LSDFi protocols become a key part of the LSD sector:盘点当下 6 个早期潜力项目

TechFlow Selected TechFlow Selected

LSDFi protocols become a key part of the LSD sector:盘点当下 6 个早期潜力项目

This article mainly introduces LSDFi protocols, which are concentrated in two categories: the first category consists of protocols that use LST as collateral in CDPs to mint USD stablecoins, and the second category consists of protocols that use LST as collateral in CDPs to mint WrapETH.

Author: Yuuki, LD Capital

After repeated hype, the LSD sector has gained significant market awareness and attention. The future growth of the LSD space is undoubtedly certain, but mainstream projects face limited marginal improvements. This high level of certainty means there's almost no meaningful expectation gap in the market to create high-risk-reward trading opportunities. At this stage, as the underlying LST (liquid staking token) yield-bearing asset base continues to expand, new LSDFi protocols built atop these assets will become the alpha within the broader LSD ecosystem.

This article primarily focuses on two types of LSDFi protocols: first, CDP-style protocols that mint USD stablecoins using LSTs as collateral; second, CDP-style protocols that mint wrapped ETH (WrapETH) using LSTs as collateral.

The rationale for focusing on these two product categories lies in the following:

-

As ETH staking rates continue to rise, the amount of liquid ETH decreases while the scale of LSTs expands accordingly;

-

Improving capital efficiency naturally drives growing demand for lending protocols using LSTs as collateral—especially when markets recover and risk appetite increases.

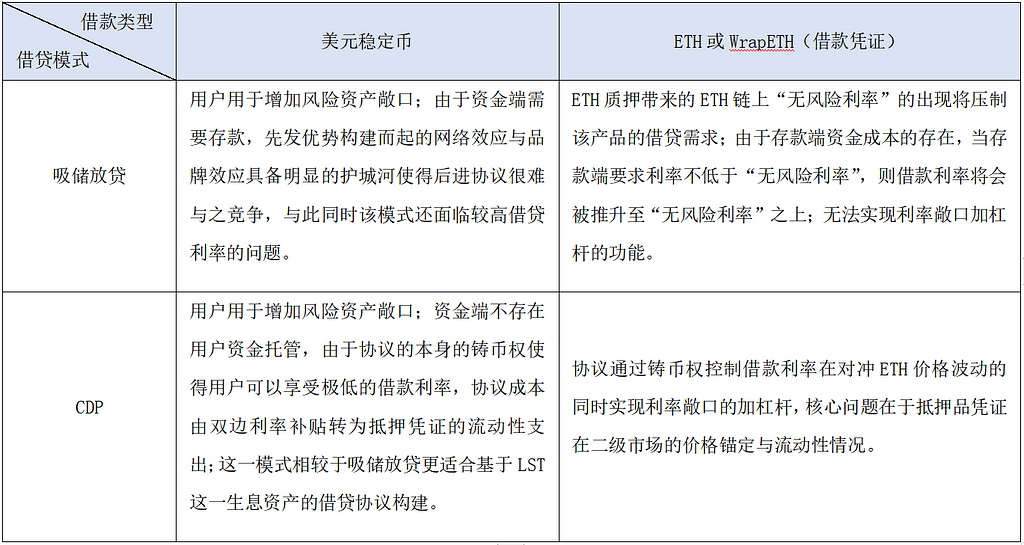

Lending protocols typically fall into two models:

-

One follows a deposit-and-lend model (e.g., Aave and Compound), which requires user deposits on the funding side. Early-mover advantages have created strong network and brand effects, forming clear moats that make it difficult for newer entrants to compete. Additionally, such models often suffer from high borrowing rates.

-

The other adopts a CDP minting model (e.g., Dai), where users do not deposit funds into a pool but instead generate loans through over-collateralized positions. The protocol’s inherent monetary authority allows users to access extremely low borrowing costs. Protocol expenses shift from bid-ask spreads to liquidity provision costs for the collateral tokens. This model is better suited for building lending protocols based on income-generating assets like LSTs—particularly for leveraged exposure to yield.

