Y Combinator CFO: Key Things Startups Need to Know from SAFEs to Dilution

TechFlow Selected TechFlow Selected

Y Combinator CFO: Key Things Startups Need to Know from SAFEs to Dilution

At each stage of the company's lifecycle, you must know how many shares of the company you've sold to investors in order to determine how many shares you still own yourself.

Compiled by TechFlow

Note: This article is part of the TechFlow special series "YC Startup Course Chinese Notes" (updated daily), dedicated to collecting and organizing Chinese versions of YC courses. The sixteenth installment features an online course by Kirsty Nathoo, CFO of Y Combinator, titled "Understanding SAFE and Priced Equity Rounds."

My name is Kirsty Nathoo, and I'm the Chief Financial Officer and a partner at Y Combinator. I've worked with over 1,500 companies—from registration and participation in YC funding, to their subsequent fundraising through convertible instruments or equity rounds. This talk aims to uncover some lesser-known aspects of the fundraising process and help you avoid mistakes we’ve seen founders make.

At every stage of a company’s lifecycle, it's essential to understand how much of your company you're selling to investors—and thus, how much you still own. But this becomes complicated because most startups first raise money using convertible instruments, which don’t immediately issue shares. As a result, many founders aren't clear on exactly how much of their company they've already sold.

I’ll discuss these mechanisms so you understand how they work and can avoid being caught off guard later. Also, too many founders blindly trust their lawyers and ignore their cap tables—this is extremely dangerous. As CEO or founder, you must take responsibility for understanding these issues.

To track all shares and sales, you can use spreadsheets or tools like captable.io and Carta. I'll include these in a resource list after the presentation. This talk will be divided into three parts:

-

First, I’ll dive deep into SAFEs (Simple Agreements for Future Equity), since most early-stage companies raise funds this way;

-

Second, I’ll cover dilution, showing how ownership evolves from incorporation through priced equity rounds;

-

Finally, I’ll offer practical advice on fundraising.

SAFEs

A SAFE is a tool where an investor gives you money now, and in return, the company promises to give them equity at a future date. SAFE stands for Simple Agreement for Future Equity. Only two terms are typically negotiated: how much money the company wants to raise and the valuation cap at which the investor invests.

Compared to negotiating a priced round, SAFEs are easier to agree upon and faster to close. Unlike debt, SAFEs carry no interest rate and have no maturity date requiring repayment.

Because SAFEs change depending on future events, they’re a crucial instrument for any startup seeking early funding. Their structure is simple, written in plain language, short, and easy to understand.

Components of a SAFE

A SAFE consists of five main sections:

The first section covers what happens under various future events—such as an equity financing, a liquidity event, or if the company is acquired before the SAFE converts.

The second is the definitions section, clarifying key terms used in the agreement, such as the definition of the company’s capitalization.

The third section contains representations made by the company to the investor, including its jurisdiction and formation details.

The fourth section includes representations made by the investor to the company, such as confirming they are an accredited investor.

The fifth section contains standard legal boilerplate language, which should not be overlooked.

Overall, the first two sections are the most important, and the third is also worth understanding. I recommend reading the entire document carefully—especially the first three sections—to fully grasp the implications of your SAFE.

