Bitget UEX Daily | US-Iran to hold next round of negotiations in Pakistan on July 11; Micron invests $9.3 billion to expand HBM factory in Hiroshima (July 06, 2026)

TechFlow Selected TechFlow Selected

Bitget UEX Daily | US-Iran to hold next round of negotiations in Pakistan on July 11; Micron invests $9.3 billion to expand HBM factory in Hiroshima (July 06, 2026)

Short-term volatility may increase, long-term bullish on AI and energy transition themes.

I. Hot News

Fed Dynamics

Fed Officials' Speeches and Policy Expectations

- Fed Governor Waller and other officials spoke today, with the market focusing on their latest statements on the interest rate path; combined with recent economic data, rate cut expectations remain but the pace is cautious.

- Institutional analysis shows that easing inflation and employment data provide room for policy adjustments. Market Impact: Speeches may reinforce short-term USD volatility and affect pricing of safe-haven assets such as gold.

International Commodities

Next Round of US-Iran Negotiations and OPEC+ Dynamics

- Saudi media reported that the US and Iran will hold the next round of negotiations in Pakistan on July 11, discussing sanctions, frozen funds, and nuclear issues; the Iranian delegation will be determined after Khamenei's funeral; OPEC+ decided to increase production by 188,000 barrels/day in August.

- Ships in the Oman shipping lane of the Strait of Hormuz decreased significantly, Iran strengthened control, and multiple ships turned back or changed routes. Market Impact: Geopolitical uncertainty supports short-term oil price volatility, while production increase plans may alleviate supply pressure, but actual execution is affected by shipping lanes, and safe-haven demand for precious metals may persist.

Macroeconomic Policy

Bank of Korea Warns of Leveraged ETF Risks

- The Bank of Korea warned that single-stock leveraged ETFs linked to Samsung and SK Hynix may exacerbate market concentration and volatility; South Korea is discussing regulatory measures today.

- Policy focuses on the risk of one-sided capital flows and amplified retail losses. Market Impact: Strengthened regulation may alleviate volatility in the semiconductor sector, but may affect trading enthusiasm for related stocks in the short term.

II. Market Review

Commodities & Forex Performance (Real-time Update)

- Spot Gold: 4,179 USD/oz, 24h Change +0.11%

- Spot Silver: 62.8 USD/oz, 24h Change +0.75%

- WTI Crude Oil: 68.32 USD/barrel, 24h Change -0.6%

- Brent Crude Oil: 71.55 USD/barrel, 24h Change -0.35%

- US Dollar Index (DXY): 100.88 points, 24h Change +0.02%

Driver Analysis: Geopolitical tension remains the core driver, with US-Iran negotiation prospects and the risk of shipping interruption in the Strait of Hormuz intertwined, leading to obstructed oil tanker transportation. Despite OPEC+ announcing production increases, actual supply recovery is slow, and oil prices show narrow oscillations. The US Dollar Index remains relatively stable, reflecting cautious Fed policy expectations, with inflation data and employment situation jointly shaping market judgment on the rate cut path. Gold and Silver as safe-haven assets benefit from uncertainty; institutions generally believe short-term correlation logic leans towards risk aversion, but if negotiations make progress, commodity prices may face correction pressure. Overall, asset correlations show macro policy and geopolitical factors dominate short-term trends; investors need to focus on the actual impact of shipping lane dynamics on energy supply.

