What Lies Behind Frax Finance's frxETH v2 High Annualized Yield While Addressing Centralization Issues?

TechFlow Selected TechFlow Selected

What Lies Behind Frax Finance's frxETH v2 High Annualized Yield While Addressing Centralization Issues?

The frxETH v2 upgrade aims to address the centralization issue while maintaining the highest annual yield (interest) in the market.

The most frequently criticized aspect of Frax Finance's frxETH v1 in the past was that all nodes were operated by the team, resulting in excessive centralization.

Simply put, the update to frxETH v2 aims to solve this centralization issue while maintaining the highest annualized yield (interest) in the market.

As for how this will be achieved, we'll attempt to understand this upgrade by tracing through the protocol design logic later on.

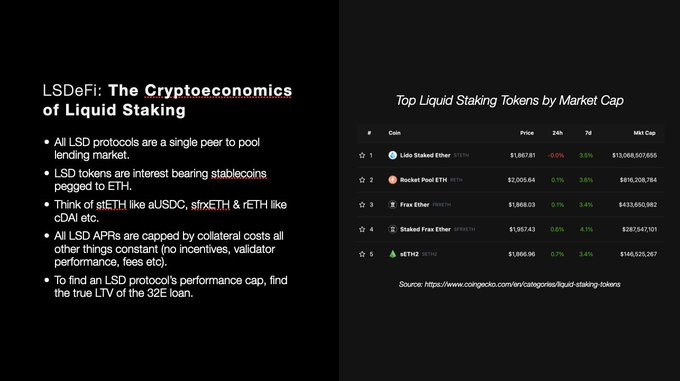

First, some background: Frax Finance founder Sam Kazemian believes that all LSD Protocols are本质上 just peer-to-pool lending protocols, where LSD tokens act as IOUs issued by the protocol when users deposit ETH into the pool. Each type of IOU differs in form—such as $stETH, a rebasing token, or $sETH, an index-growing token.

Unlike other LSD protocols, Frax Finance adopts a dual-token model based on stablecoin architecture as its conceptual starting point. The $frxETH token is a stablecoin pegged to ETH (and also serves as an IOU), but it does not bear interest distribution—it exists purely as a stablecoin. When this stablecoin is staked, it becomes sfrxETH, an ETH-yielding stablecoin.

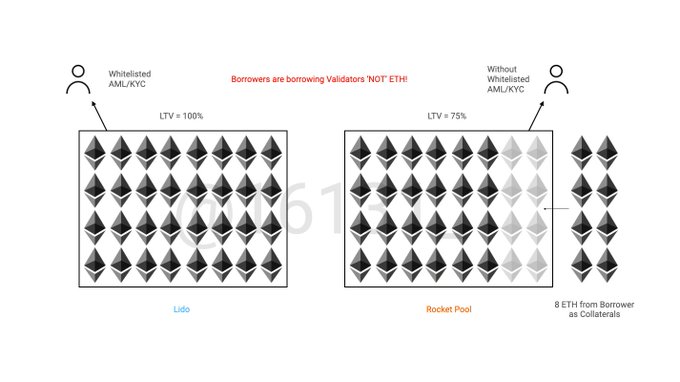

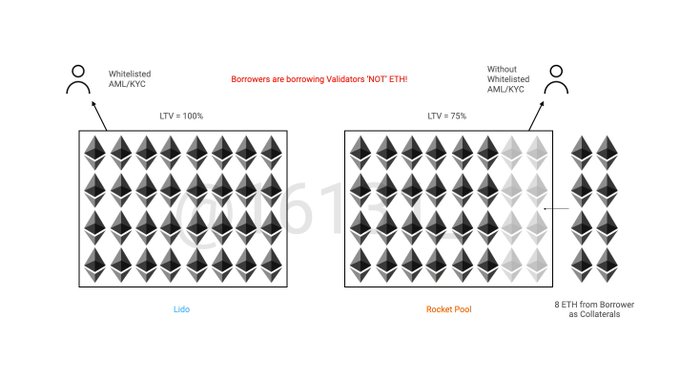

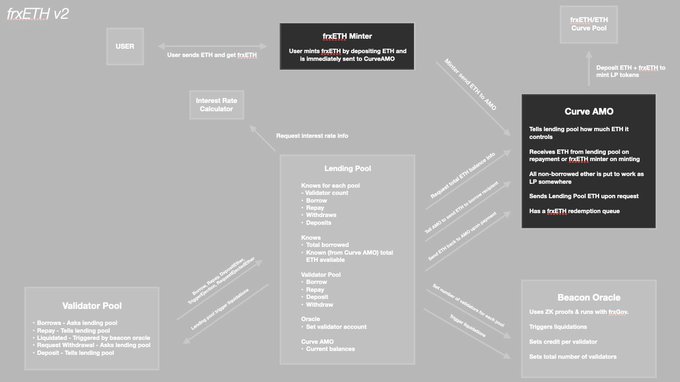

In frxETH v2, nodes do not "borrow ETH," but instead "borrow validators"—a somewhat abstract concept, differing from conventional understanding of LSDs. In protocols like Rocket Pool, nodes typically contribute 8 ETH and borrow 24 ETH to complete a full 32-ETH validator. In such cases, what is being borrowed is "ETH." But in frxETH v2, nodes act as borrowers who lend out "validators." See the illustration below.

