Bitget UEX Daily Report | Micron’s Earnings Beat Expectations, Boosting AI Sector; Oil Prices Retreat as Supply Concerns Ease; Trump’s Housing Bill Signing Delayed

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Micron’s Earnings Beat Expectations, Boosting AI Sector; Oil Prices Retreat as Supply Concerns Ease; Trump’s Housing Bill Signing Delayed

The overall market fluctuates amid the interplay of macroeconomic policies and geopolitical factors; investors are advised to focus on data validation and risk management.

I. Top News

Federal Reserve Updates The Federal Reserve’s annual stress test results show that all major banks passed successfully, clearing the way for increased stock buybacks and dividend payouts. The test assumed a severe recession scenario—including a 39% decline in commercial real estate prices, a 30% drop in residential property values, and unemployment rising to 10%. Despite absorbing over $708 billion in loan losses, banks maintained sufficient capital buffers. Market interpretation suggests this reinforces financial system resilience and helps stabilize investor confidence—but also reflects the Fed’s ongoing vigilance toward potential economic downside risks, which could influence future monetary policy paths.

International Commodities International crude oil futures declined sharply: Brent crude fell approximately 4.3% to around $73.74 per barrel, while WTI crude dropped roughly 3.9% to $70.34 per barrel—returning close to pre-Israel–Iran–U.S. conflict levels. Supply concerns eased as more tankers departed the Strait of Hormuz. Trump pressured oil companies to lower prices faster, warning of potential Department of Justice investigations if they failed to comply—further intensifying downward pressure on oil prices. In the near term, easing geopolitical tensions combined with expectations of supply recovery will continue suppressing oil prices.

Macroeconomic Policy Trump canceled his scheduled signing ceremony and press conference for the housing bill, stating he wants Congress to prioritize passage of the “Save America Act” instead. He emphasized that interest rate cuts are key to addressing housing affordability and stressed—drawing on his real estate experience—that monetary policy matters more than housing legislation. This shift underscores a reordering of policy priorities, potentially delaying initiatives to boost housing supply and exerting short-term psychological pressure on the real estate market.

II. Market Recap

Commodities & FX Performance (Real-Time Updates)

- Spot Gold: ~$4,003/oz, 24h change: -0.4%

- Spot Silver: ~$58/oz, 24h change: -4%

- WTI Crude: ~$70/bbl, 24h change: -0.5%

- Brent Crude: ~$73.4/bbl, 24h change: -0.5%

- U.S. Dollar Index (DXY): ~101.6, 24h change: +0.2%

Driver Analysis: Crude oil prices continued declining, driven by improved navigation through the Strait of Hormuz, easing supply concerns, and Trump-related comments—significantly reducing geopolitical risk premiums. As safe-haven assets, gold and silver faced concurrent pressure, while a modestly stronger dollar further diminished their appeal. Overall, macro-level Fed policy expectations and easing geopolitical tensions are interacting—imposing short-term adjustment pressure on commodities. However, if inflation data remains benign, precious metals may attract allocation at current lows. Institutions broadly expect oil prices to trade sideways within the current range in the near term, with attention focused on upcoming OPEC+ developments and the Fed’s interest-rate trajectory.

Cryptocurrency Performance

- BTC: $60,854, -3.17%

- ETH: $1,619, -3.01%

- Total Crypto Market Cap: ~$2.19 trillion, -2.4%

- Liquidations: ~$998 million liquidated in past 24h; long positions accounted for $799 million