Cryptocurrency Performance

- BTC: 63,745 USD, +1.2%

- ETH: 1,792 USD, +1.18%

- Total Cryptocurrency Market Cap: 2.26 trillion USD, 24h Change -0.55%

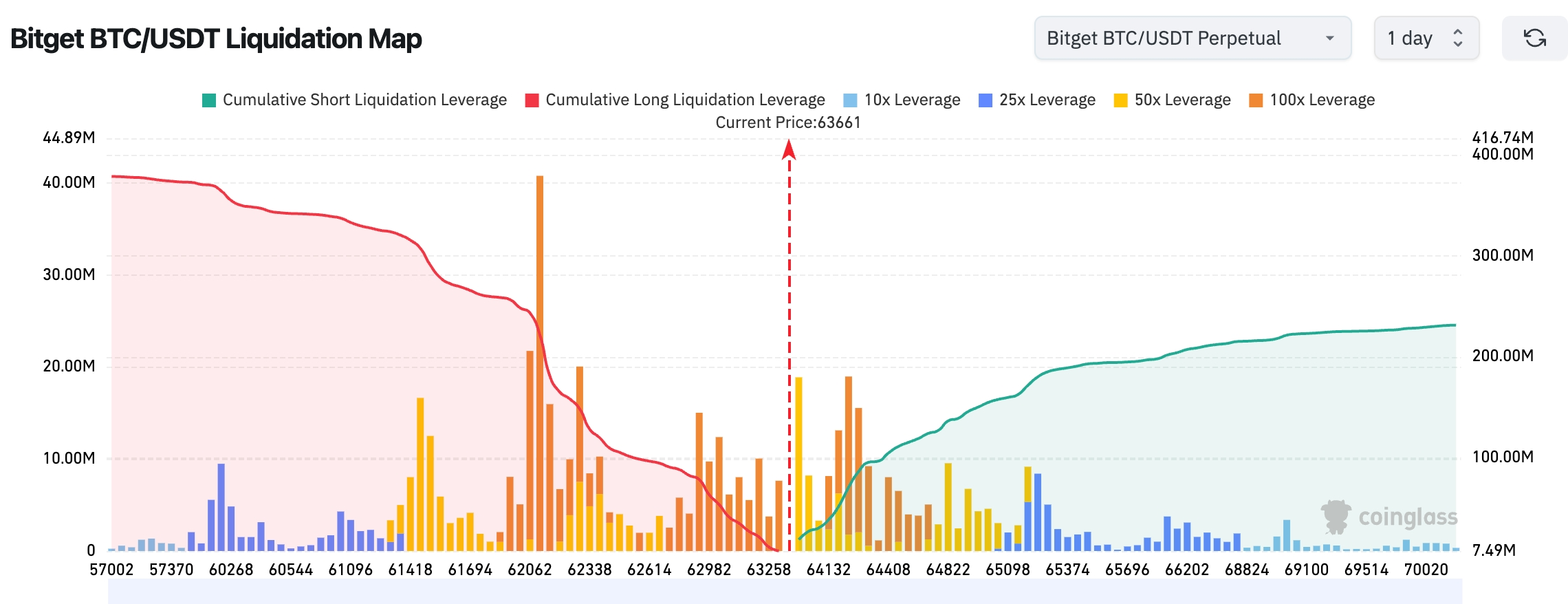

- Market Liquidation Status: 24h Total Liquidations 168 million USD, Short Liquidations 107 million USD

- Bitget BTC/USDT Liquidation Map: Near current price, major resistance above focuses on key integer levels, support below focuses on recent lows, leverage liquidation risk amplifies with volatility

Driver Analysis: Macro environment and geopolitical factors provide background support for the crypto market; US-Iran negotiation uncertainty coupled with Fed speech expectations drive cautious sentiment in risk assets. ETF capital flows show institutional interest persists, leverage liquidation data reflects market deleveraging amidst volatility. Technically, BTC and ETH show mild divergence, BTC dominance is stable while ETH lags relatively due to ecosystem events; institutional consensus believes AI and blockchain integration trends and policy signals will continue to shape medium-term trends, short-term need to guard against geopolitical events disturbing risk appetite. Overall trend leans towards oscillation, focus on capital inflows and liquidation map as short-term guidance.

US Stock Index Performance

- Dow Jones: 52,900.07 points, +1.14% (+594.83 points)

- S&P 500: 7,483.24 points, +0.01% (+0.01 points)

- Nasdaq: 25,832.67 points, -0.80% (-207.36 points)