We’ll use the two largest current protocols, Lido and Rocket Pool, to explain this concept.

Take Lido on the left as an example: if a node wants to borrow a validator, it must go through a whitelist, hence no collateral is required. This mechanism allows all ETH within the validator to come entirely from the Lending Pool, achieving an LTV = 100%, thus fully utilizing all funds.

What does LTV = 100% mean here?

I myself took some time to grasp this initially. Previously, my understanding of LTV was straightforward—for example, if I collateralize $100 worth of sfrxETH and can borrow up to $75 in Frax, then LTV = 75%. However, in the context of frxETH v2, LTV more closely means “what proportion of ETH within a validator is borrowed.”

If we interpret Rocket Pool’s mechanism using the frxETH v2 framework, refer to the right-side diagram: Node Operators (NOs) must first deposit their own 8 ETH to become “eligible to borrow a validator.” These 8 ETH are added to an existing 24 ETH in the validator to reach the full 32 ETH, resulting in LTV = 75%. For depositors (those earning interest), they only receive three-quarters of the validator’s revenue.

The ETH that NOs pledge themselves does not require them to pay rent to depositors. The trade-off is significantly higher decentralization compared to Lido. In other words, “decentralization itself comes at a cost”—a concept we’ll revisit later.

From the examples described above, we can see that a depositor’s APR is essentially the interest earned by depositing ETH into the pool—and simultaneously represents the cost for nodes to “borrow validators.”

Since this is fundamentally a lending mechanism, LTV naturally exists. All else being equal, the amount of interest a protocol can offer depositors fundamentally depends on the LTV ratio—i.e., how efficiently capital is utilized.

Frax Finance argues this is precisely why Lido can offer users higher annualized yields than Rocket Pool—the former has a higher LTV than the latter.

As mentioned earlier, frxETH v2 aims to address centralization, which necessarily involves paying a “cost for decentralization”—meaning LTV cannot reach 100%. Under this premise, we can view frxETH v2’s goal as creating a “more efficient version of Rocket Pool.”

So how can it achieve higher efficiency while preserving decentralization?

Frax Finance introduces the concept of free-market game theory here.