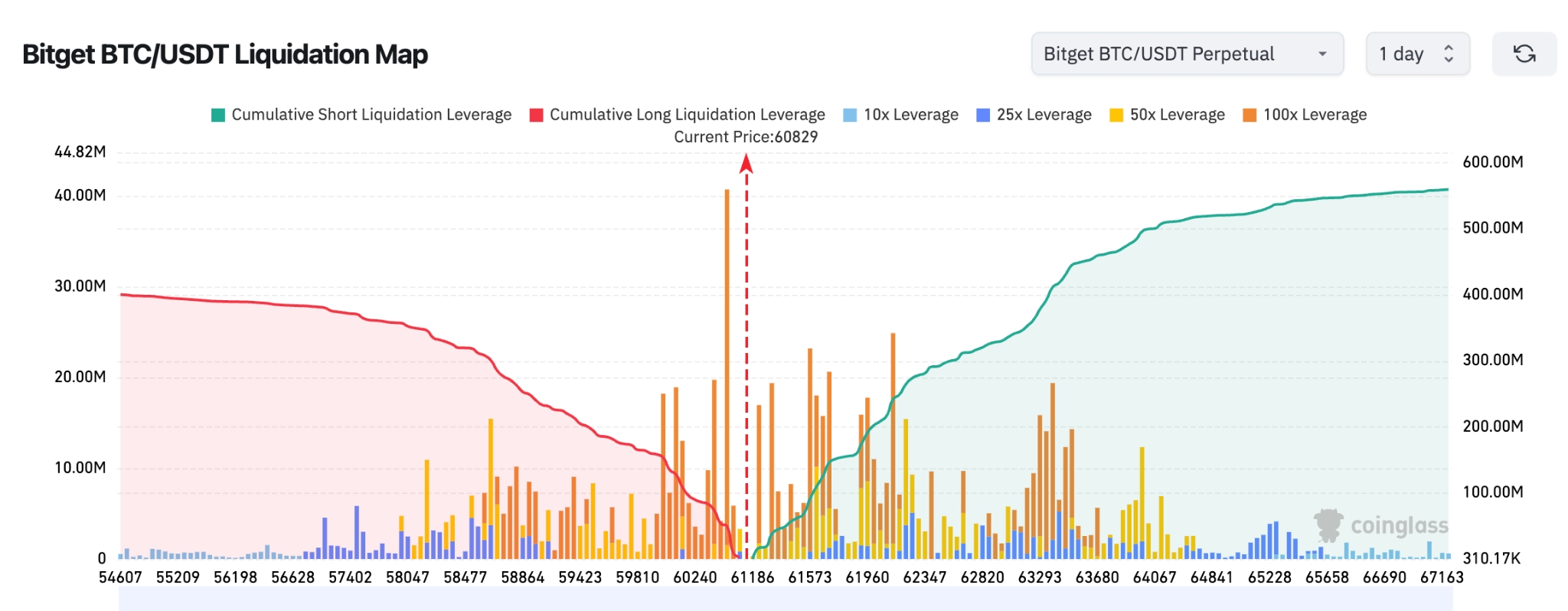

- Bitget BTC/USDT Liquidation Map: Current BTC price ~$60,829; long/short liquidations are relatively balanced near this level. However, significant short-liquidation leverage is concentrated in the $61,500–$63,500 zone above—potentially triggering cascading short-covering (“short squeeze”) if prices rise further. Major long-liquidation zones lie between $59,000–$60,200, with cumulative size notably smaller than overhead short-liquidation pressure. Overall, the map shows richer liquidity above and a structural bias toward upward price attraction in the short term.

- Spot ETF Net Flows: BTC spot ETFs saw net outflows of $17.78 million yesterday.

Driver Analysis: The crypto market was influenced by volatility in U.S. tech stocks and broader macro risk sentiment. BTC held key support but faced resistance. ETF fund flows showed phased net outflows, while leveraged liquidations amplified price swings. Micron’s earnings beat—highlighted in Futu Morning Brief—provided tailwinds for AI-themed assets, yet overall market performance remained constrained by dollar movement and risk appetite. Technically and fundamentally, BTC/ETH may diverge short-term; watch for macro data transmission effects on risk assets. Institutional views remain generally constructive on long-term AI infrastructure demand but caution against excessive leverage.

U.S. Equity Index Performance

- Dow Jones Industrial Average: ~51,849, +0.35%

- S&P 500: ~7,358, -0.1%

- Nasdaq Composite: ~25,477, -0.43%

Tech Giants’ Updates

- NVDA: ~$199, -0.52%

- AAPL: ~$293, -0.41%

- MSFT: ~$365, -2.27%

- GOOGL: ~$345, -0.24%

- AMZN: ~$233, -0.07%

- META: ~$557, -0.81%

- TSLA: ~$375, -1.59%

- SPCX: ~$154, -1.01%

Summary & Driver Analysis: U.S. equity indices posted mixed performance—Dow Jones relatively stable, Nasdaq under pressure—largely due to semiconductor stock corrections. Micron’s earnings significantly exceeded expectations and raised guidance, lifting after-hours sentiment and reinforcing AI optimism. However, some memory-related names still adjusted. Jensen Huang emphasized during the shareholder meeting that AI has entered its monetization era, strengthening long-term bullish sentiment around the “AI factory” concept. Stock-level divergence was pronounced: AI infrastructure demand drove strength in certain names, while event-specific or valuation pressures caused underperformance elsewhere. Overall, the tech sector seeks balance amid macro uncertainty—with AI remaining the dominant narrative.