Source: LD Capital

All LSDFi projects discussed below are early-stage initiatives, with most still requiring ongoing monitoring regarding product planning, functional execution, and economic design.

Type 1: CDP USD Stablecoin Protocols Using LSTs as Collateral

1. Prisma Finance: Backed by Curve Ecosystem, Liquity Fork

Product Overview:

Prisma Finance enables users to over-collateralize LST assets to mint a USD-pegged stablecoin called acUSD. Initially supported collateral includes wstETH, cbETH, rETH, sfrxETH, and WBETH. The project has received backing from key DeFi figures including the founders of Curve and Convex, FRAX Finance, CoinGecko, and OKX Ventures. According to FRAX [FIP-227], FRAX Finance invested $100,000 at a $30 million valuation, with token allocations vesting linearly over 12 months.

Key Features:

Like most over-collateralized stablecoin protocols, Prisma Finance addresses the need for improved capital efficiency—allowing users to maintain price and yield exposure to their LST holdings while leveraging via CDPs to mint stablecoins. The liquidity of acUSD is critical here, representing both the primary cost for the protocol and one of Prisma’s key competitive advantages.

Economic Model:

Prisma incorporates a ve-token model. veTokens grant governance rights over token emissions distribution across lending pools, protocol fees, pool parameters, and LP mining yields. This aims to incentivize LSD protocols (as asset issuers) and liquidity providers to lock the native token, aligning incentives and reducing sell-side pressure in secondary markets.

2. Raft: User-Friendly, Censorship-Resistant, Doxxed Team, Built on Balancer for Liquidity

Product Overview:

Raft is an immutable, decentralized lending protocol allowing users to borrow a USD-pegged stablecoin R using LSTs (currently only stETH) as collateral. It maintains censorship resistance through immutable smart contracts and a decentralized frontend. Incubated by TempusFinance, its co-founder previously worked at the Ethereum Foundation, and team members developed Nostrafinance (the first lending product on StarkNet). Raft is backed by institutions including Lemniscap, Wintermute, and GSR. All core features are live, achieving $30 million TVL within three days of launch without any token incentives.

Source:https://www.raft.fi/, LD Capital

Key Features:

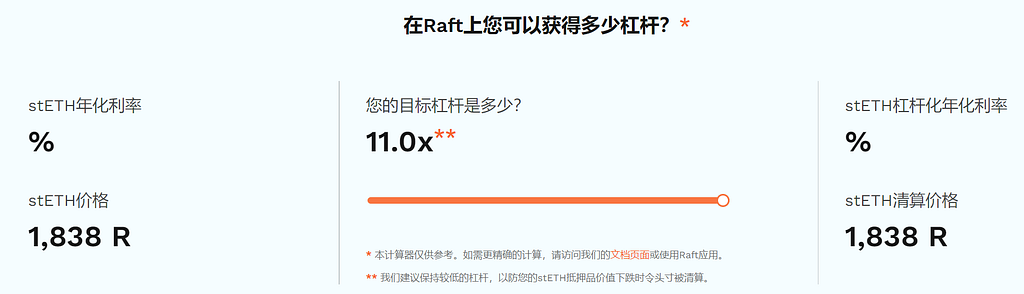

Notable features include instant swaps and one-step leverage functionality. Instant swap works similarly to Aave’s flash loans, except the R tokens originate from protocol minting. Building on this, the one-step leverage function bundles multiple steps—deposit stETH → instant swap for R → exchange R for more stETH → deposit additional stETH → mint more R → repay R flash debt—into a single transaction. This significantly improves user experience and reduces gas costs. Users can achieve up to 11x leverage.