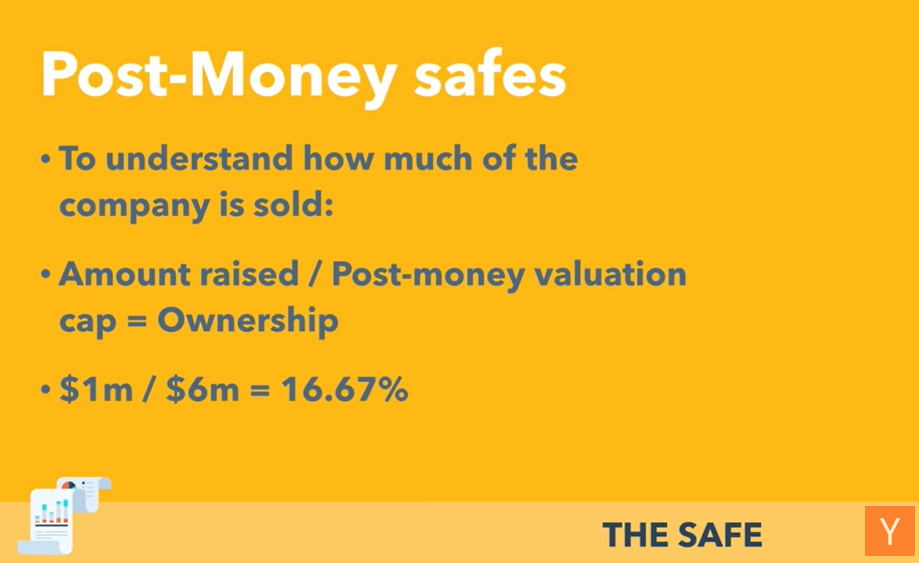

Post-Money SAFE

A post-money SAFE means the valuation cap applies after the new investment. Unlike traditional pre-money SAFEs, post-money SAFEs make it easier for founders to understand how much dilution they’re taking.

The purpose of introducing post-money SAFEs was to improve transparency. Both pre- and post-money SAFEs use the same pricing formula. For example, if the pre-money valuation is $5 million and you raise $1 million, the post-money valuation is $6 million.

With a post-money SAFE, you can easily calculate how much of your company you’ve sold: simply divide the amount raised by the post-money valuation cap.

For instance, in the above example, if an investor puts in $1 million against a $6 million post-money cap, they will own 16.67% of the company.

Variants of SAFEs

There are several common variations of the SAFE (Simple Agreement for Future Equity). Here are the main types:

-

Valuation Cap SAFE: This type sets a maximum valuation at which the investor’s SAFE will convert into equity. If the company’s valuation exceeds this cap during a future financing, the investor converts at the lower cap, receiving more shares.

-

Discount SAFE: This allows investors to convert their investment at a discounted price relative to the next priced round—for example, a 20% discount—giving them favorable terms upon conversion.

-

MFN (Most Favored Nation) SAFE: This ensures that if better terms are offered to future investors, the current SAFE holder gets those same improved terms.

-

Capped SAFE: This limits the maximum percentage of equity an investor can receive upon conversion, protecting the company from excessive dilution even if the valuation rises significantly.

Note that specific SAFE terms may vary based on negotiations between the company and investors. Customized SAFEs can be created to suit particular needs.

Dilution

Let’s assume a simple company with two founders who split the shares equally—each holding 4.625 million shares out of 9.25 million issued, meaning each owns 50%. They’ve completed the paperwork and received restricted stock subject to vesting via a Restricted Stock Purchase Agreement.

Next, the company raises funds using post-money SAFEs from two investors. Investor A invests $200,000 at a $4 million post-money cap; Investor B invests $800,000 at an $8 million post-money cap. Using the formula, Investor A owns 5% of the company, and Investor B owns 10%. So collectively, the founders have now sold 15% of the company.

Although the cap table hasn’t changed yet, the founders have effectively sold 15% of the company. This means they no longer own 100%—instead, their combined stake drops to 85%, diluted by the promised future shares.

Founders must be aware of this, because even though the cap table hasn’t updated, 15% has already been committed. You need to ensure you don’t sell too much early, as future rounds will cause further dilution.

Is everyone okay with the 15%? Yes. At this stage, only the founders are diluted—that’s how SAFEs are structured. Later SAFE investors don’t dilute earlier ones; they only dilute existing shareholders. At this point, the only existing shareholders are the founders and possibly a reserved pool for employees—these shares are now very valuable.

Why do they have different post-money caps? There could be many reasons, but let’s assume the investments happened one or six months apart, during which the company reduced its risk profile and thus negotiated a higher cap. Different caps reflect changing company conditions—just calculate each separately and sum them up.