Tech Giants Dynamics

- NVDA: 194.83 USD, -1.39%

- AAPL: 308.63 USD, +4.84%

- MSFT: 390.49 USD, +1.62%

- GOOGL: 359.91 USD, -0.36%

- AMZN: 242.67 USD, +0.40%

- META: 582.90 USD, -4.90%

- TSLA: 393.45 USD, -7.49%

- MU: 975.56 USD, -5.49%

- SPCX: 162.00 USD, +2.83%

The tech sector shows obvious differentiation characteristics: AAPL rebounded strongly (+4.84%), market interpretation relates to foldable iPhone product expectations; MSFT rose slightly, benefiting from continuous AI ecosystem layout. In contrast, TSLA (-7.49%) and META (-4.90%) corrected significantly, mainly affected by valuation pressure and short-term profit-taking. On the chip stock side, NVDA fell slightly, MU (-5.49%) faces short-term adjustment pressure despite Hiroshima expansion利好 (Wait, "利好" -> "positive news"). Despite Hiroshima expansion positive news. Futu Morning Report mentioned Micron expansion project and Samsung DRAM price increase expectations, further confirming the pulling effect of AI demand on the storage industry chain. Overall, AI core targets show relatively strong resilience, while high valuation or event-driven individual stocks show increased volatility, market rotation characteristics are significant.

Sector Movement Observation

Semiconductor/Memory Sector volatility is significant (sector intraday/short-term shows obvious differentiation, some individual stocks stand out under AI theme catalysis, but high base valuation and profit-taking pressure lead to increased overall volatility).

- Representative stocks: Micron Technology (MU) boosted by Hiroshima expansion positive news, latest closing price about 975.56 USD, daily change about -5.49% (repair signs appeared during trading after high pullback, trading volume active); SK Hynix and related dynamics continue to ferment, sector linkage effect is obvious.

- Drivers: AI large model training and inference computing power demand continues to explode, directly pushing HBM and other advanced storage chips into short supply. Micron Technology 9.3 billion USD (about 1.5 trillion JPY) Hiroshima factory expansion project officially launched, it is a key measure of its global capacity layout, expected HBM shipments will significantly increase in the second half of 2028; Japan Ministry of Economy, Trade and Industry provides up to 500 billion JPY subsidy, greatly lowering capital expenditure threshold, strengthening supply chain localization advantages. Coupled with Samsung Electronics having issued verbal notice to end customers that Q3 DRAM average selling price will increase 20% quarter-over-quarter, reflecting good upstream inventory digestion and enhanced bargaining power, price transmission is expected to support industry gross margin repair. SK Hynix promotes large-scale US IPO (potential scale about 29 billion USD), aiming to attract global AI-focused investors, further improving valuation anchoring and liquidity. Overall, industry capital expenditure and technology iteration are accelerating, AI infrastructure demand becomes core driver, but short-term still need to focus on valuation pressure and volatility risks brought by geopolitical factors.

III. In-depth Analysis of US Individual Stocks

1. Micron Technology (MU) - Hiroshima Expansion Project

Event Overview: Micron Technology officially launched the Japan Hiroshima factory expansion project, total investment about 9.3 billion USD (1.5 trillion JPY), focusing on producing high bandwidth memory chips including HBM. This project is an important part of its global expansion plan, aiming to meet strong demand for high-performance memory from AI industry, expected to start shipping HBM in the second half of 2028. Japan Ministry of Economy, Trade and Industry provides up to 500 billion JPY subsidy support. Micron CEO emphasized at the groundbreaking ceremony that the first batch of HBM wafers used for AI core storage technology will be manufactured in Hiroshima. Meanwhile, storage giants such as SK Hynix are also synchronously promoting expansion plans.

Market Interpretation: Institutions generally believe this significantly strengthens Micron's strategic position in the AI storage supply chain. HBM as a key component of NVIDIA and other AI accelerator processors, current global capacity is seriously in short supply. Micron through Japan localized production, can both obtain government subsidies to lower capital expenditure, and improve supply chain resilience and geopolitical diversification advantages. Combined with Samsung DRAM price increase expectations, industry is shifting from price competition to technology and capacity barrier competition, long-term growth certainty improves. But short-term still need to focus on HBM technology iteration pace and terminal demand landing situation.

Investment Implications: Focus on tracking AI capital expenditure cycle's continuous pulling on HBM demand, and Micron project production progress and customer certification progress.

2. Apple (AAPL) - Foldable Phone Supply Outlook

Event Overview: TF International Analyst Ming-Chi Kuo latest industry survey shows, Apple foldable iPhone assembly shipments in the second half of 2026 about 7-8 million units, among which Q3 shipments only 500,000-1 million units (accounting for about 10%). In contrast, iPhone 18 Pro/Pro Max simultaneous stock preparation volume reaches 20-22 million units. Ming-Chi Kuo judges, foldable iPhone likely to be released together with other models, but open pre-order and official sale time are both later, supply tension may continue until year-end, similar to 2017 iPhone X launch rhythm.