Source:https://www.raft.fi/, LD Capital

Economic Model: Not yet disclosed

3. Gravita Protocol: Liquity Fork, CDP Stablecoin Protocol Accepting LST Collateral

Product Overview:

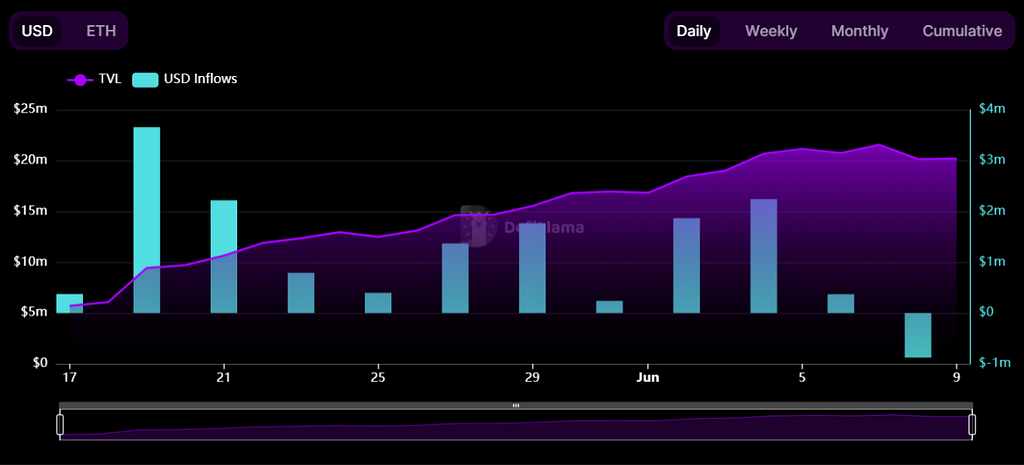

Gravita Protocol is the first Liquity fork supporting LST assets. Without offering token incentives, it reached $20 million TVL within one month of launch. Supported collateral includes WETH, stETH, rETH, and bLUSD. Its stablecoin GRAI enjoys solid liquidity depth on Curve, Bunni, and Uniswap V3.

Key Features:

Compared to Liquity, Gravita supports LST assets and offers lower borrowing costs. Borrowers pay a one-time 0.5% fee upon drawdown. If repaid within six months, part of the fee is refunded based on the loan duration, with a minimum charge equivalent to one week’s interest.

Source: Defillama, LD Capital

Economic Model: Not yet disclosed

4. PSY: Zero Borrowing Fee, Arbitrum-Based, ve(3,3) Model, Liquity Fork

Product Overview:

PSY allows users to mint a USD stablecoin (SLSD) using various LSTs and their LP tokens as collateral. Its architecture mirrors Liquity’s and is set to launch on Arbitrum.

Key Features:

PSY plans to offer zero-interest borrowing and implement a ve(3,3) token model. Further details remain to be seen and require continued tracking.