Now, suppose the company raises $1 million. One of the first uses might be hiring employees and granting them equity—say, creating an option pool or employee incentive plan. In this case, they create a pool of 750,000 shares, issuing 650,000 to early hires. This changes the cap table due to additional shareholders.

Now there are 10 million total shares: founders hold 92.5%, and the option pool holds 7.5%. But the founders don’t actually own 92.5%—they’ve already sold 15% via SAFEs. So their real ownership is about 78.6%. Forgetting the SAFEs leads to miscalculating dilution.

If you forget the SAFEs, founders might mistakenly think they still own 92.5%. Always track how much you've sold via SAFEs to accurately calculate your true ownership.

Suppose a year later the company performs well, raises a priced round, expands the option pool, and brings in major investors who take 20%. The process involves three steps: converting SAFEs into equity, creating or expanding the option pool (if needed), then closing the new investment. It’s critical to perform these calculations in the correct order and use a cap table tool.

Finally, note the term “pre-money” in the context of SAFEs—it refers to how SAFE conversions are calculated when determining the Series A share price. During this calculation, we determine where the 15% from SAFEs goes and how it affects founder and employee ownership.

Founder Loss and Delta Value of Company Stock

Whether founders lose too much equity depends on the level of dilution—the delta value.

If the delta is small, founders won’t lose much. But if it’s large, it can become problematic.

In today’s environment, investors rarely price rounds below the SAFE valuation cap. Avoid convertible notes—they complicate calculations unnecessarily.

During fundraising and negotiations, understand what you’re selling and what investors care about.

Raised capital should fuel company growth—not be overly optimized in structure.

Adding an option pool and new investment requires complex calculations, including allocating 10% post-money shares and determining per-share price.

Use post-money SAFEs whenever possible and track dilution carefully. Don’t obsess over maximizing your valuation cap—it often makes less difference than you think. The ultimate goal is to use the funds to build a successful company.

Voting Rights and Board Structure

As part of the Series A term sheet, voting rights are a key consideration. Typically, voting power stems from board composition. If you want founders to retain majority control, the Series A agreement often reflects this. For example, with two founders, the board may include both founders plus one representative from the lead investor—ensuring founders maintain board majority and thus voting control.

Lead Investor

In a SAFE round, you don’t necessarily need a lead investor, as SAFEs simplify the investment process. Once an investor agrees to fund you, they just sign and wire the money. So for SAFEs, lacking a lead is fine.

However, in a priced round, having a lead investor is crucial due to the complexity of negotiations.

Negotiating with one investor is far more efficient than with many—especially when that investor commits significant capital. They often set the terms, and other investors follow. This streamlines the entire process.

Founder Ownership

How much equity should founders give up in the seed or SAFE round? Generally, we expect founders to retain over 50% ownership.

Most Series A rounds are priced. Investors typically expect around 20% ownership, with total dilution reaching about 25%. Additionally, factor in roughly 10% for the option pool. To maintain founder control, it's important not to give away too much early. In our example, we sold 15% via SAFEs.

Of course, every company is different. Sometimes, raising some money—even on suboptimal terms—is better than none. But proceed cautiously to ensure founders retain meaningful control.

Typically, SAFE dilution is around 15%, Series A investors take about 25%, the option pool ~10%, and founders retain the rest. When founders invest their own money, they can either loan it to the company or invest via SAFE. If they use a SAFE, they may receive Series A preferred shares upon conversion.

Ways Founders Can Invest and the Implications

First, consider what happens when founders invest their own money. Second, regarding how that money is treated, it should go into a SAFE—not a note. I dislike calling it a note because a SAFE is not debt. Remember this distinction, as it affects security and treatment. Another point: founders can handle personal investment in different ways. They could lend money directly to the company. For example, if they contribute $25,000 and raise $1 million from SAFE investors, the company can repay the founder later, or keep the funds in reserve. If kept in reserve, the founder might receive preferred shares, or in some cases, the SAFE could convert into Series A preferred stock. So you can choose the best approach based on your situation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News