What does a booming VC market mean for the future of cryptocurrency?

TechFlow Selected TechFlow Selected

What does a booming VC market mean for the future of cryptocurrency?

Traditional venture capital firms/investors cannot purchase Bitcoin or Ethereum, but they can acquire equity in organizations focused on cryptocurrencies.

By Zaheer Ebtikar

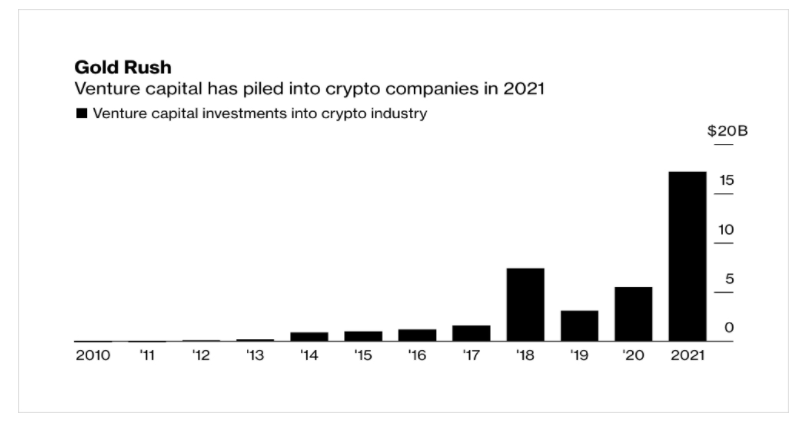

“___ has just closed another fund at ___ billion dollars, aiming to continue investing in cryptocurrency and Web3.”

If you’ve followed any kind of financial news over the past two years, you may have seen headlines like this week after week, month after month.

On the surface, this type of investment and capital allocation clearly signals value for a new industry and reaffirms a strong bid on cryptocurrencies.

However, as each investment firm raises and deploys funds into projects within this space, they are fundamentally overlooking one crucial thing. By examining early-stage traditional venture capital, drawing timely comparisons between the present and the past, and understanding the crypto market, we can explain venture capital firms’ implicit bets on future crypto asset prices.

The Early Days

To explore this further, we must first revisit the earliest days of modern venture capital and the state of emerging technologies and the internet at that time.

The “Dot Com” era is known for retail frenzy around early tech companies and wild surges in stock prices—especially in public markets—but few credit this boom to the earliest supporters of these new technologies: venture capitalists.

In the mid-1990s, venture capital was a small and relatively new form of investment, with only $7.6 billion in total capital deployed (less than 5% of the 2021 market size).

Even so, this small pool of capital ultimately became the lifeblood of a technological revolution, as nearly 70% of venture investments went to technology/internet companies, typically at later stages.

This trend did not stop; in the following years, venture capital activity grew significantly. From 1995 to 1999, investments by firms increased tenfold.

What happened next is unsurprising. Over the five years starting in 1995, publicly listed tech company stocks saw massive increases, with the top four companies delivering returns exceeding 10x—most of which coincided with fundraising peaks among the largest venture capital firms.

Not coincidentally, the most significant growth in the tech sector occurred during the era when private capital flooded into the industry. It was precisely this wave of capital that drove up public market valuations and helped establish the largest share of the U.S. economy.

This Time Is Different

To connect internet venture capital with crypto venture capital, we must identify similarities between these two markets—and more importantly, their differences—to understand the direct impact on crypto asset prices.

1) Similarities

Emerging Markets: The most obvious similarity lies in how closely aligned both industries and their underlying foundations are. In many ways, crypto represents an extension of the same core technologies built two decades ago. Similarly, both industries share a common group of early adopters, driven by passionate advocates during initial expansion phases and met with widespread skepticism regarding their long-term value.

Speculation: As previously mentioned, the early phase of the internet drew heavy attention from venture capitalists. Both industries share this trait, as the crypto sector has recently become a leader in venture capital deal flow. Historically, both sectors (in their respective eras) have been high-risk, high-reward relative to their valuations.

2) Differences

Regulatory Challenges: The financing mechanisms of crypto assets and their respective projects make the investment landscape vastly different, as investors often trade not for equity but for tokens—a clear distinction.

Beyond this, there are major differences in eligible asset classes. Only venture capitalists can invest, while traditional investors such as asset managers, mutual funds, and general stockholders cannot. Due to the ambiguity surrounding crypto investments, the broad base of investors currently able to actively participate in token and equity trading remains limited.

Shorter Liquidity Timelines: Founders, projects, and investors gaining liquidity faster alters the dynamics of funding cycles and the fundamental expectations around bets on crypto projects. Capital flows more freely, and it is this fluidity that fuels the development of new ventures within the ecosystem.

New Valuation Paradigms: The introduction of a new monetary system also changes fundraising mechanics, as projects, founders, and investors are compensated in tokens or in-kind contributions rather than cash. Additionally, protocol/project performance is often measured by token price rather than growth metrics due to stronger market liquidity and comparability.

Dedicated Followership: Founders and investors generally end up measuring their performance in Bitcoin or Ethereum as their base currency. Protocols that raise millions quickly and strive to become unicorns eventually retain employees paid in their base currency and continuously reinvest within the ecosystem. Concentration is extremely high.

Long Leverage

These differences lead to a strange correlation when venture capital firms seek to buy equity in crypto companies. When reviewing the historical growth rates of any major venture-backed crypto company, you’ll quickly notice that past projections directly reflect appreciation in crypto asset prices.

Consider this example:

A traditional venture firm/investor, "A+ Partners," is seeking investment opportunities in crypto. Unfortunately, they cannot purchase Bitcoin or Ethereum due to mandate restrictions, but they can invest in organizations focused on crypto. They choose to invest in a crypto exchange, so they must evaluate the organization’s revenue and future growth potential. For exchanges, nearly all revenue comes from trading activity. High trading volume depends almost entirely on high transaction volumes, which in turn depend almost entirely on high asset prices.

Applying this logic to forward-looking investments allows us to understand what top-tier venture capital groups envision for future crypto asset prices—even if they don’t plan to directly bet on cryptocurrencies. Even considering traditional firms that won’t invest in tokens, we can still grasp the underlying logic behind projected Bitcoin and Ethereum prices in the near term. In today’s crypto venture capital landscape, we can continue assessing funds raised through venture capital and use them to price investor expectations for crypto asset values.

Final Thoughts

Looking back at 25 years of investment history and the current red-hot venture market, we can infer a very interesting future for cryptocurrency. As we look ahead to future venture capital fundraising and new fund deployments, we must account for private investors’ implicit bets on the state of crypto asset prices and their views on where liquid markets are headed.

It’s safe to say the outlook for our industry is optimistic.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News