Type 2: CDP WrapETH Protocols Using LSTs as Collateral

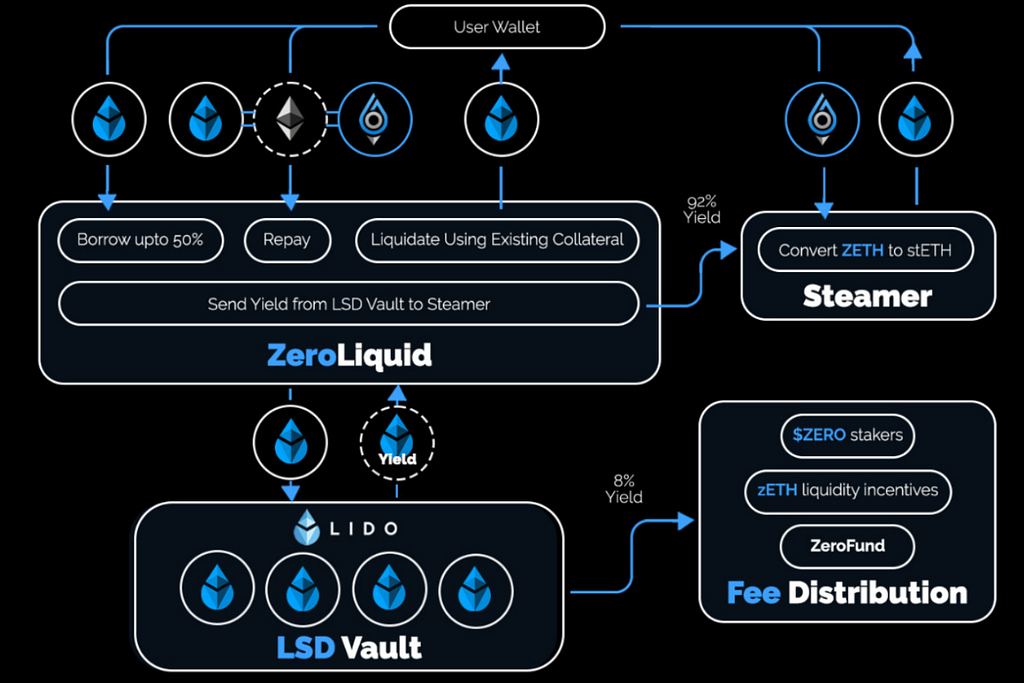

5. ZeroLiquid: Zero Borrowing Fee, No Liquidations, Interest Automatically Repays Debt

Product Overview:

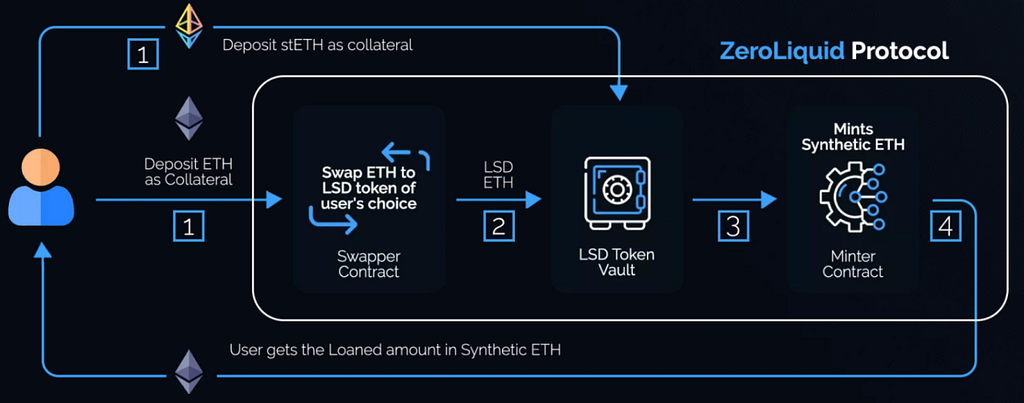

ZeroLiquid is currently on testnet and allows users to deposit LSTs to mint ZETH—a borrowing token pegged in value to ETH. When users deposit ETH, ZeroLiquid converts it into an LST (initial LTV: 50%). Since ZETH moves in tandem with ETH prices, excluding risks associated with the underlying LSD protocols (e.g., hacks or slashing events), ZeroLiquid can operate without liquidations. It effectively hedges price volatility while enabling long exposure to ETH staking yields. Initially, the protocol intends to take 8% of LST yield as revenue, adjustable via governance later.

Source: zeroliquid.gitbook.io, LD Capital

Current challenges for ZeroLiquid include low LTV, relatively high protocol fees, and how ZETH maintains its peg. While LTV and fees can be adjusted via governance, the main issue remains ensuring ZETH’s price stability. In ZeroLiquid’s economic model, liquidity incentives account for only 20% of total token supply (relatively low), meaning a robust redemption mechanism is essential to stabilize the ZETH/ETH exchange rate.

Currently, ZeroLiquid uses a “Steamer” module to provide liquidity for arbitrage in secondary markets when ZETH trades at a discount. The Steamer’s liquidity comes from users’ excess collateral and accrued yield. This design significantly impacts the protocol’s achievable LTV, and improvements in this area are worth watching.