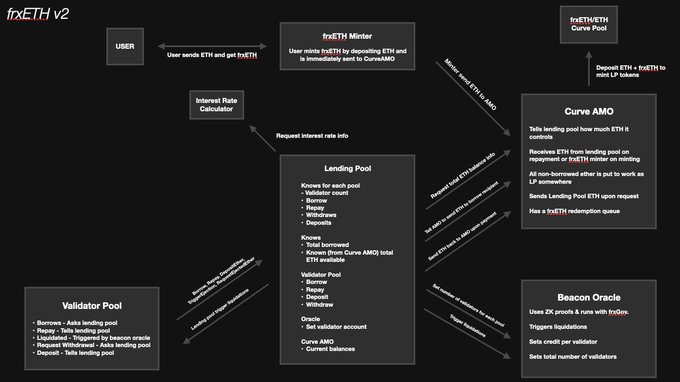

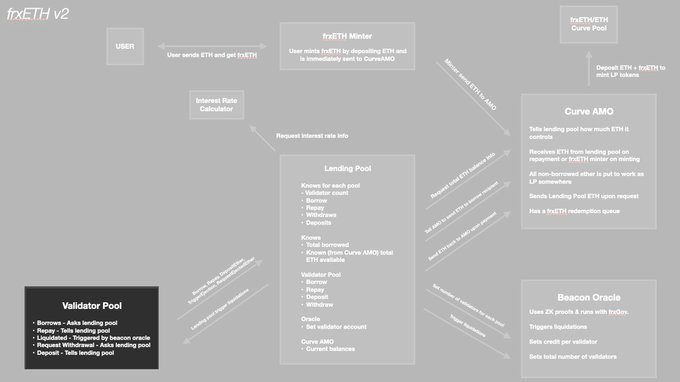

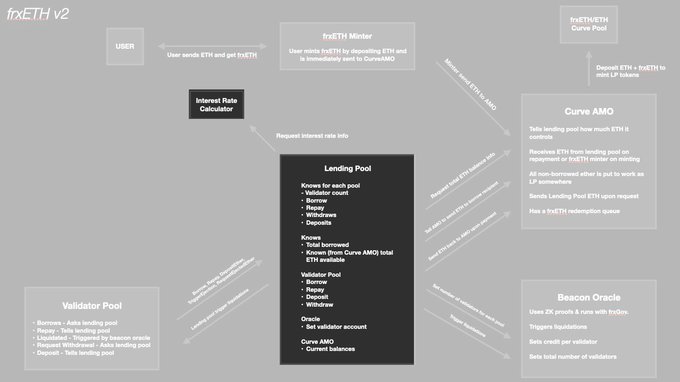

Next, I’ll walk through the design logic according to how frxETH v2 operates. First, when users deposit ETH into the protocol, they receive $frxETH—this is the function of the Minter shown at the top. Then comes the key part: the ETH is immediately sent to the Curve AMO, which subsequently allocates ETH into the Lending Pool as collateral for validators based on demand.

It’s important to clarify the relationships: deposited ETH does not go directly into the Lending Pool, but first passes through the Curve AMO. This improves overall efficiency because any ETH outside the Lending Pool can still earn yield and mining rewards (aka bribery incentives) within the Curve AMO, while also deepening the frxETH/ETH trading pair liquidity, enhancing user trading experience.

To implement this mechanism, we need to revisit frxETH’s “dual-token architecture.”

$frxETH is currently the only LSD token designed around a stablecoin concept. Precisely because it doesn’t bear interest payments, combined with Frax Finance’s substantial governance resources, it functions purely as a stablecoin within the Curve AMO—supporting user exits and maintaining price peg via the AMO.

Next, let’s introduce the Validator Pool. When NOs want to “borrow a validator” from the Validator Pool, they must post a certain amount of ETH as collateral. Using the same 8 ETH example as Rocket Pool (this number can be treated as variable X, determined by $veFXS voting—effectively allowing the protocol to control LTV size), collateral must be posted before borrowing a validator.

The Validator Pool requests 32−X (i.e., 24) ETH from the Lending Pool to complete the 32 ETH needed per validator. The key to achieving both Rocket Pool-level decentralization and higher efficiency lies in the “Interest Rate Calculator” located at the top-left corner.

Interest rates are determined solely by market forces and capital utilization, with no pre-set fees.

If borrowing a validator is cheap enough for NOs (i.e., income exceeds costs), they will proceed to borrow, pay interest to depositors, and strive to maximize MEV performance to boost their own profits—allowing high-performing nodes to self-select into the frxETH v2 ecosystem. Conversely, if the Interest Rate becomes too high, leaving little profit margin, NOs can simply return the validator, stop operations, reclaim their collateral, and wait until rates drop to a profitable level.

Allowing market dynamics to determine the optimal Interest Rate ensures frxETH v2 requires neither whitelists nor KYC, while continuously maintaining the most efficient nodes active in the network.

Although frxETH v1 was centralized, it was indeed the most operationally efficient player in the current market. In frxETH v2, the original team will also participate (in plain terms: compete from the start), helping push the efficiency of frxETH v2 to its maximum potential.

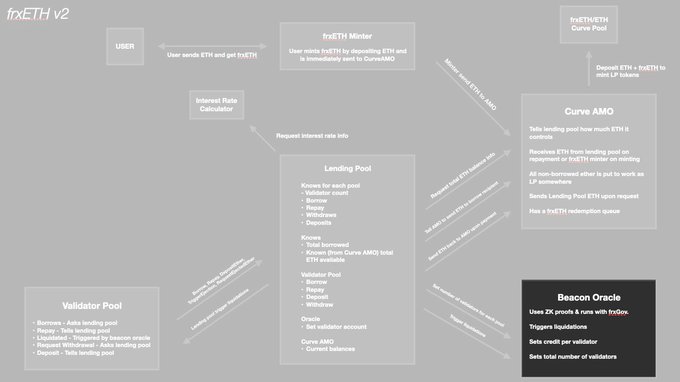

At this stage, similar to standard lending protocols, withdrawal addresses and all custody mechanisms are decentralized, fully on-chain, and non-upgradable. Interest is paid directly from cash flows generated by ETH + PoS rewards. Additionally, the Beacon Oracle achieves full decentralization via zk-proof technology, eliminating reliance on any admin keys, multi-sigs, or EOAs.

Sam Kazemian himself believes this mechanism has the potential to maintain—or even slightly exceed—the effectiveness of frxETH v1. We’ll need to observe its real-world performance once launched.

That covers everything! All explanations above are based on insights from Frax Finance founder Sam Kazemian. I find frxETH v2 relatively complex to grasp—I welcome corrections if anything is inaccurate.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News