Market Interpretation: Market views this as an important signal of Apple hardware innovation cycle. Foldable form factor expected to open new growth space, although initial shipment scale is limited, but can consolidate Apple's differentiated positioning in high-end market. Supply chain verification and stock preparation rhythm will become key observation indicators, initial supply tension may instead strengthen product scarcity and brand premium.

Investment Implications: Focus on Apple product strategy details reshaping hardware cycle expectations, and supply chain verification and stock preparation data actual progress.

3. SK Hynix - US Listing Plan

Event Overview: SK Hynix plans to list in the US with about 29 billion USD scale, or will become one of the largest foreign company IPOs in history, aiming to attract global AI investors. Underwriting fee about 0.5%, issuance scale highest can reach 2.5% of issued shares. This move mainly targets international investors unable to directly enter South Korea market, providing convenient channel to participate in pure AI memory targets.

Market Interpretation: Institutions believe, under current AI boom background, US listing timing is favorable, can both improve company liquidity and valuation attractiveness, and directly dock with global largest scale AI capital. Institutional investors holding Micron stocks stated, market is in a period of extreme frenzy for chip stocks, this move helps SK Hynix obtain broader capital support in AI memory cycle.

Investment Implications: Global capital market docking will further strengthen semiconductor AI theme investment opportunities, suggest continuing to focus on issuance final scale and subscription enthusiasm.

4. Tesla (TSLA) - Employee AI Spending Limits

Event Overview: Tesla internal memo shows, from July 6, employee weekly spending limit on AI tools set at 200 USD, exceeding limit requires management approval. This move aims to balance AI application promotion and cost control, employee use of xAI's Grok model not counted into quota limit.

Market Interpretation: Market interprets as Tesla shifting from "casting a wide net" to "precise control" signal in AI investment. On one hand reflects company's emphasis on AI tool actual usage efficiency, on other hand also shows in rapid expansion AI application process, token-based costs have begun to produce pressure on operations. Institutions believe, this move short-term may affect part of AI experiment speed, but long-term helps resources concentrate on core projects, consistent with Tesla's AI strategic direction in robotics, autonomous driving and other fields.

Investment Implications: Focus on Tesla AI cost control measures' effect on internal efficiency improvement, and its resource allocation changes on xAI and proprietary AI models.

5. NVIDIA (NVDA) - Core Beneficiary of HBM Demand

Event Overview: With Micron Hiroshima expansion, SK Hynix expansion and Samsung DRAM price increase and other multiple events fermenting, NVIDIA as global AI accelerator leader, its demand for HBM becomes storage industry chain's most direct beneficiary. Multiple institutions predict, 2026 HBM market scale will grow significantly, NVIDIA supply locking and technology cooperation in HBM3E/HBM4 era continues to deepen.

Market Interpretation: Institutional view believes, HBM has become AI infrastructure's "new oil", Micron and SK Hynix expansion essentially is serving core customers such as NVIDIA. NVIDIA through deep binding with storage manufacturers, not only can guarantee key component supply, but also maintain leading advantage in technology roadmap. Although short-term stock price affected by overall tech sector volatility, but long-term AI capital expenditure trend unchanged, its core position in AI ecosystem remains solid.

Investment Implications: Focus on tracking HBM supply chain actual expansion progress and NVIDIA new generation platform (such as Rubin) demand landing situation for HBM, focus on its pricing power and ecosystem control in AI full stack.

IV. Market & Project Dynamics

1. "1011 Insider Whale" Representative Garrett Jin posted analysis pointing out, this week market structure shows obvious changes, AI industry chain internal capital is being redistributed, storage chip market阶段性 (Wait, "阶段性" -> "phase") phase top signs appear, Micron stock price met resistance near about 1,250 USD and fell back, although financial report performance stronger than expected, but stock price still fell on heavy volume, showing "weakening after good news realization" typical top characteristics, South Korea market's SK Hynix and Samsung Electronics similarly weakened, data shows near two months foreign capital has withdrawn from South Korea stock market over 100 trillion KRW (about 65 billion USD), real capital承接 (Wait, "承接" -> "承接" -> "taking over/support") direction is not small-mid cap AI concept stocks, but core cloud computing giants represented by Google, Microsoft, Amazon etc.