Source: zeroliquid.gitbook.io, LD Capital

Economic Model:

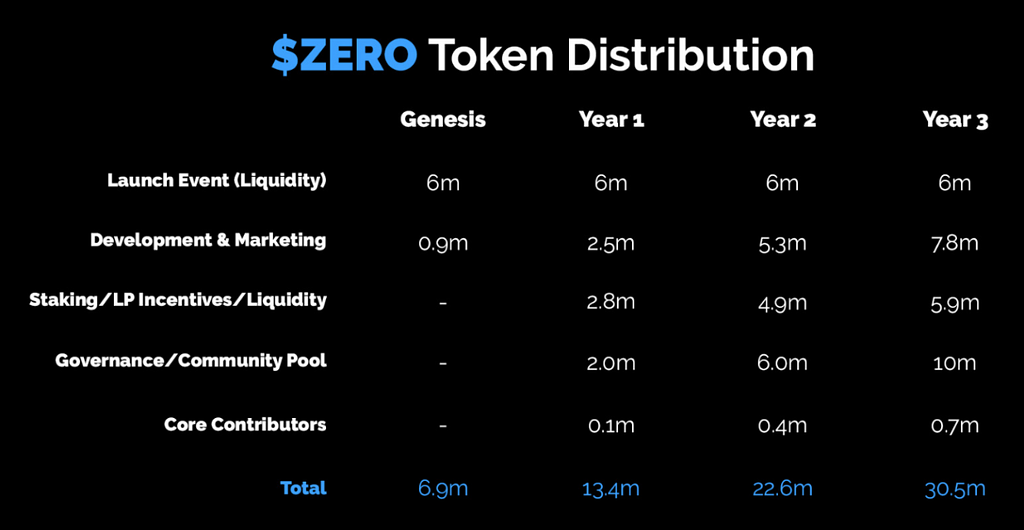

$ZERO was launched on March 19 via self-funded deployment on Uniswap, with a total supply of 30.5 million tokens (originally 100 million, followed by a community proposal burning 69.42%). Of this, 6 million were allocated for initial liquidity, 13.7 million to the community, 1 million to the treasury, and 700,000 to core contributors. Currently, 6.9 million tokens are circulating in secondary markets, with the remainder vesting over 3 months to 3 years. $ZERO grants governance rights and entitles holders to protocol revenue distributions—single-sided staking captures earnings directly.

Source: zeroliquid.gitbook.io, LD Capital

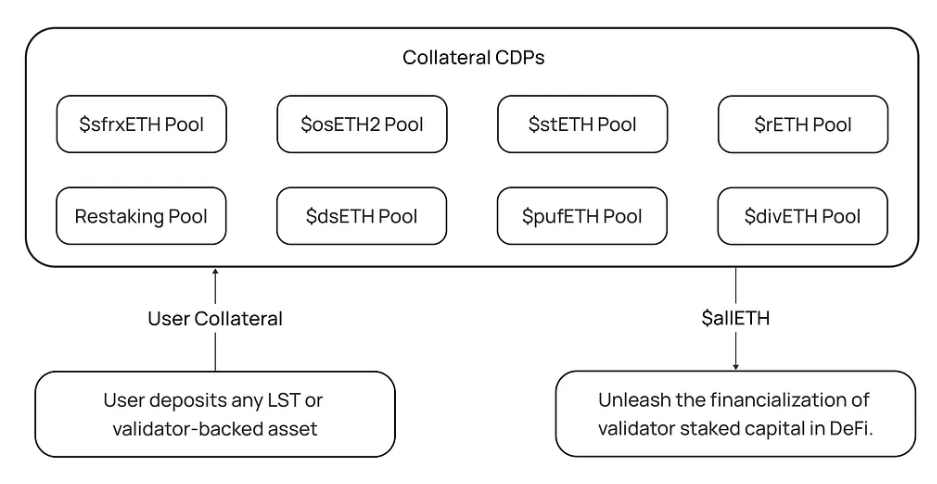

6. Ion Protocol: Zero Borrowing Rate, Supports EigenLayer Restaking Receipts

Product Overview:

Ion Protocol supports a wide range of collateral types, including LSTs, LST LP positions, staked LST LP positions, EigenLayer validator/LST/LST LP restaking receipts, and LST index products. The protocol plans to develop a customized risk model tailored to each collateral type’s unique risk-return profile. By adjusting LTVs or borrowing rates per asset class, Ion aims to guide deposit behavior, maximize capital efficiency, and ensure allETH remains over-collateralized and well-pegged.

Source: ionprotocol.medium, LD Capital

Economic Model: Not yet released

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News