributed Key Generation (DKG) protocol to prevent frontrunning on Ethereum. This protocol encrypts transaction data, making it impossible for attackers to discern specific details such as buy/sell intent, token pairs, or prices.

The process works as follows:

-

Key holders collaboratively generate a public key; only when N out of N key holders cooperate (N being the threshold) can the private key be reconstructed;

-

A batch of transactions is encrypted using the eon public key (broadcasted by Keypers to users);

-

Users verify the correctness of keys by checking whether all N Keypers submitted the same eon public key;

-

Users locally generate a batch ID and obtain an eon key;

-

N key holders use their respective private keys to decrypt the batch;

-

The decrypted batch is sent to L1/Rollup for validation;

At its core, Shutter functions as a DAO-governed platform for Keypers, using threshold encryption and DKG to encrypt the block-building process, ensuring transaction sequences remain hidden and unalterable before on-chain confirmation. However, Shutter’s approach could cost the MEV market at least $130 million annually. Similar solutions include Penumbra and Osmosis. The widespread adoption of such solutions depends heavily on integration with core blockchain layers, and we remain skeptical about their long-term profitability.

3. Chainlink FSS

FSS (Fair Sequencing Services) is Chainlink’s centralized transaction ordering solution designed to reduce negative externalities from MEV in smart contract systems. FSS does not alter existing blockchain architecture. It sequences transactions from smart contracts based on two fairness principles: causal ordering (via threshold encryption) and time-based ordering.

Where Is MEV Heading?

MEV-Boost has lowered barriers for searchers and builders. Searchers leverage powerful transaction identification algorithms and private order flow to create MEV opportunities, while builders possess block execution capabilities. Searchers embed part of their MEV profits into bids within bundles, allowing builders to simply select the most valuable bundles, package blocks, and relay them to earn revenue. This represents a more efficient block production model—but still falls short of full decentralization.

MEV currently faces several foundational realities:

1. PBS is enshrined in Ethereum’s roadmap, Uniswap leads resistance against MEV

As previously discussed, PBS implementation under MEV-Boost has been largely unsuccessful. Entities with block execution capabilities—liquid staking pools, institutions, or individuals—want a share of the MEV pie rather than just staking rewards.

Although PBS has been proposed for integration into Ethereum’s architecture, in the medium term, the market still demands MEV mitigation tools. DeFi protocols need to improve on-chain user experience to positively optimize their business models.

Recently, Uniswap launched UniswapX, employing a Dutch auction model to match supply and demand orders and concentrate liquidity. The core innovation of UniswapX is outsourcing transaction routing and aggregation to a new role called Filter. Filters work alongside Uniswap’s Router to accept and match orders. Filters can be aggregators, market makers, individuals—or even MEV searchers. Due to the bidding mechanism, traders’ potential MEV losses are compensated during the auction, internalizing Uniswap’s MEV value. In this sense, MEV achieves better value distribution within Uniswap, and searchers can contribute positively to user experience.

2. Numerous MEV solutions, limited profitability

The majority of MEV revenue goes to searchers and builders. Technical solutions like Flashbots have not achieved strong profitability. Indeed, precisely because Flashbots operates as a non-profit, it has become difficult for newer entrants to monetize.

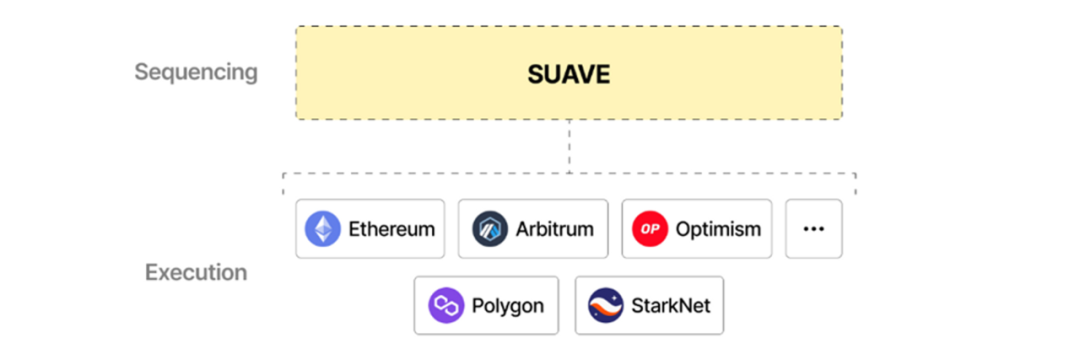

3. Cross-chain MEV extraction is becoming a trend

Ethereum’s current MEV gross profit margin no longer matches that of BSC. To maximize profits and cross-chain efficiency, single-chain Builders and Relays are bound to decline. New solutions like SUAVE aim to function as a standalone mempool and Builder chain serving other blockchains.

Given these trends, we believe the future MEV market will shift toward multi-chain extraction and lower ceiling revenues. Within sub-sectors, competition among searchers will intensify, demanding stronger order-flow access and algorithmic sophistication, while Builders will enter the MEV market at lower costs.

Conclusion

MEV is a rare foundational sector in blockchain characterized by strong cash flows, high transaction relevance, substantial revenue, and relatively low risk—though its scale fluctuates significantly with market cycles. From an investment perspective, since most MEV profits go to searchers and builders, the profitability of MEV-related protocol projects has become a challenge. We find few investment opportunities in new bidding systems or MEV protocols, and even for searchers, institutional investment avenues remain limited.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News