Sector Movement Observations Semiconductor-related sectors reacted diversely to Micron’s earnings catalyst: some stocks rebounded strongly. Micron surged notably after hours—driven by robust AI memory demand and upgraded guidance. Korea’s KOSPI index rose sharply, with SK Hynix and peers leading gains—reflecting global memory supply-chain linkages.

III. Deep Dives: U.S. Equities

1. Micron Technology (MU) – Earnings Beat Strongly Validates AI Memory Demand

Event Summary: Micron reported Q3 FY2026 results with revenue of $4.146 billion (well above consensus of ~$3.57 billion), adjusted EPS of $25.11 (far exceeding consensus of $20.50), and gross margin of 84.9%. Data center business hit a record, up 346% YoY—primarily driven by tight supply of high-bandwidth memory (HBM). CEO Sanjay Mehrotra underscored the strategic centrality of memory chips in the AI era and noted the high stability of long-term agreements with key customers. Management simultaneously raised Q4 guidance: revenue of $4.9–5.1 billion (±$100 million), adjusted EPS of ~$31—both substantially above analyst consensus.

Market Interpretation: Bank of America Securities and other institutions swiftly raised price targets to $1,500. Markets now hold an optimistic outlook extending AI-related memory demand visibility into 2027–2028. Post-earnings, shares surged nearly 15% after-hours to ~$1,205—adding over $120 billion in market cap in one day—fully reflecting market repricing of genuine AI infrastructure demand. Strong results and guidance confirmed HBM’s irreplaceable role in AI training and inference, alleviating prior concerns about supply chain bottlenecks and demand peaks—and highlighting the strong correlation between memory cycles and AI capex.

Investment Implications: This earnings beat serves as a powerful catalyst for the AI memory theme. Short-term price action is highly responsive to sentiment—suitable for traders seeking momentum opportunities. Longer-term, validated AI demand resilience warrants monitoring of quarterly HBM market share gains, sustained gross margins, and industry-wide inventory health. Should the semiconductor sector correct, it may present a high-conviction growth-allocation window—but macro interest-rate and geopolitical factors affecting capex timing warrant caution.

2. TSLA – Analysts Raise Delivery Forecasts Amid Persistent Volatility

Event Summary: Baird analysts raised Tesla’s Q2 delivery forecast to ~392,900 units and maintained full-year 2026 delivery guidance of 1.68 million units. They reiterated an “Outperform” rating and $522 price target. Market attention also centered on rumored strategic merger discussions between Tesla and SpaceX—potentially occurring within 12–18 months.

Market Interpretation: As a high-market-cap (~$1.4 trillion) growth stock, Tesla’s price remains highly sensitive to delivery figures, Robotaxi progress, and developments involving Elon Musk’s affiliated companies—recently amplifying intraday and overnight volatility. Optimistic analyst forecasts and merger narratives provide support, yet intensifying EV competition, macro interest-rate conditions, and shifts in sector-wide risk appetite continue driving sharp price swings.

Investment Implications: Suitable for investors with higher risk tolerance. Focus on delivery metrics and FSD/Robotaxi catalysts. High volatility presents both opportunity and risk—participation should integrate technical analysis and disciplined position sizing.

3. NVDA / Semiconductor Sector Representative – Industry Rumors Drive Elevated Volatility

Event Summary: Semiconductor leaders—including NVIDIA—corrected noticeably amid rumors about memory chips (e.g., SK Hynix slowing HBM expansion). Intraday volatility spiked across the sector, with large-cap names (e.g., NVDA’s >$4 trillion market cap) becoming focal points for capital flow.

Market Interpretation: While the long-term AI demand thesis remains solid, near-term uncertainty around supply-demand timing triggered profit-taking and leveraged swings—particularly among high-beta semiconductor stocks highly sensitive to sentiment shifts.