Garrett Jin believes, this round of capital migration behind logic is "Token Optimization Trend": with more and more simple tasks processed by low-cost models, value will gradually concentrate in cloud service layer, rather than base model layer, this also constitutes hyperscale cloud vendors' core moat.

2. Yesterday MicroStrategy Founder Michael Saylor again released Bitcoin Tracker related information. According to previous pattern, MicroStrategy always discloses Bitcoin increase information the day after relevant news is released.

4. Bitcoin News cited analyst @gaah_im reporting, Bitcoin Miner Cycle Pressure Composite Index has fallen to new low in 2026, entering historical "undervalued" interval. This indicator combines Puell Multiple and Reverse Miner Capitulation Index, both respectively measure miner income and cost dynamics, their synchronous signal historically has strong indicative significance for Bitcoin cycle bottoms. Previously this composite index synchronous collapse respectively appeared in 2015, 2018, 2020, 2022 and 2024 Bitcoin major bottoms nearby. This composite index previously only once touched 0.00 during 2015 capitulation period, at that time Bitcoin fell from about 300 USD to 160 USD within one week. This indicator in 2026重现 (Wait, "重现" -> "reappears") reappears similar behavior, marking miner pressure again reaches historical rare level.

5. Data shows, Meme coins proportion in altcoin market cap has fallen to 3.7%, lowest level since February 2024, holder count synchronously creates three-year new low. This proportion in November 2024 once exceeded 10%, thereafter continuously fell back.

6. CryptoQuant analyst Darkfost pointed out, Bitcoin Sharpe Ratio again touches extreme negative value area, fell below -20 then slightly rebounded. Sharpe Ratio used to measure investment risk and return relationship, negative value means relative to current return risk is higher, this matches Bitcoin consecutive third quarter closing down (latest quarter drop 16.1%).

From historical data view, such extremely pessimistic periods often last several weeks to several months, and correspond to new bottom building stage, subsequently welcome price restart. Analyst stated, data implies current is approaching this stage, but need to note this belongs to long time frame observation.

7. This week SK Hynix 29 billion USD listing in US stock market, may become largest foreign company initial stock issuance in history, but this is not only for raising funds. More key is, it hopes to compete in current global stock market's hottest field, namely memory chip field for AI computing. Synovus Trust Senior Portfolio Manager Daniel Morgan holding Micron stocks stated, market is in a period of extreme frenzy for chip stocks, now is good time to let US investors participate in your stocks. Thornburg Investment Management Portfolio Manager Zhou Di holding SK Hynix stocks stated, this issuance targets investors currently unable to enter South Korea stock market. SK Hynix listing on Nasdaq, provides investors direct, frictionless opportunity to participate in one of the most attractive pure targets in AI memory cycle.

V. Today's Market Calendar

Data Release Schedule

Important Event Preview

- Fed Governor Waller and others speak: 23:00 - Focus on interest rates and economic outlook.

- South Korea Single-Stock Leveraged ETF Regulation Discussion: Today - Focus on reviewing market volatility impact.

Institutional Views:

Well-known investment bank analysts generally believe, current market is in environment intertwined with geopolitical risk and policy expectations. US-Iran negotiation progress may alleviate part of energy supply concerns, but Strait of Hormuz tension still supports oil price and gold. US stocks aspect, tech sector differentiation continues, AI-driven expansion investment boosts semiconductor long-term prospects, while leveraged product regulation signals may affect emerging market volatility. Crypto market maintains resilience under ETF inflows and macro signal support, institutions suggest focusing on data release and officials' speeches guidance on risk appetite, overall maintain neutral to cautious configuration, prioritize defensive and high certainty growth assets. Short-term volatility may increase, long-term bullish on AI and energy transition themes.

Disclaimer: The above content is organized by AI search, manually verified and published, and does not constitute any investment advice. Data in the text inevitably contains deviations; please refer to real-time market data.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News