Investment Implications: Large-cap tech growth stocks tend to exhibit heightened volatility during earnings season and amid supply-chain news. Suitable for swing trading or as satellite allocations within core portfolios—consider sector rotation opportunities following validation from Micron’s earnings.

IV. Project & Market Updates

1. According to The Block, Bitcoin miner revenues continue declining—the 7-day moving average has fallen to ~$30 million/day, down from over $50 million/day last summer. Transaction fee contributions have become negligible—under $250,000/day. BTC’s current trading price (~$62,500) remains well below JPMorgan’s estimated production cost of ~$78,000—a gap persisting for five months—the longest in this cycle. Production cost has historically acted as a soft price floor; currently, ~20% of miners operate at a loss.

Network-level strain is emerging. Over the past six months, mining difficulty’s beta to BTC price has risen to 0.62—high-cost miners now toggle operations on/off based on price rather than running continuously at a loss. Difficulty dropped 10% in the second week of June—the second such magnitude decline this year. Publicly listed mining firms sold over 32,000 BTC in Q1 to cover operating costs—notably avoiding further capacity reductions.

2. On June 24 local time, Micron Technology released its third-quarter fiscal 2026 results ending May 28, 2026: Revenue totaled $4.146 billion (vs. $2.386 billion last quarter and $0.93 billion YoY); GAAP net income was $28.24 billion, with diluted EPS of $24.67; operating cash flow reached $25.39 billion (vs. $11.9 billion last quarter and $4.61 billion YoY). The company projects Q4 revenue of $4.9–5.1 billion and adjusted EPS of $30–32.

3. U.S. President Trump refused to sign the bipartisan housing bill—which included a four-year ban on a U.S. Central Bank Digital Currency (CBDC)—and temporarily canceled the planned signing ceremony. He demanded Congress first pass his priority “Save America ACT” election bill. The housing bill’s CBDC provision would prohibit the Fed from issuing a digital dollar before 2030—a development previously viewed by the crypto industry as a meaningful milestone.

4. Standard Chartered initiated coverage of decentralized lending protocol Aave, assigning the AAVE token a $3,500 target price by end-2030—roughly 50x its current ~$70 level. The report notes Aave’s yield correlates linearly with deposit volume. Following the KelpDAO exploit, Aave deposits fell from $44 billion to $23 billion and loans dropped from $18 billion to $9.5 billion—now considered a “bottom.” The bank forecasts total active assets in DeFi will grow to ~$2.7 trillion by 2030—37x current levels—primarily driven by stablecoin and real-world asset (RWA) tokenization. It expresses strong conviction in Aave Horizon’s permissioned RWA lending market and the long-term growth potential from GHO stablecoin fees accruing entirely to the protocol.

5. OpenAI and Broadcom jointly unveiled Jalapeño—their first AI chip optimized for large language models (LLMs). Broadcom’s CEO stated the chip reduces model inference costs by ~50% and may enable faster-than-expected large-scale deployment. Meanwhile, Broadcom expects to launch gigawatt-scale data centers with Microsoft and partners in 2026 to meet next-generation AI compute demand. Upon announcement, Broadcom’s pre-market share price rose ~3%.

V. Market Calendar

June 25 (Thursday)

- U.S. Economic Data: May PCE Price Index (Fed’s preferred inflation gauge; core PCE MoM forecast: +0.3%); Q1 GDP Final Estimate (forecast unchanged at 1.6%); Durable Goods Orders, Initial Jobless Claims, etc. (data-heavy day). ★★★★

- U.S. Earnings: BlackBerry (BB) earnings pre-market

June 26 (Friday)

- U.S. Economic Data: University of Michigan Consumer Sentiment Final Reading; Fed official speeches (Williams, Kashkari, etc.)

Institutional Views: Leading investment banks widely view Micron’s earnings beat as a confidence booster for both the semiconductor and AI sectors—robust memory demand is expected to sustain related equities. Falling oil prices reflect easing geopolitics, suggesting near-term oil prices may remain range-bound at lower levels. Though crypto markets face correction, AI themes and institutional long-term positioning provide underlying support. Amid intertwined macro-policy and geopolitical dynamics, markets remain volatile—focus is advised on data validation and risk management. Wall Street banks’ successful stress tests also bolstered financial sector stability.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute any investment advice. Data herein may contain unavoidable inaccuracies; please rely on real-time market data for decision-making.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News